The Climate100 Index 3

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

We Want to Help the World Reach Net Zero and Improve People's Lives

BP Sustainability Report 2019 Our purpose is reimagining energy for people and our planet. We want to help the world reach net zero and improve people’s lives. We will aim to dramatically reduce carbon in our operations and production and grow new low carbon businesses, products and services. We will advocate for fundamental and rapid progress towards Paris and strive to be a leader in transparency. We know we don’t have all the answers and will listen to and work with others. We want to be an energy company with purpose; one that is trusted by society, valued by shareholders and motivating for everyone who works at BP. We believe we have the experience and expertise, the relationships and the reach, the skill and the will, to do this. Introduction Message from Bernard Looney 2 Our ambition 4 2019 at a glance Energy in context 8 Sustainability at BP UN Sustainable Development Goals 11 Sustainability at BP 11 Key sustainability issues 14 Our focus areas Climate change and the energy transition 16 Our role in the energy transition 18 Our ‘reduce, improve, create’ framework 20 Accrediting our lower carbon activities 22 Reducing emissions in our operations 23 Improving our products 26 Creating low carbon businesses 30 Safety 36 Process safety 38 Personal safety 39 Safety performance 41 Our value to society 42 Creating social value 44 Social investment 45 Local workers and suppliers 46 Human rights 47 Community engagement 48 Our impact on communities 49 Labour rights 50 Doing business responsibly Environment 54 People 60 Business ethics 68 Navigating our reports Governance Our quick read Human rights governance 74 provides a summary of the Executive oversight of sustainability 74 Sustainability Report, including key Managing risks 75 highlights and performance in 2019. -

FTSE Factsheet

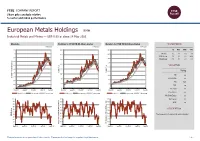

FTSE COMPANY REPORT Share price analysis relative to sector and index performance European Metals Holdings EMH Industrial Metals and Mining — GBP 0.69 at close 14 May 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 14-May-2021 14-May-2021 14-May-2021 1.1 450 900 1D WTD MTD YTD 1 Absolute 0.0 -6.8 -4.2 7.8 400 800 Rel.Sector 1.2 -2.9 -7.5 -20.3 0.9 700 Rel.Market -1.1 -5.5 -4.8 -1.3 350 0.8 600 300 0.7 VALUATION 500 0.6 250 400 Trailing Relative Price Relative 0.5 Price Relative 200 300 PE -ve 0.4 Absolute Price (local currency) (local Price Absolute 150 EV/EBITDA -ve 200 0.3 PB 12.3 100 0.2 100 PCF -ve 0.1 50 0 Div Yield 0.0 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 May-2020 Aug-2020 Nov-2020 Feb-2021 May-2021 Price/Sales +ve Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.0 100 90 90 Div Payout 0.0 90 80 80 ROE -ve 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 40 40 40 The Company is focusing in tin mining industry. -

Templeton Global Equity Income Fund August 31, 2021

FTIF - Templeton Global Equity Income Fund August 31, 2021 FTIF - Templeton Global Equity August 31, 2021 Income Fund Portfolio Holdings The following portfolio data for the Franklin Templeton funds is made available to the public under our Portfolio Holdings Release Policy and is "as of" the date indicated. This portfolio data should not be relied upon as a complete listing of a fund's holdings (or of a fund's top holdings) as information on particular holdings may be withheld if it is in the fund's interest to do so. Additionally, foreign currency forwards are not included in the portfolio data. Instead, the net market value of all currency forward contracts is included in cash and other net assets of the fund. Further, portfolio holdings data of over-the-counter derivative investments such as Credit Default Swaps, Interest Rate Swaps or other Swap contracts list only the name of counterparty to the derivative contract, not the details of the derivative. Complete portfolio data can be found in the semi- and annual financial statements of the fund. Security Security Shares/ Market % of Coupon Maturity Identifier Name Positions Held Value TNA Rate Date B4TX8S1 AIA GROUP LTD 70,295 $839,367 1.10% N/A N/A 012653101 ALBEMARLE CORP 7,404 $1,752,822 2.31% N/A N/A 025816109 AMERICAN EXPRESS CO 12,293 $2,040,146 2.68% N/A N/A BYPBS67 ARCELORMITTAL SA 14,303 $479,701 0.63% N/A N/A 0989529 ASTRAZENECA PLC 11,321 $1,323,868 1.74% N/A N/A 084670702 BERKSHIRE HATHAWAY INC 2,308 $659,557 0.87% N/A N/A 09857L108 BOOKING HOLDINGS INC 520 $1,195,828 1.57% -

