Capstone Headwaters Restaurants M&A Coverage Report Q1 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

National Retailer & Restaurant Expansion Guide Spring 2016

National Retailer & Restaurant Expansion Guide Spring 2016 Retailer Expansion Guide Spring 2016 National Retailer & Restaurant Expansion Guide Spring 2016 >> CLICK BELOW TO JUMP TO SECTION DISCOUNTER/ APPAREL BEAUTY SUPPLIES DOLLAR STORE OFFICE SUPPLIES SPORTING GOODS SUPERMARKET/ ACTIVE BEVERAGES DRUGSTORE PET/FARM GROCERY/ SPORTSWEAR HYPERMARKET CHILDREN’S BOOKS ENTERTAINMENT RESTAURANT BAKERY/BAGELS/ FINANCIAL FAMILY CARDS/GIFTS BREAKFAST/CAFE/ SERVICES DONUTS MEN’S CELLULAR HEALTH/ COFFEE/TEA FITNESS/NUTRITION SHOES CONSIGNMENT/ HOME RELATED FAST FOOD PAWN/THRIFT SPECIALTY CONSUMER FURNITURE/ FOOD/BEVERAGE ELECTRONICS FURNISHINGS SPECIALTY CONVENIENCE STORE/ FAMILY WOMEN’S GAS STATIONS HARDWARE CRAFTS/HOBBIES/ AUTOMOTIVE JEWELRY WITH LIQUOR TOYS BEAUTY SALONS/ DEPARTMENT MISCELLANEOUS SPAS STORE RETAIL 2 Retailer Expansion Guide Spring 2016 APPAREL: ACTIVE SPORTSWEAR 2016 2017 CURRENT PROJECTED PROJECTED MINMUM MAXIMUM RETAILER STORES STORES IN STORES IN SQUARE SQUARE SUMMARY OF EXPANSION 12 MONTHS 12 MONTHS FEET FEET Athleta 46 23 46 4,000 5,000 Nationally Bikini Village 51 2 4 1,400 1,600 Nationally Billabong 29 5 10 2,500 3,500 West Body & beach 10 1 2 1,300 1,800 Nationally Champs Sports 536 1 2 2,500 5,400 Nationally Change of Scandinavia 15 1 2 1,200 1,800 Nationally City Gear 130 15 15 4,000 5,000 Midwest, South D-TOX.com 7 2 4 1,200 1,700 Nationally Empire 8 2 4 8,000 10,000 Nationally Everything But Water 72 2 4 1,000 5,000 Nationally Free People 86 1 2 2,500 3,000 Nationally Fresh Produce Sportswear 37 5 10 2,000 3,000 CA -

Restaurant Trends App

RESTAURANT TRENDS APP For any restaurant, Understanding the competitive landscape of your trade are is key when making location-based real estate and marketing decision. eSite has partnered with Restaurant Trends to develop a quick and easy to use tool, that allows restaurants to analyze how other restaurants in a study trade area of performing. The tool provides users with sales data and other performance indicators. The tool uses Restaurant Trends data which is the only continuous store-level research effort, tracking all major QSR (Quick Service) and FSR (Full Service) restaurant chains. Restaurant Trends has intelligence on over 190,000 stores in over 500 brands in every market in the United States. APP SPECIFICS: • Input: Select a point on the map or input an address, define the trade area in minute or miles (cannot exceed 3 miles or 6 minutes), and the restaurant • Output: List of chains within that category and trade area. List includes chain name, address, annual sales, market index, and national index. Additionally, a map is provided which displays the trade area and location of the chains within the category and trade area PRICE: • Option 1 – Transaction: $300/Report • Option 2 – Subscription: $15,000/License per year with unlimited reporting SAMPLE OUTPUT: CATEGORIES & BRANDS AVAILABLE: Asian Flame Broiler Chicken Wing Zone Asian honeygrow Chicken Wings To Go Asian Pei Wei Chicken Wingstop Asian Teriyaki Madness Chicken Zaxby's Asian Waba Grill Donuts/Bakery Dunkin' Donuts Chicken Big Chic Donuts/Bakery Tim Horton's Chicken -

