Q1 2017 Colliers Investment Market Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CBL & ASSOCIATES PROPERTIES INC (Form: 8-K

SECURITIES AND EXCHANGE COMMISSION FORM 8-K Current report filing Filing Date: 2002-04-25 | Period of Report: 2002-03-31 SEC Accession No. 0000910612-02-000004 (HTML Version on secdatabase.com) FILER CBL & ASSOCIATES PROPERTIES INC Mailing Address Business Address 61048 LEE HIGHWAY SUITE ONE PARK PLACE CIK:910612| IRS No.: 621545718 | State of Incorp.:DE | Fiscal Year End: 1231 300 6148 LEE HWY SUITE 300 Type: 8-K | Act: 34 | File No.: 001-12494 | Film No.: 02621546 ONE PARK PLACE CHATTANOOGA TN 37421 SIC: 6798 Real estate investment trusts CHATTANOOGA TN 37421 4238550001 Copyright © 2012 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document Securities Exchange Act of 1934 -- Form 8-K SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report: April 25, 2002 ------------------------------------------------------------------------------- CBL & ASSOCIATES PROPERTIES, INC. ------------------------------------------------------------------------------- (Exact name of registrant as specified in its charter) Delaware 1-12494 62-1545718 ---------------------- -------------------- ------------------------ (State or other (Commission (IRS Employer jurisdiction of File Number) Identification Number) incorporation) 2030 Hamilton Place Boulevard, Chattanooga, TN 37421 ------------------------------------------------------------------------------- (Address of principal executive offices) Registrant's telephone number, including area code: ------------------------------------------------------------------------------- (423) 855-0001 CBL & ASSOCIATES PROPERTIES, INC. Conference Call Outline - First Quarter 2002 April 25, 2002 @ 10:00 a.m. EDT Good morning. We appreciate your participation in today's call to discuss our results for the first quarter of 2002. With me today is Stephen Lebovitz, our President, and Kelly Sargent, our Director of Investor Relations, who will first read our Safe Harbor disclosure. -

Voluntary Petition for Non-Individuals Filing for Bankruptcy 04/20

Case 21-31717 Document 1 Filed in TXSB on 05/26/21 Page 1 of 54 Fill in this information to identify the case: United States Bankruptcy Court for the Southern District of Texas Case number (if known): Chapter 11 Check if this is an amended filing Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy 04/20 If more space is needed, attach a separate sheet to this form. On the top of any additional pages, write the debtor’s name and the case number (if known). For more information, a separate document, Instructions for Bankruptcy Forms for Non-Individuals, is available. 1. Debtor’s name Laredo Outlet Shoppes, LLC 2. All other names debtor used N/A in the last 8 years Include any assumed names, trade names, and doing business as names 3. Debtor’s federal Employer Identification Number (EIN) 81-1563566 4. Debtor’s address Principal place of business Mailing address, if different from principal place of business 2030 Hamilton Place Blvd. Number Street Number Street CBL Center, Suite 500 P.O. Box Chattanooga Tennessee 37421 City State ZIP Code City State ZIP Code Location of principal assets, if different from principal place of business Hamilton County County 1600 Water Street Number Street Laredo Texas 78040 City State ZIP Code 5. Debtor’s website (URL) www.cblproperties.com 6. Type of debtor ☒ Corporation (including Limited Liability Company (LLC) and Limited Liability Partnership (LLP)) ☐ Partnership (excluding LLP) ☐ Other. Specify: Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy Page 1 WEIL:\97969900\8\32626.0004 Case 21-31717 Document 1 Filed in TXSB on 05/26/21 Page 2 of 54 Debtor Laredo Outlet Shoppes, LLC Case number (if known) 21-_____ ( ) Name A. -