Carbon Trust NI

Reducing our carbon footprint An initial action plan for Northern Ireland 02 Reducing our carbon footprint Preface In June 2000, the Royal Commission on The Carbon Trust is a part of the UK Government’s Environmental Pollution (RCEP) published its strategy for developing and implementing this review of energy prospects for the 21st century national framework. The Carbon Trust helps and their environmental implications. This called business and the public sector cut carbon for concerted action to halt the rise in the emissions, and supports the development of low atmospheric concentrations of carbon dioxide carbon technologies. (CO2) and other greenhouse gases, which are beginning to induce substantial climate change on In Northern Ireland, it is working with the Northern a global scale. Ireland Government Departments to adapt this national framework into a programme of practical The RCEP concluded that the only workable way actions that can be implemented at local level. of limiting CO2 emissions (or ‘carbon emissions’) was to allocate national quotas that would As part of this process, the Carbon Trust and Invest converge to a standard allocation per person over NI sponsored a project to develop an action plan 50 to 100 years. that would realise deep reductions in Northern Ireland’s carbon emissions by 2050. For the UK, an international agreement along these lines implies a 60% reduction in carbon The objectives of the project were to: emissions from 1997 by 2050, and 80% by 2100. • Explore how the RCEP recommendation of a 60% In its -

To Arrive at the Total Scores, Each Company Is Marked out of 10 Across

BRITAIN’S MOST ADMIRED COMPANIES THE RESULTS 17th last year as it continues to do well in the growing LNG business, especially in Australia and Brazil. Veteran chief executive Frank Chapman is due to step down in the new year, and in October a row about overstated reserves hit the share price. Some pundits To arrive at the total scores, each company is reckon BG could become a take over target as a result. The biggest climber in the top 10 this year is marked out of 10 across nine criteria, such as quality Petrofac, up to fifth from 68th last year. The oilfield of management, value as a long-term investment, services group may not be as well known as some, but it is doing great business all the same. Its boss, Syrian- financial soundness and capacity to innovate. Here born Ayman Asfari, is one of the growing band of are the top 10 firms by these individual measures wealthy foreign entrepreneurs who choose to make London their operating base and home, to the benefit of both the Exchequer and the employment figures. In fourth place is Rolls-Royce, one of BMAC’s most Financial value as a long-term community and environmental soundness investment responsibility consistent high performers. Hardly a year goes past that it does not feature in the upper reaches of our table, 1= Rightmove 9.00 1 Diageo 8.61 1 Co-operative Bank 8.00 and it has topped its sector – aero and defence engi- 1= Rotork 9.00 2 Berkeley Group 8.40 2 BASF (UK & Ireland) 7.61 neering – for a decade. -

Enhance Innovation and Agility with Digital Twins Executive Summary

Enhance innovation and agility with Digital Twins Executive Summary There’s no denying we live in uncertain and rapidly changing times and companies are looking for every opportunity to become more agile. Digital twins is a rapidly emerging technology that delivers to this end. Not to be confused as a mere dashboard, a digital twin is a virtual replica of a physical object, machine part, system, process or entire lifecycle. Digital twin technology enables real-time monitoring and control, the ability to learn with AI and ML, to autonomously update, self-heal, and even improve systems and designs over time. This paper seeks to achieve four objectives. First, to help the reader understand Digital twin technology and its potential. Second, to provide a structured way of looking at the various use cases and applications of this technology. Third, to feature Microsoft partners who have differentiated capabilities that bring digital twin visions to life. Fourth, to discuss the Azure Digital Twin platform and other investments from Microsoft in this space. Digital twin technology is commonly applied to manufacturing across key applications that span manufacturing scenarios/use-cases. The priority scenarios, or use cases, as they relate in Manufacturing are 1) Product, 2) Factory, 3) Supply Chain, and 4) Spaces. The top applications include configuration management, asset management, process control, performance management and simulation modeling. Configuration management tracks bills of materials, around assets as designed, manufactured, configured, and maintained. E.g. For complex & expensive assets like aircrafts this information is typically maintained by tail number. Asset management deals with telemetry of an asset itself and gives insight in to how something is working. -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

