AFRICAN BANKS the Race to Transform This Is a Free PDF of Our Previous Edition of the Top 200 Banks

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

International Comparison of Bank Fraud

Journal of Cybersecurity, 3(2), 2017, 109–125 doi: 10.1093/cybsec/tyx011 Research paper Research paper International comparison of bank fraud reimbursement: customer perceptions and contractual terms Ingolf Becker,1,* Alice Hutchings,2 Ruba Abu-Salma,1 Ross Anderson,2 Nicholas Bohm,3 Steven J. Murdoch,1 M. Angela Sasse,1 and Gianluca Stringhini1 1Computer Science Department, University College London, Gower Street, London WC1E 6BT; 2 University of Cambridge Computer Laboratory, 15 JJ Thomson Avenue, CB3 0FD; 3Foundation for Information Policy Research *Corresponding author: E-mail: [email protected] Received 7 May 2017; accepted 17 November 2017 Abstract The study presented in this article investigated to what extent bank customers understand the terms and conditions (T&Cs) they have signed up to. If many customers are not able to understand T&Cs and the behaviours they are expected to comply with, they risk not being compensated when their accounts are breached. An expert analysis of 30 bank contracts across 25 countries found that most contract terms were too vague for customers to infer required behaviour. In some cases the rules vary for different products, meaning the advice can be contradictory at worst. While many banks allow customers to write Personal identification numbers (PINs) down (as long as they are disguised and not kept with the card), 20% of banks categorically forbid writing PINs down, and a handful stipulate that the customer have a unique PIN for each account. We tested our findings in a survey with 151 participants in Germany, the USA and UK. They mostly agree: only 35% fully understand the T&Cs, and 28% find important sections are unclear. -

Ecobank Group Annual Report 2018 Building

BUILDING AFRICA’S FINANCIAL FUTURE ECOBANK GROUP ANNUAL REPORT 2018 BUILDING AFRICA’S FINANCIAL FUTURE ECOBANK GROUP ANNUAL REPORT 2018 ECOBANK GROUP ANNUAL REPORT CONTENTS 05 Performance Highlights 08 Ecobank is the leading Pan-African Banking Institution 09 Business Segments 10 Our Pan-African Footprint 15 Board and Management Reports 16 Group Chairman’s Statement 22 Group Chief Executive’s Review 32 Consumer Bank 36 Commercial Bank 40 Corporate and Investment Bank 45 Corporate Governance 46 Board of Directors 48 Directors’ Biographies 53 Directors’ Report 56 Group Executive Committee 58 Corporate Governance Report 78 Sustainability Report 94 People Report 101 Risk Management 141 Business and Financial Review 163 Financial Statements 164 Statement of Directors’ Responsibilities 165 Auditors’ Report 173 Consolidated Financial Statements 178 Notes to Consolidated Financial Statements 298 Five-year Summary Financials 299 Parent Company’s Financial Statements 305 Corporate Information 3 ECOBANK GROUP ANNUAL REPORT 3 PERFORMANCE HIGHLIGHTS 5 ECOBANK GROUP ANNUAL REPORT PERFORMANCE HIGHLIGHTS For the year ended 31 December (in millions of US dollars, except per share and ratio data) 2018 2017 Selected income statement data Operating income (net revenue) 1,825 1,831 Operating expenses 1,123 1,132 Operating profit before impairment losses & taxation 702 700 Impairment losses on financial assets 264 411 Profit before tax 436 288 Profit for the year 329 229 Profit attributable to ETI shareholders 262 179 Profit attributable per share ($): Basic -

African Markets Revealed

AFRICAN MARKETS REVEALED SEPTEMBER 2020 • Steven Barrow • Ferishka Bharuth • Mulalo Madula • Angeline Moseki • Fausio Mussa • Jibran Qureishi • Dmitry Shishkin • Gbolahan Taiwo www.standardbank.com/research 1 Standard Bank African Markets Revealed September 2020 Recovering, but not out of the woods • The worst of the pandemic will arguably be reflected in Q2:20 GDP growth outcomes. Of the countries in our coverage, we see only a handful of economies escaping recession in 2020. • Economic growth in Q2:20 contracted by 6.1% y/y, 3.3% y/y, and 3.2% y/y in Nigeria, Mozambique and Uganda respectively. The Ghanaian economy too contracted by 3.2% y/y in Q2:20, even worse than the 0.4% y/y contraction that we forecast for our bear scenario in the May edition of this publication. • The more diversified economies and those with large subsistence agriculture sectors could post mild, yet positive, growth in 2020. Most East African countries fall into this bracket. Egypt too might also avoid a technical recession this year. • However, Nigeria, Angola, Zambia and even Botswana, being overly reliant on just a few sectors to drive growth, will most likely contract this year. The only question is by how much? • Tourism-dependent economies will take a hit. We still don’t see any meaningful recovery in tourism until a global vaccine is at hand. The weakness in the tourism sector is mostly a BOP problem rather than a growth problem for many African countries. However, the service value chain that relies on a robust tourism sector too, will most likely weigh down growth in these economies. -

