Trusted Knowledge Partner

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Labcorp and the Clinical Lab Testing Industry

UNITED STATES DISTRICT COURT MIDDLE DISTRICT OF NORTH CAROLINA GREENSBORO DIVISION ) SHERYL ANDERSON, MARY CARTER, ) TENA DAVIDSON, ROBERT ) HUFFSTUTLER, RAMZI KHAZEN, ) CASE NO. 1:17-cv-193 CHAIM MARCUS, LILY MARTYN, ) JONAH MCCAY, HOLDEN SHERIFF, ) VICTORIA SMITH, MICHELLE ) JURY TRIAL REQUESTED SULLIVAN, SHONTELLE THOMAS, ) JOSEPH WATSON, and MICHAEL ) WILSON individually and on behalf of all ) others similarly situated, ) ) Plaintiffs, ) ) vs. ) ) LABORATORY CORPORATION OF ) AMERICA HOLDINGS, ) ) Defendant. ) ) AMENDED CLASS ACTION COMPLAINT Case 1:17-cv-00193-TDS-JLW Document 42 Filed 08/10/18 Page 1 of 142 TABLE OF CONTENTS INTRODUCTION ............................................................................................................... 1 JURISDICTION AND VENUE .......................................................................................... 7 PARTIES ............................................................................................................................. 7 A. Plaintiffs .............................................................................................................. 7 B. Defendant ............................................................................................................ 9 FACTUAL ALLEGATIONS .............................................................................................. 9 A. LabCorp and the Clinical Lab Testing Industry ................................................. 9 B. LabCorp’s Business Model .............................................................................. -

Our Five Pillars Of

L aboratory Corporation of America 2011 Annual Report Our Five Pillars of ® Laboratory Corporation of America Holdings Success 358 South Main Street Burlington, NC 27215 336-584-5171 www.labcorp.com 2011 ANNUAL REPORT 120097_L01_CVR.indd 1 3/12/12 2:07 PM Laboratory Corporation OF America About LabCorp® Shareholder and Company Information Laboratory Corporation of America® Holdings, an S&P 500 company, is a pioneer in commercializing new diagnostic technologies and the first in its industry to embrace genomic testing. With annual revenues of $5.5 billion in 2011, over 31,000 employees worldwide, and more than 220,000 clients, LabCorp offers more than 4,000 tests Corporate Headquarters Transfer Agent Safe Harbor 358 South Main Street American Stock Transfer & Trust Company Forward-looking statements in this annual report ranging from routine blood analyses to reproductive genetics to companion diagnostics. Burlington, NC 27215 Shareholder Services are subject to change based on various important 336-584-5171 6201 Fifteenth Avenue factors, including without limitation, competitive LabCorp furthers its scientific expertise and innovative clinical testing technology Brooklyn, NY 11219 actions in the marketplace and adverse actions through its specialized labs and the LabCorp Specialty Testing Group: The Center for Information Sources 800-937-5449 of governmental and other third-party payers. Information about LabCorp is available from www.amstock.com Actual results could differ materially from those Molecular Biology and Pathology, National -

Membership | July 2021

Membership | July 2021 CLINICAL LABORATORY INDUSTRY/TRADE CureDuchenne Duke Center for Research Vanderbilt University TESTING SERVICES ASSOCIATIONS Emily’s Entourage on Personalized Health Medical Center Dasman Diabetes Institute American Clinical EveryLife Foundation for Care West Cancer Center Invitae Laboratory Association Rare Disease Essentia Institute of Rural Laboratory Corporation of BIO (Biotechnology Fight Colorectal Cancer Health RESEARCH TOOL America (LabCorp) Innovation Organization) Friends of Cancer European Infrastructure for COMPANIES Quest Diagnostics Biocom California Research Translational Medicine Octave Biosciences PhRMA GI Cancers Alliance Harvard Business School DIAGNOSTIC Global Liver Institute Hospital Albert Einstein STRATEGIC PARTNERS COMPANIES IT/INFORMATICS GO2 Foundation for Lung HudsonAlpha Institute for Accenture Admera Health COMPANIES Cancer Biotechnology Arnold & Porter Agendia NV 2bPrecise HealthyWomen iCAN – Digital Precision Artisan Healthcare Agilent Technologies Assurance Health Data International Cancer Cancer Medicine at Consulting Alacris Theranostics Change Healthcare Advocacy Network University of Helsinki Bioscience Valuation BSV GmbH Concert Genetics KRAS Kickers Instituto de Salud Carlos III GmbH Almac Diagnostics DNAnexus LUNGevity Foundation Intermountain Healthcare Blue Latitude Health Asuragen Flatiron Health Multiple Myeloma Johns Hopkins Boston Healthcare Caprion Proteomics GNS Healthcare Research Foundation Individualized Health Associates Caris Life Sciences M2Gen National Alliance -

