Ripe for Change: Ending Human Suffering in Supermarket Supply

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hypermarket Lessons for New Zealand a Report to the Commerce Commission of New Zealand

Hypermarket lessons for New Zealand A report to the Commerce Commission of New Zealand September 2007 Coriolis Research Ltd. is a strategic market research firm founded in 1997 and based in Auckland, New Zealand. Coriolis primarily works with clients in the food and fast moving consumer goods supply chain, from primary producers to retailers. In addition to working with clients, Coriolis regularly produces reports on current industry topics. The coriolis force, named for French physicist Gaspard Coriolis (1792-1843), may be seen on a large scale in the movement of winds and ocean currents on the rotating earth. It dominates weather patterns, producing the counterclockwise flow observed around low-pressure zones in the Northern Hemisphere and the clockwise flow around such zones in the Southern Hemisphere. It is the result of a centripetal force on a mass moving with a velocity radially outward in a rotating plane. In market research it means understanding the big picture before you get into the details. PO BOX 10 202, Mt. Eden, Auckland 1030, New Zealand Tel: +64 9 623 1848; Fax: +64 9 353 1515; email: [email protected] www.coriolisresearch.com PROJECT BACKGROUND This project has the following background − In June of 2006, Coriolis research published a company newsletter (Chart Watch Q2 2006): − see http://www.coriolisresearch.com/newsletter/coriolis_chartwatch_2006Q2.html − This discussed the planned opening of the first The Warehouse Extra hypermarket in New Zealand; a follow up Part 2 was published following the opening of the store. This newsletter was targeted at our client base (FMCG manufacturers and retailers in New Zealand). -

Iacarrefoura2000ieng.Pdf

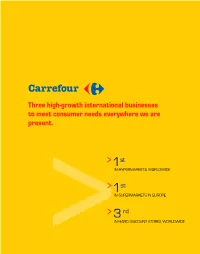

Three high-growth international businesses to meet consumer needs everywhere we are present. > 1st IN HYPERMARKETS WORLDWIDE > 1st IN SUPERMARKETS IN EUROPE > 3 rd >IN HARD DISCOUNT STORES WORLDWIDE MESSAGEMESSAGE FROM THE CHAIRMAN > At the end of January, the European Commission cleared our mer- ger with Promodès. We decided on the rapid consolidation of all our hyper- markets under the Carrefour trade name, and all our supermarkets under a common trade name in each country. > In 87 hypermarkets and 490 supermarkets in France, and 117 hypermarkets and 109 supermarkets in Spain, Italy, Greece, Turkey, Indonesia, China and Korea, the current teams in Continent, Pryca, Continente, Euromercato, Stoc, Maxor and Supeco stores transform- ed those stores and reopened under the Carrefour or Champion name by the end of the year (January in Italy). > This was a major undertaking since the changes involved more than the name of the store or shelf displays. The changes meant train- ing men and women in new working methods and harmonizing product lines. Inevitably, this effort resulted in some disruption, which explains the year-end drop or slowdown in sales revenue in France and Spain. Sometimes custo- mers could not immediately find products in their usual place, sometimes products were not available in the store for short periods due to system changes. In the first half of 2001, all these stores should steadily return to normal operating conditions. > We plan to continue these changes in other countries. In Belgium, 60 hypermarkets will transfer to the Carrefour trade name by the end of 2001. In France and Spain, we will continue to make progress in pooling logistics, creating synergies over the long term. -

