CBL & ASSOCIATES PROPERTIES INC (Form: 8-K

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FAYETTE MALL Lexington, KY CBL PROPERTIES

MALL FAYETTE Lexington, KY CBL PROPERTIES HIGHLIGHTS NUMBER OF STORES 150 TRADE AREA 824,980 (2017 est.) SIZE 1,203,002 square feet CENTER EMPLOYMENT 2,750 (est.) FEATURED STORES Macy’s, Dillard’s, DICK’S Sporting Goods, JCPenney, Altar’d State, Apple, The Cheesecake Factory, Cinemark (16 1971 screens), Coach, Disney, H&M, Michael Kors, and Sephora YEAR OPENED WEBSITE ShopFayette-Mall.com CORPORATE OFFICE: FOR LEASING: CBL Center, Suite 500 MALL OFFICE: CBL PROPERTIES Laura Farren 3401 Nicholasville Road, Suite 303 cblproperties.com 2030 Hamilton Place Boulevard p. 423.490.8620 c. 423.463.4589 Lexington, KY 40503 NYSE: CBL Chattanooga, TN 37421-6000 [email protected] 859.272.3493 423.855.0001 DEMOGRAPHICS TRADE AREA FACTS PRIMARY SECONDARY TOTAL • Known as the “Horse Capital of the World,” Lexington, Kentucky POPULATION TRENDS TRADE AREA TRADE AREA TRADE AREA contributes over $5 billion a year to the state’s horse industry. 2022 Projection 420,298 448,220 868,518 • Lexington is the financial, retail, healthcare and cultural core of the 2017 Estimate 396,214 428,766 824,980 entire Bluegrass region. 2010 Census 369,850 412,671 782,521 • High household income of almost $80,000 is fueled by some of the 2017-2022 % Change 6.08% 4.54% 5.28% largest corporations in the U.S., including Toyota’s primary Camry/ Avalon/Lexus ES350 manufacturing facility, Ashland Oil, Lexmark, 2017 Daytime Population Estimate 251,368 189,885 441,253 IBM, Square D, The Trane Company, and Tempur-Pedic. • 27 companies, including Toyota, Florida Tile, EnerBlu Inc. and AVERAGE HOUSEHOLD INCOME Xooker invested $1.5 billion in the Lexington area for business 2022 Projection $92,586 $76,397 $84,384 expansion in 2017. -

Voluntary Petition for Non-Individuals Filing for Bankruptcy 04/20

Case 21-31717 Document 1 Filed in TXSB on 05/26/21 Page 1 of 54 Fill in this information to identify the case: United States Bankruptcy Court for the Southern District of Texas Case number (if known): Chapter 11 Check if this is an amended filing Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy 04/20 If more space is needed, attach a separate sheet to this form. On the top of any additional pages, write the debtor’s name and the case number (if known). For more information, a separate document, Instructions for Bankruptcy Forms for Non-Individuals, is available. 1. Debtor’s name Laredo Outlet Shoppes, LLC 2. All other names debtor used N/A in the last 8 years Include any assumed names, trade names, and doing business as names 3. Debtor’s federal Employer Identification Number (EIN) 81-1563566 4. Debtor’s address Principal place of business Mailing address, if different from principal place of business 2030 Hamilton Place Blvd. Number Street Number Street CBL Center, Suite 500 P.O. Box Chattanooga Tennessee 37421 City State ZIP Code City State ZIP Code Location of principal assets, if different from principal place of business Hamilton County County 1600 Water Street Number Street Laredo Texas 78040 City State ZIP Code 5. Debtor’s website (URL) www.cblproperties.com 6. Type of debtor ☒ Corporation (including Limited Liability Company (LLC) and Limited Liability Partnership (LLP)) ☐ Partnership (excluding LLP) ☐ Other. Specify: Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy Page 1 WEIL:\97969900\8\32626.0004 Case 21-31717 Document 1 Filed in TXSB on 05/26/21 Page 2 of 54 Debtor Laredo Outlet Shoppes, LLC Case number (if known) 21-_____ ( ) Name A. -