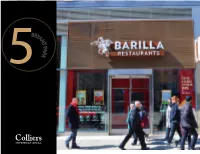

5Bryant Pa Rk

B RYA N T P A R 5 K B RYA N T P A R 5 K CURRENTLY Barilla Restaurants SIZE Ground: 2,748 SF POSSESSION TERM Arranged Assignment of lease through October 31, 2029 RENT FRONTAGE Upon Request 20 Feet COMMENTS RENT - Fully built restaurant with venting in place located directly on Bryant Park Upon Request - Restaurant installation is three and a half years old - 11.5 years remaining on the lease NEIGHBORING TENANTS - Bryant Park sees 6 million visitors annually Whole Foods, Equinox, Tourneau, Sweetgreen, Cava, - Bryant Park annual subway ridership: 16,000,000 on the B. D, F, M and 7 Joe & the Juice, La Colombe, SoulCycle, Juice Press, - Over 70 Million square feet of office space Zara, COS, & Other Stories and Aureole - 17,000+ hotel rooms ZACH NATHAN DAVID A. GREEN Director Vice Chairman + 1 212 716 3791 + 1 212 716 3599 [email protected] [email protected] B B RYA RYA N N T T P P A A R R K 5 K 5 GROUND FLOORPLAN Sixth Avenue - Fully built restaurant with venting in place located directly on Bryant Park - Restaurant installation is three and a half years old - 11.5 years remaining on the lease - Bryant Park sees 6 million visitors annually - Bryant Park annual subway ridership: 16,000,000 on the B. D, F, M and 7 - Over 70 Million square feet of office space West 40th Street - 17,000+ hotel rooms ZACH NATHAN DAVID A. GREEN Director Vice Chairman + 1 212 716 3791 + 1 212 716 3599 [email protected] [email protected] 65th Street Central Park Fifth Avenue Fifth Central Park South The Plaza Grand Army Plaza 58th Street Bergdorf Goodman Van Cleef & Arpels 57th Street 57th Street N F Bulgari Q Piaget Mikimoto R Prada W Abercrombie & Fitch 56th Street Harry Winston Jewelers Henri Bendel Fifth Avenue Presbyterian Church 55th Street Wempe Warwick The University Club Hotel 54th Street Gap / Gap Kids St. -

Franklin Street Franklin Street

BEST PATIO IN THE FINANCIAL DISTRICT FRANKLIN265 STREET HIGHEST CONCENTRATION OF EMPLOYEES IN BOSTON IN IMMEDIATE BLOCKS DOWNTOWN BOSTON STEPS FROM POST OFFICE SQUARE FINANCIAL DISTRICT AREA STATS HIGHEST CONCENTRATION DAYTIME POPULATION OF EMPLOYEES IN BOSTON 33M SF OFFICE SPACE 300K 85,000 EMPLOYEES (1/2 BOSTON’S INVENTORY) WITHIN EYESIGHT STEPS FROM... BOSTON GARDEN 1.7 ACRE PARK POST OFFICE SQUARE FANEUIL HALL 317 403 ROOM ROOM HOTEL HOTEL ROSE KENNEDY GREENWAY NEWLY RENOVATED BOSTON DOWNTOWN/ LANGHAM HOTEL FANEUIL HALL HILTON HOTEL NEW OFFICE TENANTS IN THE MARKET FANEUIL HALL UNION OYSTER HOUSE SEPHORA ANN TAYLOR JOE’S AREA BANANA REPUBLIC URBAN OUTFITTERS HARD ROCK CAFE GAP RETAIL COACH UNIQLO MCCORMICK & SCHMICK’S TUMI SUNGLASS HUT FEDEX GOVERNMENT CENTER - 10,828 ENTREES WAGAMAMA BOSTON MARRIOTT CVS LONG WHARF STARBUCKS STAPLES CITIZENS BANK 4 7 ELEVEN CITIZENS BANK SAM ADAMS SEVEN-ELEVEN THE KINSALE CAFFE NERO BANK OF AMERICA COCOBEET DUNKIN DONUTS LEGAL SEA FOODS WOLFGANGS SANTANDER SANTANDER THE OCEANAIRE SWEETGREEN STATE STREET PROVISIONS BROOKS BROTHERS RUTH’S CHRIS HAYMARKET - 11,469 ENTREES TATTE CLOVER SPYCE WAREHOUSE MOOO... B GOOD STARBUCKS DIG INN SWEETGREEN FEDEX MARIEL TRADESMAN COFFEE THE HILTON LUKE’S LOBSTER FIRST REPUBLIC CVS CHIPOTLE BANK BROADSIDE TAVERN LOVE ART SUSHI BRIX FLAT BLACK FIN POINT WALGREENS HOMEGOODS DUNKIN DONUTS T. MOBILE THE LANGHAM PARK STREET - 19,688 ENTREES SAM LA GRASSA’S TJ MAXX STARBUCKS POST SANTANDER BANK OFFICE FRANKLIN265 STREET MARSHALLS SQUARE EQUINOX PLANET FITNESS KANES DONUTS PRIMARK REPUBLIC FITNESS FIDELITY HALE & HEARTY SWEETGREEN OLD NAVY STARBUCKS INTELLIGENTSIA YVONNE’S ROCHE BROS. PALM EVERYBODY FIGHTS COSI PRET A MANGER DOWNTOWN CROSSING - 23,478 ENTREES CAFFE NERO BANK OF AMERICA THE BAR METHOD TD AMERITRADE JAMES HOOK CO. -