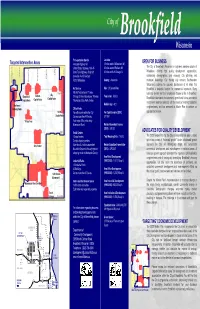

Brookfield Square Area Redevelopment Strategy

City of Brookfield Wisconsin Transportation Service Location: Targeted Intervention Areas Interstate Highway 94 15 miles west of Milwaukee, WI OPEN FOR BUSINESS United States Highways 18 & 45 65 miles east of Madison, WI The City of Brookfield, Wisconsin is a dynamic western suburb of State Trunk Highways 59 & 190 90 miles north of Chicago, IL Milwaukee, offering high quality development opportunities, 124 Lilly Lilly Barker Canadian Pacific Railroad outstanding demographics, and visionary City planning and Pilgrim Calhoun Calhoun Port of Milwaukee County: Waukesha municipal leadership. Our thriving city remains Southeastern Brookfield Springdale Springdale Wisconsin’s address for success. Businesses of all kinds find Air Service Size: 26 Square Miles Brookfield a desirable location for commercial expansion. Many Capitol Mitchell International, 17 miles Lilly- business owners and their employees choose to live in Brookfield. Brookfield- Calhoun- Chicago O’Hare International, 88 miles Population: 38,823 Brookfield understands that economic growth and future commercial Capitol Node Capitol Node Capitol Node Waukesha Crites Field, 6 miles investments must be balanced with the needs of existing residential Median Age: 42.5 Northwest neighborhoods, and has prepared its Master Plan to achieve an Gateway Node Office Parks 124 St.- Ten office parks within the City Per Capita Income (2000): appropriate balance. Capitol Node Covers more than 400 acres $37,292 Village Area Four major office parks along Bluemound Road Median Household Income (2000): $76,132 North Retail Centers ADVOCATES FOR QUALITY DEVELOPMENT 13 retail centers Total Housing Units: 14,203 The 2020 Master Plan for the City of Brookfield has been created 5 major shopping centers within the context of “balanced growth.” Under a balanced growth Civic Center More than 5.4 million square feet Median Equalized Home Value approach the City will strategically target and concentrate Brookfield Square is the only regional (2002): $242,330 commercial development and redevelopment in selected areas. -

Lakefront Festival of Arts Fact Sheet

LAKEFRONT FESTIVAL OF ARTS FACT SHEET FESTIVAL HOURS Friday, June 19: 12–8 p.m. Saturday, June 20: 10 a.m.–7 p.m. Sunday, June 21: 10 a.m.–5 p.m. MUSEUM HOURS Friday, June 19: 10 a.m–8 p.m. Saturday, June 20: 10 a.m.–7 p.m. Sunday, June 21: 10 a.m.–5 p.m. TICKETS General public: $10 at the gate Kids 16 and under: Free with a paid adult MAM members: $7 with valid membership card Advance tickets: $7 when ordered at www.mam.org or at one of several advanced retail locations, listed on www.mam.org/lfoa Purchase a ticket to LFOA and receive 50% off Museum admission! ADVANCED TICKET LOCATIONS • MAM.org – advanced and combo tickets • Participating Pick 'n Save® Stores • Affordable Art & Frames: 14685 W Capitol Dr, Brookfield • Artist and Display Supply, Inc., 9015 W. Burleigh St., Milwaukee • Boston Store: Grand Avenue, Bayshore, Brookfield Square, Furniture Gallery Brookfield, Mayfair, Regency Mall Racine, and Southridge Malls • Cudahy Tap Room: 3558 E. Barnard, Cudahy • Elite Fitness & Racquet Clubs: Highland Elite; 13825 W. Burleigh, Brookfield; North Shore Elite; 5750 N. Glen Park, Glendale • Fiddleheads Espresso Bar and Café, 192 S. Main St., Thiensville • Hawks Nursery, 12217 W. Watertown Plank Rd., Wauwatosa • Katie Gingrass Gallery 241 N. Broadway, Milwaukee • The Little Read Book, 7603 W. State St., Wauwatosa • Milwaukee Art Museum Store, 700 N. Art Museum Dr., Milwaukee • Mequon Chiropractic: 10521 N Port Washington Rd., Mequon • Samson Family Jewish Community Center of Greater Milwaukee, 6255 N. Santa Monica Blvd., Whitefish Bay • Sommer’s Suburu: 7211 Mequon Rd., Mequon • Sven’s Cafe: 2699 S. -

