Turkey Brief Turkish – Canadian Relations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

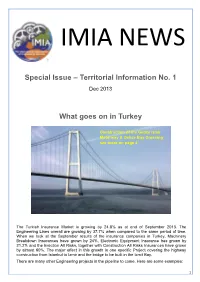

Special Issue – Territorial Information No. 1 What Goes on in Turkey

IMIA NEWS Special Issue – Territorial Information No. 1 Dec 2013 What goes on in Turkey Construction of the Gebze Izmir Motorway & Gebze Bay Crossing see more on page 4 More info p.2 The Turkish Insurance Market is growing by 24.8% as at end of September 2013. The Engineering Lines overall are growing by 37.7% when compared to the same period of time. When we look at the September results of the insurance companies in Turkey, Machinery Breakdown Insurances have grown by 24%, Electronic Equipment Insurance has grown by 21.2% and the Erection All Risks, together with Construction All Risks Insurances have grown by almost 60%. The major effect in this growth is one specific Project covering the highway construction from Istanbul to Izmir and the bridge to be built in the Izmit Bay. There are many other Engineering projects in the pipeline to come. Here are some examples: 1 THE THIRD BOSPHORUS BRIDGE Bridge of Firsts The 3rd Bridge, which is going to be built on the Bosphorus, Istanbul within the Northern Marmara Motorway Project executed by IC Ictas – Astaldi Consortium, is considered the future of transportation and commerce. The 3rd bridge, which is going to be built on the Bosphorus, Istanbul after the Bogazici Bridge, which started operating in 1972, and the Fatih Sultan Mehmet Bridge, which was completed in 1988, is regarded as the bridge of firsts. 8 lanes of motorway and 2 lanes of railway will be located at the same level on the 3rd Bosphorus Bridge, which will be a product of professional engineering and advanced technology built by a team, most of whom are Turkish engineers. -

The Cause of Misfire in Counter-Terrorist Financing Regulation

UNIVERSITY OF CALIFORNIA RIVERSIDE Making a Killing: The Cause of Misfire in Counter-Terrorist Financing Regulation A Dissertation submitted in partial satisfaction of the requirements for the degree of Doctor of Philosophy in Political Science by Ian Oxnevad June 2019 Dissertation Committee: Dr. John Cioffi, Chairperson Dr. Marissa Brookes Dr. Fariba Zarinebaf Copyright by Ian Oxnevad 2019 The Dissertation of Ian Oxnevad is approved: ________________________________________________ ________________________________________________ ________________________________________________ Committee Chairperson University of California, Riverside ABSTRACT OF THE DISSERTATION Making a Killing: The Cause of Misfire in Counter-Terrorist Financing Regulation by Ian Oxnevad Doctor of Philosophy, Graduate Program in Political Science University of California, Riverside, June 2019 Dr. John Cioffi, Chairperson Financial regulations designed to counter the financing of terrorism have spread internationally over past several decades, but little is known about their effectiveness or why certain banks get penalized for financing terrorism while others do not. This research addresses this question and tests for the effects of institutional linkages between banks and states on the enforcement of these regulations. It is hypothesized here that a bank’s institutional link to its home state is necessary to block attempted enforcement. This research utilizes comparative studies of cases in which enforcement and penalization were attempted, and examines the role of institutional links between the bank and state in these outcomes. The case comparisons include five cases in all, with three comprising positive cases in which enforcement was blocked, and two in which penalty occurred. Combined, these cases control for rival variables such as rule of law, state capacity, iv authoritarianism, and membership of a country in a regulatory body while also testing for the impact of institutional linkage between a bank and its state in the country’s national political economy. -

Exploring the Impact of Socio-Political Crises on the Operational Performance of the Turkish Airlines

