Njokoya Hazvibviri R113077n

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ecobank Group Annual Report 2018 Building

BUILDING AFRICA’S FINANCIAL FUTURE ECOBANK GROUP ANNUAL REPORT 2018 BUILDING AFRICA’S FINANCIAL FUTURE ECOBANK GROUP ANNUAL REPORT 2018 ECOBANK GROUP ANNUAL REPORT CONTENTS 05 Performance Highlights 08 Ecobank is the leading Pan-African Banking Institution 09 Business Segments 10 Our Pan-African Footprint 15 Board and Management Reports 16 Group Chairman’s Statement 22 Group Chief Executive’s Review 32 Consumer Bank 36 Commercial Bank 40 Corporate and Investment Bank 45 Corporate Governance 46 Board of Directors 48 Directors’ Biographies 53 Directors’ Report 56 Group Executive Committee 58 Corporate Governance Report 78 Sustainability Report 94 People Report 101 Risk Management 141 Business and Financial Review 163 Financial Statements 164 Statement of Directors’ Responsibilities 165 Auditors’ Report 173 Consolidated Financial Statements 178 Notes to Consolidated Financial Statements 298 Five-year Summary Financials 299 Parent Company’s Financial Statements 305 Corporate Information 3 ECOBANK GROUP ANNUAL REPORT 3 PERFORMANCE HIGHLIGHTS 5 ECOBANK GROUP ANNUAL REPORT PERFORMANCE HIGHLIGHTS For the year ended 31 December (in millions of US dollars, except per share and ratio data) 2018 2017 Selected income statement data Operating income (net revenue) 1,825 1,831 Operating expenses 1,123 1,132 Operating profit before impairment losses & taxation 702 700 Impairment losses on financial assets 264 411 Profit before tax 436 288 Profit for the year 329 229 Profit attributable to ETI shareholders 262 179 Profit attributable per share ($): Basic -

Faculty of Commerce

FACULTY OF COMMERCE DEPARTMENT OF BANKING AND FINANCE IMPACT OF GREEN BANKING STRATEGIES ON CUSTOMER SATISFACTION: A CASE OF COMMERCIAL BANKS IN ZIMBABWE BY EDWIN DEMERA STUDENT NUMBER: R156409C SUPERVISOR: PROFESSOR L. CHIKOKO THIS DISSERTATION IS SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENTS OF THE MASTER OF COMMERCE IN BANKING AND FINANCE DEGREE IN THE DEPARTMENT OF BANKING AND FINANCE AT MIDLANDS STATE UNIVERSITY OCTOBER 2019 GWERU: ZIMBABWE RELEASE FORM NAME OF STUDENT: EDWIN DEMERA DISSERTATION TITLE: IMPACT OF GREEN BANKING STRATEGIES ON CUSTOMER SATISFACTION: A CASE OF COMMERCIAL BANKS IN ZIMBABWE. DEGREE TITLE: MASTER OF COMMERCE DEGREE IN BANKING AND FINANCE YEAR THE DEGREE IS GRANTED: 2019 Permission is hereby granted to Midlands State University to produce single copies of this project and lend or sell such copies for private, scholarly or scientific research purposes only. The author reserves other publication rights neither the project nor extensive extracts from it may be printed or otherwise reproduced without the author’s written permission. SIGNED ………………………………………………….. PERMANENT ADDRESS 18633 Unit L, Seke, Chitungwiza, Zimbabwe DATE October 2019 i APPROVAL FORM The undersigned certify that they have read and recommend to Midlands State University for acceptance a research project titled “Impact of green banking strategies on customer satisfaction: A case of commercial banks in Zimbabwe” submitted by Edwin Demera in partial fulfilment of the requirements for the Master of Commerce Degree in Banking and Finance. …………………………………………. …………………………………………. SUPERVISOR DATE …………………………………………. …………………………………………. CHAIRPERSON DATE ii DECLARATION I, Edwin Demera, declare that this dissertation is my original work. It is being submitted in partial fulfillment of the requirements of the Master of Commerce in Banking and Finance Degree in the Faculty of Commerce at Midlands State University. -

