General Diagnostic Tests for Cross Section Dependence in Panels

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Signalling Virtue, Promoting Harm: Unhealthy Commodity Industries and COVID-19

SIGNALLING VIRTUE, PROMOTING HARM Unhealthy commodity industries and COVID-19 Acknowledgements This report was written by Jeff Collin, Global Health Policy Unit, University of Edinburgh, SPECTRUM; Rob Ralston, Global Health Policy Unit, University of Edinburgh, SPECTRUM; Sarah Hill, Global Health Policy Unit, University of Edinburgh, SPECTRUM; Lucinda Westerman, NCD Alliance. NCD Alliance and SPECTRUM wish to thank the many individuals and organisations who generously contributed to the crowdsourcing initiative on which this report is based. The authors wish to thank the following individuals for contributions to the report and project: Claire Leppold, Rachel Barry, Katie Dain, Nina Renshaw and those who contributed testimonies to the report, including those who wish to remain anonymous. Editorial coordination: Jimena Márquez Design, layout, illustrations and infographics: Mar Nieto © 2020 NCD Alliance, SPECTRUM Published by the NCD Alliance & SPECTRUM Suggested citation Collin J; Ralston R; Hill SE, Westerman L (2020) Signalling Virtue, Promoting Harm: Unhealthy commodity industries and COVID-19. NCD Alliance, SPECTRUM Table of contents Executive Summary 4 INTRODUCTION 6 Our approach to mapping industry responses 7 Using this report 9 CHAPTER I ADAPTING MARKETING AND PROMOTIONS TO LEVERAGE THE PANDEMIC 11 1. Putting a halo on unhealthy commodities: Appropriating front line workers 11 2. ‘Combatting the pandemic’ via marketing and promotions 13 3. Selling social distancing, commodifying PPE 14 4. Accelerating digitalisation, increasing availability 15 CHAPTER II CORPORATE SOCIAL RESPONSIBILITY AND PHILANTHROPY 18 1. Supporting communities to protect core interests 18 2. Addressing shortages and health systems strengthening 19 3. Corporate philanthropy and COVID-19 funds 21 4. Creating “solutions”, shaping the agenda 22 CHAPTER III PURSUING PARTNERSHIPS, COVETING COLLABORATION 23 1. -

Directory of Fire Safe Certified Cigarette Brand Styles Updated 11/20/09

Directory of Fire Safe Certified Cigarette Brand Styles Updated 11/20/09 Beginning August 1, 2008, only the cigarette brands and styles listed below are allowed to be imported, stamped and/or sold in the State of Alaska. Per AS 18.74, these brands must be marked as fire safe on the packaging. The brand styles listed below have been certified as fire safe by the State Fire Marshall, bear the "FSC" marking. There is an exception to these requirements. The new fire safe law allows for the sale of cigarettes that are not fire safe and do not have the "FSC" marking as long as they were stamped and in the State of Alaska before August 1, 2008 and found on the "Directory of MSA Compliant Cigarette & RYO Brands." Filter/ Non- Brand Style Length Circ. Filter Pkg. Descr. Manufacturer 1839 Full Flavor 82.7 24.60 Filter Hard Pack U.S. Flue-Cured Tobacco Growers, Inc. 1839 Full Flavor 97 24.60 Filter Hard Pack U.S. Flue-Cured Tobacco Growers, Inc. 1839 Full Flavor 83 24.60 Non-Filter Soft Pack U.S. Flue-Cured Tobacco Growers, Inc. 1839 Light 83 24.40 Filter Hard Pack U.S. Flue-Cured Tobacco Growers, Inc. 1839 Light 97 24.50 Filter Hard Pack U.S. Flue-Cured Tobacco Growers, Inc. 1839 Menthol 97 24.50 Filter Hard Pack U.S. Flue-Cured Tobacco Growers, Inc. 1839 Menthol 83 24.60 Filter Hard Pack U.S. Flue-Cured Tobacco Growers, Inc. 1839 Menthol Light 83 24.50 Filter Hard Pack U.S. -