IBN HALDUN UNIVERSITY SCHOOL OF GRADUATE STUDIES MASTER OF SCIENCE IN AIR TRANSPORT MANAGEMENT MASTER THESIS EXPLORING THE IMPACT OF SOCIO-POLITICAL CRISES ON THE OPERATIONAL PERFORMANCE OF THE TURKISH AIRLINES VİLDAN HAVVA KESİCİ THESIS SUPERVISOR: PROF. MUSTAFA KEMAL YILMAZ ISTANBUL, 2020 IBN HALDUN UNIVERSITY SCHOOL OF GRADUATE STUDIES MASTER OF SCIENCE IN AIR TRANSPORT MANAGEMENT MASTER THESIS EXPLORING THE IMPACT OF SOCIO-POLITICAL CRISES ON THE OPERATIONAL PERFORMANCE OF THE TURKISH AIRLINES by VİLDAN HAVVA KESİCİ A thesis submitted to the School of Graduate Studies in partial fulfillment of the requirements for the degree of Master of Science in Management THESIS SUPERVISOR: PROF. MUSTAFA KEMAL YILMAZ ISTANBUL, 2020 ÖZ SOSYO-POLİTİK KRİZLERİN TÜRK HAVA YOLLARI’NIN FAALİYET PERFORMANSINA ETKİLERİ Kesici, Vildan Havva Hava Taşımacılığı Yönetimi Yüksek Lisans Programı Tez Danışmanı: Prof. Dr. Mustafa Kemal Yılmaz Ocak 2020, 90 sayfa Çalışmada, 2010-2018 döneminde Türkiye’de yaşanan sosyo-politik birtakım krizlerin, Türk Hava Yolları’nın faaliyet peformansı üzerindeki etkisi, arz edilen koltuk kilometre (ASK), ücretli yolcu kilometre (RPK), yolcu doluluk oranı (PLF) ve taşınan yolcu sayıları gibi parametreler değerlendirilerek araştırılmıştır. Bu olaylar kronolojik sıra itibari ile; Gezi Parkı, Rus askeri jetinin vurulması, 15 Temmuz askeri darbe girişimi ve elektronik cihazların yasaklanmasıdır. Söz konusu olayların etkileri bölgesel bazda dört farklı algoritma kullanılarak analiz edilmiştir: (1) nedensel etki analizi, (2) aykırı değer algoritması (ODA), (3) kırılma noktası algoritması (BDA) ve (4) değişim noktası algoritması (CPA). Çalışma bulguları, sosyo-politik krizlerin Türk Hava Yolları'nın faaliyet performansı üzerinde bölgesel olarak sınırlı ölçüde etkileri olduğunu göstermiştir. CPA, Gezi Park döneminde yurtiçi, Afrika ve Kuzey Amerika bölgelerinde RPK’da; Avrupa, Uzak Doğu ve Kuzey Amerika bölgelerinde ASK değerlerinde değişim tespit etmiştir. -

Sustainability Report 2013 Kibar Holding Sustainability Report 2013

SUSTAINABILITY REPORT www.kibar.com TABLE OF CONTENTS ABOUT THE REPORT 3 MESSAGES 4 KİBAR GROUP 6 WORKPLACE 16 OUR ENVIRONMENTAL AWARENESS 19 THE VALUE WE ADD TO THE SOCIETY 24 2 The Sustainability Report 2013 of Kibar Group includes Assan Aluminyum, Assan Gıda, Assan Hanil, Assan Panel and İSPAK. Unless otherwise stated, the information ABOUT related to all companies of Kibar Group is under the title of Kibar Group. GLOBAL COMPACT THE Ten principles of the United Nations Global Compact (UNGC) consist of the titles of human rights, labor standards, environment and anti-corruption. The United Nations Global Compact particularly asks companies to embrace, support and implement REPORT these principles. This report has been prepared in For more information about the principles of the United Nations Global Compact, please accordance with the Global Compact visit http://www.globalcompactturkiye.org/global-compact-turkiye/ilkeler/. Progress Report. The report covers the period of January-December The Global Compact, launched by the United Nations in 2000, is an important initiative 2013. However, certain data is compared to 2011 and 2012 in order today with more than 8000 signatory companies and over 12,000 participants in total to obtain more significant results. of 145 counties around the world. In Turkey, UNGC has been active since 2002 and has For any opinion and suggestions 291 members as of 2013. about the report, please contact [email protected]. The United Nations Global Compact asks the signatory companies embracing its 10 universal principles to reveal their existing practices within the scope of the said principles, their management approaches based on performance and their planning to the stakeholders and the large masses via progress reports at least once in a year. -