CBL & Associates Properties 2012 Annual Report

COVER PROPERTIES : Left to Right/Top to Bottom MALL DEL NORTE, LAREDO, TX CROSS CREEK MALL, FAYETTEVILLE, NC BURNSVILLE CENTER, BURNSVILLE, MN OAK PARK MALL, KANSAS CITY, KS CBL & Associates Properties, Inc. 2012 Annual When investors, business partners, retailers Report CBL & ASSOCIATES PROPERTIES, INC. and shoppers think of CBL they think of the leading owner of market-dominant malls in CORPORATE OFFICE BOSTON REGIONAL OFFICE DALLAS REGIONAL OFFICE ST. LOUIS REGIONAL OFFICE the U.S. In 2012, CBL once again demon- CBL CENTER WATERMILL CENTER ATRIUM AT OFFICE CENTER 1200 CHESTERFIELD MALL THINK SUITE 500 SUITE 395 SUITE 750 CHESTERFIELD, MO 63017-4841 strated why it is thought of among the best 2030 HAMILTON PLACE BLVD. 800 SOUTH STREET 1320 GREENWAY DRIVE (636) 536-0581 THINK 2012 Annual Report CHATTANOOGA, TN 37421-6000 WALTHAM, MA 02453-1457 IRVING, TX 75038-2503 CBLCBL & &Associates Associates Properties Properties, 2012 Inc. Annual Report companies in the shopping center industry. (423) 855-0001 (781) 398-7100 (214) 596-1195 CBLPROPERTIES.COM HAMILTON PLACE, CHATTANOOGA, TN: Our strategy of owning the The 2012 CBL & Associates Properties, Inc. Annual Report saved the following resources by printing on paper containing dominant mall in SFI-00616 10% postconsumer recycled content. its market helps attract in-demand new retailers. At trees waste water energy solid waste greenhouse gases waterborne waste Hamilton Place 5 1,930 3,217,760 214 420 13 Mall, Chattanooga fully grown gallons million BTUs pounds pounds pounds shoppers enjoy the market’s only Forever 21. COVER PROPERTIES : Left to Right/Top to Bottom MALL DEL NORTE, LAREDO, TX CROSS CREEK MALL, FAYETTEVILLE, NC BURNSVILLE CENTER, BURNSVILLE, MN OAK PARK MALL, KANSAS CITY, KS CBL & Associates Properties, Inc. -

Johnson Creek Premium Outlets

JOHNSON CREEK, WISCONSIN PROPERTY OVERVIEW JOHNSON CREEK PREMIUM OUTLETS® JOHNSON CREEK, WI JOHNSON CREEK PREMIUM OUTLETS JOHNSON CREEK, WI 26 MAJOR METROPOLITAN AREAS SELECT TENANTS 45 Wisconsin Dells 41 Madison: 30 miles adidas, American Eagle Outfitters, Ann Taylor Factory Store, 151 Milwaukee: 35 miles Banana Republic Factory Store, Calvin Klein Company Store, Carter’s Outlet, Coach, Columbia Sportswear, Crocs, Eddie Bauer Outlet, Gap Watertown Outlet, Gymboree Outlet, LOFT Outlet, Nike Factory Store, OshKosh Madison Milwaukee RETAIL Lake Mills 94 B’gosh, Polo Ralph Lauren Factory Store, Talbots, Tommy Hilfiger Jefferson GLA (sq. ft.) 278,000; 60 stores Company Store, Under Armour 14 90 Fort Atkinson 26 12 OPENING DATES TOURISM / TRAFFIC 43 Opened 1998 The center is located on the northwest quadrant of I-94 and Hwy. 26 and Expanded 1999 is en route to the University of Wisconsin and Wisconsin Dells (2.5 million annual visitors). Average daily traffic on I-94 is 29,000 and on Hwy. 26, over 13,000. PARKING RATIO 5.22:1 LOCATION / DIRECTIONS I-94 at Hwy. 26. Thirty miles east of Madison and 35 miles west of RADIUS POPULATION Milwaukee, Wisconsin. 15 miles: 114,415 30 miles: 703,139 — Take I-94 to Hwy. 26, Exit 267 45 miles: 2,511,808 AVERAGE HH INCOME 30 miles: $80,407 Information as of 5/1/17. Source: SPG Research; trade area demographic information per STI: PopStats (2016). MASTER PLAN DRESSBARN OLD 26 RD. NIKE FACTORY STORE GAP OUTLET I-94 COLUMBIA SPORTSWEAR POLO RALPH LAUREN UNDER FACTORY STORE ARMOUR EDDIE BAUER OUTLET OLD NAVY NORTH LINMAR LN. -

