View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Het Oversteken Van De Vallei Van De Lasne Door De Pruisische Troepen Op 18 Juni 1815

The passage of the valley of the Lasne by the Prussian units on the 18th of June 1815. According to Von Bülow himself it was the information of major Von Falckenhausen which led Blücher to decide to cross the valley of the Lasne and to occupy the Bois de Paris. 1 Others believe it was major Von Lützow’s information which led Blücher to do so. 2 From shortly before 10 a.m. onwards, Von Lützow had, accompanied by lieutenant Von Massow and a detachment of the 2nd regiment of Silesian hussars (3), observed the positions of Wellington and Napoleon from a covered position in the western edge of the Bois de Paris. 4 Von Lützow reported to Blücher that the Bois de Paris was not occupied and that the French right flank wasn’t secured at all. Before he did so, Von Lützow left lieutenant Von Massow with the hussars behind in the wood. Some patrols had crossed the valley of the Lasne. One of them reported: Der Weg nach La Haye durch Lasne führend geht ziemlich sanft herunter das diesseitige Ufer ist bei weitem steiler. Der Weg ist, so lang das Defilée, mit 20 Fuss hohen Wenden eingeschlossen. … Der Bach der Lasne ist nur unbedeutend 2 bis 3 Fuss tief. [..] Block 5 It was Von Valentini himself, who, accompanied by a farmer and a private called Dieterichs, also acqainted himself with the fact that both the village of Lasne and the Bois de Paris were not occupied by the enemy. 6 After the 2nd regiment of Silesian hussars had entered Chapelle Saint Lambert, it detached one squadron to Lasne to verify whether it was occupied. -

Inbw Calendriers 2021 Lasne

Calendrier 2021 des collectes de déchets Commune de Lasne Téléchargez gratuitement l’application Recycle! pour tout connaître sur les collectes des déchets. PMC : vous serez averti personnellement lorsqu’il y aura du nouveau pour le sac bleu Ensemble Trions bien Recyclons mieux Janvier Février Mars Avril Mai Juin Juillet Août Septembre Octobre Novembre Décembre PMC 12-26 9-23 9-23 6-20 4-18 1-15-29 13-27 10-24 7-21 5-19 2-16-30 14-28 Papiers-cartons 5 2 2-30 27 25 22 20 17 14 12 9 7 Ordures ménagères Tous les mercredis (le lendemain en cas de jour férié) et organiques Encombrants Enlèvements à la demande (voir au verso) Déchets verts Les samedis 24/04 – 08/05 – 22/05 – 05/06 – 19/06 – 03/07 – 24/07 – 14/08 – 04/09 – 18/09 – 02/10 – 16/10 – 30/10 – 13/11 Pour de plus amples renseignements sur les collectes de déchets, voir au verso. Remarques importantes : Un problème concernant les collectes de déchets ou les bulles à verre ? Contactez in BW (votre intercommunale de gestion des déchets) • Les collectes commencent dès 6 h du matin (5 h en cas de canicule). Prière de sortir vos déchets la veille à partir de 18 h. 0800 49 057 • Placez-les à un endroit bien visible pour les collecteurs. • S’ils n’ont pas été collectés, contactez in BW (0800/49 057 ou [email protected] [email protected]) le jour même et laissez vos déchets sur le trottoir jusqu’au soir du jour ouvrable suivant. -