WT/TPR/S/398/Rev.1 30 November 2020 (20-8614) Page

WT/TPR/S/398/Rev.1 30 November 2020 (20-8614) Page: 1/119 Trade Policy Review Body TRADE POLICY REVIEW REPORT BY THE SECRETARIAT ZIMBABWE Revision This report, prepared for the third Trade Policy Review of Zimbabwe, has been drawn up by the WTO Secretariat on its own responsibility. The Secretariat has, as required by the Agreement establishing the Trade Policy Review Mechanism (Annex 3 of the Marrakesh Agreement Establishing the World Trade Organization), sought clarification from Zimbabwe on its trade policies and practices. Any technical questions arising from this report may be addressed to: Mr. Jacques Degbelo (tel.: 022 739 5583), Mr. Thomas Friedheim (tel.: 022 739 5083), and Ms. Catherine Hennis-Pierre (tel.: 022 739 5640). Document WT/TPR/G/398 contains the policy statement submitted by Zimbabwe. Note: This report was drafted in English. WT/TPR/S/398/Rev.1 • Zimbabwe - 2 - CONTENTS SUMMARY ........................................................................................................................ 7 1 ECONOMIC ENVIRONMENT ........................................................................................ 10 1.1 Main Features of the Economy .....................................................................................10 1.2 Recent Economic Developments ...................................................................................10 1.2.1 Monetary and exchange rate policies ..........................................................................14 1.2.2 Fiscal policy ............................................................................................................17 -

Banking for Africa's Tomorrow, Today

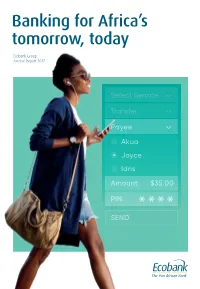

Banking for Africa’s tomorrow, today Ecobank Group Annual Report 2017 Select Service Transfer Payee Akua Joyce Idris Amount: $35.00 PIN: SEND Banking for Africa’s tomorrow, today Ecobank Group Annual Report 2017 2017 Annual Report 2 Contents Contents 3 Performance Highlights 04 2017 Performance Highlights 06 A leading pan-African Bank 08 Business Model 09 Our Pan-African footprint 10 Board and Management Reports 12 Group Chairman’s statement 14 Group Chief Executive’s review 17 Consumer Bank 25 Commercial Bank 27 Corporate and Investment Bank 29 Corporate Governance 32 Board of Directors 34 Directors’ biographies 36 Directors’ report 41 Corporate Governance report 43 Sustainability report 58 People report 66 Risk Management 70 Business and Financial Review 102 Financial Statements 120 Statement of Directors’ responsibilities 122 Auditors’ report 123 Consolidated financial statements 128 Notes to consolidated financial statements 133 Five-year summary financials 213 Parent Company’s financial statements 214 Corporate Information 218 Executive management 220 Share capital overview 222 Holding company and subsidiaries 225 Shareholder contacts 226 Customer contact centers 227 2017 Annual Report 4 Our 2017 results were substantially better than in 2016 with marked improvements from all our three divisions, especially in our Corporate and Investment Bank. Ecobank achieved substantial cost savings as we ‘right-sized’ our businesses whilst we also restricted lending as we embedded greater discipline into our risk management procedures and took decisive -

Banking for Africa's Tomorrow, Today

Banking for Africa’s tomorrow, today Ecobank Group Annual Report 2017 Select Service Transfer Payee Akua Joyce Idris Amount: $35.00 PIN: SEND Banking for Africa’s tomorrow, today Ecobank Group Annual Report 2017 2017 Annual Report 2 Contents Contents 3 Performance Highlights 04 2017 Performance Highlights 06 A leading pan-African Bank 08 Business Model 09 Our Pan-African footprint 10 Board and Management Reports 12 Group Chairman’s statement 14 Group Chief Executive’s review 17 Consumer Bank 25 Commercial Bank 27 Corporate and Investment Bank 29 Corporate Governance 32 Board of Directors 34 Directors’ biographies 36 Directors’ report 41 Corporate Governance report 43 Sustainability report 58 People report 66 Risk Management 70 Business and Financial Review 102 Financial Statements 120 Statement of Directors’ responsibilities 122 Auditors’ report 123 Consolidated financial statements 128 Notes to consolidated financial statements 133 Five-year summary financials 213 Parent Company’s financial statements 214 Corporate Information 218 Executive management 220 Share capital overview 222 Holding company and subsidiaries 225 Shareholder contacts 226 Customer contact centers 227 2017 Annual Report 4 Our 2017 results were substantially better than in 2016 with marked improvements from all our three divisions, especially in our Corporate and Investment Bank. Ecobank achieved substantial cost savings as we ‘right-sized’ our businesses whilst we also restricted lending as we embedded greater discipline into our risk management procedures and took decisive -