State City Shopping Center Address

State City Shopping Center Address AK ANCHORAGE 5TH AVENUE MALL SUR 406 W 5TH AVE AL FULTONDALE PROMENADE FULTONDALE 3363 LOWERY PKWY AL HOOVER RIVERCHASE GALLERIA 2300 RIVERCHASE GALLERIA AL MOBILE BEL AIR MALL 3400 BELL AIR MALL AR FAYETTEVILLE NW ARKANSAS MALL 4201 N SHILOH DR AR FORT SMITH CENTRAL MALL 5111 ROGERS AVE AR JONESBORO MALL @ TURTLE CREEK 3000 E HIGHLAND DR STE 516 AR LITTLE ROCK SHACKLEFORD CROSSING 2600 S SHACKLEFORD RD AR NORTH LITTLE ROCK MC CAIN SHOPG CNTR 3929 MCCAIN BLVD STE 500 AR ROGERS PINNACLE HLLS PROMDE 2202 BELLVIEW RD AZ CHANDLER MILL CROSSING 2180 S GILBERT RD AZ FLAGSTAFF FLAGSTAFF MALL 4600 N US HWY 89 AZ GLENDALE ARROWHEAD TOWNE CTR 7750 W ARROWHEAD TOWNE CENTER AZ GOODYEAR PALM VALLEY CORNERST 13333 W MCDOWELL RD AZ LAKE HAVASU CITY SHOPS @ LAKE HAVASU 5651 HWY 95 N AZ MESA SUPERST'N SPRINGS ML 6525 E SOUTHERN AVE AZ NOGALES MARIPOSA WEST PLAZA 220 W MARIPOSA RD AZ PHOENIX AHWATUKEE FOOTHILLS 5050 E RAY RD AZ PHOENIX CHRISTOWN SPECTRUM 1727 W BETHANY HOME RD AZ PHOENIX PARADISE VALLEY MALL 4510 E CACTUS RD AZ TEMPE TEMPE MARKETPLACE 1900 E RIO SALADO PKWY STE 140 AZ TUCSON EL CON SHPG CNTR 3501 E BROADWAY AZ TUCSON TUCSON MALL 4530 N ORACLE RD AZ TUCSON TUCSON SPECTRUM 5265 S CALLE SANTA CRUZ AZ YUMA YUMA PALMS S C 1375 S YUMA PALMS PKWY CA ANTIOCH ORCHARD @SLATTEN RCH 4951 SLATTEN RANCH RD CA ARCADIA WESTFLD SANTA ANITA 400 S BALDWIN AVE CA BAKERSFIELD VALLEY PLAZA 2501 MING AVE CA BREA BREA MALL 400 BREA MALL CA CARLSBAD PLAZA CAMINO REAL 2555 EL CAMINO REAL CA CARSON SOUTHBAY PAV @CARSON 20700 AVALON -

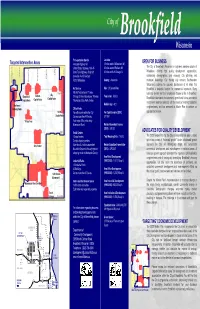

Brookfield Square Area Redevelopment Strategy

City of Brookfield Wisconsin Transportation Service Location: Targeted Intervention Areas Interstate Highway 94 15 miles west of Milwaukee, WI OPEN FOR BUSINESS United States Highways 18 & 45 65 miles east of Madison, WI The City of Brookfield, Wisconsin is a dynamic western suburb of State Trunk Highways 59 & 190 90 miles north of Chicago, IL Milwaukee, offering high quality development opportunities, 124 Lilly Lilly Barker Canadian Pacific Railroad outstanding demographics, and visionary City planning and Pilgrim Calhoun Calhoun Port of Milwaukee County: Waukesha municipal leadership. Our thriving city remains Southeastern Brookfield Springdale Springdale Wisconsin’s address for success. Businesses of all kinds find Air Service Size: 26 Square Miles Brookfield a desirable location for commercial expansion. Many Capitol Mitchell International, 17 miles Lilly- business owners and their employees choose to live in Brookfield. Brookfield- Calhoun- Chicago O’Hare International, 88 miles Population: 38,823 Brookfield understands that economic growth and future commercial Capitol Node Capitol Node Capitol Node Waukesha Crites Field, 6 miles investments must be balanced with the needs of existing residential Median Age: 42.5 Northwest neighborhoods, and has prepared its Master Plan to achieve an Gateway Node Office Parks 124 St.- Ten office parks within the City Per Capita Income (2000): appropriate balance. Capitol Node Covers more than 400 acres $37,292 Village Area Four major office parks along Bluemound Road Median Household Income (2000): $76,132 North Retail Centers ADVOCATES FOR QUALITY DEVELOPMENT 13 retail centers Total Housing Units: 14,203 The 2020 Master Plan for the City of Brookfield has been created 5 major shopping centers within the context of “balanced growth.” Under a balanced growth Civic Center More than 5.4 million square feet Median Equalized Home Value approach the City will strategically target and concentrate Brookfield Square is the only regional (2002): $242,330 commercial development and redevelopment in selected areas. -