Carrefour Group, Building RELATIONSHIPS a L R EPO RT

2007 ANNUAL REPORT CARREFOUR GROUP, BUILDIng RELATIONSHIPS RT EPO R L A U ANN Carrefour SA with capital of 1,762,256,790 euros 2007 RCS Nanterre 652 014 051 www.groupecarrefour.com N°1 in Europe 30 countries N°2 worldwide OTHERS PUBLICATIONS: RAPPORT DÉVELOPPEMENT DURABLE 2007 102.442 billion euros in sales carrEFOUR carrEFOUR incl. tax under GROUP GROUP Group banners 16,899,020 sq.m sales area BUILDING FInancIAL RESPOnsIBLE REPORT RELATIONSHIPS 2007 490,042 employees 2007 Sustainability Report 2007 Financial Report stores More than 3 billion cash 14,991 transactions per year YOU CAN FIND THE LATEST CARREFOUR GROUP NEWS AND THE INTERACTIVE ANNUAL REPORT AT WWW.GROUPECARREFOUR.COM Design, copywriting and production: Translation: Photocredits: Carrefour Photo Library, Lionel Barbe, Christophe Gay/Skyzone, Nicolas Landemard, Gilles Leimdorfer/Rapho, Jean-Erick Pasquier/Rapho, Michel Labelle, all rights reserved - p. 2-3: Getty Images/Bruno Morandi - p. 4-5: Getty Images/ Hans Neleman - p. 6-7: Getty Images/Lonely Planet Images/Krzysztof Dydynski - p. 8-9: Getty Images/Daly & Newton - p. 16: Getty Images/Shannon Fagan - p. 24: Getty Images/Daly & Newton - p. 32: Getty Images/Frank Herholdt - p. 36: Corbis/Beathan - p. 38: Getty Images/fStop - p. 39: Getty Images/Darryl Estrine - p. 40: Corbis/Jose Luis Pelaez - p. 41: Getty Images/Somos/Veer - p. 42: Getty Images/Floresco Images - p. 45: Getty Images/Dimitri Vervitsiotis. CARREFOUR / ATACADAO / CARREFOUR EXPRESS / CARREFOUR BAIRRO / CARREFOUR CITY / CARREFOUR MARKET / 5 MINUT CARREFOUR / Paper: the Carrefour group is committed to the responsible management of its paper sourcing. The paper used for this document is certified PEFC (Programme for the Endorsement of Forest Certification schemes). -

Nielsen QBN Europe Q4 2017

EUROPE QUARTER BY NUMBERS Q4 2017 1 Copyright © 2017 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute. Copyright © 2017 The Nielsen Company CONTENTS SECTION 1 THE BIG PICTURE: EUROPE WEST Message from Olivier Deschamps…………………..…………………….………03 EUROPE AT A GLANCE Key economic drivers………………………………………………………….……04 Looking through Europe West FMCG lens………………………………...……06 COUNTRY SNAPSHOT Belgium……….………………………………………….…………………………..07 France……….………………………………………..….…………………………..10 Germany……….……………………………………..….…………………………..13 Italy……………………………………………………….…………………………..16 Netherlands..….…………………………………….……………….………………19 Portugal……….……………………………………..………………….……………22 Spain………………………………………………………………….………………25 United Kingdom.……………….…………………………………….………………28 IN THE INDUSTRY Retail Channel Universe Update……...………………………..…………………93 2 Copyright © 2018 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute. THE BIG PICTURE: EUROPE WEST Welcome to the first edition of Europe Quarter by Numbers that includes key Western European markets for Q4 2017, complimenting the view of Central and East Europe already in place. Our ambition is to provide context and insight into how broader macroeconomic factors are influencing consumer sentiment and spending patterns in the retail scene. After tough times in the last few years, 2017 showed a dynamic economic environment across Europe, with positive consumer confidence in the region reaching some of the highest levels seen for some time. While nations can draw similarities among the positive impacts on Olivier Deschamps consumer sentiment, Europeans diverge in the national issues of greatest concern - terrorism Retail Services Lead Markets remains high on the list and health is definitely a key priority with countries like Portugal showing notable peaks. Encouraged by lower risk of terrorism and better economic conditions, tourists flocked to the region in 2017 (+8%), particularly in Mediterranean countries. France was still the number one global tourist destination and Spain is about to exceed USA. -

The Benelux Food Retail Market Retail Foods Netherlands

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 6/25/2012 GAIN Report Number: NL2014 Netherlands Retail Foods The Benelux Food Retail Market Approved By: Mary Ellen Smith Prepared By: Marcel Pinckaers Report Highlights: The turnover of the Benelux food retail industry for 2011 is estimated at € 56.3 billion. For 2012, turnover is expected to increase by 2.5 percent. The retail market is fairly consolidated. Top 3 food retailers in the Netherlands have a market share of 64 percent while in Belgium the leading 3 retailers have 72 percent of the market. Sustainable food (including organic products) is one of the most important growth markets in food retail. The market share for private label products continues to go up in both Belgium and the Netherlands. The demand for convenient, healthy and new innovative products continues to be strong. Post: The Hague SECTION I. MARKET SUMMARY Benelux Food Retail Market Approximately 80 percent of the Dutch food retail outlets are full service supermarkets, operating on floor space between 500 and 1,500 square meters located downtown and in residential areas. Retailers with full service supermarkets have responded to the need of the Dutch to have these supermarkets close to their house. The remaining 20 percent includes mainly convenience stores (near office buildings and train/metro stations), some wholesalers and just a few superstores (convenient located alongside highways in shopping malls and industrial parks). The Belgians show a different shopping pattern. -

Retail Supermarket Globalization: Who’S Winning?

RETAIL SUPERMARKET GLOBALIZATION: WHO’S WINNING? October 2001 CORIOLISRESEARCH Coriolis Research Ltd. is a strategic market research firm founded in 1997 and based in Auckland, New Zealand. Coriolis primarily works with clients in the food and fast moving consumer goods supply chain, from primary producers to retailers. In addition to working with clients, Coriolis regularly produces reports on current industry topics. Recent reports have included an analysis of the impact of the arrival of the German supermarket chain Aldi in Australia, answering the question: “Will selling groceries over the internet ever work?,” and this analysis of retail supermarket globalization. ! The lead researcher on this report was Tim Morris, one of the founding partners of Coriolis Research. Tim graduated from Cornell University in New York with a degree in Agricultural Economics, with a specialisation in Food Industry Management. Tim has worked for a number of international retailers and manufacturers, including Nestlé, Dreyer’s Ice Cream, Kraft/General Foods, Safeway and Woolworths New Zealand. Before helping to found Coriolis Research, Tim was a consultant for Swander Pace (now part of Kurt Salmon) in San Francisco, where he worked on management consulting and acquisition projects for clients including Danone, Heinz, Bestfoods and ConAgra. ! The coriolis force, named for French physicist Gaspard Coriolis (1792-1843), may be seen on a large scale in the movement of winds and ocean currents on the rotating earth. It dominates weather patterns, producing the counterclockwise flow observed around low- pressure zones in the Northern Hemisphere and the clockwise flow around such zones in the Southern Hemisphere. It is the result of a centripetal force on a mass moving with a velocity radially outward in a rotating plane. -

Carrefour-RA2001-GB.Qxd

Annual report 2001 Annual report 2001 Our customers come first Société anonyme with share capital of ¤ 1 777 889 635 Head Office: 6, avenue Raymond Poincaré – 75016 Paris – France Postal Address: BP 419.16 – 75769 Paris Cedex 16 – France Tel.: 33 (0)1 53 70 19 00 / Fax: 33 (0)1 53 70 86 16 www.carrefour.com Profil The world's second largest food retailer, Carrefour operates over 9,000 stores in 30 countries. The Group is recognized for its expertise in three major food retail formats: hypermarkets, supermarkets and hard discount stores. It is also developing convenience and cash & carry stores in some countries. Thanks to the complementary elements of its different store formats, the Group can meet the consumer needs of all its customers. As the leading European food retailer, Carrefour has carved out strong strategic positions in two regions with high growth potential: Latin America, where the Group is the leader in modern food retail, and Asia, where it was the first international retailer to establish a presence. In 2001, Carrefour posted consolidated sales of ¤ 69.5 billion (51% from international business) and net income from recurring operations of ¤ 1.2 billion. As of December 31, Carrefour had a total workforce of 383,000 worldwide. Overview of the Group 2 Interview with Daniel Bernard 4 Management 6 Financial Highlights 8 Shareholder information 10 AN INTERNATIONAL GROUP STREAMLINED FOR SUCCESS The power of its store networks 14 A sense for business 16 A sense of our customers 18 Mobilizing our talents 20 A commitment to -

Carrefour Registration Document

Registration Document Annual Financial Report 2016 REGISTRATION DOCUMENT 2016 Annual Financial Report 1 5 Presentation of Carrefour 7 Consolidated Financial Statements as of December 31, 2016 169 1.1 History of Carrefour 8 1.2 Presentation of Carrefour 12 5.1 Consolidated income statement 170 1.3 Carrefour in 2016 20 5.2 Consolidated statement of comprehensive income 171 5.3 Consolidated statement of financial position 172 5.4 Consolidated statement of cash flows 174 2 5.5 Consolidated statement of changes Corporate social responsibility 27 in shareholders’ equity 176 5.6 Notes to the Consolidated Financial Statements 177 2.1 CSR at Carrefour 28 5.7 Statutory Auditors’ report on the Consolidated 2.2 Carrefour’s CSR performance 36 Financial Statements 245 2.3 Action plans 38 2.4 Carrefour CSR results 76 6 Company Financial Statements 3 as of December 31, 2016 247 Corporate governance 93 6.1 Balance Sheet at December 31, 2016 248 3.1 Corporate governance code 94 6.2 Income statement for the year 3.2 Composition and operation of the Board of ended December 31, 2016 249 Directors 94 6.3 Statement of cash flows 250 3.3 Executive Management 114 6.4 Notes to the Company Financial Statements 251 3.4 Compensation and benefits granted to Company officers 117 6.5 Statutory Auditors’ report on the Annual Financial Statements 267 3.5 Risk management 128 3.6 Internal control and risk management procedure 138 3.7 Statutory Auditors’ report prepared in 7 accordance with Article L. 225-235 of the Information about the Company 269 French commercial code -

Download (7Mb)

r::: ·-..0 .c::l ·-I.. ..tn ·-c The EC distribution sector is undergoing considerable restructuring. Changes include concentration, reduction in the number of traditional wholesalers, transformations c: in the retail sector and a tendency towards 0 ·-~ diversification and internationalisation. :::J Moreover, the future of the distributive sector will be ..a influenced by the achievement of the internal market ·-1.. and the opening-up of Eastern Europe. ~tn The Economic •!• wholesale distribution (NACE 61 ), defined ·-c importance of the as "units exclusively or primarily engaged industry in the EC in the resale of goods in their own name economy to retailers or other wholesalers, to manu- In analysing the overall importance of the facturers and others for further process- sector within the economy, the major pro- ing, to professional users, including craft- blems are those of definition and of adequ- smen, or to other major users." ate statistics. The definition issue is chiefly •!• retail distribution (NACE 64 and 65) , due to the fact that the divisions between defined as the distribution to final con- the sub-sectors concerned (manufacturers, sumers of wholesalers, transporters, agents, retailers) - food, drink and tobacco; are becoming less clear. These actors are - dispensing chemicals; tending to overlap, and the fact that manu- - medical goods, cosmetics and cleaning facturers or transporters are fulfilling roles materials; which were typically those of wholesalers - clothing ; means that this activity is not recorded in - footwear and leather goods; the official NACE statistics for th is sector. - furnishing fabrics and other household tex- This consequent lack of reliable statistics tiles; makes it difficult to assess the value of - household equipment, fittings, appliances, the sector in the Community economy. -

In-Store Case Studies

In-store Case Studies Business as a Force for Good in Times of a Crisis Collaboration for Healthier Lives The Coalition of Action’s response to Covid-19 Best practices from CGF members and stakeholders classified by category: • Employees • Digital & on line • In store • In communities • Vulnerable populations • Local businesses • Healthcare organizations • General Public This pack contains the In Store case studies In store Company list Ahold Delhaize Carrefour 6 Grupo Exito 4 Migros Ticaret 3 Russian retailers Tesco Walgreens 2 Ahold Delhaize 2 Carrefour 7 Grupo Exito 5 Migros Ticaret 4 Smurfit Kappa Tesco 2 Walmart Aldi Carulla Grupo Exito 6 Migros Ticaret 5 Spar Tesco 3 Walmart 2 Aldi 2 Continente Grupo Exito 7 Migros Ticaret 6 Spar 2 Tesco 4 Walmart 3 Aldi 3 Coop JD.com Migros Ticaret 7 Spar 3 Tesco 5 Walmart 4 Aldi 4 Costco Jeronimo Martins Migros Ticaret 8 Spar 4 The Giant Co. Walmart 5 Alibaba Dia % Johnson & Johnson Migros Ticaret 9 Spar 5 Tilda Walmart 6 Amazon Ebro Jumbo Migros Ticaret 10 Spar 6 Tyson Whole Foods Amazon 2 Ebro 2 Kesco Morrisons Spar 7 UK retailers Whole Foods 2 Amazon 3 E-Leclerc Konzum Musgrave Spar 8 UK retailers 2 Whole Foods 3 Asda Eurocash Lala New Hope Liuhe Spar 9 Us retailers Woolworths Auto mercado FairPrice Lawson PEFC Spar 10 Us retailers 2 Woolworths 2 Carrefour FairPrice 2 Leon Pepsico Spar 11 Us retailers 3 Woolworths 3 Carrefour 2 Franprix & Monoprix Loblaw Perifem Sainsbury’s Vermont Deli X5 Retail Group Carrefour 3 Grupo Exito Lush PicknPay St. Hubert Vkusvill X5 Retail Group 2 Carrefour 4 Grupo -

Ending Human Suffering in Supermarket Supply Chains

RIPE FOR CHANGE ENDING HUMAN SUFFERING IN SUPERMARKET SUPPLY CHAINS .........................REPORT © Oxfam International June 2018 This paper was written by Robin Willoughby and Tim Gore. Oxfam acknowledges the assistance of Ajmal Abdulsamad, Evelyn Astor, Sabita Banerji, the Bureau for the Appraisal of Social Impacts for Citizen Information (BASIC), Derk Byvanck, Man‑Kwun Chan, Celine Charveriat, Lies Craeynest, Anouk Franck, Gary Gereffi, Sloane Hamilton, Franziska Humbert, Steve Jennings, Peter McAllister, Rashmi Mistry, Eric Munoz, Ed Pomfret, Fenella Porter, Art Prapha, Laura Raven, Olivier de Schutter, Ruth Segal, Kaori Shigiya, Matthew Spencer, Dannielle Taaffe, Emma Wadley and Rachel Wilshaw. For further information on the issues raised in this paper please email [email protected] This publication is copyright but the text may be used free of charge for the purposes of advocacy, campaigning, education, and research, provided that the source is acknowledged in full. The copyright holder requests that all such use be registered with them for impact assessment purposes. For copying in any other circumstances, or for re‑use in other publications, or for translation or adaptation, permission must be secured and a fee may be charged. Email [email protected] The information in this publication is correct at the time of going to press. Published by Oxfam GB for Oxfam International under ISBN 978‑1‑78748‑178‑7 in June 2018. DOI: 10.21201/2017.1787 Oxfam GB, Oxfam House, John Smith Drive, Cowley, Oxford, OX4 2JY, UK Cover photo: Mu is 29 and the mother of three children, all of whom are back at home in Myanmar. She is a shrimp peeler in Thailand earning a daily rate of 310 THB, or about $9.30, plus overtime. -

Innovation and Efficiency of European Retail. Best Examples Innovation and Efficiency of Preliminary Schedule European Retail

WWW.FFORWARD.BIZ INNOVATION AND EFFICIENCY OF EUROPEAN RETAIL. BEST EXAMPLES INNOVATION AND EFFICIENCY OF PRELIMINARY SCHEDULE EUROPEAN RETAIL. BEST EXAMPLES Preliminary Schedule of “Innovation and Efficiency of European Retail. Best Examples” Management Tour* * Please be advised: 1) Under certain circumstances, the schedule may be changed (in case of force majeure). If a visit to a certain company cannot be carried out, tour organizers will arrange a meeting at an equally prominent company in the same field. 2) When drawing up the schedule, tour participants’ requests and objectives are taken into account. Some visits are included in the schedule based on organizing company’s long-term experience.3) All the visits are interactive; the guiding expert will be happy to answer any questions the tour participants may have. 2 WWW.FFORWARD.BIZ INNOVATION AND EFFICIENCY OF EUROPEAN RETAIL. BEST EXAMPLES PRELIMINARY SCHEDULE SUNDAY MONDAY Arrival. 7:00-8:00 11:00-14:00 Breakfast at the hotel. Visit to Tesco Extra Wembley. https://www.tesco.com/ 8:00-9:00 Official welcome and tour overview. Getting acquainted and discussing the tour. 9:00-11:00 Visit to Whole Foods www.wholefoodsmarket.com Whole Foods is an American retail chain, which owns 460 grocery stores in the US, Canada, and Great Britain. There are nine Whole Foods stores in the United Kingdom, seven of which are in London. The first store opened in June Welcome to Great Britain! The group arrives at Heathrow 2007 had a total area of 7,400 m2. Whole Foods sells primarily natural and Airport and is then transferred to a hotel.