Exports: the Heart of Nep

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Journal of International Environmental Application & Science

Journal of International Environmental Application & Science ISSN-1307-0428 Editor in Chief: Prof. Dr. Sukru DURSUN, Environmental Engineering Department, Engineering & Natural Science Faculty, Konya Technical University, Konya, TURKEY EDITORIAL BOARD Prof. Dr. Lynne BODDY Prof. Dr. IR. