U.S. Sweets Sector: Ice Cream - Bakery and Pastry - Coffee

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Merchant Wishlist REP#______

Merchant Wishlist REP#_____________ Organization: ____________________ Contact name: _________________ Email: __________________________ Phone: _______________________ Fax to 1-888-870-9040 or email Address: ________________________ City: _________________________ [email protected] State: ____________ Zip: __________ Number of cards: _______________ We use the central address you provide like a pin point in a map, then create a list of the closest 100-200 merchants by distance and move your wishlist merchants to the top of the list. We do NOT call only the wishlist merchants and then wait until they get back with us (your card would never get finished if we did). 15 to 20% of merchants will provide an offer. We cannot guarantee the participation of any merchant. We reserve the right to determine final merchants and card design. List your local wishlist merchants (excluding Fast Food national merchants). This is a great place to include A&W Chipotle Jack’s PDQ Taco Bell your favorite eateries, hair care, hardware, Auto Arby's Church's KFC Pollo Tropical Taco John's Baja Fresh Culver's Krystal Popeyes Tijuana Flats Care, and others. Include known owner’s names Bojangles' Del Taco Long John Silver's Qdoba Wendy's 1. Burger King El Pollo Loco McDonald's Rally's Whataburger Captain D's Farmer Boys Moe's Red Robin White Castle 2. Carl's Jr. Five Guys Noodles & Co Rubio's Wienerschnitzel Checkers In-N-Out Burger Panda Express Sonic Drive-In Wingstop 3. Chick-fil-A Jack in the Box Panera Bread Steak 'n Shake Zaxby's 4. Subs/Sandwiches Boston Market Firehouse Subs Jimmy John's Portillo’s Schlotzsky's 5. -

Restaurant Trends App

RESTAURANT TRENDS APP For any restaurant, Understanding the competitive landscape of your trade are is key when making location-based real estate and marketing decision. eSite has partnered with Restaurant Trends to develop a quick and easy to use tool, that allows restaurants to analyze how other restaurants in a study trade area of performing. The tool provides users with sales data and other performance indicators. The tool uses Restaurant Trends data which is the only continuous store-level research effort, tracking all major QSR (Quick Service) and FSR (Full Service) restaurant chains. Restaurant Trends has intelligence on over 190,000 stores in over 500 brands in every market in the United States. APP SPECIFICS: • Input: Select a point on the map or input an address, define the trade area in minute or miles (cannot exceed 3 miles or 6 minutes), and the restaurant • Output: List of chains within that category and trade area. List includes chain name, address, annual sales, market index, and national index. Additionally, a map is provided which displays the trade area and location of the chains within the category and trade area PRICE: • Option 1 – Transaction: $300/Report • Option 2 – Subscription: $15,000/License per year with unlimited reporting SAMPLE OUTPUT: CATEGORIES & BRANDS AVAILABLE: Asian Flame Broiler Chicken Wing Zone Asian honeygrow Chicken Wings To Go Asian Pei Wei Chicken Wingstop Asian Teriyaki Madness Chicken Zaxby's Asian Waba Grill Donuts/Bakery Dunkin' Donuts Chicken Big Chic Donuts/Bakery Tim Horton's Chicken -

Downtown Grand Rapidsdining Guide

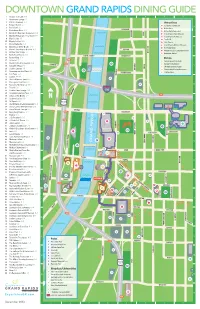

DOWNTOWN GRAND RAPIDS DINING GUIDE 1 Angel’s Thai Cafe H-5 1 2 3 4 5 6 7 8 2 Apartment Lounge I-7 88 13 3 B.O.B.’s Brewery J-4 Attractions 4 Bagger Dave’s J-3 C Gerald R. Ford Museum A A 5 Bar Divani J-5 D DeVos Place LEONARD 6 Bartertown Diner J-8 G DeVos Performance Hall A 7 Bentham’s Riverfront Restaurant H-4 L Grand Rapids Public Museum ONROE 8 Big Boy Restaurant - Pearl Street H-1 IONI M P Grand Rapids Art Museum 9 Big O’s Cafe I-5 T The B.O.B. 10 Biggby Coffee H-5 V Civic Theatre 11 Bistro Bella Vita K-4 W Grand Rapids Children’s Museum B B 12 Bobarino’s at The B.O.B. J-4 N 38 Y Van Andel Arena 13 Brann’s Steakhouse & Grille A-1 MASON Z Urban Institute of Contemporary Arts 14 Buffalo Wild Wings J-5 DIVISIO BB Downtown Market 15 Bull’s Head Tavern H-5 SIXTH STREET NEWBERRY 16 Burger King H-1 Hotels 86A 17 CC Cafe F-5 M Amway Grand Plaza Hotel 18 Charley’s Crab Restaurant K-3 86B B K Holiday Inn Downtown FOUR A C 19 Cinco De Mayo I-5 C TH ST AWA N JW Marriott Grand Rapids T 20 CitySen Lounge I-5 IONI E 68 OT S Courtyard by Marriott Downtown 21 Cornucopia at the Plaza H-4 A TROWBRIDGE U CityFlats Hotel 22 Cult Pizza J-8 ONRO M 23 Cygnus 27 H-4 P 24 Donk’s Mexican Joint H-5 77B 25 Flanagan’s Irish Pub H-5 D 26 Founders Brewing Co. -

Columbus Catholic School

OFFICE USE: Columbus Catholic Received by: Date: SCRIP ORDER FORM Filled by: Date: Please make checks payable to: Entered by: Date: GIFT CARD PROGRAM Purchaser:____________________________________________________DATE:______/______/______ Phone:_(_____)_________________Email:____________________________________Check #:_________Cash Order Pick Up Options: Hold at Scrip Office Pick Up at School:_______________________________________________________________________ Send Home with CCS Student (Name & Bldg):_________________________________________________ MUST HAVE A SIGNED AUTHORIZATION FORM ON FILE! Credit My Scrip Benefits to: Family Fee/Tuition Family Name:_____________________________________________________ OLP Parish SJB Parish SH Parish Corpus Christi Ms. B Memorial Scholarship Tuition Assistance Customer Signature: _______________________________________________________________________ See Back of form for Ordering Information Note: Rebates are subject to change Check www.shopwithscrip.com for a complete list of over 750 retailers available! Rev. 7/19 Scrip-To-Go Order Form Product Rebate Qty Ext Price Product Rebate Qty Ext Price 2-1/2 Cups Cupcakery & Bakeshop $15 20.00% Little Caesars $20 8.00% *Advance Auto Parts $25 or $100 7.00% Lumberyard Bar & Grill $25 10.00% Amazon.com $25 2.25% * Mall Furniture ($ per request) 4.00% Applebee's $25 8.00% * Marshfield Country Club ($ per request) 8.00% Arby's $10 8.00% Maurices $20 7.00% * Avon ($ by request) Alexis Vine 10.00% McDonalds $5 5.00% Baltus Gas $10 10.00% McDonalds $10 5.00% -

