Carrefour Group Building Responsible Relationships No.1 in Europe

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Décision N° 18-DCC-65 Du 27 Avril 2018 Relative À La Prise De Contrôle

RÉPUBLIQUE FRANÇAISE Décision n° 18-DCC-65 du 27 avril 2018 relative à la prise de contrôle exclusif des sociétés Zormat, Les Chênes et Puech Eco par la société Carrefour Supermarchés France L’Autorité de la concurrence, Vu le dossier de notification adressé complet au service des concentrations le 15 mars 2018, relatif à la prise de contrôle exclusif des sociétés Zormat, Les Chênes et Puech Eco par la société Carrefour Supermarchés France, et formalisée par un protocole de cession en date du 1er février 2018 ; Vu le livre IV du code de commerce relatif à la liberté des prix et de la concurrence, et notamment ses articles L. 430-1 à L. 430-7 ; Vu les engagements présentés les 15 mars et 18 avril 2018 par la partie notifiante ; Vu les éléments complémentaires transmis par la partie notifiante au cours de l’instruction ; Adopte la décision suivante : I. Les entreprises concernées et l’opération 1. La société Carrefour Supermarchés France SAS (ci-après « CSF ») est une filiale à 100 % du groupe Carrefour, lequel est actif dans le secteur du commerce de détail à dominante alimentaire, ainsi que dans la distribution en gros à dominante alimentaire. En France, le groupe Carrefour exploite des hypermarchés, supermarchés, commerces de proximité, cash and carry, sous les enseignes Carrefour, Carrefour Market, Carrefour City, Carrefour Contact, Carrefour Express, Carrefour Montagne, Huit à 8, Marché Plus, Proxi et Promocash. Le groupe Carrefour dispose par ailleurs d’une activité de drive et exploite plusieurs sites marchands sur internet : www.carrefour.fr, www.ooshop.carrefour.fr et www.rueducommerce.fr. -

Retail Food Sector Retail Foods France

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 9/13/2012 GAIN Report Number: FR9608 France Retail Foods Retail Food Sector Approved By: Lashonda McLeod Agricultural Attaché Prepared By: Laurent J. Journo Ag Marketing Specialist Report Highlights: In 2011, consumers spent approximately 13 percent of their budget on food and beverage purchases. Approximately 70 percent of household food purchases were made in hyper/supermarkets, and hard discounters. As a result of the economic situation in France, consumers are now paying more attention to prices. This situation is likely to continue in 2012 and 2013. Post: Paris Author Defined: Average exchange rate used in this report, unless otherwise specified: Calendar Year 2009: US Dollar 1 = 0.72 Euros Calendar Year 2010: US Dollar 1 = 0.75 Euros Calendar Year 2011: US Dollar 1 = 0.72 Euros (Source: The Federal Bank of New York and/or the International Monetary Fund) SECTION I. MARKET SUMMARY France’s retail distribution network is diverse and sophisticated. The food retail sector is generally comprised of six types of establishments: hypermarkets, supermarkets, hard discounters, convenience, gourmet centers in department stores, and traditional outlets. (See definition Section C of this report). In 2011, sales within the first five categories represented 75 percent of the country’s retail food market, and traditional outlets, which include neighborhood and specialized food stores, represented 25 percent of the market. In 2011, the overall retail food sales in France were valued at $323.6 billion, a 3 percent increase over 2010, due to price increases. -

Hypermarket Lessons for New Zealand a Report to the Commerce Commission of New Zealand

Hypermarket lessons for New Zealand A report to the Commerce Commission of New Zealand September 2007 Coriolis Research Ltd. is a strategic market research firm founded in 1997 and based in Auckland, New Zealand. Coriolis primarily works with clients in the food and fast moving consumer goods supply chain, from primary producers to retailers. In addition to working with clients, Coriolis regularly produces reports on current industry topics. The coriolis force, named for French physicist Gaspard Coriolis (1792-1843), may be seen on a large scale in the movement of winds and ocean currents on the rotating earth. It dominates weather patterns, producing the counterclockwise flow observed around low-pressure zones in the Northern Hemisphere and the clockwise flow around such zones in the Southern Hemisphere. It is the result of a centripetal force on a mass moving with a velocity radially outward in a rotating plane. In market research it means understanding the big picture before you get into the details. PO BOX 10 202, Mt. Eden, Auckland 1030, New Zealand Tel: +64 9 623 1848; Fax: +64 9 353 1515; email: [email protected] www.coriolisresearch.com PROJECT BACKGROUND This project has the following background − In June of 2006, Coriolis research published a company newsletter (Chart Watch Q2 2006): − see http://www.coriolisresearch.com/newsletter/coriolis_chartwatch_2006Q2.html − This discussed the planned opening of the first The Warehouse Extra hypermarket in New Zealand; a follow up Part 2 was published following the opening of the store. This newsletter was targeted at our client base (FMCG manufacturers and retailers in New Zealand). -