Please See the Linked

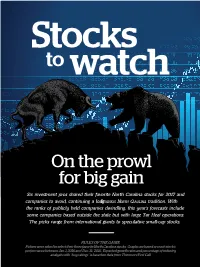

Stocks to watch On the prowl for big gain Six investment pros shared their favorite North Carolina stocks for 2017 and companies to avoid, continuing a longBUSINESS NORTH CAROLINA tradition. With the ranks of publicly held companies dwindling, this year’s forecasts include some companies based outside the state but with large Tar Heel operations. The picks range from international giants to speculative small-cap stocks. RULES OF THE GAME Pickers were asked to select their three favorite North Carolina stocks. Graphs are based on each stock’s performance between Jan. 1, 2016 and Dec. 13, 2016. Expected growth rates and percentage of industry 54 Business north analysts with Carolina “buy ratings” is based on data from Thomson/First Call. Ann Benjamin Zuraw Patrick Rush President, Zuraw Financial Advisors LLC, Chief executive officer, Triad Financial Advisors, Greensboro Greensboro (2%) 2% LOWE’S SYNGENTA COS. (LOW) AG (SYT) JAN ’16 ............................DEC ’16 JAN ’16 ............................DEC ’16 MARKET CAP: $63.4 BILLION MARKET CAP: $38.1 BILLION P/E RATIO: 27 EXPECTED FIVE-YEAR EPS GROWTH: 16% P/E RATIO: 31 EXPECTED FIVE-YEAR EPS GROWTH: 8% Lowe’s is the second-largest home-improvement retailer in the world A leading Swiss agricultural company with significant operations with 2,300 stores. Recent earnings were disappointing, particularly in in North Carolina, it is being acquired by ChemChina at about same-store sales growth compared with Home Depot, leaving a valu- $93 per share. Regulators are considering the buyout and have ation discount. More household formation and bank lending should delayed their decision, sparking speculation that the deal will be prompt more home-improvement spending. -

The CEO Action for Diversity & Inclusion™ Aims to Rally The

The CEO Action for Diversity & Inclusion™ aims to rally the business community to advance diversity & inclusion within the workplace by working collectively across organizations and sectors. It outlines a specific set of actions the undersigned companies will take to cultivate a trusting environment where all ideas are welcomed and employees feel comfortable and empowered to discuss diversity & inclusion. All the signatories serve as leaders of their companies and have committed to implementing the following pledge within their workplaces. Where companies have already implemented one or several of the commitments, the undersigned commit to support other companies in doing the same. The persistent inequities across our country underscore our urgent, national need to address and alleviate racial, ethnic and other tensions and to promote diversity within our communities. As leaders of some of America’s largest corporations, we manage thousands of employees and play a critical role in ensuring that inclusion is core to our workplace culture and that our businesses are representative of the communities we serve. Moreover, we know that diversity is good for the economy; it improves corporate performance, drives growth and enhances employee engagement. Simply put, organizations with diverse teams perform better. We recognize that diversity & inclusion are multifaceted issues and that we need to tackle these subjects holistically to better engage and support all underrepresented groups within business. To do this, we believe we also need to address honestly and head-on the concerns and needs of our diverse employees and increase equity for all, including Blacks, Latinos, Asians, Native Americans, LGBTQ, disabled, veterans and women. -

Quarterly Commentary

NELSON ROBERTS QUARTERLY COMMENTARY 2013 | FOURTH QUARTER ECONOMIC OVERVIEW The Good, The Bad and The Ugly INSIDE Wow! What a year. Think back for a moment to most of the Democratic Blue Dogs retired or voted THIS ISSUE where we were this time last year. At the end of the out of office and the Tea Party driving much of the last trading day of 2012, Congress had failed to Republican agenda. ECONOMIC OVERVIEW pass legislation to avert the Fiscal Cliff. This term However, the markets treated blustering politicians The Good, The Bad was coined by Fed Chairman Ben Bernanke to like the Boy Who Cried Wolf. Even as the US and The Ugly describe the tax increases and spending cuts that government shut down in early October and came previous laws had set for implementation on New closer to hitting the debt ceiling in the weeks that ASSET Year’s Day, 2013. Chairman Bernanke predicted MANAGEMENT followed, the market plodded along, inching ever The Year in Review that the combination of cuts and taxes would derail higher as investors realized that the brinksmanship the nascent recovery of the US economy. Financial FEATURED was an empty threat. It appears that some of our EQUITY Armageddon seemed imminent. Then at the 11th elected representatives have taken the failures of Bio-Reference Laboratories, Inc. (BRLI) hour on New Year’s Eve, the Senate passed a bill this political tactic to heart with the recent compromise that increased taxes on the wealthiest 2%. The spending bill engineered by Democratic Senator WEALTH House convened later that evening and also passed Patty Murray and Republican Congressman Paul MANAGEMENT News You Can Use: the bill. -