5Bryant Pa Rk

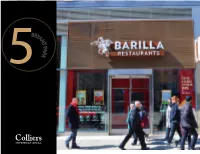

B RYA N T P A R 5 K B RYA N T P A R 5 K CURRENTLY Barilla Restaurants SIZE Ground: 2,748 SF POSSESSION TERM Arranged Assignment of lease through October 31, 2029 RENT FRONTAGE Upon Request 20 Feet COMMENTS RENT - Fully built restaurant with venting in place located directly on Bryant Park Upon Request - Restaurant installation is three and a half years old - 11.5 years remaining on the lease NEIGHBORING TENANTS - Bryant Park sees 6 million visitors annually Whole Foods, Equinox, Tourneau, Sweetgreen, Cava, - Bryant Park annual subway ridership: 16,000,000 on the B. D, F, M and 7 Joe & the Juice, La Colombe, SoulCycle, Juice Press, - Over 70 Million square feet of office space Zara, COS, & Other Stories and Aureole - 17,000+ hotel rooms ZACH NATHAN DAVID A. GREEN Director Vice Chairman + 1 212 716 3791 + 1 212 716 3599 [email protected] [email protected] B B RYA RYA N N T T P P A A R R K 5 K 5 GROUND FLOORPLAN Sixth Avenue - Fully built restaurant with venting in place located directly on Bryant Park - Restaurant installation is three and a half years old - 11.5 years remaining on the lease - Bryant Park sees 6 million visitors annually - Bryant Park annual subway ridership: 16,000,000 on the B. D, F, M and 7 - Over 70 Million square feet of office space West 40th Street - 17,000+ hotel rooms ZACH NATHAN DAVID A. GREEN Director Vice Chairman + 1 212 716 3791 + 1 212 716 3599 [email protected] [email protected] 65th Street Central Park Fifth Avenue Fifth Central Park South The Plaza Grand Army Plaza 58th Street Bergdorf Goodman Van Cleef & Arpels 57th Street 57th Street N F Bulgari Q Piaget Mikimoto R Prada W Abercrombie & Fitch 56th Street Harry Winston Jewelers Henri Bendel Fifth Avenue Presbyterian Church 55th Street Wempe Warwick The University Club Hotel 54th Street Gap / Gap Kids St. -

Restaurants in West Des Moines, Iowa

RESTAURANTS IN WEST DES MOINES, IOWA NAME ADDRESS AREA PHONE NAME ADDRESS AREA PHONE NAME ADDRESS AREA PHONE Restaurants - American Restaurants - Other Ethnic La Barista Coffee Bar 1963 Grand Avenue G3 515-267-1814 Applebee's Neighborhood Grill 6190 Mills Civic Pkwy B5 515-225-8646 Jethro's Jambalaya 9350 University Avenue inset 1 opens soon Let Them Eat Cake 405 Maple Street H4 515-277-1709 Bambino's Restaurant 1220 R 45 Hwy inset 2 515-981-9127 Mi Patria (Ecuadorian) 1410 22nd Street F1 515-222-2755 My Favorite Muffin 4949 Westown Pkwy # 170 D1 515-457-7117 Champps Americana 101 Jordan Creek Pkwy # 12520 B4 515-440-6565 Saraj (Bosnian) 1300 50th St # 206 D2 515-255-1133 Starbucks 101 Jordan Creek Pkwy # 12118 B4 515-222-2254 Cheesecake Factory 101 Jordan Creek Pkwy # 12550 B4 515-457-9888 Restaurants - Seafood Starbucks 1990 Grand Ave (in HyVee) G3 515-223-8151 Dahl's Grocery 1208 Prospect G3 515-224-2144 Bonefish Grill 650 S Prairie View Dr # 100 C4 515-267-0064 Starbucks 2800 University Ave # H3 F1 515-223-4200 Dahl's Grocery - Jordan Creek Cafe 5003 EP True Parkway D3 515-225-4445 Joe's Crab Shack 130 S Jordan Creek Pkwy B4 515-226-9966 Starbucks 5405 Mills Civic Pkwy (in Target) C4 515-223-0262 Famous Dave's 1720 22nd St F1 515-267-0800 Red Lobster 3838 Westown Pkwy E1 515-226-2150 Starbucks 555 S 51st St (in HyVee) D4 515-221-2610 Fire Creek Grill 800 S 50th St # 110 D5 515-224-0500 Waterfront Seafood Market 2900 University Ave # A4 F1 515-223-5106 Starbucks 6305 Mills Civic Pkwy B4 515-223-9263 Fresh Cafe & Market 1721 25th St -