Hamburg Pavilion Lexington, Kentucky a Community Cited by a National Publication As One of the “Smartest” in America Spends Its Time Wisely —

Hamburg Pavilion Hamburg Pavilion Lexington, Kentucky A community cited by a national publication as one of the “smartest” in America spends its time wisely — and that’s why shoppers come to Hamburg Pavilion, a PARIS, KY GEORGETOWN, KY center that combines the convenience of the traditional VERSAILLES, KY power center with the aesthetics, entertainment, and LEXINGTON, KY WINCHESTER, KY dining opportunities of a lifestyle center. Located in Lexington, Ky., Hamburg Pavilion serves 10 MILES a growing, widely varying audience, including executives from the many international corporations in the area, students from some of the premier colleges and universities in the United States, and visitors who flock to the “Horse Capital of the World.” Hamburg Pavilion is part of the excitement, too. Hamburg Pavilion Lexington, Kentucky • Open-air regional center • One of the largest shopping centers in Kentucky • Renovation and expansion planned • Multiple anchors include fashion discounters, apparel, electronics, books, cinema, sporting goods, crafts, and pet goods Property Description major roads I-75 and Man O’ War center description Super-regional power center with a lifestyle center Boulevard anchors Target, Kohl’s, Dick’s Sporting Goods, At Home, total sf 980,000 and Regal Cinemas # of stores 75 key tenants Best Buy, Marshall’s, White House Black Market, DSW, Michael’s, PetsMart, Party City, Victoria’s Secret, Loft, # of parking 5,900 Old Navy, Babies R Us and Barnes & Noble THE CENTER THE MARKET STARWOOD Hamburg Pavilion “… A youthful ambiance -

Lakefront Festival of Arts Fact Sheet

LAKEFRONT FESTIVAL OF ARTS FACT SHEET FESTIVAL HOURS Friday, June 19: 12–8 p.m. Saturday, June 20: 10 a.m.–7 p.m. Sunday, June 21: 10 a.m.–5 p.m. MUSEUM HOURS Friday, June 19: 10 a.m–8 p.m. Saturday, June 20: 10 a.m.–7 p.m. Sunday, June 21: 10 a.m.–5 p.m. TICKETS General public: $10 at the gate Kids 16 and under: Free with a paid adult MAM members: $7 with valid membership card Advance tickets: $7 when ordered at www.mam.org or at one of several advanced retail locations, listed on www.mam.org/lfoa Purchase a ticket to LFOA and receive 50% off Museum admission! ADVANCED TICKET LOCATIONS • MAM.org – advanced and combo tickets • Participating Pick 'n Save® Stores • Affordable Art & Frames: 14685 W Capitol Dr, Brookfield • Artist and Display Supply, Inc., 9015 W. Burleigh St., Milwaukee • Boston Store: Grand Avenue, Bayshore, Brookfield Square, Furniture Gallery Brookfield, Mayfair, Regency Mall Racine, and Southridge Malls • Cudahy Tap Room: 3558 E. Barnard, Cudahy • Elite Fitness & Racquet Clubs: Highland Elite; 13825 W. Burleigh, Brookfield; North Shore Elite; 5750 N. Glen Park, Glendale • Fiddleheads Espresso Bar and Café, 192 S. Main St., Thiensville • Hawks Nursery, 12217 W. Watertown Plank Rd., Wauwatosa • Katie Gingrass Gallery 241 N. Broadway, Milwaukee • The Little Read Book, 7603 W. State St., Wauwatosa • Milwaukee Art Museum Store, 700 N. Art Museum Dr., Milwaukee • Mequon Chiropractic: 10521 N Port Washington Rd., Mequon • Samson Family Jewish Community Center of Greater Milwaukee, 6255 N. Santa Monica Blvd., Whitefish Bay • Sommer’s Suburu: 7211 Mequon Rd., Mequon • Sven’s Cafe: 2699 S. -