Laboratory Corporation of America Holdings (Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. ) Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐ Check the appropriate box: ☐ Preliminary Proxy Statement ☐ Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) ☒ Definitive Proxy Statement ☐ Definitive Additional Materials ☐ Soliciting Material under §240.14a-12 Laboratory Corporation of America Holdings (Name of Registrant as Specified In Its Charter) (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (Check the appropriate box): ☒ No fee required. ☐ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: ☐ Fee paid previously with preliminary materials. ☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. (1) Amount Previously Paid: (2) Form, Schedule or Registration Statement No.: (3) Filing Party: (4) Date Filed: Table of Contents Table of Contents DEAR SHAREHOLDER: “In 2020, we have a clear strategy that is focused on our customers and leverages our science, technology, and delivery to improve health and improve lives.” ADAM H. -

In the Court of Chancery of the State of Delaware

EFiled: Apr 28 2020 03:30PM EDT Transaction ID 65604938 Case No. 2020-0305-PAF IN THE COURT OF CHANCERY OF THE STATE OF DELAWARE RAYMOND EUGENIO, Derivatively on Behalf of Nominal Defendant, LABORATORY CORPORATION OF C.A. No. 2020-0305-PAF AMERICA HOLDINGS, Plaintiff, vs. LANCE V. BERBERIAN, GLENN A. EISENBERG, ADAM H. SCHECHTER, KERRII B. ANDERSON, JEAN-LUC BÉLINGARD, JEFFREY DAVIS, D. GARY GILLILAND, M.D., PH.D., DAVID P. KING, GARHENG KONG, M.D., PH.D., PETER M. NEUPERT, RICHELLE P. PARHAM, and R. SANDERS WILLIAMS, M.D., Defendants, and LABORATORY CORPORATION OF AMERICA HOLDINGS, Nominal Defendant. VERIFIED SHAREHOLDER DERIVATIVE COMPLAINT Plaintiff Raymond Eugenio (“Plaintiff”), by and through his undersigned attorneys, submits this Verified Shareholder Derivative Complaint (the “Complaint”) against defendants named herein. Plaintiff alleges the following based upon information and belief, except as to those allegations concerning Plaintiff, which are alleged upon personal knowledge. Plaintiff’s information and belief is based upon, among other things, the investigation conducted by and under the supervision of his counsel which included, among other things: (a) a review and analysis of regulatory filings filed by Laboratory Corporation of America Holdings (“LabCorp” or the “Company”) with the United States Securities and Exchange Commission (“SEC”); (b) documents produced by LabCorp pursuant to 8 Del. C. § 220; (c) a review and analysis of press releases and media reports issued and disseminated by LabCorp; (d) a review of other publicly available information concerning LabCorp, including articles in the news media and analyst reports; (e) complaints and related materials in litigation commenced against some or all of the Individual Defendants (defined below) and/or the Company; and (f) applicable rules and regulations. -

NOTICE of ANNUAL MEETING and PROXY STATEMENT Dear Fellow Shareholders

2020 NOTICE OF ANNUAL MEETING AND PROXY STATEMENT Dear Fellow Shareholders, I began writing this letter to review our 2019 performance and to discuss the promise of 2020 at the end of February. At that time, the performance trajectory that we had ended in 2019 had continued “Our teams are doing exactly through the first two months of 2020. At that moment, I was very optimistic that 2020 would be a very positive what they have been called year, perhaps the best our company has ever enjoyed. We have been transforming Tenet into a much different upon and trained to do, with company than we had two years ago when we started this turnaround effort, and were taking our performance honor and a selfless courage to the next level before the unfortunate events of the that has defined us as an COVID-19 pandemic unfolded several weeks ago. Today America is faced with one of the most organization and has made us challenging periods in our history. As a country, our world was turned upside down on December 7, 1941 an integral part of our communities.” when Pearl Harbor was attacked, and on September 11, 2001, and each time we came back stronger than ever. Our history as a country is to pick ourselves up and deal with adversity head on and with a resolve to win the conflict. This virus has been likened to a war with an invisible enemy and the warriors on the front lines committed to win are nurses, doctors, other skilled professionals, support personnel and hospital administrators. -

Laboratory Corporation of America Holdings

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 May 30, 2007 (Date of earliest event reported) LABORATORY CORPORATION OF AMERICA HOLDINGS (Exact Name of Registrant as Specified in its Charter) DELAWARE 1-11353 13-3757370 (State or other jurisdiction (Commission (I.R.S. Employer of Incorporation) File Number) Identification No.) 358 SOUTH MAIN STREET, 27215 336-229-1127 BURLINGTON, NORTH CAROLINA (Address of principal executive offices) (Zip Code) (Registrant's telephone number including area code) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) ITEM 7.01. Regulation FD Disclosure On May 30, 2007, Laboratory Corporation of America® Holdings (LabCorp®) (NYSE: LH), announced that David P. King, Chief Executive Officer, William B. (Brad) Hayes, Executive Vice President and Chief Financial Officer, and Bradford T. Smith, Executive Vice President, Corporate Affairs, are scheduled to speak at the Bank of America 2007 Health Care Conference in Las Vegas, NV. LabCorp’s presentation is planned for Thursday, May 31, 2007 at 10:40 a.m. -