Bankruptcy Forms for Non-Individuals, Is Available

Case 17-31455 Doc 1 Filed 09/01/17 Entered 09/01/17 17:27:08 Desc Main Document Page 1 of 53 Fill in this information to identify your case: United States Bankruptcy Court for the: WESTERN DISTRICT OF NORTH CAROLINA Case number (if known) Chapter 11 Check if this an amended filing Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy 4/16 If more space is needed, attach a separate sheet to this form. On the top of any additional pages, write the debtor's name and case number (if known). For more information, a separate document, Instructions for Bankruptcy Forms for Non-Individuals, is available. 1. Debtor's name Portrait Innovations, Inc. 2. All other names debtor used in the last 8 years Include any assumed names, trade names and doing business as names 3. Debtor's federal Employer Identification 56-2179394 Number (EIN) 4. Debtor's address Principal place of business Mailing address, if different from principal place of business 2016 Ayrsley Town Blvd., Suite 200 Charlotte, NC 28273 Number, Street, City, State & ZIP Code P.O. Box, Number, Street, City, State & ZIP Code Mecklenburg Location of principal assets, if different from principal County place of business Number, Street, City, State & ZIP Code 5. Debtor's website (URL) www.portraitinnovations.com 6. Type of debtor Corporation (including Limited Liability Company (LLC) and Limited Liability Partnership (LLP)) Partnership (excluding LLP) Other. Specify: Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy page 1 Case 17-31455 Doc 1 Filed 09/01/17 Entered 09/01/17 17:27:08 Desc Main Document Page 2 of 53 Debtor Portrait Innovations, Inc. -

Pleasant Prairie Premium Outlets® the Simon Experience — Where Brands & Communities Come Together

PLEASANT PRAIRIE PREMIUM OUTLETS® THE SIMON EXPERIENCE — WHERE BRANDS & COMMUNITIES COME TOGETHER More than real estate, we are a company of experiences. For our guests, we provide distinctive shopping, dining and entertainment. For our retailers, we offer the unique opportunity to thrive in the best retail real estate in the best markets. From new projects and redevelopments to acquisitions and mergers, we are continuously evaluating our portfolio to enhance the Simon experience - places where people choose to shop and retailers want to be. We deliver: SCALE Largest global owner of retail real estate including Malls, Simon Premium Outlets® and The Mills® QUALITY Iconic, irreplaceable properties in great locations INVESTMENT Active portfolio management increases productivity and returns GROWTH Core business and strategic acquisitions drive performance EXPERIENCE Decades of expertise in development, ownership, and management That’s the advantage of leasing with Simon. PROPERTY OVERVIEW ® Shorewood PLEASANT PRAIRIE PREMIUM OUTLETS Madison 94 18 Milwaukee PLEASANT PRAIRIE, WI Fort Atkinson 94 Oak Creek 12 PLEASANTLake PRAIRIE43 Geneva 14 PREMIUM OUTLETS Racine MAJOR METROPOLITAN AREAS SELECT TENANTS PLEASANT PRAIRIE, WI 41 Kenosha Chicago, IL: 60 miles Ann Taylor Factory Store, Arc’teryx I Salomon, Banana Republic Factory Milwaukee: 35 miles Store, Brooks Brothers Factory Store, Calvin Klein Company Store, Lake Michigan WI Beloit Coach Factory Store, Cole Haan Outlet, Express Factory Outlet, Gap Rockford IL 14 North RETAIL Factory Store, HUGO BOSS Factory Store, J.Crew Factory, kate spade new Chicago york, LACOSTE Outlet, Michael Kors Outlet, NikeFactoryStore, The North 90 Woodstock 94 GLA (sq. ft.) 403,000; 90 stores Face, Polo Ralph Lauren Factory Store, UGG® Australia, Under Armour 51 41 Factory House Evanston 39 20 OPENING DATES 94 29 TOURISM / TRAFFIC Wheaton Rochelle 80 Opened 1988 Chicago Expanded 2006 Pleasant Prairie is an outlet shopping destination that is well established throughout Illinois and Wisconsin. -