Results TOP FAST-FOOD RESTAURANTS

Results TOP FAST-FOOD RESTAURANTS Top fast-food restaurants Definition Fast-food restaurant Fast-food restaurants are food retailing institutions with a limited menu that offer pre-cooked or quickly prepared food available for take-out.1 Many provide seating for customers, but no wait staff. Customers typically pay before eating and choose and clear their own tables. They are also known as quick-service restaurants (QSRs). Top fast-food advertisers Fast-food restaurants that ranked in the top-25 in total advertising spending in 2019 and/or targeted their advertising to children, Hispanic, and/or Black consumers (N=27). Fast-food company Corporation or other entity that owns the restaurant. Some fast-food companies own more than one different fast-food restaurant chain. In this report, we focus on the 25 U.S. fast-food restaurants and/or Black consumers. U.S. sales of these 27 restaurants with the highest advertising spending in 2019, plus two totaled $188 billion in 2019, an average increase of 24% over restaurants with TV advertising targeted to children, Hispanic, 2012 salesi (see Table 3). Table 3. Sales ranking of top fast-food advertisers: 2019 Sales ranking 2019 % Top-25 ad U.S. sales change spending 2019 2012 Company Restaurant Category ($ mill) vs. 2012 in 2012 1 1 McDonald's Corp McDonald's Burger $40,413 14% √ 2 3 Starbucks Corp Starbucks Snack $21,550 78% √ 3 9 Chick-fil-A Chick-fil-A Chicken $11,000 138% √ 4 6 Yum! Brands Taco Bell Global $11,000 47% √ 5 5 Restaurant Brands Intl Burger King Burger $10,300 20% √ 6 2 Doctor's -

Inspire Brands Completes Acquisition of Dunkin' Brands

Inspire Brands Completes Acquisition of Dunkin’ Brands . Becomes second-largest restaurant company in the U.S. by system sales and locations . Inspire now encompasses: $26 billion in system sales; nearly 32,000 restaurants in 60+ countries; 600,000+ company and franchise team members; 3,200+ franchisees ATLANTA – December 15, 2020 – Inspire Brands, Inc. (“Inspire”) today announced the completion of its $11.3 billion acquisition of Dunkin’ Brands Group, Inc. (“Dunkin’ Brands”). With the addition of Dunkin’ and Baskin-Robbins, Inspire now encompasses nearly 32,000 restaurants across more than 60 countries generating $26 billion in annual system sales, making it the second-largest restaurant company in the U.S. by both system sales and locations. Inspire’s family of brands includes Arby’s®, Baskin- Robbins®, Buffalo Wild Wings®, Dunkin’®, Jimmy John’s®, Rusty Taco®, and SONIC Drive-In®. “We are very excited to welcome the Dunkin’ and Baskin-Robbins brands into the Inspire family. Dunkin’ and Baskin-Robbins are category leaders and two of the most iconic restaurant brands in the world,” said Paul Brown, Co-founder and Chief Executive Officer of Inspire. “This is an incredible moment in our journey as a company. I want to thank all our team members, franchisees and suppliers whose hard work helped make this possible.” The acquisition of Dunkin’ Brands furthers Inspire’s goal of bringing together a family of highly differentiated and complementary brands. Both Dunkin’ and Baskin-Robbins will benefit by leveraging the capabilities and best practices of Inspire’s shared services platform. Additionally, both brands will also benefit Inspire by adding a highly talented team, strong franchisee network, large and loyal customer base, scaled international platform, as well as a robust consumer packaged goods licensing capability. -