Public Notice

PUBLIC NOTICE PROVISIONAL LIST OF TAXPAYERS EXEMPTED FROM 6% WITHHOLDING TAX FOR JANUARY – JUNE 2016 Section 119 (5) (f) (ii) of the Income Tax Act, Cap. 340 Uganda Revenue Authority hereby notifies the public that the list of taxpayers below, having satisfactorily fulfilled the requirements for this facility; will be exempted from 6% withholding tax for the period 1st January 2016 to 30th June 2016 PROVISIONAL WITHHOLDING TAX LIST FOR THE PERIOD JANUARY - JUNE 2016 SN TIN TAXPAYER NAME 1 1000380928 3R AGRO INDUSTRIES LIMITED 2 1000049868 3-Z FOUNDATION (U) LTD 3 1000024265 ABC CAPITAL BANK LIMITED 4 1000033223 AFRICA POLYSACK INDUSTRIES LIMITED 5 1000482081 AFRICAN FIELD EPIDEMIOLOGY NETWORK LTD 6 1000134272 AFRICAN FINE COFFEES ASSOCIATION 7 1000034607 AFRICAN QUEEN LIMITED 8 1000025846 APPLIANCE WORLD LIMITED 9 1000317043 BALYA STINT HARDWARE LIMITED 10 1000025663 BANK OF AFRICA - UGANDA LTD 11 1000025701 BANK OF BARODA (U) LIMITED 12 1000028435 BANK OF UGANDA 13 1000027755 BARCLAYS BANK (U) LTD. BAYLOR COLLEGE OF MEDICINE CHILDRENS FOUNDATION 14 1000098610 UGANDA 15 1000026105 BIDCO UGANDA LIMITED 16 1000026050 BOLLORE AFRICA LOGISTICS UGANDA LIMITED 17 1000038228 BRITISH AIRWAYS 18 1000124037 BYANSI FISHERIES LTD 19 1000024548 CENTENARY RURAL DEVELOPMENT BANK LIMITED 20 1000024303 CENTURY BOTTLING CO. LTD. 21 1001017514 CHILDREN AT RISK ACTION NETWORK 22 1000691587 CHIMPANZEE SANCTUARY & WILDLIFE 23 1000028566 CITIBANK UGANDA LIMITED 24 1000026312 CITY OIL (U) LIMITED 25 1000024410 CIVICON LIMITED 26 1000023516 CIVIL AVIATION AUTHORITY -