TEC Brabant Wallon

Aalst Brussegem Borgt Peutie Perk Wijgmaal-kern Houwaart Loksbergen Mollem Delle Kortrijk-Dutsel Grimbergen ¾B Berg ¿ B Molenbeek-Wersbeek Vilvoorde ¾¿ Bollebeek Nederokkerzeel Lignes régulières Putkapel Holsbeek Tielt ¾¿B Asse-Ter-Heide Krokegem Groot Molenveld 35 : Jodoigne - Grez-Doiceau 115 : Braine-l'Alleud - Tubize Parcours principalHamme Variante Tarification HORIZON + Waanrode Erembodegem 10 : Navette de La Hulpe 36 : Braine-l'Alleud - Wavre 116 : Soignies - Braine-le-Comte - Rebecq - Tubize - Halle Steenokkerzeel 11 : Ottignies - Einstein - Fleming 37 : Wavre Gare - Bierges Verseau 3 3 C : Louvain-la-Neuve - Wavre - Ixelles/ElseneMelsbroek 121 : Alsemberg Winderickxplein - Argenteuil Berlaymont Affligem Kobbegem Machelen 14 : Navette de Rixensart 38 : Rosières - Genval - Basse-Wavre 122 : Rhode-Saint-Genèse Clos Fleuri / Kortenaken Cbis : Louvain-la-Neuve - Wavre - Kraainem/CrainhemSTEENOKKERZEEL - Woluwe Asse ¾¿B 15 : Navette de Genval 40 : Uccle/Ukkel - Alsemberg - Braine-l'Alleud Sint-Genius-Rode Bloemenhof - Argenteuil Berlaymont ¾¿B 36 36 Strombeek-Bever Herent Sint-Joris-Winge 16 : Nivelles - Zoning Sud 43 : Tubize - Ittre Prison - Ittre Croiseau 123 : Bruxelles Midi / Brussel Zuid - Argenteuil Berlaymont Asbeek Wemmel Koningslo ¾¿B 17 : Ottignies - Clinique - Petit-Ry 47 : Tubize - Virginal - Ittre Croiseau 124 : Uccle Héros / Ukkel Helden - Argenteuil Berlaymont Veltem-Beisem¾¿B 71 Relegem 71 MACHELEN Attenhoven Kiezegem 1 : Jodoigne - Louvain-la-Neuve - Ottignies Tarification HORIZON + 18 : Leuven - Hamme-Mille - Jodoigne -

Centre Provincial De L'agriculture Et De La Ruralité

Edition 2016 Ed. Resp. Hervé Champagne, fonctionnaire de l’information – Province du Brbabant wallon, av. Einstein, 2 à 1300 Wavre Centre provincial de l’agriculture et de la ruralité L’agriculture brabançonne wallonne | Edition 2016 Centre provincial de l’agriculture et de la ruralité L’agriculture brabançonne wallonne | Edition 2016 Centre provincial de l’agriculture et de la ruralité 17, rue Saint-Nicolas. 1310 La Hulpe Téléphone : 02 656 09 70 - Télécopieur : 02 652 03 06 [email protected] Avec la participation de « Brabant wallon Agro-Qualité asbl » 3 Préambule ......................................................................................................................... 5 1. L’agriculture brabançonne wallonne, les chiffres clés ............................................. 6 2. Statistiques agricoles générales en Brabant wallon ................................................. 8 3. Le Brabant wallon parmi les autres provinces wallonnes ..................................... 9 4. Evolution du nombre d’exploitations agricoles ...................................................... 10 5. Evolution de la superficie agricole utilisée (SAU) ...................................................... 11 6. Superficie, rendements et productions en Brabant wallon...................................... 12 7. Evolution de la taille des exploitations agricoles ........................................................ 13 8. Perspectives de reprises d’exploitation ...................................................................... -

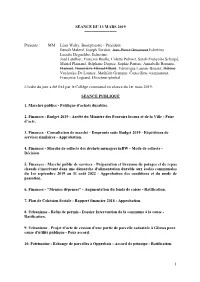

Procès Verbal Du Conseil Du 13 Mars 2019

SEANCE DU 13 MARS 2019 ============== Présents : MM Léon Walry, Bourgmestre - Président Benoît Malevé, Joseph Tordoir, Jean-Pierre Beaumont,Echevins Lucette Degueldre, Echevine; José Letellier, François Ruelle, Colette Prévost, Sarah-Françoise Scharpé, Muriel Flamand, Stéphane Deprez, Sophie Parisse, Annabelle Romain- Flament, Geneviève Flémal-Ottoul, Véronique Laenen-Bousez, Hélène Vuylsteke-De Lannoy, Mathilde Gramme, Conseillers communaux Françoise Legrand, Directeur général. L'ordre du jour a été fixé par le Collège communal en séance du 1er mars 2019. SEANCE PUBLIQUE 1. Marchés publics - Politique d'achats durables. 2. Finances - Budget 2019 - Arrêté du Ministre des Pouvoirs locaux et de la Ville - Prise d’acte. 3. Finances - Consultation de marché - Emprunts suite Budget 2019 - Répétitions de services similaires - Approbation. 4. Finances - Marché de collecte des déchets ménagers inBW - Mode de collecte - Décision 5. Finances - Marché public de services - Préparation et livraison de potages et de repas chauds s'inscrivant dans une démarche d'alimentation durable aux écoles communales du 1er septembre 2019 au 31 août 2022 - Approbation des conditions et du mode de passation. 6. Finances - "Menues dépenses" - Augmentation du fonds de caisse - Ratification. 7. Plan de Cohésion Sociale - Rapport financier 2018 - Approbation. 8. Urbanisme - Refus de permis - Dossier Intervention de la commune à la cause - Ratification. 9. Urbanisme - Projet d'acte de cession d'une partie de parcelle cadastrée à Glimes pour cause d'utilité publique - Pour accord. 10. Patrimoine - Echange de parcelles à Opprebais - Accord de principe - Ratification. 1 11. Travaux - Marché public de fournitures - Rénovation et mise en place d'un système de chauffage à l'église d'Opprebais - Mode et conditions de passation du marché - Approbation. -