CBL & Associates Properties 2012 Annual Report

COVER PROPERTIES : Left to Right/Top to Bottom MALL DEL NORTE, LAREDO, TX CROSS CREEK MALL, FAYETTEVILLE, NC BURNSVILLE CENTER, BURNSVILLE, MN OAK PARK MALL, KANSAS CITY, KS CBL & Associates Properties, Inc. 2012 Annual When investors, business partners, retailers Report CBL & ASSOCIATES PROPERTIES, INC. and shoppers think of CBL they think of the leading owner of market-dominant malls in CORPORATE OFFICE BOSTON REGIONAL OFFICE DALLAS REGIONAL OFFICE ST. LOUIS REGIONAL OFFICE the U.S. In 2012, CBL once again demon- CBL CENTER WATERMILL CENTER ATRIUM AT OFFICE CENTER 1200 CHESTERFIELD MALL THINK SUITE 500 SUITE 395 SUITE 750 CHESTERFIELD, MO 63017-4841 strated why it is thought of among the best 2030 HAMILTON PLACE BLVD. 800 SOUTH STREET 1320 GREENWAY DRIVE (636) 536-0581 THINK 2012 Annual Report CHATTANOOGA, TN 37421-6000 WALTHAM, MA 02453-1457 IRVING, TX 75038-2503 CBLCBL & &Associates Associates Properties Properties, 2012 Inc. Annual Report companies in the shopping center industry. (423) 855-0001 (781) 398-7100 (214) 596-1195 CBLPROPERTIES.COM HAMILTON PLACE, CHATTANOOGA, TN: Our strategy of owning the The 2012 CBL & Associates Properties, Inc. Annual Report saved the following resources by printing on paper containing dominant mall in SFI-00616 10% postconsumer recycled content. its market helps attract in-demand new retailers. At trees waste water energy solid waste greenhouse gases waterborne waste Hamilton Place 5 1,930 3,217,760 214 420 13 Mall, Chattanooga fully grown gallons million BTUs pounds pounds pounds shoppers enjoy the market’s only Forever 21. COVER PROPERTIES : Left to Right/Top to Bottom MALL DEL NORTE, LAREDO, TX CROSS CREEK MALL, FAYETTEVILLE, NC BURNSVILLE CENTER, BURNSVILLE, MN OAK PARK MALL, KANSAS CITY, KS CBL & Associates Properties, Inc. -

Store # State City Mall/Shopping Center Name Address Date

Store # State City Mall/Shopping Center Name Address Date 2918 AL ALABASTER COLONIAL PROMENADE 340 S COLONIAL DR Now Open! 2218 AL HOOVER RIVERCHASE GALLERIA 2300 RIVERCHASE GALLERIA Now Open! 219 AL MOBILE BEL AIR MALL MOBILE, AL 36606-3411 Now Open! 2840 AL MONTGOMERY EASTDALE MALL MONTGOMERY, AL 36117-2154 Now Open! 2956 AL PRATTVILLE HIGH POINT TOWN CENTER PRATTVILLE, AL 36066-6542 Now Open! 2875 AL SPANISH FORT SPANISH FORT TOWN CENTER 22500 TOWN CENTER AVE Now Open! 2869 AL TRUSSVILLE TUTWILER FARM 5060 PINNACLE SQ Now Open! 2709 AR FAYETTEVILLE NW ARKANSAS MALL 4201 N SHILOH DR Now Open! 1961 AR FORT SMITH CENTRAL MALL 5111 ROGERS AVE Now Open! 2914 AR LITTLE ROCK SHACKLEFORD CROSSING 2600 S SHACKLEFORD RD Now Open! 663 AR NORTH LITTLE ROCK MCCAIN SHOPPING CENTER 3929 MCCAIN BLVD STE 500 Now Open! 2879 AR ROGERS PINNACLE HLLS PROMDE 2202 BELLVIEW RD Now Open! 2936 AZ CASA GRANDE PROMNDE AT CASA GRANDE 1041 N PROMENADE PKWY Now Open! 157 AZ CHANDLER MILL CROSSING 2180 S GILBERT RD Now Open! 251 AZ GLENDALE ARROWHEAD TOWNE CENTER 7750 W ARROWHEAD TOWNE CENTER Now Open! 2842 AZ GOODYEAR PALM VALLEY CORNERST 13333 W MCDOWELL RD Now Open! 2940 AZ LAKE HAVASU CITY SHOPS AT LAKE HAVASU 5651 HWY 95 N Now Open! 2419 AZ MESA SUPERSTITION SPRINGS MALL 6525 E SOUTHERN AVE Now Open! 2846 AZ PHOENIX AHWATUKEE FOOTHILLS 5050 E RAY RD Now Open! 1480 AZ PHOENIX PARADISE VALLEY MALL 4510 E CACTUS RD Now Open! 2902 AZ TEMPE TEMPE MARKETPLACE 1900 E RIO SALADO PKWY STE 140 Now Open! 1130 AZ TUCSON EL CON SHOPPING CENTER 3501 E BROADWAY Now Open! 90 -