ECOBANK ZIMBABWE LIMITED Versus DAINSMEAL INVESTMENTS (PRIVATE) LIMITED and TENDAI CHIDYAUSIKU and TIRIVANGANI CHIDYAUSIKU and CROWHILL FARM (PRIVATE) LIMITED

1 HH 170-20 HC 5303/19 ECOBANK ZIMBABWE LIMITED versus DAINSMEAL INVESTMENTS (PRIVATE) LIMITED and TENDAI CHIDYAUSIKU and TIRIVANGANI CHIDYAUSIKU and CROWHILL FARM (PRIVATE) LIMITED HIGH COURT OF ZIMBABWE CHIKOWERO J HARARE, 17 February 2020 and 4 March 2020 Opposed application K. Kanyemba, for the applicant K. Kachambwa, for the respondents CHIKOWERO J: This is an application for summary judgment. On 21 June 2019 applicant issued summons against respondents for repayment of the sum of ZWL$298 801-80 plus interest, collection commission and costs on the higher scale. Respondents entered appearance to defend and requested for further particulars. This prompted the applicant to institute this application. The principal claim arose from a loan in the sum of ZWL$300 000 which the applicant advanced to the first respondent in terms of a written loan agreement. The second and third respondents bound themselves as sureties and co-principal debtors; having appended their signatures to Unlimited Personal Guarantees. The fourth respondent signed an Irrevocable Unlimited Cross Company Guarantee and bound itself as surety and co-principal debtor. The first respondent did not repay the loan in terms of the loan agreement. It made part- payments. 2 HH 170-20 HC 5303/19 Receipt of the summons was the result of this state of affairs. But the matter itself turns on whether the court application for summary judgment is valid. In Savanna Tobacco Company (Private) Limited v (1) Al Shams Global Limited (2) Interfin Banking Corporation Limited SC 25/18, at p 6 of the cyclostyled judgment, quoted with approval are the following words of MAKARAU JP (as she then was) in CABS v Ndahwi HH 18/10: “Summary judgment proceedings demand different considerations. -

AFRICAN BANKS the Race to Transform This Is a Free PDF of Our Previous Edition of the Top 200 Banks

2019 REVIEW TOP AFRICAN BANKS The race to transform This is a free PDF of our previous edition of the Top 200 Banks. For the latest edition, subscribe to The Africa Report, or get in touch - [email protected] The Africa Report Subscribe now to get the full picture Discover The Africa Report TOP 200 AFRICAN BANKS 2 Contents 03 OVERVIEW Bank to the future The race to transform 05 RANKING Our exclusive list NICHOLAS NORBROOK [email protected] 11 PROFILE Godwin Emefiele As these words are written – in fintechs that are not encumbered 13 SOUTH AFRICA early 2021 – the outlook could not brick-and-mortar legacies. Pain at home and joy be more different for the African With the pandemic switching the abroad banks measured in this 2018 rank- digital economy into overdrive, ing. Pandemic obliges. The debt banks that get left behind will find overhang many African countries it harder than ever to catch up. 17 INTERVIEW are currently facing was present The consumer of tomorrow does Jim Ovia back then but was nowhere near as not want to stand in a line in your systemically threatening. banking hall, ever. 19 DEBATE Zambia became the first default As Microsoft founder and phi- Private equity vs. of the coronavirus era in November, lanthropist Bill Gates once said: public markets when spiraling debts forced the “Banking is necessary, banks are country to miss a payment to re- not”. James Mwangi, the CEO of imburse its creditors. Kenya’s Equity Bank, told The 23 FINTECH But there are echoes that will be Africa Report last September that Is there a bubble in familiar. -