Bank Code Finder

No Institution City Heading Branch Name Swift Code 1 AFRICAN BANKING CORPORATION LTD NAIROBI ABCLKENAXXX 2 BANK OF AFRICA KENYA LTD MOMBASA (MOMBASA BRANCH) AFRIKENX002 3 BANK OF AFRICA KENYA LTD NAIROBI AFRIKENXXXX 4 BANK OF BARODA (KENYA) LTD NAIROBI BARBKENAXXX 5 BANK OF INDIA NAIROBI BKIDKENAXXX 6 BARCLAYS BANK OF KENYA, LTD. ELDORET (ELDORET BRANCH) BARCKENXELD 7 BARCLAYS BANK OF KENYA, LTD. MOMBASA (DIGO ROAD MOMBASA) BARCKENXMDR 8 BARCLAYS BANK OF KENYA, LTD. MOMBASA (NKRUMAH ROAD BRANCH) BARCKENXMNR 9 BARCLAYS BANK OF KENYA, LTD. NAIROBI (BACK OFFICE PROCESSING CENTRE, BANK HOUSE) BARCKENXOCB 10 BARCLAYS BANK OF KENYA, LTD. NAIROBI (BARCLAYTRUST) BARCKENXBIS 11 BARCLAYS BANK OF KENYA, LTD. NAIROBI (CARD CENTRE NAIROBI) BARCKENXNCC 12 BARCLAYS BANK OF KENYA, LTD. NAIROBI (DEALERS DEPARTMENT H/O) BARCKENXDLR 13 BARCLAYS BANK OF KENYA, LTD. NAIROBI (NAIROBI DISTRIBUTION CENTRE) BARCKENXNDC 14 BARCLAYS BANK OF KENYA, LTD. NAIROBI (PAYMENTS AND INTERNATIONAL SERVICES) BARCKENXPIS 15 BARCLAYS BANK OF KENYA, LTD. NAIROBI (PLAZA BUSINESS CENTRE) BARCKENXNPB 16 BARCLAYS BANK OF KENYA, LTD. NAIROBI (TRADE PROCESSING CENTRE) BARCKENXTPC 17 BARCLAYS BANK OF KENYA, LTD. NAIROBI (VOUCHER PROCESSING CENTRE) BARCKENXVPC 18 BARCLAYS BANK OF KENYA, LTD. NAIROBI BARCKENXXXX 19 CENTRAL BANK OF KENYA NAIROBI (BANKING DIVISION) CBKEKENXBKG 20 CENTRAL BANK OF KENYA NAIROBI (CURRENCY DIVISION) CBKEKENXCNY 21 CENTRAL BANK OF KENYA NAIROBI (NATIONAL DEBT DIVISION) CBKEKENXNDO 22 CENTRAL BANK OF KENYA NAIROBI CBKEKENXXXX 23 CFC STANBIC BANK LIMITED NAIROBI (STRUCTURED PAYMENTS) SBICKENXSSP 24 CFC STANBIC BANK LIMITED NAIROBI SBICKENXXXX 25 CHARTERHOUSE BANK LIMITED NAIROBI CHBLKENXXXX 26 CHASE BANK (KENYA) LIMITED NAIROBI CKENKENAXXX 27 CITIBANK N.A. NAIROBI NAIROBI (TRADE SERVICES DEPARTMENT) CITIKENATRD 28 CITIBANK N.A. -

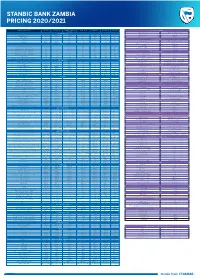

Pricing Guide 2021.Pdf

STANBIC BANK ZAMBIA PRICING 2020/2021 TYPE OF TRANSACTION PRIVATE EXECUTIVE ACHIEVER (EVERYDAY CORPORATE COMMERCIAL ENTERPRISE TAMANGA INVOICE DISCOUNTING BANKING) Arrangement Fee 2.5% Secured 5% unsecured ADMINISTRATION Interest rate LCY Customised Montly Management Fees ZMW 330 ZMW 110 ZMW 55 ZMW 200 ZMW 165 ZMW 150 ZMW 100 Interest rate FCY Customised Debit Activity Fees Free Free Free Free Free Free Free DISTRIBUTOR FINANCE Credit Activity Fees Free Free Free Free Free Free Free Arrangement fee 2.5% Secured 5% unsecured Bundle Pricing ZMW 385 ZMW 165 ZMW 87 N/A N/A N/A N/A DEPOSIT Management fee per quarter Customised Local cheque deposit at branch Free Free Free Free Free Free Free Rollover fee Customised Own Bank cheque within clearing area Free Free Free Free Free Free Free Interest rate (ZMW) Customised Own Bank cheque outside clearing area Free Free Free Free Free Free Free Interest rate (USD) Customised Agent Bank cheque within clearing area Free Free Free Free Free Free Free FOREIGN CURRENCY SERVICES Agent Bank cheque outside clearing area Free Free Free Free Free Free Free Purchase of Foreign Exchange Cash Deposit at Branch Free Free Free Free Free Free Free Foreign notes No charge Bulk Cash Deposit Foreign Currency ( Above $50,000) 1% 1% 1% 1% 1% 1% 1% Telegraphic Transfer/SWIFT (inward) US$20 flat WITHDRAWALS Drafts/Bills/Cheques 1.1% min US$40 plus VAT + Foreign charges At branch within K25,000 ATM limit Free Free ZMW 120 N/A N/A N/A N/A Drafts/Bills/Cheques 1.1% min US$40 plus VAT + Foreign charges Own ATM ZMW 9 ZMW 9 ZMW -