Johnson Creek Premium Outlets

JOHNSON CREEK, WISCONSIN PROPERTY OVERVIEW JOHNSON CREEK PREMIUM OUTLETS® JOHNSON CREEK, WI JOHNSON CREEK PREMIUM OUTLETS JOHNSON CREEK, WI 26 MAJOR METROPOLITAN AREAS SELECT TENANTS 45 Wisconsin Dells 41 Madison: 30 miles adidas, American Eagle Outfitters, Ann Taylor Factory Store, 151 Milwaukee: 35 miles Banana Republic Factory Store, Calvin Klein Company Store, Carter’s Outlet, Coach, Columbia Sportswear, Crocs, Eddie Bauer Outlet, Gap Watertown Outlet, Gymboree Outlet, LOFT Outlet, Nike Factory Store, OshKosh Madison Milwaukee RETAIL Lake Mills 94 B’gosh, Polo Ralph Lauren Factory Store, Talbots, Tommy Hilfiger Jefferson GLA (sq. ft.) 278,000; 60 stores Company Store, Under Armour 14 90 Fort Atkinson 26 12 OPENING DATES TOURISM / TRAFFIC 43 Opened 1998 The center is located on the northwest quadrant of I-94 and Hwy. 26 and Expanded 1999 is en route to the University of Wisconsin and Wisconsin Dells (2.5 million annual visitors). Average daily traffic on I-94 is 29,000 and on Hwy. 26, over 13,000. PARKING RATIO 5.22:1 LOCATION / DIRECTIONS I-94 at Hwy. 26. Thirty miles east of Madison and 35 miles west of RADIUS POPULATION Milwaukee, Wisconsin. 15 miles: 114,415 30 miles: 703,139 — Take I-94 to Hwy. 26, Exit 267 45 miles: 2,511,808 AVERAGE HH INCOME 30 miles: $80,407 Information as of 5/1/17. Source: SPG Research; trade area demographic information per STI: PopStats (2016). MASTER PLAN DRESSBARN OLD 26 RD. NIKE FACTORY STORE GAP OUTLET I-94 COLUMBIA SPORTSWEAR POLO RALPH LAUREN UNDER FACTORY STORE ARMOUR EDDIE BAUER OUTLET OLD NAVY NORTH LINMAR LN. -

Bankruptcy Forms for Non-Individuals, Is Available

Case 17-31455 Doc 1 Filed 09/01/17 Entered 09/01/17 17:27:08 Desc Main Document Page 1 of 53 Fill in this information to identify your case: United States Bankruptcy Court for the: WESTERN DISTRICT OF NORTH CAROLINA Case number (if known) Chapter 11 Check if this an amended filing Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy 4/16 If more space is needed, attach a separate sheet to this form. On the top of any additional pages, write the debtor's name and case number (if known). For more information, a separate document, Instructions for Bankruptcy Forms for Non-Individuals, is available. 1. Debtor's name Portrait Innovations, Inc. 2. All other names debtor used in the last 8 years Include any assumed names, trade names and doing business as names 3. Debtor's federal Employer Identification 56-2179394 Number (EIN) 4. Debtor's address Principal place of business Mailing address, if different from principal place of business 2016 Ayrsley Town Blvd., Suite 200 Charlotte, NC 28273 Number, Street, City, State & ZIP Code P.O. Box, Number, Street, City, State & ZIP Code Mecklenburg Location of principal assets, if different from principal County place of business Number, Street, City, State & ZIP Code 5. Debtor's website (URL) www.portraitinnovations.com 6. Type of debtor Corporation (including Limited Liability Company (LLC) and Limited Liability Partnership (LLP)) Partnership (excluding LLP) Other. Specify: Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy page 1 Case 17-31455 Doc 1 Filed 09/01/17 Entered 09/01/17 17:27:08 Desc Main Document Page 2 of 53 Debtor Portrait Innovations, Inc. -