Franklin Street Franklin Street

BEST PATIO IN THE FINANCIAL DISTRICT FRANKLIN265 STREET HIGHEST CONCENTRATION OF EMPLOYEES IN BOSTON IN IMMEDIATE BLOCKS DOWNTOWN BOSTON STEPS FROM POST OFFICE SQUARE FINANCIAL DISTRICT AREA STATS HIGHEST CONCENTRATION DAYTIME POPULATION OF EMPLOYEES IN BOSTON 33M SF OFFICE SPACE 300K 85,000 EMPLOYEES (1/2 BOSTON’S INVENTORY) WITHIN EYESIGHT STEPS FROM... BOSTON GARDEN 1.7 ACRE PARK POST OFFICE SQUARE FANEUIL HALL 317 403 ROOM ROOM HOTEL HOTEL ROSE KENNEDY GREENWAY NEWLY RENOVATED BOSTON DOWNTOWN/ LANGHAM HOTEL FANEUIL HALL HILTON HOTEL NEW OFFICE TENANTS IN THE MARKET FANEUIL HALL UNION OYSTER HOUSE SEPHORA ANN TAYLOR JOE’S AREA BANANA REPUBLIC URBAN OUTFITTERS HARD ROCK CAFE GAP RETAIL COACH UNIQLO MCCORMICK & SCHMICK’S TUMI SUNGLASS HUT FEDEX GOVERNMENT CENTER - 10,828 ENTREES WAGAMAMA BOSTON MARRIOTT CVS LONG WHARF STARBUCKS STAPLES CITIZENS BANK 4 7 ELEVEN CITIZENS BANK SAM ADAMS SEVEN-ELEVEN THE KINSALE CAFFE NERO BANK OF AMERICA COCOBEET DUNKIN DONUTS LEGAL SEA FOODS WOLFGANGS SANTANDER SANTANDER THE OCEANAIRE SWEETGREEN STATE STREET PROVISIONS BROOKS BROTHERS RUTH’S CHRIS HAYMARKET - 11,469 ENTREES TATTE CLOVER SPYCE WAREHOUSE MOOO... B GOOD STARBUCKS DIG INN SWEETGREEN FEDEX MARIEL TRADESMAN COFFEE THE HILTON LUKE’S LOBSTER FIRST REPUBLIC CVS CHIPOTLE BANK BROADSIDE TAVERN LOVE ART SUSHI BRIX FLAT BLACK FIN POINT WALGREENS HOMEGOODS DUNKIN DONUTS T. MOBILE THE LANGHAM PARK STREET - 19,688 ENTREES SAM LA GRASSA’S TJ MAXX STARBUCKS POST SANTANDER BANK OFFICE FRANKLIN265 STREET MARSHALLS SQUARE EQUINOX PLANET FITNESS KANES DONUTS PRIMARK REPUBLIC FITNESS FIDELITY HALE & HEARTY SWEETGREEN OLD NAVY STARBUCKS INTELLIGENTSIA YVONNE’S ROCHE BROS. PALM EVERYBODY FIGHTS COSI PRET A MANGER DOWNTOWN CROSSING - 23,478 ENTREES CAFFE NERO BANK OF AMERICA THE BAR METHOD TD AMERITRADE JAMES HOOK CO. -

Arby's Restaurant Group (ARG) Operates the Arby's Fast Food Chain Popular for Its Hot Roast Beef Sandwiches

Arby’s Restaurant 2312 Trustar Lane NW | Bemidji, MN | 56601 Keith A. Sturm, CCIM | 612.376.4488 | [email protected] 50 South 6th Street | Suite 1418 Amanda C. Leathers | 612.436.0045 | [email protected] Minneapolis, MN | 55402 Deborah K. Vannelli, CCIM | 612.376.4475 | [email protected] www.nnnsales.com Look Upland. Where Properties & People Unite! Arby’s Restaurant CONFIDENTIALITY & DISCLAIMER Bemidji, MN NET LEASED DISCLAIMER Upland Real Estate Group, Inc. hereby advises all prospective purchasers of Net Leased property as follows: The information contained in this Marketing Package has been obtained from sources we believe to be reliable. However, Upland Real Estate Group, Inc. has not and will not verify any of this information, nor has Upland Real Estate Group, Inc. conducted any investigation regarding these matters. Upland Real Estate Group, Inc. makes no guarantee, warranty or representation whatsoever about the accuracy or completeness of any information provided. As the Buyer of a net leased property, it is the Buyer’s responsibility to independently confirm the accuracy and completeness of all material information before completing any purchase. This Marketing Package is not a substitute for your thorough due diligence investigation of this investment opportunity. Upland Real Estate Group, Inc. expressly denies any obligation to conduct a due diligence examination of this Property for Buyer. Any projections, opinions, assumptions or estimates used in this Marketing Package are for example only and do not represent the current or future performance of this property. The value of a net leased property to you depends on factors that should be evaluated by you and your tax, financial, legal and other advisors. -