Strong Foundations Healthy Performance

STRONG FOUNDATIONS HEALTHY PERFORMANCE 2019 ANNUAL REPORT 2019 ANNUAL REPORT CONTENTS Anadolu Isuzu continues its Introduction 2 CORPORATE PROFILE operations in line with its growth 4 2019 FINANCIAL AND OPERATIONAL HIGHLIGHTS 6 HIGHLIGHTS IN 2019 strategy without interruption with 12 MESSAGE FROM THE CHAIRMAN OF THE BOARD OF DIRECTORS the market diversity its product 14 MESSAGE FROM THE PRESIDENT OF THE AUTOMOTIVE GROUP 16 MESSAGE FROM THE GENERAL MANAGER portfolio provides, its marketing 20 ANADOLU ISUZU FROM PAST TO PRESENT 22 SHAREHOLDERS OF ANADOLU ISUZU competencies and the support of 26 ANADOLU ISUZU’S PRODUCT PORTFOLIO its shareholders in the light of its 42 THE ECONOMY IN TURKEY AND THE WORLD 43 OVERVIEW OF THE SECTOR strengthening financial structure. In 2019 Tuğrul Arıkan 46 IN SUMMARY General Manager 47 EXPORT ACTIVITIES 53 MARKETING AND DEALER NETWORK DEVELOPMENT ACTIVITIES 55 AFTER-SALES SERVICES 56 SUPPLY CHAIN AT ANADOLU ISUZU 58 R&D AT ANADOLU ISUZU 62 PRODUCTION 64 ANADOLU ISUZU AND THE ENVIRONMENT 67 INDUSTRY 4.0 AND DIGITALIZATION PROJECTS 69 IM GLOBAL LEADER COMPANY 71 ENERGY PERFORMANCE OF ANADOLU ISUZU 72 HUMAN RESOURCES 78 OHS/EMPLOYEE SAFETY 79 SOCIAL AWARENESS PROJECTS AT ANADOLU ISUZU Corporate Governance 82 BOARD OF DIRECTORS 87 SENIOR MANAGEMENT 90 ORGANIZATION CHART 92 INDEPENDENT AUDIT REPORT 94 OTHER INFORMATION ABOUT ACTIVITIES 102 2019 AFFILIATE REPORT 103 CORPORATE GOVERNANCE Financial Information 125 CONSOLIDATED FINANCIAL STATEMENTS FOR THE PERIOD 31 DECEMBER 2019 AND INDEPENDENT AUDITOR’S REPORT FOR -

Sıra No Kod Banka Adı Kod Banka

Tablo: TCMB Ödeme Sistemleri Katılımcı Listesi (2020) Koda Göre Sıralama Alfabetik Sıralama SIRA NO KOD BANKA ADI KOD BANKA ADI 1 0001 T.C. MERKEZ BANKASI 0100 ADABANK A.Ş. 2 0004 İLLER BANKASI A.Ş. 0046 AKBANK T.A.Ş. 3 0010 T.C.ZİRAAT BANKASI A.Ş. 0143 AKTİF YATIRIM BANKASI A.Ş. 4 0012 T. HALK BANKASI A.Ş. 0203 ALBARAKA TÜRK KATILIM BANKASI A.Ş. 5 0014 T. SINAİ KALKINMA BANKASI A.Ş. 0124 ALTERNATİFBANK A.Ş. 6 0015 T. VAKIFLAR BANKASI T.A.O 0135 ANADOLUBANK A.Ş. 7 0016 T. EXİMBANK 0091 ARAP TÜRK BANKASI 8 0017 T. KALKINMA BANKASI A.Ş. 0149 BANK OF CHINA TURKEY A.Ş. 9 0029 BİRLEŞİK FON BANKASI A.Ş. 0142 BANKPOZİTİF KREDİ VE KALK.BANK.A.Ş. 10 0032 T. EKONOMİ BANKASI A.Ş. 0029 BİRLEŞİK FON BANKASI A.Ş. 11 0046 AKBANK T.A.Ş. 0125 BURGAN BANK A.Ş. 12 0059 ŞEKERBANK T.A.Ş. 0092 CITIBANK A.Ş. 13 0062 T. GARANTİ BANKASI A.Ş. 0134 DENİZBANK A.Ş. 14 0064 T. İŞ BANKASI A.Ş. 0115 DEUTSCHE BANK A.Ş. 15 0067 YAPI VE KREDİ BANKASI A.Ş. 0138 DİLER YATIRIM BANKASI A.Ş. 16 0091 ARAP TÜRK BANKASI 0103 FİBABANKA A.Ş. 17 0092 CITIBANK A.Ş. 0150 GOLDEN GLOBAL YATIRIM BANKASI A.Ş.(*) 18 0096 TURKISH BANK A.Ş. 0139 GSD YATIRIM BANKASI A.Ş. 19 0098 JPMORGAN CHASE BANK N.A. 0123 HSBC BANK A.Ş. 20 0099 ING BANK A.Ş. 0109 ICBC TURKEY BANK A.Ş. 21 0100 ADABANK A.Ş. -