STARBUCKS: from CROP to CUP APRIL 2015 the IMPACT of SOURCING INDUSTRIAL CONVENTIONAL MILK Updated January 2018

COALITION POWERED BY GREEN AMERICA STARBUCKS: FROM CROP TO CUP APRIL 2015 THE IMPACT OF SOURCING INDUSTRIAL CONVENTIONAL MILK updated January 2018 A MILK COMPANY Starbucks is one of the world’s most popular and widespread coffeehouse brands. It has over 22,000 cafes in 66 countries.1 In Manhattan alone there are 9 Starbucks per square mile.2 Starbucks built its reputation on delivering specialty coffee, putting a lot of energy into telling the story of its coffee from field to café. But what the company fails to address is the fact that each year, it purchases over 140,000,000 gallons of milk— enough to fill an Olympic-sized swimming pool 212 times.3 The fact is that Starbucks is a milk company as much or more than it is a coffee company. It is beyond time that it addresses the many negative impacts the industrial conventional dairy supply chain, from feed crop to cup, has on animal welfare and human and environmental health. If Starbucks’ goal, as stated on the company’s website, is to “share great coffee with [its] friends and help make the world a little better,” it is essential that the company transitions to organic milk.4 By setting the organic milk standard for coffee chains, Starbucks can demonstrate a serious commitment to providing environmentally and socially conscious products. Competitor com- panies like Pret A Manger are able to offer organic milk at a lower price than Starbucks charges for conventional dairy. It is our responsibility as consumers to vote with our dollars and use our voices to persuade the dairy industry to im- prove. -

SBA Franchise Directory Effective April 8, 2020 SBA FRANCHISE

SBA Franchise Directory Effective April 8, 2020 SBA SBA FRANCHISE FRANCHISE IS AN SBA IDENTIFIER IDENTIFIER MEETS FTC ADDENDUM SBA ADDENDUM ‐ NEGOTIATED CODE Start CODE BRAND DEFINITION? NEEDED? Form 2462 ADDENDUM Date NOTES When the real estate where the franchise business is located will secure the SBA-guaranteed loan, the Collateral Assignment of Lease and Lease S3606 #The Cheat Meal Headquarters by Brothers Bruno Pizza Y Y Y N 10/23/2018 Addendum may not be executed. S2860 (ART) Art Recovery Technologies Y Y Y N 04/04/2018 S0001 1-800 Dryclean Y Y Y N 10/01/2017 S2022 1-800 Packouts Y Y Y N 10/01/2017 S0002 1-800 Water Damage Y Y Y N 10/01/2017 S0003 1-800-DRYCARPET Y Y Y N 10/01/2017 S0004 1-800-Flowers.com Y Y Y 10/01/2017 S0005 1-800-GOT-JUNK? Y Y Y 10/01/2017 Lender/CDC must ensure they secure the appropriate lien position on all S3493 1-800-JUNKPRO Y Y Y N 09/10/2018 collateral in accordance with SOP 50 10. S0006 1-800-PACK-RAT Y Y Y N 10/01/2017 S3651 1-800-PLUMBER Y Y Y N 11/06/2018 S0007 1-800-Radiator & A/C Y Y Y 10/01/2017 1.800.Vending Purchase Agreement N N 06/11/2019 S0008 10/MINUTE MANICURE/10 MINUTE MANICURE Y Y Y N 10/01/2017 1. When the real estate where the franchise business is located will secure the SBA-guaranteed loan, the Addendum to Lease may not be executed. -