F&B and Retail Performance Summary

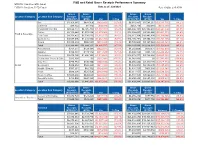

F&B and Retail Gross Receipts Performance Summary MTD PFY: Feb 20 vs. MTD: Feb 21 FYTD PY: Feb 20 vs. FYTD: Feb 21 Data as of: 2/28/2021 Run: 4/3/2021 2:45:35 PM 12:00:00 AM Gross Gross Gross Gross Location Category Location Sub Category Receipts Receipts Receipts Receipts (MTD PFY) (MTD) Var % Chg (FYTD PFY) (FYTD) Var % Chg Bar $1,304,445 $683,506 ($620,940) (47.6%) $6,915,987 $3,584,251 ($3,331,736) (48.2%) Cafeteria $94,422 $4,412 ($90,010) (95.3%) $563,776 $20,988 ($542,788) (96.3%) Casual Dining / Bar $8,622,777 $4,725,760 ($3,897,017) (45.2%) $46,204,191 $25,962,497 ($20,241,694) (43.8%) Coffee $2,113,840 $1,033,894 ($1,079,946) (51.1%) $12,008,453 $5,566,940 ($6,441,513) (53.6%) Food & Beverage Fast Food $4,732,427 $2,720,270 ($2,012,157) (42.5%) $26,617,764 $16,492,804 ($10,124,960) (38.0%) Quick Serve $3,087,096 $1,424,890 ($1,662,206) (53.8%) $16,105,292 $7,854,187 ($8,251,105) (51.2%) Snack $1,039,834 $506,591 ($533,243) (51.3%) $5,780,045 $3,187,024 ($2,593,021) (44.9%) Total $20,994,841 $11,099,323 ($9,895,517) (47.1%) $114,195,509 $62,668,691 ($51,526,818) (45.1%) Accessories $751,271 $129,194 ($622,077) (82.8%) $4,282,609 $879,671 ($3,402,938) (79.5%) Apparel $460,801 $149,112 ($311,689) (67.6%) $3,092,455 $864,193 ($2,228,262) (72.1%) Convenience $2,475,796 $1,456,149 ($1,019,648) (41.2%) $13,378,877 $8,728,854 ($4,650,022) (34.8%) Destination Themed Gifts $325,092 $0 ($325,092) (100.0%) $1,742,871 $0 ($1,742,871) (100.0%) Duty Free $778,784 $230,746 ($548,038) (70.4%) $6,056,484 $1,429,170 ($4,627,314) (76.4%) Retail -

CARIBOU COFFEE 520 JEFFERSON BOULEVARD • BIG LAKE, MN 55309 Affiliated Business Disclosure Property

BRAND NEW CONSTRUCTION COMPLETED DECEMBER 2019 FOR SALE CARIBOU COFFEE 520 JEFFERSON BOULEVARD • BIG LAKE, MN 55309 Affiliated Business Disclosure Property. All references to acreages, square footages, and other measurements are approximations. This Memorandum describes certain documents, including CBRE, Inc. operates within a global family of companies with many subsidiaries leases and other materials, in summary form. These summaries may not be and related entities (each an “Affiliate”) engaging in a broad range of commercial complete nor accurate descriptions of the full agreements referenced. Additional real estate businesses including, but not limited to, brokerage services, property information and an opportunity to inspect the Property may be made available and facilities management, valuation, investment fund management and to qualified prospective purchasers. You are advised to independently verify the development. At times different Affiliates, including CBRE Global Investors, Inc. accuracy and completeness of all summaries and information contained herein, or Trammell Crow Company, may have or represent clients who have competing to consult with independent legal and financial advisors, and carefully investigate interests in the same transaction. For example, Affiliates or their clients may the economics of this transaction and Property’s suitability for your needs. ANY have or express an interest in the property described in this Memorandum (the RELIANCE ON THE CONTENT OF THIS MEMORANDUM IS SOLELY AT “Property”), and may be the successful bidder for the Property. Your receipt YOUR OWN RISK. of this Memorandum constitutes your acknowledgment of that possibility and your agreement that neither CBRE, Inc. nor any Affiliate has an obligation to The Owner expressly reserves the right, at its sole discretion, to reject any or all disclose to you such Affiliates’ interest or involvement in the sale or purchase of expressions of interest or offers to purchase the Property, and/or to terminate the Property. -