Cee / Middle East / North Africa This Week

CEE / MIDDLE EAST / NORTH AFRICA THIS WEEK January 21, 2011 POLAND 2 CZECH REPUBLIC 12 HUNGARY 20 SLOVAKIA 25 TURKEY 31 BULGARIA 40 ROMANIA 45 CROATIA 49 SERBIA 54 BOSNIA & HERZEGOVINA 59 ALBANIA 64 MIDDLE EAST & N. AFRICA 67 Written by IntelliNews. The report is based on sources which we believe to be reliable, but no warranty, either express or implied, is provided in relation to the accuracy or completeness of the information. The views expressed are our best judgement as of the date of issue and are subject to change without notice. Opinions are not necessarily those of Internet Securities Inc., Euromoney Institutional Investor PLC or its affiliates. Internet Securities Inc. and Euromoney Institutional Investor PLC take no responsibility for decisions made on the basis of these opinions. Any redistribution of this information is strictly prohibited. Copyright © 1999-2011 Internet Securities, Inc., all rights reserved. A Euromoney Institutional Investor company. Copyright © 1998-2011 Sofia, all rights reserved. COPYING PROHIBITED. COPYRIGHT 1999-2011 INTERNET SECURITIES, INC., ALL RIGHTS RESERVED POLAND MACROECONOMIC REVIEW Eurostat: Poland's HICP inflation The Harmonised Index of Consumer Prices (HICP) in Poland amounted to 0.3% m/m in accelerates to 2.9% y/y in December December, 2010 and was 2.9% in annual terms vs. 2.6% y/y a month earlier, the EU's statistical office Eurostat has said. In line with Eurostat's estimations, the average HICP inflation for the whole 27 EU amounted to 2.6% y/y in December (vs. 2.3% in November). In the euro-zone, the inflation was 2.2% y/y vs. -

VERGİ NO UNVAN ADRES TELEFON FAKS (VAR / YOK) Altında Olanlar Için EVET / HAYIR) 1 0380753722 AKSU ELEKTRİKLİ EV ALETLERİ SANAYİ VE TİCARET A.Ş