F 10 Million, the Next Largest City Will Have a Population Of

AP HUMAN GEOGRAPHY THE GRAND REVIEW Unit I: Geography: Its Nature and Perspective Identify each type of map: 1. 2. 3. 4. Match the following: 5. a computer system that stores, organizes, a. cultural diffusion retrieves, analyzes, and displays geographic data 6. the forms superimposed on the physical b. cultural ecology environment by the activities of humans 7. the spread of an idea or innovation from its source c. cultural landscape 8. interactions between human societies and the d. environmental determinism physical environment 9. a space-based global navigation satellite system e. GIS 10. the physical environment, rather than social f. GPS conditions, determines culture 11. the small- or large-scale acquisition of g. remote sensing information of an object or phenomenon, either in recording or real time Choose the one that does not belong: 12. a. township and range 16. a. major airport b. clustered rural settlement b. grid street pattern c. grid street pattern c. major central park d. natural harbor 13. a. site e. public sports facility b. situation c. its relative location 17. a. Westernization b. uniform consumption preferences 14. a. latitude and longitude c. enhanced communications b. site d. local traditions c. situation d. absolute location 18. a. time zones b. China 15. a. globalization c. United States railroads b. nationalism d. 15 degrees c. foreign investment d. multinational corporations Match the following (some regions have more than one answer): 19. formal region a. Milwaukee 20. functional region b. the Milwaukee Journal Sentinel 21. vernacular region c. Wisconsin d. the South e. an airline hub f. -

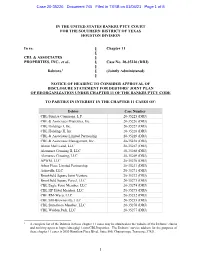

Chapter 11 § CBL & ASSOCIATES § PROPERTIES, INC., Et Al., § Case No

Case 20-35226 Document 745 Filed in TXSB on 01/04/21 Page 1 of 8 IN THE UNITED STATES BANKRUPTCY COURT FOR THE SOUTHERN DISTRICT OF TEXAS HOUSTON DIVISION In re: § Chapter 11 § CBL & ASSOCIATES § PROPERTIES, INC., et al., § Case No. 20-35226 (DRJ) § Debtors.1 § (Jointly Administered) § NOTICE OF HEARING TO CONSIDER APPROVAL OF DISCLOSURE STATEMENT FOR DEBTORS’ JOINT PLAN OF REORGANIZATION UNDER CHAPTER 11 OF THE BANKRUPTCY CODE TO PARTIES IN INTEREST IN THE CHAPTER 11 CASES OF: Debtor Case Number CBL/Sunrise Commons, L.P. 20-35225 (DRJ) CBL & Associates Properties, Inc. 20-35226 (DRJ) CBL Holdings I, Inc. 20-35227 (DRJ) CBL Holdings II, Inc. 20-35228 (DRJ) CBL & Associates Limited Partnership 20-35229 (DRJ) CBL & Associates Management, Inc. 20-35230 (DRJ) Akron Mall Land, LLC 20-35267 (DRJ) Alamance Crossing II, LLC 20-35268 (DRJ) Alamance Crossing, LLC 20-35269 (DRJ) APWM, LLC 20-35270 (DRJ) Arbor Place Limited Partnership 20-35231 (DRJ) Asheville, LLC 20-35271 (DRJ) Brookfield Square Joint Venture 20-35272 (DRJ) Brookfield Square Parcel, LLC 20-35273 (DRJ) CBL Eagle Point Member, LLC 20-35274 (DRJ) CBL HP Hotel Member, LLC 20-35275 (DRJ) CBL RM-Waco, LLC 20-35232 (DRJ) CBL SM-Brownsville, LLC 20-35233 (DRJ) CBL Statesboro Member, LLC 20-35276 (DRJ) CBL Walden Park, LLC 20-35277 (DRJ) 1 A complete list of the Debtors in these chapter 11 cases may be obtained on the website of the Debtors’ claims and noticing agent at https://dm.epiq11.com/CBLProperties. The Debtors’ service address for the purposes of these chapter 11 cases is 2030 Hamilton Place Blvd., Suite 500, Chattanooga, Tennessee 37421. -