106,762 26.0% 5 Businesses 1,872

TIMES SQUARE | NOVEMBER 2020 KEY INDICATORS November By the Numbers Monthly Key Economic Indicators 5 businesses Re-opened from COVID-19 closures in Times Square 26.0% Hotel occupancy during October in Times Square 106,762 Average Daily Visitors to Times Square 1,872 Photo credit: Gothamist, CS Muncy Thousand watched from Times Square as Total SF Leased in Times Square ballots poured in for the Presidential Election. Average Daily Visitors Pedestrian Count November brought on average 106,762 pedestrians per day to AVERAGE DAILY 2020 PEDESTRIAN COUNT Times Square, a 68.4% decline 2019 from 2019 but on par with last 450,000 month. 400,000 366,695 337,864 The past three months, Times 350,000 Square’s pedestrian counts have 300,000 steadily exceeded daily averages 250,000 over 100,000. 200,000 150,000 Foot traffc peaked on November 107,598 106,762 7th, the day of the Presidental 100,000 Election result announcement, at 50,000 189,751 people. This marks 0 OCTOBER NOVEMBER the highest daily count since Source: Springboard March. TIMES SQUARE | NOVEMBER 2020 KEY INDICATORS Commercial Real Estate Class A In November, Times Square’s occu- pancy rate remained consis- XXXXXXOCCUPANCY RATE/ XXXXTIMES SQUARE PRICE PER SQUARE FOOT XXXXMIDTOWN tent with September and October CLASS A PRICE PER SF at 92.5%. Midtown’s occupancy 95% rate remained unchanged from pre- $64 $65 vious months at 89.5%. 93% $65 $68 TImes Square’s net effective rent re- 91% mained unchanged from last month $74 $73 $73 $74 due to minimal leasing activity. -

Staff Favs 2019-2020 Colors Hobbies Restaurants Drinks Snacks Candy Scents

Staff Favs 2019-2020 Colors Hobbies Restaurants Drinks Snacks Candy Scents Julie Armstrong 10/11 MWF Red, neutrals Reading, movies, family time Rusty Taco, Komodo Loco, Mexican, BJ’s, Chick Fil A Starbucks Vanilla Latte, Unsweet tea w/raspberry Popcorn with M & M’s, anything sweet & salty Fall Scents (leaves, pumpkin, apple spice, vanilla, Christmas ) Carrie Barton 9/13 MWF Green, blue, black Reading, basketball, puzzles Chick Fil A, Wendy’s, Braums, Roman’s Pizza Coffee, coke Salt & vinegar chips, popcorn Licorice (red & black), peanut M&M’s, Werthers Vanilla, anything baking smell, jasmine LeAnn Bielss 11/17 MWF Purple Watching sports, music, reading Chick Fil A, Rosa’s, Sonic Dr. Pepper, unsweet tea Popcorn, yogurt pretzels, fruit Chocolate, Heath Bar, M&M’s Mulberry, vanilla Amber Bloom 5/12 TTH Pink, blue Watercolor painting, reading Chuy’s, Panera Half/half tea, flavored water Popcorn, flavored nuts Dove cark chocolate (love raspberry/mint) Light citrus scents Todd Bramlett 1/4 M-F Green & gold (of course) Basketball, sports Whataburger, Starbucks Tea Popcorn, cherries Dots What? I am a dude, whatever! Heather Brisman 4/10 MWF Neutrals Crafting Chuy’s, In & Out Unsweet tea Chips/nuts (salty) Butterfinger Fall scents Lynn Calmes 8/5 MWF Navy blue, teal Reading, hiking, playing word games Chili’s, Chick Fil A, On the Border Coke, strawberry limeade, lemonade Chex mix, trail mix Milk chocolate, peanut or caramel M&M’s Tropical scents Micah Caswell 6/23 MWF Blue Reading LSA Coffee Nuts Dots Jenny Coffey 3/8 MWF Mint, pink, light blue, -