1/79 ELEKTRİK VE ELEKTRONİK İHRACATÇILARI BİRLİĞİ NİSAN 2019 OLAĞAN GENEL KURULUNA KATILABİLECEKLERİN LİSTESİ İMALATÇI/TEDARİKÇİ BORÇ DURUMU (Doğrudan İhracatı Sınırın 0 VERGİ NO UNVAN ADRES TELEFON FAKS (VAR / YOK) Altında Olanlar için EVET / HAYIR) 1 0380753722 AKSU ELEKTRİKLİ EV ALETLERİ SANAYİ VE TİCARET A.Ş. AKÇABURGAZ MAH. 3036. SOK. NO.2/3 ESENYURT - İSTANBUL 02128866169 02128866919 YOK HAYIR İKİTELLİ ORGANİZE SANAYİ BÖLG. B.DALAN CD. DERSANKOOP SAN SİT S6C BL N:130 2 6080059840 LİDER REZİSTANS MAKİNA SAN VE TİCARET LİMİTED ŞİRKETİ +90(533)779 14 78 VAR HAYIR BAŞAKŞEHİR - İSTANBUL 3 0010381354 A DIŞ TİCARET LİMİTED ŞİRKETİ ÇIRPICI MAH.74/C SOK.NO:74/A ZEYTİNBURNU - İSTANBUL +90(212)416 81 23 +90(212)505 08 29 VAR HAYIR 4 0010803261 A ROYAL SOĞUTMA END.MUTFAK SAN.VE TİC.LTD.ŞTİ. KEÇECİ PİRİ MAH.HASBAHÇE SK.N.9 BEYOĞLU / İSTANBUL BEYOĞLU - İSTANBUL +90(212)361 32 86 YOK HAYIR 5 0010724648 AB POVER BALİSTİK GÜV. VE ENR. SİST. İNŞ. MAD. SAN. VE TİC. LTD. ŞTİ. TURGUT ÖZAL BULV. CUMHURİYET MAH. NO:51/2 BÜYÜKÇEKMECE - İSTANBUL +90(212)444 44 28 +90(212)394 36 58 VAR HAYIR 6 0010736571 ABA LED AYDINLATMA SAN.VE TİC.A.Ş. AKÇABURGAZ MAHALLESİ AKÇABURGAZ CADDESİ NO:43 ESENYURT - İSTANBUL +90(212)222 42 10 +90(212)222 42 11 YOK HAYIR 7 0010658532 ABAMET ÇEVRE TEKNOLOJİLERİ MÜHENDİSLİK MAKİNE İNŞAAT SAN.VE TİC.LTD.ŞTİ. ŞEMSETTİN GÜNALTAY CD.NO:89/11 KADIKÖY - İSTANBUL +90(216)373 33 30 +90(216)373 38 33 VAR HAYIR 8 0010047133 ABB ELEKTRIK SANAYİ ANONİM ŞİRKETİ ORGANIZE SANAYI BOLGESI 2.CAD NO.16 ÜMRANİYE - İSTANBUL +90(216)528 22 00 +90(216)466 53 85 YOK HAYIR 9 0010691250 ABB İHRACAT TİCARET VE ELEKTRİK SANAYİ ANONİM ŞİRKETİ ORGANİZE SANAYİ BÖLGESİ 2.CADDE NO:16 YUKARI DUDULLU ÜMRANİYE - İSTANBUL +90(216)528 22 00 +90(216)466 53 84 YOK HAYIR SARAY MAH. -

A Sectorial Analysis of Possible Information Leakages Prior to Merger and Acquisition Deals in Istanbul Stock Exchange

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Sönmezer, Sıtkı Article — Published Version A Sectorial Analysis of Possible Information leakages prior to Merger and Acquisition Deals in Istanbul Stock Exchange Journal of Economics and Political Economy Suggested Citation: Sönmezer, Sıtkı (2014) : A Sectorial Analysis of Possible Information leakages prior to Merger and Acquisition Deals in Istanbul Stock Exchange, Journal of Economics and Political Economy, ISSN 2148-8347, KSP Journals, Istanbul, Vol. 1, Iss. 2, pp. 186-194, http://dx.doi.org/10.1453/jepe.v1i2.63 , http://kspjournals.org/index.php/JEPE/article/view/63 This Version is available at: http://hdl.handle.net/10419/105848 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. -

Annual Report DBX ETF Trust

May 31, 2021 Annual Report DBX ETF Trust Xtrackers Eurozone Equity ETF (EURZ) Xtrackers International Real Estate ETF (HAUZ) Xtrackers Japan JPX-Nikkei 400 Equity ETF (JPN) DBX ETF Trust Table of Contents Page Shareholder Letter ....................................................................... 1 Management’s Discussion of Fund Performance ............................................. 3 Performance Summary Xtrackers Eurozone Equity ETF ......................................................... 4 Xtrackers International Real Estate ETF .................................................. 6 Xtrackers Japan JPX-Nikkei 400 Equity ETF .............................................. 8 Fees and Expenses ....................................................................... 10 Schedules of Investments Xtrackers Eurozone Equity ETF ......................................................... 11 Xtrackers International Real Estate ETF .................................................. 16 Xtrackers Japan JPX-Nikkei 400 Equity ETF .............................................. 25 Statements of Assets and Liabilities ........................................................ 30 Statements of Operations ................................................................. 31 Statements of Changes in Net Assets ....................................................... 32 Financial Highlights ...................................................................... 34 Notes to Financial Statements ............................................................. 36 Report -