Store Listing

APPENDIX C STORE LISTING All shipments must be shipped to the Dry Goods Distribution Center at with the specific store number indicated on the Shipping Label, Carton, and Packing Slip. Do not ship directly to the store. DRY GOODS - Distribution Center 6565 Brady Street Davenport, IA 52806 Store # Initials Store Name/Location Store # Initials Store Name/Location 1001 FXVY Fox Valley/Aurora, IL 1040* SLIN Southlake Mall/Merrilville, IN 1002 WFLD Woodfield Mall/Schaumburg, IL 1041* PCMI Partridge Creek/Clinton Township, MI 1003 WSTN West Towne/Madison, WI 1042* DPIL Deer Park Town Center/Deer Park, IL 1004 MYFR Mayfair Mall/Milwaukee, WI 1043* OPKS Oak Park Mall/Overland Park, KS 1005 TWOK Twelve Oaks Mall/Detroit, MI 1044* EWMI Eastwood Towne Center/Lansing, MI 1006 RSDL Rosedale Mall/Roseville, MN 1045* NLNC Northlake Mall/Charlotte, NC 1007 ORSQ Orland Square/Orland Park, IL 1046* LJIL Louis Joliet Mall/Joliet, IL 1008 JDCR Jordan Creek Mall/West Des Moines, IA 1047** SPOH SouthPark Mall/Strongsville, OH 1009 STDL Southdale Center/Edina, MN 1048** BPOH Beachwood Place/Beachwood, OH 1010 CRIA Coralridge Mall/Coralville, IA 1049** CVNC Crabtree Valley Mall/Raleigh, NC 1011 HWIL Westfield Hawthorn/Vernon Hills, IL 1050** CSTN CoolSprings Galleria/Franklin, TN 1012 APMN Apache Mall/Rochester, MN 1051** GHTN Mall at Green Hills/Nashville, TN 1013 FMIN Fashion Mall/Indianapolis, IN 1052** FPOH Franklin Park Mall/Toledo, OH 1014 CRMN Crossroads Center/St. Cloud, MN 1053** GWNE Gateway Mall/Lincoln, NE 1015 RDMN Ridgedale Center/Minnetonka, MN -

Pleasant Prairie Premium Outlets® the Simon Experience — Where Brands & Communities Come Together

PLEASANT PRAIRIE PREMIUM OUTLETS® THE SIMON EXPERIENCE — WHERE BRANDS & COMMUNITIES COME TOGETHER More than real estate, we are a company of experiences. For our guests, we provide distinctive shopping, dining and entertainment. For our retailers, we offer the unique opportunity to thrive in the best retail real estate in the best markets. From new projects and redevelopments to acquisitions and mergers, we are continuously evaluating our portfolio to enhance the Simon experience - places where people choose to shop and retailers want to be. We deliver: SCALE Largest global owner of retail real estate including Malls, Simon Premium Outlets® and The Mills® QUALITY Iconic, irreplaceable properties in great locations INVESTMENT Active portfolio management increases productivity and returns GROWTH Core business and strategic acquisitions drive performance EXPERIENCE Decades of expertise in development, ownership, and management That’s the advantage of leasing with Simon. PROPERTY OVERVIEW ® Shorewood PLEASANT PRAIRIE PREMIUM OUTLETS Madison 94 18 Milwaukee PLEASANT PRAIRIE, WI Fort Atkinson 94 Oak Creek 12 PLEASANTLake PRAIRIE43 Geneva 14 PREMIUM OUTLETS Racine MAJOR METROPOLITAN AREAS SELECT TENANTS PLEASANT PRAIRIE, WI 41 Kenosha Chicago, IL: 60 miles Ann Taylor Factory Store, Arc’teryx I Salomon, Banana Republic Factory Milwaukee: 35 miles Store, Brooks Brothers Factory Store, Calvin Klein Company Store, Lake Michigan WI Beloit Coach Factory Store, Cole Haan Outlet, Express Factory Outlet, Gap Rockford IL 14 North RETAIL Factory Store, HUGO BOSS Factory Store, J.Crew Factory, kate spade new Chicago york, LACOSTE Outlet, Michael Kors Outlet, NikeFactoryStore, The North 90 Woodstock 94 GLA (sq. ft.) 403,000; 90 stores Face, Polo Ralph Lauren Factory Store, UGG® Australia, Under Armour 51 41 Factory House Evanston 39 20 OPENING DATES 94 29 TOURISM / TRAFFIC Wheaton Rochelle 80 Opened 1988 Chicago Expanded 2006 Pleasant Prairie is an outlet shopping destination that is well established throughout Illinois and Wisconsin.