Response: Just Eat Takeaway.Com N. V

NON- CONFIDENTIAL JUST EAT TAKEAWAY.COM Submission to the CMA in response to its request for views on its Provisional Findings in relation to the Amazon/Deliveroo merger inquiry 1 INTRODUCTION AND BACKGROUND 1. In line with the Notice of provisional findings made under Rule 11.3 of the Competition and Markets Authority ("CMA") Rules of Procedure published on the CMA website, Just Eat Takeaway.com N.V. ("JETA") submits its views on the provisional findings of the CMA dated 16 April 2020 (the "Provisional Findings") regarding the anticipated acquisition by Amazon.com BV Investment Holding LLC, a wholly-owned subsidiary of Amazon.com, Inc. ("Amazon") of certain rights and minority shareholding of Roofoods Ltd ("Deliveroo") (the "Transaction"). 2. In the Provisional Findings, the CMA has concluded that the Transaction would not be expected to result in a substantial lessening of competition ("SLC") in either the market for online restaurant platforms or the market for online convenience groceries ("OCG")1 on the basis that, as a result of the Coronavirus ("COVID-19") crisis, Deliveroo is likely to exit the market unless it receives the additional funding available through the Transaction. The CMA has also provisionally found that no less anti-competitive investors were available. 3. JETA considers that this is an unprecedented decision by the CMA and questions whether it is appropriate in the current market circumstances. In its Phase 1 Decision, dated 11 December 20192, the CMA found that the Transaction gives rise to a realistic prospect of an SLC as a result of horizontal effects in the supply of food platforms and OCG in the UK. -

Marketing Particulars

On the Instruction of Lloyds Banking Group TO LET – NEW LEASE AVAILABLE CHESTER, 4 Foregate Street CH1 1HA Location Chester is an historic city located approximately 36 miles south west of Manchester, and approximately 25 miles south of Liverpool. It is located at the western end of the M56 motorway, which links with the M6 and M60 motorways. The property is situated on Foregate Street, the prime retail pitch within Chester city centre. Nearby occupiers include Lloyds Bank, HSBC Bank, WHSmith, Clarks and JD Sports. Description The ground floor comprises a shell unit with open plan floor space. The basement floor consists of ancillary storage and toilets. Accommodation • Prime Retail Location • Heavy Footfall Ground Floor 34.90 sq m 376 sq ft • New lease terms available Basement Floor 78.78 sq m 794 sq ft EPC An EPC can be made available upon Tenure request. The property is available on an FRI Leasehold basis. Viewing Length of term to be negotiated. By appointment via this office: Rent Ross Jackson £40,000 pax. t: + 44 161 233 5492 e: [email protected] Rates CBRE Limited We are informed by the Local Rating Authority that the current rateable Henrietta House, Henrietta Place value of the property is £34,500 and the rates payable are £17,008.50. London W1G 0NB The UBR for 2018/2019 is 49.3 p. Interested parties are advised to make www.cbre.co.uk/retail their own enquiries with the Local Authority for verification purposes. Date of Issue 13 th June 2018 On the Instruction of Lloyds Banking Group TO LET – NEW LEASE AVAILABLE CHESTER, 4 Foregate Street CH1 1HA DISCLAIMER: CBRE Limited CBRE Limited on its behalf and for the Vendors or Lessors of this property whose Agents they are, give notice that: 1. -