Iacarrefoura2000ieng.Pdf

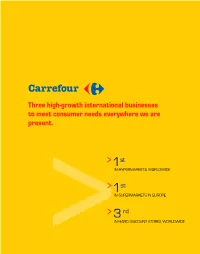

Three high-growth international businesses to meet consumer needs everywhere we are present. > 1st IN HYPERMARKETS WORLDWIDE > 1st IN SUPERMARKETS IN EUROPE > 3 rd >IN HARD DISCOUNT STORES WORLDWIDE MESSAGEMESSAGE FROM THE CHAIRMAN > At the end of January, the European Commission cleared our mer- ger with Promodès. We decided on the rapid consolidation of all our hyper- markets under the Carrefour trade name, and all our supermarkets under a common trade name in each country. > In 87 hypermarkets and 490 supermarkets in France, and 117 hypermarkets and 109 supermarkets in Spain, Italy, Greece, Turkey, Indonesia, China and Korea, the current teams in Continent, Pryca, Continente, Euromercato, Stoc, Maxor and Supeco stores transform- ed those stores and reopened under the Carrefour or Champion name by the end of the year (January in Italy). > This was a major undertaking since the changes involved more than the name of the store or shelf displays. The changes meant train- ing men and women in new working methods and harmonizing product lines. Inevitably, this effort resulted in some disruption, which explains the year-end drop or slowdown in sales revenue in France and Spain. Sometimes custo- mers could not immediately find products in their usual place, sometimes products were not available in the store for short periods due to system changes. In the first half of 2001, all these stores should steadily return to normal operating conditions. > We plan to continue these changes in other countries. In Belgium, 60 hypermarkets will transfer to the Carrefour trade name by the end of 2001. In France and Spain, we will continue to make progress in pooling logistics, creating synergies over the long term. -

FRENCH MARKET PRESENTATION for : FEVIA from : Sophie Delcroix – Elise Deroo – Green Seed France Date : 19Th June, 2014

FRENCH MARKET PRESENTATION For : FEVIA From : Sophie Delcroix – Elise Deroo – Green Seed France Date : 19th June, 2014 FEVIA 1 I. GREEN SEED GROUP : WHO WE ARE II. MARKET BACKGROUND AND CONSUMER TRENDS III. THE FRENCH RETAIL SECTOR IV. KEY RETAILERS PROFILES V. FOODSERVICE VI. KEY LEARNINGS VII. CASE STUDIES FEVIA 2 Green Seed Group Having 25 years of experience, the Green Seed Group is a unique international network of 11 offices in Europe, North America and Australia, specializing in the food & beverage sector OUR MISSION Advise both French and foreign food and beverage companies or marketing boards, on how to develop a sustainable and profitable position abroad Green Seed France help you to develop your activity in France using our in-depth knowledge of the local food and beverage market and our established contacts within the trade FEVIA 3 A growing and unique international network Germany (+ A, CH) The Netherlands Scandinavia U.S.A./Canada Great Britain Belgium France Portugal Spain Italy 11 offices covering 18 countries Australasia FEVIA 4 The Green Seed model Over the last decade, one of the most important trends in the French food & drink trade has been for retailers to deal with their suppliers on a direct line. Green Seed France has developed its business model around this trend. We act as business facilitators ensuring that every step of the process is managed with maximum efficiency. From first market visit, to launch as well as the ongoing relationship that follows. We offer a highly cost-effective solution of “flexible local sales and marketing management support” aimed at adding value. -