Africa Beyond Covid-19: President George Weah, US Senator Chris

Africa Beyond Covid-19: President George Weah, US Senator Chris Coons, Tony Elumelu and Other Global Leaders at the 2nd UBA Africa Day Conversations Urge Government and Private Sector Collaboration . Demand a new deal in and for Africa . Advocate speedy implementation of AFCFTA . Call for Increased Investment in Digital Connectivity United Bank for Africa (UBA) celebrated Africa Day 2020, by bringing together global leaders at the 2nd UBA Africa Day Conversations, screened live across the continent. UBA helps set the debate around African economic development through its series of “Africa Conversations”. This year, the focus was on the Sustainable Development Goals (SDGs) and the Covid-19 pandemic. Leaders emphasised the need for meaningful collaboration between governments and the private sector, as a requirement for the quick recovery of the economy of the African continent post Covid-19. The panel included the President of Liberia, H.E George Weah; United States Senator Chris Coons; the President & Chairman of the Board of Directors of the African Export–Import Bank (AFREXIMBANK), Professor Benedict Okey Oramah; President, International Committee of the Red Cross (ICRC), Peter Maurer; and was moderated by the Group Chairman, UBA Plc, Tony O. Elumelu. Other leading voices contributing were the Founder, Africa CEO Forum, Amir Ben Yahmed; the Secretary-General of the African Caribbean and Pacific Group of States (ACP), H.E George Chikoti; Administrator, United Nations Development Program (UNDP), Achim Steiner and Donald Kaberuka, the former President of the African Union. Elumelu spoke on the need to mobilise quickly and explained the necessity to identify a more fundamental solution to Africa’s challenges. -

Digital Access: the Future of Financial Inclusion in Africa Acronyms

DIGITAL ACCESS: THE FUTURE OF FINANCIAL INCLUSION IN AFRICA ACRONYMS ADC Alternative Delivery Channel ISO International Organization for Standardization AFSD African Financial Sector Database IT Information Technology ARPU Average Revenue Per User KES Kenyan Shilling API Application Programming Interface KPI Key Performance Indicator ATM Automated Teller Machine KYC Know Your Customer B2P Business to Person LAPO MfB Lift Above Poverty Organization BCEAO Central Bank of West Africa (Banque Centrale Microfinance Bank des Etats de l’Afrique de l’Ouest) M-banking Mobile Banking BOI Banking Operations Intermediary M-wallet Mobile Wallet BVN Bank Verification Number MFI Microfinance Institution CEO Chief Executive Officer MM Mobile Money CBA Commercial Bank of Africa MSME Micro, Small and Medium Enterprise CBN Central Bank of Nigeria MTN Mobile Telephone Network CFA West African Franc, or Central African Franc MNO Mobile Network Operator CGAP Consultative Group to Assist the Poor MVNO Mobile Virtual Network Operator CRM Customer Relationship Management NFC Near Field Communication DFS Digital Financial Services OTC Over the Counter DJ Disc Jockey P2B Person to Business DVD Digital Versatile Disc P2P Person to Person E-banking Electronic Banking PC Personal Computer EFT Electronic Funds Transfer PIN Personal Identification Number EMI e-Money Issuer POS Point of Sale E-money Electronic Money PSP Payment Service Provider E-wallet Electronic Wallet E-warehousing Electronic Warehousing QR Quick Response FCMB First City Monument Bank RCT Randomized -