Court-Saint-Etienne Plan Communal De Mobilité Phase 3

Court-Saint-Etienne Plan Communal de Mobilité Phase 3 - Plan d'action 14 février 2011 Association momentanée En collaboration avec Tables des matières 1 INTRODUCTION..............................................................................................................3 1.1 Rappel des objectifs du PCM .................................................................................................................... 3 1.2 Le présent document................................................................................................................................. 4 2 AMENAGEMENT DU TERRITOIRE ................................................................................5 3 LE RESEAU ROUTIER....................................................................................................6 3.1 Hiérarchisation du réseau.......................................................................................................................... 6 3.2 Le centre de Court-Saint-Etienne ............................................................................................................ 10 3.3 Gestion des vitesses ............................................................................................................................... 13 3.4 Principes d'aménagement des routes régionales .................................................................................... 15 3.5 Modération de la vitesse......................................................................................................................... -

Relive and Refight the Battle of Waterloo CONTENTS

For 2 Players Ages 12 & Up ® Rules of the game Relive and refight the battle of Waterloo www.stratego.com CONTENTS INTRO 2 PART II CONTENTS 2 STANDARD GAME 7 THE GAME 2 10. TERRAIN TILES 7 11. MANEUVER CARDS 8 PART I THE BASICS 3 PART III 1. WINNING THE GAME 3 EXPERT GAME 9 2. SET-UP 3 12. PLANCENOIT 9 3. LINES OF RETREAT 3 13. THE PURSUIT 10 4. THE PIECES 4/5 14. EXTRA SCENARIOS 10/11 5. THE COMMANDERS 5 GAME PIECES 12/13 6. ARMY SET UP 5 7. MOVEMENT 6 8. ATTACK 6 9. THE PRUSSIANS ARRIVE! 6 ® “Napoleon regained his Empire by simply showing his Hat.” Quote from Honoré de Balzac. After having ruled over 80 million people, subdued the greater CONTENTS part of the continent and influenced European politics for almost 20 years, Napoleon Bonaparte, Emperor of the French, was • 47 x Blue Pieces finally driven into exile in April 1814 by the armies of Austria, • 45 x Red Pieces Prussia and Russia. From his island on Elba off the Italian coast, • 13 x Black Pieces he watched France under the restored Bourbon monarchy writhe • 1 x Game Board in confusion and unrest. In February 1815, convinced that the • 1 x Battle Die army would fight for him as they had done in the past from the hot • 2 x Hill Tiles sands of Egypt to the cold snows of Russia, Napoleon escaped and • 2 x Mud Tiles returned to France. The leaders of the European powers, gathered • 3 x Building Tiles at the Congress of Vienna, swore no peace with Bonaparte, • 15 x Maneuver Cards branded him an outlaw and hurried to take up arms again. -