DEPUTY SHERIFF HARARE Versus METBANK ZIMBABWE and ECOBANK ZIMBABWE LIMITED

1 HH 230-13 HC 7831-12 DEPUTY SHERIFF HARARE versus METBANK ZIMBABWE and ECOBANK ZIMBABWE LIMITED HIGH COURT OF ZIMBABWE CHIGUMBA J HARARE, 2 April 2013 & 24 July 2013 F. Girach , for the Judgment Creditor T Mpofu , for the respondent Opposed Application CHIGUMBA J: These are interpleader proceedings brought by the applicant, the Deputy Sheriff of Harare, in terms of Order 30 r 205 of the High Court Rules, 1971. The relief that the applicant seeks is for the claimant and or alternatively the judgment creditor’s claim to be dismissed, with costs following the cause. The background giving rise to this matter is as follows: During the course and scope of carrying out his duties as Deputy Sheriff of Harare, namely the execution of a writ in the case between Ecobank Zimbabwe Limited, Borlscade Investments (Pvt) Ltd and 3 Ors, case number HC 10435/11B, the applicant attached certain funds being held in trust by Metbank Zimbabwe (hereinafter referred to as Metbank. The writ of execution had been issued on 8 June 2012, and, according to the notice of seizure and attachment Borlscade Investments (Private) Limited (hereinafter referred to as Borlscade) was indebted to Ecobank Zimbabwe Limited (hereinafter referred to as Ecobank) in the sum of US$3 862 360, 00 in respect of capital and costs, and a total sum of US$5 431 321, 42 when interest and commission were added. The claimant, Metbank, admitted that judgment in default was obtained by the respondent Ecobank against Borlscade, Cecil Rhanniel Chengetai Muderede and Michelle Fadzai Muderede (the debtors) under case number HC 7640/11, on 2 May 2012. -

Penresa Focus on Zimbabwe

PENRESA FOCUS ON ZIMBABWE AUGUST 2018 EDITION Produced in association with Inside this issue, exclusive interviews with H.E. Emmerson Mnangagwa Hon. Constantino Chiwenga Hon. Patrick Chinamasa Hon. Supa Mandiwanzira #visitzimbabwe ZIMBABWE Open For Business Under the new dispensation of President Mnangagwa, Zimbabwe’s economic transformation is driven by a stable political environment, improved business confidence, re-engagement of bilateral investments in the country and anticipated turnaround from key economic sectors such as agriculture, mining, industry, ICT and tourism. t the World Economic Forum in Davos this business, all moving towards the national January, President Emmerson Dambudzo vision to be a middle-income country by Mnangagwa put the global marketplace 2030. on notice that Zimbabwe is now “open for Since his announcement, the spirit of business.” Since coming into power last the new dispensation has spread outside year in November, ED, as he is affectionately the borders and the nation has been hugely known, has made his intention clear that encouraged by the goodwill it has received Zimbabwe has to discard its isolationist from abroad. Dr. John Mangudya, Governor A policies which led to the country being of the Reserve Bank of Zimbabwe, states: behind by nearly two decades. He has “We want to increase the footprint of underscored the urgent need to pursue business in Zimbabwe. It means that rapid economic growth and a trajectory of we are changing the narrative, from a transformation. “Opening up Zimbabwe closed economy to an open economy.” for business means that we can trade This renewed domestic and foreign investor freely with the rest of the world and that confidence has seen Zimbabwe’s projected we can access capital freely and invest economic growth increase from 3.7% to more in the infrastructure,” says Lazarus 4.5% in 2018. -

2011 Annual Report

ZIMBABWE'S PRE-EMINENT PRIVATE EQUITY INVESTMENT COMPANY ANNUAL REPORT 2011 CONTENTS LETTER to SHAREHOLDERS 03 Directorate 13 2011 FINANCIAL STATEMENTS 20 INDEPENDENT AUDITOR'S REPORT 20 Statement OF FINANCIAL POSITION 21 Statement OF COMPREHENSIVE INCOME 22 Statement OF CASHflows 23 Statement OF CHANGES IN EQUITY 24 notes to THE FINANCIAL statements 25 01 BRAINWORKS CAPITAL MANAGEMENT (Private) LIMITED WWW.brainworkscapital.COM ANNUAL REPORT 2011 WE ARE A MEDIUM to lonG TERM INVESTOR 02 BRAINWORKS CAPITAL MANAGEMENT (Private) LIMITED WWW.brainworkscapital.COM ANNUAL REPORT 2011 LETTER TO SHAREHOLDERS Dear Shareholders We are pleased to present the inaugural annual report to shareholders of Brainworks Capital Management (Private) Limited (herein referred to as “the Company”) for the seven months ended 31 December 2011. In May 2011, the Company, a private equity investment firm focusing on investing in Zimbabwe, was launched. Since the beginning of 2011, the operating environment has been challenging, but we remain confident in the future of this country and the opportunities it offers. Our belief in deploying intellectual capital, operating expertise and financial capital to grow value in Zimbabwe continues to be central in our stated investment model of co-investing with outstanding international operating partners in high growth opportunities. We abide by the set of values listed below which we believe to be pivotal to our success: 1. INTEGRITY We strive to provide services to stakeholders with the highest levels of integrity. This is essential to achieving the shared goal of creating value for all stakeholders. 2. RESPECT We believe in respect amongst team members and for all stakeholders thereby creating lasting relationships. -