Monthly Professional Factsheet Uk Opportunities Fund a Income Shares 31 August 2021

pro.en.xx.20210831.GB00BGV1T511.pdf UK Opportunities Fund A Income Shares For Investment Professionals Only FIDELITY INVESTMENT FUNDS 2 MONTHLY PROFESSIONAL FACTSHEET UK OPPORTUNITIES FUND A INCOME SHARES 31 AUGUST 2021 Strategy Fund Facts Leigh Himsworth identifies specific areas of the market that he believes are capable of Launch date: 01.09.11** delivering consistent growth. Within these themes, he employs disciplined cash flow Portfolio manager: Leigh Himsworth analysis to seek out companies capable of delivering earnings growth without Appointed to fund: 01.09.11 materially increasing their risk profile. On this basis, Leigh builds a high conviction Years at Fidelity: 7 portfolio of quality growth companies. Each holding in the portfolio has a weighting that Fund size: £602m allows it to make a meaningful contribution to performance. Risk management takes Number of positions in fund*: 55 into account factors that could impact a number of companies in the portfolio. Fund reference currency: UK Sterling (GBP) Fund domicile: United Kingdom Fund legal structure: OEIC Management company: FIL Investment Services (UK) Limited Capital guarantee: No Portfolio Turnover Cost (PTC): 0.48% Portfolio Turnover Rate (PTR): 182.08% *A definition of positions can be found on page 3 of this factsheet in the section titled “How data is calculated and presented.” Objectives & Investment Policy Share Class Facts • The fund aims to increase the value of your investment over a period of 5 years or Other share classes may be available. Please refer to the prospectus for more details. more. • The fund will invest at least 70% in shares (and their related securities) of a blend of Launch date: 15.05.19 different sized UK companies. -

The Performance of the Department of Energy & Climate Change 2012-13

DEPARTMENTAL OVERVIEW The performance of the Department of Energy & Climate Change 2012-13 NOVEMBER 2013 Our vision is to help the nation spend wisely. Our public audit perspective helps Parliament hold government to account and improve public services. The National Audit Office scrutinises public spending for Parliament and is independent of government. The Comptroller and Auditor General (C&AG), Amyas Morse, is an Officer of the House of Commons and leads the NAO, which employs some 860 staff. The C&AG certifies the accounts of all government departments and many other public sector bodies. He has statutory authority to examine and report to Parliament on whether departments and the bodies they fund have used their resources efficiently, effectively, and with economy. Our studies evaluate the value for money of public spending, nationally and locally. Our recommendations and reports on good practice help government improve public services, and our work led to audited savings of almost £1.2 billion in 2012. Contents Introduction Aim and scope of this briefing 4 Part One About the Department 5 Part Two Recent NAO work on the Department 24 Appendix One The Department’s sponsored bodies at 1 April 2013 29 Appendix Two Results of the Civil Service People Survey 2012 30 Appendix Three Publications by the NAO on the Department since April 2011 32 Appendix Four Cross-government reports of relevance to the Department since April 2011 34 Links to external websites were valid at the time of publication of this report. The National Audit Office is not responsible for the future validity of the links. -

Resilience of Your Supply Chain… About Us

WE INVITE YOU TO INCREASE THE RESILIENCE OF YOUR SUPPLY CHAIN… ABOUT US The Transported Asset Protection Association (TAPA) was formed 23 years ago by leading global Manufacturers & Logistics Service Providers to make their supply chains more resilient. Transported Asset Protection Association Today, TAPA is the world’s leading Security Expert Network for everyone in the supply chain … and we invite you to join our family. Joining our Association will give you access to supply chain resilience insight, trends and tools as well as industry-leading security standards, training and CARGO CRIME IN EMEA unique networking opportunities with like-minded supply chain professionals. With today’s unprecedented focus on supply chain resilience, TAPA’s presence • Thefts from supply chains cost businesses in Europe alone more than in the Europe, Middle East & Africa (EMEA) region is greater than at any time in €8.2 billion a year* our history … and we are growing at a record pace. I kindly ask you to spend a • All types of products are now a target for cargo thieves** moment reading this invitation to find out more about us. • Cargo thefts recorded in 48 countries in EMEA in 12 months** I would also welcome a conversation with you to answer any further questions you may have. You can reach me at [email protected] • Average annual loss for major cargo crimes = €536,889** I hope we will be speaking soon. • Annual increase in recorded cargo thefts = 114.7%** • Supply chain theft incidents reported to TAPA in EMEA in 12 months** = 8,548 •