Carrefour Group, Building RELATIONSHIPS a L R EPO RT

2007 ANNUAL REPORT CARREFOUR GROUP, BUILDIng RELATIONSHIPS RT EPO R L A U ANN Carrefour SA with capital of 1,762,256,790 euros 2007 RCS Nanterre 652 014 051 www.groupecarrefour.com N°1 in Europe 30 countries N°2 worldwide OTHERS PUBLICATIONS: RAPPORT DÉVELOPPEMENT DURABLE 2007 102.442 billion euros in sales carrEFOUR carrEFOUR incl. tax under GROUP GROUP Group banners 16,899,020 sq.m sales area BUILDING FInancIAL RESPOnsIBLE REPORT RELATIONSHIPS 2007 490,042 employees 2007 Sustainability Report 2007 Financial Report stores More than 3 billion cash 14,991 transactions per year YOU CAN FIND THE LATEST CARREFOUR GROUP NEWS AND THE INTERACTIVE ANNUAL REPORT AT WWW.GROUPECARREFOUR.COM Design, copywriting and production: Translation: Photocredits: Carrefour Photo Library, Lionel Barbe, Christophe Gay/Skyzone, Nicolas Landemard, Gilles Leimdorfer/Rapho, Jean-Erick Pasquier/Rapho, Michel Labelle, all rights reserved - p. 2-3: Getty Images/Bruno Morandi - p. 4-5: Getty Images/ Hans Neleman - p. 6-7: Getty Images/Lonely Planet Images/Krzysztof Dydynski - p. 8-9: Getty Images/Daly & Newton - p. 16: Getty Images/Shannon Fagan - p. 24: Getty Images/Daly & Newton - p. 32: Getty Images/Frank Herholdt - p. 36: Corbis/Beathan - p. 38: Getty Images/fStop - p. 39: Getty Images/Darryl Estrine - p. 40: Corbis/Jose Luis Pelaez - p. 41: Getty Images/Somos/Veer - p. 42: Getty Images/Floresco Images - p. 45: Getty Images/Dimitri Vervitsiotis. CARREFOUR / ATACADAO / CARREFOUR EXPRESS / CARREFOUR BAIRRO / CARREFOUR CITY / CARREFOUR MARKET / 5 MINUT CARREFOUR / Paper: the Carrefour group is committed to the responsible management of its paper sourcing. The paper used for this document is certified PEFC (Programme for the Endorsement of Forest Certification schemes). -

Country Retail Scene Report

SPAIN COUNTRY RETAIL SCENE REPORT December 2012 KANTAR RETAIL 24 – 28 Bloomsbury Way, London WC1A 2PX, UK / Tel. +44 (0)207 031 0272 / www.KantarRetail.com INFORMATION / INSIGHT / STRATEGY / EXECUTION © Kantar Retail 2012 245 First Street 24 – 28 Bloomsbury Way T +44 (0) 207 0310272 Suite 1000 London, WC1A 2PX F +44 (0) 207 0310270 Cambridge, MA 02142 UK [email protected] USA www.kantarretail.com Index I. Key Themes .......................................................................................................... 2 II. Socio – Economic Background .............................................................................. 3 III. Key Players in the Grocery Retail Sector ............................................................ 11 IV. Grocery Retail Channels ..................................................................................... 19 V. Conclusion ........................................................................................................... 24 © 2012 KANTAR RETAIL | 2012 Spain Retail Scene | www.kantarretail.com 1 245 First Street 24 – 28 Bloomsbury Way T +44 (0) 207 0310272 Suite 1000 London, WC1A 2PX F +44 (0) 207 0310270 Cambridge, MA 02142 UK [email protected] USA www.kantarretail.com I. Key Themes National players are capturing growth and increasing concentration in Spain Despite the economic turmoil in Spain, leading Spanish grocery retailers are expected to see their growth accelerate in the coming years, led by retailers such as Mercadona and Dia, both growing at over 5% per year. Mercadona is by far the largest Spanish grocery retailer in terms of sales and has successfully adapted its strategy to the economic crisis that Spain is facing. Its impressive business model has enabled it to retain shopper loyalty and support robust physical expansion and the retailer is looking to further strengthen its domination of the supermarket channel and the grocery market overall. Due to the strong growth of two of the top five grocery retailers in Spain the dominance of a few major players will increase. -

Retail Foods

Required Report: Required - Public Distribution Date: June 22, 2021 Report Number: FR2021-0003 Report Name: Retail Foods Country: France Post: Paris Report Category: Retail Foods Prepared By: Laurent J Journo Approved By: Kathryn Snipes Report Highlights: During the Covid-19 pandemic the French government designated the retail sector as essential and most firms had a continuity in operations. The nationwide lockdown and closing of restaurants resulted in a boost to the retail sector. Ordering on-line and picking-up at the store (also known as Click and Collect or E-drive) sales rose 40 percent in 2020 and represented 7.8 percent of all retail food sales. The French retail distribution network is diverse and sophisticated and offers a variety of opportunities for U.S. food and food products provided they conform to EU regulations. THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Market Fact Sheet: France EXECUTIVE SUMMARY The Covid-19 pandemic suppress economic growth. In 2020 its Quick Facts CY 2020 gross domestic product (GDP) contracted 8.3 percent from 2019 to $2.28 trillion. Imports of Consumer-Oriented Products (USD million) 42** France is the world's seventh largest industrialized economy and the EU's second largest economy after Germany. It has List of Top 10 Growth Products in Host Country substantial agricultural resources and maintains a strong 1) Almonds 2) Pet food 3) Pistachios 4) Grapefruit manufacturing sector. France's dynamic services sector 5) Wine 6) Peanuts 7) Food preparations 8) Beer accounts for an increasing share of economic activity and has 9) Sweet Potatoes10) Sauces and seasonings been responsible for most job creation in recent years. -