Cadenza Document

VGM Club Report Date: Jul 2019 Contracted Manufacturer Report Mfr Name Has Rebate Has Pricing 3M Y Y Abbott Nutrition Y N ACH Food Companies Y N Advance Food Products LLC AFP Y Y AdvancePierre Y Y Agro Farma Inc Y Y Ajinomoto Windsor Inc (formerly Windsor Frozen Foods) Y N Allied Buying Corporation (ABC) Y N All Round Foods Bakery Products Y N Alpha Baking/National Baking Y N American Licorice Co Y N American Metalcraft Y N American Roland Food Corp Y N Amplify Snack Brands Y N Amy's Kitchen Inc Y N Anchor Packaging Y Y Antonio Mozzarella Factory Y N Appetizers And Inc Y Y Apple & Eve Y Y Argo Tea Y Y Arizona Tea - Hornell Brewing Company Y Y Armanino Foods Y Y Armour-Eckrich Meats LLC DBA Carando Y N Armour Eckrich - Smithfield Y Y Ateeco/Mrs T's Pierogies Y Y Atlantic Mills Co Y Y Awake Chocolate Y N Azar Nut Company Y N Bagcraft Packaging LLC Y N Bake N Joy Inc Y N Bakery De France Y Y Ballard Brands Y Y BarFresh Corporation Inc Y Y Barilla America Inc Y Y Basic American Food Co Y Y Bay Valley Foods LLC Y N Belgioioso Cheese Inc Y N Bel Kaukauna Cheese Co Y Y Berks Packing Co Inc Y N Berry Plastics Diet Kits Y N Berry Plastics Liners Y Y Beverage Air Y N Page 1 Of 9 VGM Club Report Date: Jul 2019 Contracted Manufacturer Report Mfr Name Has Rebate Has Pricing Beyond Meat Y Y B&G Foods Inc Y Y Big City Reds /American Foods Y N Big Red Inc Y Y BioSelect N Y Biscomerica Corp. -

BG Coffee 2021

BG Brunch Facts: Stone Ridge Golf Club and SamB's Restaurant serves buffet brunches during the holidays Baristas from Flatlands Coffee competed in the Specialty Coffee Association National Barista Bowling Green Championships C O F F E E T O U R A D D R E S S Grounds for Thought won an Arts and Business Partnership Award 217 S. Main St. from Americans for the Arts for Bowling Green, OH 43402 their involvement with the arts 1-800-866-0046 During Memorial Day weekend, Sunset Bistro and Broad Wing W E B S I T E Tattoo raise money for veterans through a tattooing event VisitBGOhio.org Did you know that Starbucks offers a Puppucino that consists C A L E N D E R / M A P / A P P of solely whipped cream? GoBGOhio.com Stimmel's Market sells over 200 dozen donuts during National Donut Day! S O C I A L M E D I A Craving some Bowling Green @VisitBGOhio coffee? Grounds for Thought and A S E L F - G U I D E D T O U R O F Flatlands have online stores for you to order your favorite roast! B O W L I N G G R E E N ' S C O F F E E A N D B R E A K F A S T S P O T S ! Slow Drippers Quick Fixes Biggby Coffee Panera Bread Everyday People Cafe: Juniper Brewing Company Bob Evans Starbucks A d d r e s s : A d d r e s s : 3 0 9 S M a i n S t r e e t 1 3 9 S M a i n S t r e e t Burger King Taco Bell Dunkin Donuts T h i s p o p u l a r b r u n c h s p o t f e a t u r e s m a n y J u n i p e r i s s e r v i n g u p d e l i c i o u s c o f f e e Subway u n i q u e c r e a t i o n s i n c l u d i n g a n e v e r d r i n k s a n d b r e a k f a s t i t e m s o f a l l k i n d s .