Sampoerna University

SU Catalogue 2018-2019 1 WELCOME TO SAMPOERNA UNIVERSITY Welcome to Sampoerna University. We would like to congratulate each of you, our students, for your achievement in As the future of Indonesia lies in your hands, we hope that you will use your time becoming a member of the Sampoerna University community. here at Sampoerna University to gain the knowledge and skills required when you enter the professional world. It is a world where you will have to compete in Sampoerna University will provide you with an international education as you the labor force in all the ASEAN countries and beyond. study the discipline of your choice. We have established collaborations with overseas universities to ensure that you will have a pathway to your future In addition to knowledge, we hope that you will develop comprehensive social with international recognition. Our campus is the ideal place for developing and skills and moral values that will empower you to make meaningful contributions achieving your intellectual potential. to your community. Social competencies include empathy and awareness of other people, ability to listen to and understand disparate views, as well as to You will follow the learning process in different study programs in a broad range communicate across social differences. With these social competencies, we are of subjects. However, the variety of these subjects should not segregate you from confident that our students can work as a team, assume constructive roles in your fellow students undertaking other study programs. The interdisciplinary the community, and become wise and caring human beings. courses and dialogue between all fields of study are at the core of our curriculum. -

Cigarette Minimum Retail Price List

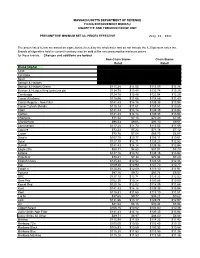

MASSACHUSETTS DEPARTMENT OF REVENUE FILING ENFORCEMENT BUREAU CIGARETTE AND TOBACCO EXCISE UNIT PRESUMPTIVE MINIMUM RETAIL PRICES EFFECTIVE July 26, 2021 The prices listed below are based on cigarettes delivered by the wholesaler and do not include the 6.25 percent sales tax. Brands of cigarettes held in current inventory may be sold at the new presumptive minimum prices for those brands. Changes and additions are bolded. Non-Chain Stores Chain Stores Retail Retail Brand (Alpha) Carton Pack Carton Pack 1839 $86.64 $8.66 $85.38 $8.54 1st Class $71.49 $7.15 $70.44 $7.04 Basic $122.21 $12.22 $120.41 $12.04 Benson & Hedges $136.55 $13.66 $134.54 $13.45 Benson & Hedges Green $115.28 $11.53 $113.59 $11.36 Benson & Hedges King (princess pk) $134.75 $13.48 $132.78 $13.28 Cambridge $124.78 $12.48 $122.94 $12.29 Camel All others $116.56 $11.66 $114.85 $11.49 Camel Regular - Non Filter $141.43 $14.14 $139.35 $13.94 Camel Turkish Blends $110.14 $11.01 $108.51 $10.85 Capri $141.43 $14.14 $139.35 $13.94 Carlton $141.43 $14.14 $139.35 $13.94 Checkers $71.54 $7.15 $70.49 $7.05 Chesterfield $96.53 $9.65 $95.10 $9.51 Commander $117.28 $11.73 $115.55 $11.56 Couture $72.23 $7.22 $71.16 $7.12 Crown $70.76 $7.08 $69.73 $6.97 Dave's $107.70 $10.77 $106.11 $10.61 Doral $127.10 $12.71 $125.23 $12.52 Dunhill $141.43 $14.14 $139.35 $13.94 Eagle 20's $88.31 $8.83 $87.01 $8.70 Eclipse $137.16 $13.72 $135.15 $13.52 Edgefield $73.41 $7.34 $72.34 $7.23 English Ovals $125.44 $12.54 $123.59 $12.36 Eve $109.30 $10.93 $107.70 $10.77 Export A $120.88 $12.09 $119.10 $11.91 -

Front Matter

Cambridge University Press 978-1-108-84489-5 — A Concise History of Greece Richard Clogg Frontmatter More Information cambridge concise histories A Concise History of Greece Now reissued in a fourth, updated edition, this book provides a concise, illustrated introduction to the modern history of Greece, from the irst stirrings of the national movement in the late eighteenth century to the present day. As Greece emerges from a devastating economic crisis, this fourth edition offers analyses of contemporary political, economic and social devel- opments. It includes additional illustrations, together with updated tables and suggestions for further reading. A new concluding chapter considers the trajectory of Greek history over the two hundred years since the beginning of the War of Independence in 1821. Designed to provide a basic introduc- tion, the irst edition of this hugely successful Concise History won the Runciman Award for a best book on an Hellenic topic in 1992 and has been translated into thirteen languages, including all the languages of the Balkans. richard clogg has been lecturer in Modern Greek History at the School of Slavonic and East European Studies and King’s College, University of London; Reader in Modern Greek History at King’s College; and Professor of Modern Balkan History in the University of London. From 1990 to 2005 he was a Fellow of St Antony’s College, Oxford, of which he is now an Emeritus Fellow. He has written extensively on Greek history and politics from the eighteenth century to the present. His most recent book is Greek to Me: A Memoir of Academic Life (2018). -

Altria Group, Inc. 2013 Annual Report

Altria Group, Inc. 2013 Annual Report altria.com Altria’s Operating Companies Philip Morris USA Inc. (PM USA) Philip Morris USA is the largest tobacco company in the U.S. and has about half of the U.S. cigarette market’s retail share. Altria Group, Inc. U.S. Smokeless Tobacco Company LLC (USSTC) U.S. Smokeless Tobacco Company is the n an Altria Company largest producer and marketer of moist Annual Report 2013 smokeless tobacco, one of the fastest growing tobacco segments in the U.S. John Middleton Co. (Middleton) John Middleton is a leading manufacturer of machine-made large cigars and pipe tobacco. Ste. Michelle Wine Estates Ltd. (Ste. Michelle) Ste. Michelle Wine Estates ranks among the top-ten producers of premium wines in the U.S. Nu Mark LLC (Nu Mark) Nu Mark is focused on responsibly developing and marketing innovative tobacco products for adult tobacco consumers. Philip Morris Capital Corporation (PMCC) Philip Morris Capital Corporation manages an existing portfolio of leveraged and direct finance lease investments. Altria Group, Inc. 6601 W. Broad Street Richmond, VA 23230-1723 Our Mission is to own and develop financially disciplined Shareholder Information businesses that are leaders in responsibly providing adult tobacco and wine consumers with superior branded products. Shareholder Response Center: Direct Stock Purchase and If you do not have Internet Stock Computershare Trust Company, Dividend Reinvestment Plan: access, you may call: Exchange Listing: N.A. (Computershare), our trans- Altria Group, Inc. offers a Direct 1-804-484-8222 The principal stock fer agent, will be happy to answer Stock Purchase and Dividend exchange on which questions about your accounts, Reinvestment Plan, administered Internet Access Altria Group, Inc.’s certificates, dividends or the by Computershare. -

Page 1 of 15

Updated September14, 2021– 9:00 p.m. Date of Next Known Updates/Changes: *Please print this page for your own records* If there are any questions regarding pricing of brands or brands not listed, contact Heather Lynch at (317) 691-4826 or [email protected]. EMAIL is preferred. For a list of licensed wholesalers to purchase cigarettes and other tobacco products from - click here. For information on which brands can be legally sold in Indiana and those that are, or are about to be delisted - click here. *** PLEASE sign up for GovDelivery with your EMAIL and subscribe to “Tobacco Industry” (as well as any other topic you are interested in) Future lists will be pushed to you every time it is updated. *** https://public.govdelivery.com/accounts/INATC/subscriber/new RECENTLY Changed / Updated: 09/14/2021- Changes to LD Club and Tobaccoville 09/07/2021- Update to some ITG list prices and buydowns; Correction to Pall Mall buydown 09/02/2021- Change to Nasco SF pricing 08/30/2021- Changes to all Marlboro and some RJ pricing 08/18/2021- Change to Marlboro Temp. Buydown pricing 08/17/2021- PM List Price Increase and Temp buydown on all Marlboro 01/26/2021- PLEASE SUBSCRIBE TO GOVDELIVERY EMAIL LIST TO RECEIVE UPDATED PRICING SHEET 6/26/2020- ***RETAILER UNDER 21 TOBACCO***(EFF. JULY 1) (on last page after delisting) Minimum Minimum Date of Wholesale Wholesale Cigarette Retail Retail Brand List Manufacturer Website Price NOT Price Brand Price Per Price Per Update Delivered Delivered Carton Pack Premier Mfg. / U.S. 1839 Flare-Cured Tobacco 7/15/2021 $42.76 $4.28 $44.00 $44.21 Growers Premier Mfg. -

Tobacco Compliant List by Brand Name ______

OKLAHOMA OFFICE OF ATTORNEY GENERAL TOBACCO ENFORCEMENT UNIT 313 NW 21st STREET OKLAHOMA CITY, OKLAHOMA 73105-3207 _____________________________________________________________________________ Tobacco Compliant List by Brand Name _________________________________________ 1839 (RYO) – PM - (Premier Manufacturing, Inc.) 1839 – PM - (Premier Manufacturing, Inc.) 24/7 – NPM - (Xcaliber International Ltd., LLC) 305 – NPM - (Dosal Tobacco Company) American Bison – PM - (Wind River Tobacco Company) American Bison (RYO) – PM - (Wind River Tobacco Company) Aura – NPM - (Cheyenne International, LLC) Bali Shag (RYO) – PM - (Top Tobacco, LP) Basic – PM - (Philip Morris, USA) Benson & Hedges – PM - (Philip Morris, USA) Berkley (FL, MS, TX only) – NPM - (Xcaliber International Ltd., LLC) Berley – NPM - (Xcaliber International Ltd., LLC) Bronson – PM - (Liggett Group LLC) Bugler (RYO) – PM - (Scandinavian Tobacco Group Lane Limited) Cambridge – PM – (Philip Morris, USA) Camel – PM - (R.J. Reynolds Tobacco Company) Camel Wides – PM - (R.J. Reynolds Tobacco Company) Canoe (RYO) – PM - (Wind River Tobacco Company) Capri – PM - (R.J. Reynolds Tobacco Company) Effective 06/01/2021 Carlton – PM - (R.J. Reynolds Tobacco Company) Carnival – NPM - (KT&G Corporation) Chesterfield – PM - (Philip Morris, USA) Cheyenne – NPM - (Cheyenne International, LLC) Crowns – PM - (Commonwealth Brands, Inc.) DTC – NPM - (Dosal Tobacco Company) Decade – NPM - (Cheyenne International, LLC) Doral – PM - (R.J. Reynolds Tobacco Company) Drum (RYO) – PM - (Top Tobacco, LP) Dunhill -

A Concise History of Greece

A Concise History of Greece richard clogg published by the press syndicate of the university of cambridge The Pitt Building, Trumpington Street, Cambridge, United Kingdom cambridge university press The Edinburgh Building, Cambridge cb2 2ru,UK 40 West 20th Street, New York, ny 10011-4211,USA 477 Williamstown Road, Port Melbourne, vic 3207, Australia Ruiz de Alarcon´ 13, 28014 Madrid, Spain Dock House, The Waterfront, Cape Town 8001, South Africa http://www.cambridge.org C Cambridge University Press 1992 This book is in copyright. Subject to statutory exception and to the provisions of relevant collective licensing agreements, no reproduction of any part may take place without the written permission of Cambridge University Press. First published 1992 Reprinted 5 times Second edition 2002 Printed in the United Kingdom at the University Press, Cambridge Typeface Sabon 10/13 pt. System LATEX 2ε [TB] A catalogue record for this book is available from the British Library Library of Congress Cataloguing in Publication Data Clogg, Richard, 1939– A concise history of Greece / Richard Clogg. p. cm. – (Cambridge concise histories) Includes bibliographical references and index. isbn 0 521 80872 3 – isbn 0 521 00479 9 (pbk) 1. Greece – History – 1821– i. Title ii. Series. df802.C57 1991 949.5-dc20 91–25872 CIP isbn 0 521 80872 3 hardback isbn 0 521 00479 9 paperback contents List of illustrations page viii Preface xv 1 Introduction 1 2 Ottoman rule and the emergence of the Greek state 1770–1831 7 3 Nation building, the ‘Great Idea’ and National Schism -

An International Education System in Indonesia

sampoernaacademy.sch.id Critical Thinking Creativity Collaboration An International Education System in Indonesia i Table of Contents Message from the Director 2 About STEAM Education 4 Our Unique Education System 6 Student Achievements 8 Facilities 12 Levels Offered 14 Pre-School 16 Elementary 18 Middle School 20 High School 22 Parents and Students Testimonials 24 ii 1 Students today live in a vastly different era from that MESSAGE FROM of their parents. Learning is not confined solely to the THE DIRECTOR classroom. It exists at any time and in any place. Is your child equipped to deal with this new reality? Dr. Mustafa Guvercin Putera Sampoerna Director of Sampoerna Academy Strongest Sampoerna Academy is an educational institution that upholds Curriculum Asian values at the forefront of learning. Since its first establishment, the Academy have been producing passionate lifelong learners Project who are able to meet the challenges of the rapidly changing Based world, and who care deeply for their fellows and the environment. Learning Blended The Right Learning The high quality education provided in Sampoerna Academy is not accidental, but intentional. In our schools, we instill 21st Education for Century Skills within the Cambridge International Examination Personalized Your Child Learning curriculum. We also believe that children learn more by doing. Experience This is why Project Based Learning and STEAM Education are at the core of our teaching philosophy. Academic Quality The era of globalization and the ASEAN Economic Community Multiple International has greatly impacted Indonesia. Among them is the increased Languages Benchmarking competitiveness as the job market became global. Furthermore, technology advancement has caused a significant shifting in our lives, and transformed business models in all sectors. -

Iowa Cigarette Brand List

Iowa Directory of Certified Tobacco Product Manufacturers and Brands PLEASE NOTE Flavored Cigarettes & RYO are now illegal. Regardless of being on this List. See footnote *(3) 8/12/20 Iowa Additions to the Directory (within the last six months) PM Nat's Philip Morris USA cigarettes 8/12/20 PM Montego Liggett Group Inc. cigarettes 6/8/20 Deletions to the Directory (within the last six months) PM Nat's Sherman 1400 Broadway NYC, Ltd. cigarettes 8/12/20 PM Ace King Maker Marketing cigarettes 5/7/20 PM Dreams Kretek International cigarettes 5/7/20 PM Gold Crest King Maker Marketing cigarettes 5/7/20 PM Wings Japan Tobacco International cigarettes 5/7/20 Type of Manufacturer is for Participating (PM) or Non-Participating (NPM) with the Master Settlement Agreement. TYPE BRAND MANUFACTURER PRODUCT DATE PM 1839 Premier Manufacturing cigarettes 10/1/14 PM 1839 Premier Manufacturing roll your own 10/1/14 NPM 24/7 Xcaliber International Ltd. cigarettes 12/13/18 PM American Bison Wind River Tobacco Co., LLC roll your own 7/22/03 NPM Aura Cheyenne International, LLC cigarettes 8/4/10 PM Bali Shag Top Tobacco, L.P. roll your own 11/9/18 PM Baron American Blend Farmers Tobacco Company of Cynthiana, Inc. cigarettes 9/20/05 PM Basic Philip Morris USA cigarettes 7/22/03 PM Benson & Hedges Philip Morris USA cigarettes 7/22/03 NPM Berley Xcaliber International Ltd. cigarettes 12/13/18 PM Black & Gold Sherman 1400 Broadway NYC, Ltd. cigarettes 7/22/03 PM Bronson Liggett Group Inc cigarettes 4/11/06 PM Bugler Scandinavian Tobacco Group Lane Ltd. -

Complaint Counsel's Motion for an Order That Respondent Altria Has Waived Privilege

FEDERAL TRADE COMMISSION | OFFICE OF THE SECRETARY | FILED 2/12/2021 | OSCARPUBLIC NO. 600662 | PUBLIC UNITED STATES OF AMERICA FEDERAL TRADE COMMISSION OFFICE OF ADMINSTRATIVE LAW JUDGES In the Matter of Altria Group, Inc. DOCKET NO. 9393 a corporation; and JUUL Labs, Inc. a corporation. COMPLAINT COUNSEL’S MOTION FOR AN ORDER THAT RESPONDENT ALTRIA HAS WAIVED PRIVILEGE Pursuant to Rules 3.22 and 2.11(d), of the Commission Rules of Practice, 16 C.F.R. § 3.22 and 16 C.F.R. § 2.11(d), Complaint Counsel respectfully moves the Court for an order that (1) Respondent Altria has waived any claims of privilege as to documents that it produced during the Commission’s pre-complaint investigation and subsequently sought to claw back and (2) that Altria is precluded from clawing back any documents produced during the pre-complaint investigation going forward from the date of this motion. As set forth in the attached memorandum, Respondent did not take even minimally reasonable steps to prevent disclosure of the purportedly privileged documents that it produced and did not promptly rectify its errors in producing nearly 10,000 documents that it subsequently sought to claw back. See Rule 2.11(d) of the Commission Rules of Practice, 16 C.F.R. 2.11(d). A proposed order is attached. Dated: February 12, 2021 Respectfully submitted, /s/ Frances Anne Johnson Frances Anne Johnson Dominic E. Vote FEDERAL TRADE COMMISSION | OFFICE OF THE SECRETARY | FILED 2/12/2021 | OSCARPUBLIC NO. 600662 | PUBLIC Peggy Bayer Femenella Jennifer Milici James Abell Erik Herron Joonsuk Lee Meredith Levert Kristian Rogers David Morris Michael Blevins Michael Lovinger Stephen Rodger Counsel Supporting the Complaint Federal Trade Commission Bureau of Competition 600 Pennsylvania Ave., NW Washington, DC 20580 Telephone: (202) 326-3221 Email: [email protected] FEDERAL TRADE COMMISSION | OFFICE OF THE SECRETARY | FILED 2/12/2021 | OSCARPUBLIC NO.