Carrefour 15Th November 2017 Standing at a Cross-Roads Food Retailing Fair Value EUR20 Vs

INDEPENDENT RESEARCH Carrefour 15th November 2017 Standing at a cross-roads Food retailing Fair Value EUR20 vs. EUR22 (price EUR16.83) BUY Bloomberg CA FP France is the group’s Achilles heel and Alexandre Bompard is set to Reuters CARR.PA unveil his solutions on January 23th. At this stage, the combination of a 12-month High / Low (EUR) 23.6 / 16.5 positive timing (return to inflation?), a depressed valuation (the market Market capitalisation (EURm) 13,034 Enterprise Value (BG estimates EURm) 16,343 is valuing the French hypermarkets at a negative €3.4bn) and an event- Avg. 6m daily volume ('000 shares) 3 583 driven momentum underpin our maintained Buy opinion. Our Fair Free Float 83.4% Value (€20 vs €22) is the average of a DCF (€17.6) and a SOP (€22.5). 3y EPS CAGR -6.2% Gearing (12/16) 38% Dividend yields (12/17e) 3.43% Although the group is crippled, Carrefour’s market capitalisation does not reflect the value of its assets in our view. Based on the SOP, which enables YE December 12/16 12/17e 12/18e 12/19e Revenue (EURm) 76,645 78,813 79,950 82,493 us to appreciate the asset liquidating market value, we derive an estimated Curr Op Inc. 2,351 2,010 2,070 2,197 share price of €22.5. At the current level of €17, we conclude that the EURm) market is valuing the French hypermarkets at a negative €3.4bn. Basic EPS (EUR) 1.01 0.93 1.05 1.15 Diluted EPS (EUR) 1.40 1.06 1.05 1.15 EV/Sales 0.22x 0.21x 0.22x 0.22x Alexandre Bompard’s task is focused on the price positioning/future of EV/EBITDA 4.4x 4.5x 4.8x 4.6x EV/EBIT 8.5x 8.8x 8.5x 8.1x the hypermarkets in France (embroiled in the Leclerc trap), the re- P/E 12.0x 15.9x 16.1x 14.6x definition of the offer (too premium currently?) and the digitalisation of ROCE 8.7 7.6 7.5 7.7 the group (lost in the Amazonian forest). -

Nielsen QBN Europe Q4 2017

EUROPE QUARTER BY NUMBERS Q4 2017 1 Copyright © 2017 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute. Copyright © 2017 The Nielsen Company CONTENTS SECTION 1 THE BIG PICTURE: EUROPE WEST Message from Olivier Deschamps…………………..…………………….………03 EUROPE AT A GLANCE Key economic drivers………………………………………………………….……04 Looking through Europe West FMCG lens………………………………...……06 COUNTRY SNAPSHOT Belgium……….………………………………………….…………………………..07 France……….………………………………………..….…………………………..10 Germany……….……………………………………..….…………………………..13 Italy……………………………………………………….…………………………..16 Netherlands..….…………………………………….……………….………………19 Portugal……….……………………………………..………………….……………22 Spain………………………………………………………………….………………25 United Kingdom.……………….…………………………………….………………28 IN THE INDUSTRY Retail Channel Universe Update……...………………………..…………………93 2 Copyright © 2018 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute. THE BIG PICTURE: EUROPE WEST Welcome to the first edition of Europe Quarter by Numbers that includes key Western European markets for Q4 2017, complimenting the view of Central and East Europe already in place. Our ambition is to provide context and insight into how broader macroeconomic factors are influencing consumer sentiment and spending patterns in the retail scene. After tough times in the last few years, 2017 showed a dynamic economic environment across Europe, with positive consumer confidence in the region reaching some of the highest levels seen for some time. While nations can draw similarities among the positive impacts on Olivier Deschamps consumer sentiment, Europeans diverge in the national issues of greatest concern - terrorism Retail Services Lead Markets remains high on the list and health is definitely a key priority with countries like Portugal showing notable peaks. Encouraged by lower risk of terrorism and better economic conditions, tourists flocked to the region in 2017 (+8%), particularly in Mediterranean countries. France was still the number one global tourist destination and Spain is about to exceed USA. -