250 Patrick Boulevard 250 Patrick Boulevard | in the Brookfield Lakes Corporate Center Brookfield, Wisconsin

250 PATRICK BOULEVARD 250 Patrick Boulevard | in the Brookfield Lakes Corporate Center Brookfield, Wisconsin NOW LEASING | 3,366 sf Irgens is proud to offer prime office space for lease at Brookfield Lakes Corporate Center in the heart of Brookfield. The property offers easy access to Bluemound Road and excellent connectivity to The Corridor with the 2018 extension of Patrick Boulevard. Nearby amenities including The Corridor, The Corners, Brookfield Square Mall, banks, hotels, restaurants, and retailers make 250 Patrick Boulevard an ideal location for tenants and guests. Local, award-winning property management provides an unparalleled tenant experience. FOR MORE INFORMATION ABOUT THIS PROPERTY, PLEASE CONTACT: Tim Nelson, CCIM | [email protected] | 414.443.2553 833 East Michigan Street | Suite 400 | Milwaukee, WI 53202 tele 414.443.0700 | fax 414.443.1400 | irgens.com PROJECT DESCRIPTION Location 250 Patrick Boulevard, Brookfield, Wisconsin 53005 | in the Brookfield Lakes Corporate Center Description Flexible, convenient and strategic, 250 Patrick Boulevard offers excellent value in a prime location. Enjoy a beautiful park-like setting near Brookfield area amenities. Amenities - Newly renovated lobby and common areas - Outdoor patio with seating area and pond views - Award-winning, pro-active property management team - Tenant improvement packages available - Upgraded lighting, signage and landscaping - Near connection of Patrick Boulevard to Golf Road BUILDING IMAGES FLOOR PLANS Suite 180 AVAILABLE 3,366 RSF AMENITIES MAP Fleming’s Starbucks Stir Crazy Wasabi Sushi Lounge Fresh Market Chipotle Westmoor Country Club Petco Office Depot Brookfield Square Mall Fuddruckers Blackfinn Ameripub Sheraton Milwaukee Cooper’s Hawk Buffalo Wild Wings Michaels Walgreen’s Bravo! Cucina Italiana Jo-Ann Fabrics buybuy Baby Mitchell’s Fish Market Party City World Market Brookfield Hills Golf Course SteinMart Bed, Bath & Beyond Moorland Road Ulta Beauty Golf Galaxy Noodles & Co. -

Brookfield Square Milwaukee (Brookfield), WI

Brookfield Square Milwaukee (Brookfield), WI Location I-94 at Bluemound Road Anchors Boston Store, JCPenney, Sears and Barnes & Noble Booksellers Size 1,000,568 square feet Website ShopBrookfieldSquareMall.com Mall Facts Brookfield Square has more than 100 specialty stores including ALDO, American Eagle, Bravo! Cucina Italiana, Coopers Hawk Winery & Restaurant, francesca’s, H&M, LOFT, The Limited, The North Face and Victoria’s Secret. Brookfield Square also offers nine quick-serve eateries and six sit-down restaurants. New specialty retailers and restaurants include Body Central, Crazy 8, Divino Gelato, Opa Gyros, rue21, Torrid and Tradehome Shoes. Located on the mall’s periphery are Fleming’s Prime Steakhouse and Wine Bar, Ethan Allen, Stir Crazy and The Fresh Market. Trade Area Brookfield Square is located in one of Milwaukee’s fastest growing and most Facts affluent areas, just off I-94, southeastern Wisconsin’s main thoroughfare. Brookfield Square is positioned just ten miles west of downtown Milwaukee in the city of Brookfield, one of Wisconsin’s strongest economic areas. Brookfield has a thriving economy with six million square feet of corporate office space and five million square feet of existing industrial space. Four of Brookfield’s major office parks are located within one mile of the mall employing upwards of 10,000 employees. Major employers in the area include Wheaton Franciscan Healthcare, GE Medical Services, Harley-Davidson and Quad Graphics. There are eight colleges and universities located within Brookfield Square’s trade area with the University of Wisconsin at Milwaukee and Marquette University hosting more than 25,000 students. Brookfield Square draws from a primary market that encompasses some of Milwaukee’s most affluent zip codes.