Financial Market Headlines

| CASABLANCA | 08/31/2021 FINANCIAL MARKET HEADLINES | MOROCCO | ATTIJARIWAFA BANK | NBI up 0.7% in H1 2021 In H1 2021, Attijariwafa bank's NBI recorded an increase of 0.7% to MAD 12.5 Bn compared to MAD 12.4 Bn during the same pe- riod of the previous year. | MOROCCO | BANK OF AFRICA | NBI up 2% in H1 2021 In Q2 2021, Bank Of Africa's NBI recorded a decline of 4% to MAD 3.7 Bn. In H1 2021, Bank Of Africa’s NBI stood at MAD 7.2 Bn, up 2.4%. | MOROCCO | BMCI | A sharp increase of NIGS in H1 2021 Indicators (MAD Mn) H1 2020 H1 2021 Change NBI 1 554 1 514 -2,6% Gross Operating Income 638 544 -14,7% GOI margin 41,0% 35,9% -5,1 pts Cost of risk 494 225 -54,5% NIGS 61 254 313,2% Net margin 4,0% 16,8% +12,8 pts | MOROCCO | CIH BANK | Consolidated NBI up 7% in H1 2021 In H1 2021, CIH Bank's consolidated Net Banking Income amounted to MAD 1,500.6 Mn compared to MAD 1,402.8 Mn in H1 2020, i.e. an increase of 7.0%. | MOROCCO | COSUMAR | Consolidated revenue up 3% in H1 2021 At the end of Q2 2021, Cosumar's consolidated revenue stood at MAD 2,408 Mn, up 9.1% year-on-year. In this context, the opera- tor's consolidated revenue in H1 2021 shows an increase of 2.9% to MAD 4,382 Mn. | MOROCCO | TOTALENERGIES MARKETING MAROC | Sales volume up 17% in H1 2021 In H1 2021, TotalEnergies Marketing Maroc's sales volume increased by 17% to 871 KT against 747 KT a year earlier. -

Stanbic Bank Zambia PMI™ Output Returns to Growth in May

News Release Embargoed until 1030 CAT (0830 UTC) 3 June 2021 Stanbic Bank Zambia PMI™ Output returns to growth in May Key findings PMI sa, >50 = improvement since previous month 60 First rise in activity for 27 months 55 Near-stabilisation of employment 50 45 Sharpest rise in purchase costs since December 40 2016 35 30 '15 '16 '17 '18 '19 '20 '21 Data were collected 12-24 May 2021 Sources: Stanbic Bank, IHS Markit. Output returned to growth in the Zambian private sector meant that firms were able to work through backlogs during May, one month after the same had been the case during May. A modest reduction in outstanding business for new orders. New business ticked back down slightly was recorded, ending a two-month sequence of in the latest survey period, but there were further signs accumulation. that overall business conditions are more conducive to Employment was broadly stable, falling only fractionally growth than has been the case for some time. As a result, and at the joint-slowest pace in the current 16-month firms continued to expand their purchasing activity and sequence of decline. kept their staffing levels broadly unchanged. Firms meanwhile increased their purchasing activity The headline figure derived from the survey is the for the second month running, leading to a further Purchasing Managers’ Index™ (PMI™). Readings above accumulation of inventories as suppliers' delivery times 50.0 signal an improvement in business conditions on improved for the first time in 16 months. Firms reported the previous month, while readings below 50.0 show a that competition among suppliers had been behind deterioration. -

Money Transfer Systems: the Practice and Potential for Products in Kenya

Shelter Afrique Building, Mamlaka Road MicroSave-Africa P.O. Box 76436, Nairobi, Kenya Tel: 254 2 2724801/2724806/2726397 An Initiative of Austria/CGAP/DFID/UNDP Fax: 254 2 2720133 Website: www.MicroSave-Africa.com Email: [email protected] PASSING THE BUCK Money Transfer Systems: The Practice and Potential for Products in Kenya Kamau Kabbucho, Cerstin Sander and Peter Mukwana May 2003 PASSING THE BUCK: Money Transfer Systems: The Practice and Potential for Products in Kenya i Kamau Kabbucho, Cerstin Sander and Peter Mukwana Table of Contents EXECUTIVE SUMMARY ............................................................................................................................................IV BACKGROUND ................................................................................................................................................................ IV SUMMARY OF FINDINGS ................................................................................................................................................. IV STRUCTURE OF THE REPORT........................................................................................................................................... VI INTRODUCTION ............................................................................................................................................................ 1 BACKGROUND AND OBJECTIVES ..................................................................................................................................... 1 -

Annual Integrated R E P O

2019 2019 ANNUAL ANNUAL INTEGRATED INTEGRATED REPORT REPORT INTRODUCING THE GROUP.....................................................................................................................................................8 BANK OF AFRICA, more than 60 years of continuous development ................................................................................9 BANK OF AFRICA Today......................................................................................................................................................................................... 11 Shareholders ........................................................................................................................................................................................................................ 13 BANK OF AFRICA Group’s business lines............................................................................................................................................... 16 Geographical presence................................................................................................................................................................................................ 17 A pan-African vocation................................................................................................................................................................................................ 18 Intra-Group synergies for Africa’s development ..................................................................................................................................