Liste Points De Vente

MATCH CHATEAU SALINS CARREFOUR EXPRESS METZ-COISLIN CARREFOUR EXPRESS VERDUN MATCH COMMERCY EUVILLE CARREFOUR CITY METZ-CLERCS BOUTIQUE GERARDMER CARREFOUR EXPRESS ETAIN CARREFOUR CITY MONTIGNY BOUTIQUE EPINAL-JEUXEY BOUTIQUE VOID-VACON CARREFOUR MARKET YUTZ LEADER PRICE GERARDMER CARREFOUR MARKET THIONVILLE LEADER PRICE RAON L'ETAPE CARREFOUR MARKET MANOM MAISON IMAGERIE D'EPINAL L'EPICERIE FINE DE SAINT LOUIS MAISON ROBERT MIRECOURT Moselle (57) STATION SANDAUCOURT AUCHAN SEMECOURT BOUTIQUE MOULINS LES METZ COTE LORRAIN AUCHAN SUPERMARCHE XXEME BOUTIQUE SEMECOURT NosOÙ RETROUVER Points LEUR deGOÛT venteUNIQUE ? CORPS METZ BOUTIQUE THIONVILLE LA HALLE DES 3 ABBAYES AUCHAN SUPERMARCHE METZ ST BOUTIQUE FORBACH COMME UNE FLEUR JACQUES BOUTIQUE MUNDOLSHEIM MATCH EST/PONT A MOUSSON CARREFOUR CONTACT CIREY AUCHAN SUPERMARCHE PLANTIERES Meurthe-et-Moselle (54) BOUTIQUE BEST FAREBERSVILLER CORA BORNY AUCHAN LAXOU MATCH EST/ST MAX CARREFOUR CONTACT NANCY TICKETS JEANNE D'ARC MEURTHE-ET-MOSELLE LE JARDIN DES SAVEURS Bas-Rhin (67) AUCHAN TOMBLAINE MATCH EST/DOMBASLE BOUTIQUE GEISPOLHEIM CARREFOUR CONTACT MATCH EST/CHAMPIGNEULLES CORA MOULINS LES METZ AUCHAN NANCY LOBAU RICHARDMENIL MATCH EST/VILLERS CORA MONDELANGE AUCHAN MONT ST MARTIN CARREFOUR CONTACT DIEULOUARD MATCH EST/ST NICOLAS CORA SARREGUEMINES CORA MONCEL LES LUNEVILLE CARREFOUR CITY NANCY ST Vosges (88) CORA STE MARIE AUX CHENE CORA ESSEY LES NANCY MATCH EST/JOFFRE NANCY GEORGES AUCHAN SUPERMARCHE GOLBEY Haut-Rhin (68) BOUTIQUE WITTENHEIM LECLERC MARLY CORA HOUDEMONT MATCH EST/VILLERUPT -

Carrefour Took a New Look at Its Business and Formulated a New Ambition: to Become the Preferred Retailer

22.07.2010 08:20 PDF_QUADRI_300dpi_txvecto 22.07.2010 08:20 PDF_QUADRI_300dpi_txvecto 1 In 2009, Carrefour took a new look at its business and formulated a new ambition: to become the preferred retailer. The retailer that knows its customers, anticipates their desires Report2009 Annual and delights them within its stores. The retailer that inspires trust through product quality, prices and socially-responsible commitments. The retailer that helps customers achieve a better quality of life every day. Carrefour has what it takes to reach its goals: its brand, stores, products, services and teams, all gathered around the same values. In 2009, 475,000 committed employees, caring about customer needs and positive at all times, joined forces to ensure that clients enjoy shopping at Carrefour again and again. 3 billion 7th employer checkouts per year worldwide in the private sector in 2009 2 Our ambition: to become the preferred retailer Satisfying the needs of our customers and consumers is no longer enough. Carrefour must wow and delight them every day. 3 To be recognized Actions speak louder than words. We work hard every day to offer the best products and services at the best prices, creating more value for our customers and consumers. And as we develop this value, we keep building up their recognition. 2009 Annual Report2009 Annual and loved Love begins with very little things. Just like people, a brand is stronger when loved. We do everything in our power to build a relationship with our customers, consumers and partners based on loyalty and trust. And earn their loyalty a little more every day.