State of the Chains, 2020

www.nycfuture.org DECEMBER 2020 STATE OF THE CHAINS, 2020 Our thirteenth annual ranking of national retailers in New York City finds by far the largest overall decline in the number of chain stores, and the third consecutive year-over-year drop in national retailer locations. The year was marked by unprecedented economic volatility across all sectors, and within all boroughs, as the national retail market experienced unprecedented contraction as a result of the COVID-19 outbreak and subsequent shutdowns and store closures. CONTENTS INTRODUCTION 3 SIDEBAR: WHERE THE CHANGE IS OCCURRING 9 NEW YORK CITY’S LARGEST NATIONAL RETAILERS, 2020 11 NATIONAL RETAILER GROWTH BY INDUSTRY CATEGORY, 2019-2020 23 NATIONAL RETAILERS IN NYC BY ZIP CODE 24 MANHATTAN 29 BROOKLYN 32 This report was written by Marco Torres and edited by Charles Shaviro, Eli Dvorkin, and Jonathan Bowles. QUEENS 34 BRONX 37 Center for an Urban Future (CUF) is a leading New York STATEN ISLAND 38 City–based think tank that generates smart and sustainable public policies to reduce inequality, increase economic mobility, and grow the economy. General operating support for the Center for an Urban Future has been provided by The Clark Foundation and the Bernard F. and Alva B. Gimbel Foundation. CUF is also grateful for support from Fisher Brothers for the Middle Class Jobs Project. Executive Director: Jonathan Bowles Editorial & Policy Director: Eli Dvorkin Associate Editor: Laird Gallagher Data Researcher: Charles Shaviro Events & Operations Manager: Stephanie Arevalo Board of Directors: Gifford Miller (Chairman), Michael Connor (Vice Chair), Max Neukirchen (Treasurer), John H. Alschuler, Margaret Anadu, Jonathan Bowles, Russell Dubner, Lisa Gomez, Jalak Jobanputra, Kyle Kimball, David Lebenstein, Eric S. -

Non-Participating Airport Outlets

Non-participating airport outlets Category Departments Baskin & Robbins Bombay Chowpatty Bricco Café Brioche Doree Burger King Butlers Café CAFÉ Chocolat Café Nero Camden Foods Camden Foods Carluccios Caviar House Charley's Grill and Sub Cho Gao Chowking Cinnabon Cold Stone Cosi Dining / Costa restaurants Delizie Draft House Giraffe Haagen Daaz Heineken Bar JACK'S Bar & Grill KFC Krispy Kreme Le Pain Qoutidien Mary Brown Masale McDonalds Mezzanine Restaurant Mezze Express O' Briens Ocean Basket Paul Café PICNIC Gourmet Market Pink Berry Pint 19 Pret A Manger Pulp Bar Juice Red Carpet Rosso Vivo Rupee Room Safar Seafood Bar Seafood Restaurant Shake Shack Shawarmanji Starbucks Subway Sweet Factory Taqado Taste of India Texas Chicken Thai Express The HUB The Kitchen/Wolfgang The Noodle House Wafi Gourmet (WG) Yo! Sushi Al Ansari Al Noor Bank Currency Commercial Bank of Dubai Dubai Express Exchange Emirates NBD Services Sharaf Exchange Travelex Exchange UAE Exchange BE Relax Spa Dubai International Hotel Massage and O2 Spa Fitness Spa Express** Timeless Spa Boots Pharmacy BinSina Dallmayr Vending Machines Masafi Vending Machine Red Bull Vending Machine Retailer Le Clos Self Service Kiosk Sweet Factory Al Wefaq Car Rental Alpha Destinations Management Arabian Tours Atlantis The Palm Dubai AVIS Diamond Lease Car Rental Dollar rent a car Dollar Car Rental Europe Car Europe rent a car Fast Rent-A-Car Golden Sands Hotel Apartments Hotels/Rent a Habtoor Hotel Car Hertz Intercontinental Hotel Group Jumeirah Stay Different Lotus Hotel Marriot The Ritz Carlton Movenpick National rent a car Payless Car Rental Sixt Car Rental The Address Hotel Thrifty Car Rental Thrifty rent a car Airport Business Center Aramex Baggage Wrapping Services DU Telecommunication Others Du Business Center Etisalat Telecommunication Etisalat Business Center CNN Traveller .