Association of Automotive Manufacturers

OTOMOTİV SANAYİİ DERNEĞİ AUTOMOTIVE MANUFACTURERS ASSOCIATION AUTOMOTIVE MANUFACTURERS ASSOCIATION 2015 OSD “OICA” Üyesidir OSD is a Member of “OICA” 2 AUTOMOTIVE MANUFACTURERS ASSOCIATION (OSD) ESTABLISHMENT The Automotive Manufacturers Association (OSD) held its preliminary meeting on 11 January 1974. After quickly fulfilling the conditions set forth in Law of Associations No. 1630, it was established as the Association of the Manufacturers of Land Vehicles, Trucks, Pick-ups, Buses and P.Cars on 14 June 1974. The initial number of automotive manufacturers represented by the OSD was eleven. The number of OSD members reached fourteen by 2015. Changes made to the bylaws of the Association on 7 November 1979 resulted in its name being changed to the more convenient Automotive Manufacturers Association. The membership of the Automotive Manufacturers Association consists of top executives who are chosen by their own companies – three from each company. The Board of Directors of the association is chosen from among these members. The goals of the Automotive Manufacturers Association are as follows: 1. To aid in improving the manufacture of various motor vehicles made in Turkey, including p.cars, trucks, pick-ups, trailers,, buses, minibuses and tractors, and in developing the industry as a whole; 2. To contribute to the automotive industry and the economy of the country, and work towards making available within Turkey all parts and spare parts used in the automotive industry, as well as the tools and equipment necessary to make them; 3. To study common issues of the industry, including those related to marketing, to make recommendations to both public and private institutions involved in the sector and to follow them up; 4. -

Arcadius 8; (Column

index INDEX 319 Arcadius 8; (column of) 184 Balat 213–14 Archaeological Museum 93ff Baldwin, Count of Flanders 15 Argonauts, myth of 259, 263, 276 Balıklı Kilisesi 197–98 Major references, in cases where many are listed, are given in bold. Numbers in italics Armenian, Armenians 25, 189, 192, Balkapanı Han 132 are picture references. 193, 241–42, 258, 278; (Cemetery) Baltalimanı 258 268; (Patriarchate) 192 Balyan family of architects 34, 161, 193; Arnavutköy 255 (burial place of) 268 A Alexander, emperor 67 Arsenal (see Tersane) Balyan, Karabet 34, 247 Abdülaziz, sultan 23, 72, 215, 251; Alexander the Great 7; (sculptures of) 96 Ashkenazi Synagogue 228 Balyan, Kirkor 34, 234 (burial place of) 117 Alexander Sarcophagus 94, 95 Astronomer, office of 42 Balyan, Nikoğos 34, 246, 247, 249, Abdülhamit I, sultan 23, 118; (burial Alexius I, emperor 13, 282 At Meydanı (see Hippodrome) 252, 255, 274, 275 place of) 43 Alexius II, emperor 14 Atatürk 24, 42, 146, 237, 248; Balyan, Sarkis 34, 83, 247, 258, 272, Abdülhamit II, sultan 23, 251, 252, Alexius III, emperor 14 (Cultural Centre) 242; (Museum) 243; 267 278; (burial place of) 117 Alexius IV, emperor 15 (statue of) 103 Bank, Ottoman 227 Abdülmecit I, sultan 71, 93, 161, 164, Alexius V, emperor 15 Atik Ali Pasha 171; (mosque of) 119 Barbarossa, pirate and admiral 152, 247; (burial place of) 162 Ali Pasha of Çorlu, külliye of 119–20 Atik Mustafa Paşa Camii 216 250, 250; (burial place of) 250; Abdülmecit II, last caliph 24 Ali Sufi, calligrapher 157, 158 Atik Sinan, architect 130, 155, 212; (ensign