Six Years Ago Labcorp Embarked on a Journey Guided by a Strategic Plan

LAB_015_CvrsL01v2.qxd 3/30/04 11:05 AM Page 1 Six years ago LabCorp embarked on a journey guided by a strategic plan. Today, this plan remains more relevant than ever. Laboratory Corporation of America 2003 Annual Report 358 South Main Street Burlington, NC 27215 336-584-5171 Annual Report 2003 www.labcorp.com LAB_015_CvrsL01v2.qxd 3/30/04 11:05 AM Page 2 DIRECTORS AND OFFICERS LABORATORY CORPORATION OF AMERICA® HOLDINGS 2003 LABCORP® BUSINESS DESCRIPTION LabCorp is the first commercial laboratory to fully embrace genomic testing. Through a national network of laboratories, LabCorp (LH) provides more than 4,400 clinical tests. The Company has 31 primary testing locations, more than 1,100 patient service centers and serves clients in all 50 states. Left to right: Wendy E. Lane, M. Keith Weikel, Ph.D., Andrew G. Wallace, M.D., James B. Powell, M.D., Robert E. Mittelstaedt, Jr., FINANCIAL HIGHLIGHTS Jean-Luc Bélingard, and Thomas P. Mac Mahon Laboratory Corporation of America® Holdings (in millions) BOARD OF DIRECTORS Thomas P. Mac Mahon James B. Powell, M.D. Year Ended December 31, 2003(a) 2002(b)(c) 2001(d) 2000(e) 1999 Chairman of the Board, President and Chief Executive Officer Director Statement of Operations Data: Former President and Chief Executive Officer Jean-Luc Bélingard of TriPath Imaging, Inc., a developer of analytical Net sales $2,939.4 $2,507.7 $2,199.8 $1,919.3 $1,698.7 Director systems for cytology and pathology Chief Executive Officer of Ipsen SA Gross profit 1,224.6 1,061.8 925.6 766.6 629.1 Committees: Audit, Ethics and Quality Assurance a diversified French health care holding company Operating income 533.7 435.0 367.6 245.6 149.7 Committees: Compensation, Ethics and Quality Assurance Andrew G. -

Florida Bill Would Squash False Claims Case Against

Volume 11, No. 1 January 2016 FLORIDA BILL WOULD SQUASH FALSE CLAIMS C ONTENTS CASE AGAINST QUEST AND LABCORP controversial bill sponsored by Florida State Representative Jay Trum- HEADLINE NEWS bull (R) seeks to retroactively define the term “usual and customary” for Florida Bill Would Squash A the purposes of billing Florida’s Medicaid program. If passed into state law, False Claims Lawsuit ......................1, 2-3 HB 421 would effectively kill a major false claims lawsuit that Florida Attor- Senators Pressure CMS on ney General Pam Bondi is aggressively pursuing against Quest Diagnostics PAMA Lab Test Reporting ..............1, 11 and LabCorp. Continued on page 2. Dr. Bostwick Starts New Lab Company ...............................1, 3-4 SENATORS PRESSURE CMS TO ADD HOSPITAL 2016 LAB OUTLOOK LABS AND DELAY PAMA REPORTING Exclusive Interviews with: ens. Orrin Hatch (R-Utah) and Ron Wyden (D-Oregon) on January 6 • Doug VanOort, NeoGenomics Surged the Centers for Medicare and Medicaid Services (CMS) to estab- • Ben Davis, MD, PathGroup lish a more expansive methodology for identifying laboratories that must • Colin Goldschmidt, MD, report private payment rates and give labs more time before they have to Sonic Healthcare begin reporting the payment rates. The proposed payment rule effectively • Dean Li, MD, ARUP Laboratories excludes hospital labs, which would result in lower prices once the new • Krista Crews, ProPath payment system is finalized. Continued on page 11. • Francisco Velazquez, MD, PAML SPECIAL NEW YEAR’S REPORT: • Ran Whitehead, PeaceHealth Labs LAB EXECS SHARE OUTLOOK FOR 2016 • David Goldberg, Enzo Clinical Labs or an inside look at what may be in store for the clinical lab and pa- • Khosrow Shotorbani, TriCore Labs Fthology business this year, Laboratory Economics interviewed the top • Panna Sharma, Cancer Genetics executives at a diverse group of 10 lab companies.