Le Brabant Wallon En Chiffres Fondation Economique Et Sociale Du Brabant Wallon

EDITION 2017 LE BRABANT WALLON EN CHIFFRES FONDATION ECONOMIQUE ET SOCIALE DU BRABANT WALLON LE BRABANT WALLON EN CHIFFRES | 01 TABLE LA PROVINCE DU BRABANT WALLON DES MATIÈRES EN QUELQUES DONNÉES La Province du Brabant wallon Beauvechain en quelques données 03 Hélécine Grez-Doiceau La Hulpe Introduction 04 Jodoigne Waterloo Rixensart Wavre Chapitre 1 : Population 06 Chaumont- Gistoux Orp-Jauche Tubize Incourt Braine-le- Lasne Château Braine- l’Alleud Ottignies-LLN Chapitre 2 : Niveau de vie 16 Rebecq Mont- Ramillies Ittre St-Guibert Perwez Chapitre 3 : Enseignement et formation 24 Court- Walhain St-Etienne Genappe Chapitre 4 : Emploi et chômage 40 Nivelles Chastre Chapitre 5 : Activité économique 47 Villers-la-Ville Chapitre 6 : Activités et entreprises 58 Chapitre 7 : Occupation du territoire et prix 64 Annexe Top 100 des entreprises du Brabant wallon La Province du Brabant wallon c’est : au niveau de l’emploi localisé 71 • Une des 5 provinces de la Wallonie. • Un seul arrondissement judiciaire et administratif qui regroupe 27 communes dont Wavre est le chef-lieu. • Un territoire d’une superficie de 1.091 km2 (soit 3,6% du territoire national et 6,5% du territoire wallon). • Une population de 396.840 habitants au 1er janvier 2016. • Une situation géographique privilégiée au cœur de l’Europe : • limitrophe de Bruxelles, capitale européenne • voisine de la Région flamande • traversée par ou à proximité des grands axes autoroutiers et ferroviaires : E411, E40, E19, A8, N25 et les lignes 124, 140, 161 renforcées par le futur RER • Un cadre de vie et de travail agréable et diversifié. • Une fiscalité, pour certaines communes, parmi les plus basses de Wallonie . -

Votre Commune En Chiffres: Court-Saint-Etienne

Votre commune en chiffres: Court-Saint-Etienne Votre commune en chiffres: Court-Saint-Etienne SPF Economie, DG Statistique et information ´economique SPF Economie, DG Statistique et information ´economique Votre commune en chiffres: Court-Saint-Etienne Votre commune en chiffres: Court-Saint-Etienne Introduction Court-Saint-Etienne : Court-Saint-Etienne est une commune de la province de Brabant wallon et fait partie de la R´egion wallonne. Ses communes voisines sont Chastre, Genappe, Mont-Saint-Guibert, Ottignies-Louvain-la-Neuve et Villers-la-Ville. Court-Saint-Etienne a une superficie de 26,6 km2 et compte 9.943 ∗ habitants, soit une densit´ede 373,2 habitants par km2. 63% ∗ de sa population a entre 18 et 64 ans. Parmi les 589 communes belges, elle se situe `ala 139`eme y place par rapport au revenu moyen net par habitant le plus ´elev´eet `ala 344`eme z place par rapport aux prix des terrains `ab^atir les plus chers. ∗. Situation au 1/1/2011 y. Revenus de l'ann´ee2009 - Exercice d'imposition 2010 z. Ann´eede r´ef´erence : 2011 SPF Economie, DG Statistique et information ´economique Votre commune en chiffres: Court-Saint-Etienne Votre commune en chiffres: Court-Saint-Etienne Table des mati`eres 1 Table des mati`eres 2 Population Composition de la population Pyramide des ^ages pour Court-Saint-Etienne 3 Territoire Densit´ede population pour Court-Saint-Etienne et ses communes limitrophes Occupation du sol 4 Immobilier Prix des terrains `ab^atir en Belgique Prix des terrains `ab^atir pour Court-Saint-Etienne et environs Prix des terrains `ab^atir -