Zimbabwe Was Funded by Finmark Trust and Produced by Cenfri

THIS REPORT WAS PRODUCED BY THE CENTRE FOR FINANCIAL REGULATION AND INCLUSION (CENFRI) AUTHORS Hennie Bester, Christine Hougaard, Wadzanai Machena, Catherine Denoon-Stevens, Waqas Rana, Comfort Phelane, and Jaco Weideman. In-country support & stakeholder coordination: Africa Corporate Advisors (ACA). PARTNERING FOR A COMMON PURPOSE Making Access Possible (MAP) is a multi-country initiative to support financial inclusion through a process of evidence-based country diagnostic and stakeholder dialogue, leading to the development of national financial inclusion roadmaps that identify key drivers of financial inclusion and recommended action. Through its design, MAP seeks to strengthen and focus the domestic development dialogue on financial inclusion. The global project seeks to engage with various other international platforms and entities impacting on financial inclusion, using the evidence gathered at the country level. The MAP methodology and process has been developed jointly by United Nations Capital Development Fund (UNCDF), FinMark Trust (FMT) and the Centre for Financial Regulation and Inclusion (Cenfri) to foster inclusive financial sector growth. At country level, the core MAP partners, collaborate with Government, other key stakeholders and donors to ensure an inclusive, holistic process. MAP Zimbabwe was funded by FinMark Trust and produced by Cenfri. ACKNOWLEDGEMENTS The authors would like to extend their gratitude to all of those who assisted us in compiling this report. The Ministry of Finance and Economic Development (MOFED) -

Ecobank Has the Network Advantage Customers, Products, Geography

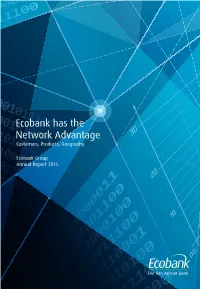

Ecobank has the Network Advantage Customers, Products, Geography. Ecobank Group Annual Report 2015 Contents Contents 2015 Highlights 02 Ecobank at a glance 04 Unique pan-African footprint 06 Performance highlights 08 Board and Management Reports 10 Board of Directors 12 Directors’ biographies 14 Group Chairman’s statement 18 Directors’ report 21 Group Chief Executive’s review 24 Group Chief Operating Officer’s review 30 Corporate and Investment Bank 32 Domestic Bank 33 Treasury 34 Business and Financial Review 36 Corporate Governance 64 Corporate Governance report 66 Sustainability report 81 People report 96 Risk Management 100 Financial Statements 126 Statement of Directors’ responsibilities 128 Auditors’ report 129 Consolidated financial statements 130 Notes to consolidated financial statements 135 Five-year summary financials 217 Parent Company’s financial statements 218 Corporate Information 222 Executive management 224 Shareholder information 226 Holding company and subsidiaries 233 Shareholder contacts 234 Customer contact centers 235 01 2015 Annual Report 2015 highlights Our challenge remains to extract the maximum shareholder value from Africa’s largest financial services platform. With a clear strategic roadmap to market leadership in Middle Africa and a reinvigorated senior management team to implement it, we are confident of achieving our medium-term objectives. 02 03 2015 Annual Report Ecobank is the leading pan-African banking institution in Africa Founded in 1985 and headquartered in Lomé, Togo, Ecobank provides banking, consumer and commercial finance, investments, and securities and asset management to approximately 11 million customers ranging from individuals, small and medium-sized enterprises, regional and multinational corporations, financial institutions and international organisations through 1,268 branches and offices, 2,773 ATMs, the internet (ecobank.com) and mobile banking.