'No Troops but the British': British National Identity and the Battle For

‘No Troops but the British’: British National Identity and the Battle for Waterloo Kyle van Beurden BA/BBus (Accy) (QUT), BA Honours (UQ) A thesis submitted for the degree of Master of Philosophy at The University of Queensland in 2015 School of Historical and Philosophical Inquiry British National Identity and the Battle for Waterloo Kyle van Beurden Abstract In the ‘long eighteenth-century’ British national identity was superimposed over pre-existing identities in Britain in order to bring together the somewhat disparate, often warring, states. This identity centred on war with France; the French were conceptualised as the ‘other’, being seen by the British as both different and inferior. For many historians this identity, built in reaction and opposition to France, dissipated following the defeat of Napoleon at Waterloo in 1815, as Britain gradually introduced changes that allowed broader sections of the population to engage in the political process. A new militaristic identity did not reappear in Britain until the 1850s, following the Crimean War and the Indian Mutiny. This identity did not fixate on France, but rather saw all foreign nations as different and, consequently, inferior. An additional change was the increasing public interest in the army and war, more generally. War became viewed as a ‘pleasurable endeavour’ in which Britons had an innate skill and the army became seen as representative of that fact, rather than an outlet to dispose of undesirable elements of the population, as it had been in the past. British identity became increasingly militaristic in the lead up to the First World War. However, these two identities have been seen as separate phenomena, rather than the later identity being a progression of the earlier construct. -

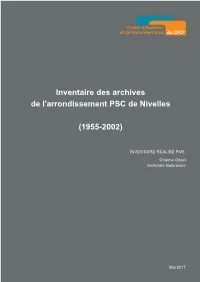

Inventaire Des Archives De L'arrondissement PSC De Nivelles

INVENTAIRE RÉALISÉ PAR : TABLE DES MATIÈRES Table des matières ...................................................................................................................... 1 Description générale du fonds .................................................................................................... 3 A. Identification ..................................................................................................................... 3 B. Histoire du producteur et des archives .............................................................................. 3 B.I. Histoire du producteur ................................................................................................. 3 B.II. Histoire des archives .................................................................................................. 4 C. Contenu et structure ........................................................................................................... 4 C.I. Contenu ....................................................................................................................... 4 C.II. Sélection et élimination .............................................................................................. 5 C.III. Accroissement .......................................................................................................... 5 C.IV. Mode de classement ................................................................................................. 5 D. Consultation et utilisation ................................................................................................. -

Une Boucle Pédestre De 38 Km Pour Relier L'abbaye De Villers-La-Ville À

www.globaldesign.be 2015 Février : Edition – D/2015/10.966/3 : légal Dépôt Stéphane Colin, Président - MTPVBW - Président Colin, Stéphane Une boucle pédestre de 38 km pour relier l’Abbaye de Villers-la-Ville à la Butte du Lion dit de Waterloo. Editeur responsable : : responsable Editeur P Cette boucle peut être entreprise tant depuis Waterloo que depuis Villers-la-Ville. R1 à R5 3 P P P Elle permet de découvrir des villages et leur patrimoine historique, P 1 2 4 9 parcourir chemins et sentiers, apprécier H3 la beauté des paysages champêtres. R0R P et de la Province du Brabant wallon Brabant du Province la de et 8 Cette balade off re une belle occasion de Avec le soutien du Commissariat général au Tourisme de Wallonie de Tourisme au général Commissariat du soutien le Avec N5 Chaussée de Charleroi Couture H5 Saint-Germain (re)découvrir le patrimoine naturel, P Donnez-nous votre feedback après votre balade ! ! balade votre après feedback votre Donnez-nous bâti et rural de toute beauté de P 7 6 cette région du Brabant wallon. www.waterloo-tourisme.com [email protected] [email protected] P Non accessible aux Tél. +32 (0)2 352 09 10 09 352 (0)2 +32 Tél. 5 poussettes/buggies. 218 chaussée de Bruxelles - 1410 Waterloo 1410 - Bruxelles de chaussée 218 Maison du Tourisme de Waterloo de Tourisme du Maison H4 R7 Maransart sur votre smartphone ou votre tablette. votre ou smartphone votre sur N5 ou via l’appli «Rando Around Villers-la-Ville» Villers-la-Ville» Around «Rando l’appli via ou Plancenoit www.paysdevillers-tourisme.be - onglet «Bouger» (format pdf) pdf) (format «Bouger» onglet - www.paysdevillers-tourisme.be Découvrez et téléchargez gratuitement d’autres balades sur sur balades d’autres gratuitement téléchargez et Découvrez Hébergements situés à moins de 5 km du circuit www.facebook.com/paysdevillers www.facebook.com/paysdevillers (H1-H2-H3-H7-H8-H9 : hors carte) www.paysdevillers-tourisme.be Les hébergements repris ici sont situés à moins de 5 km du circuit.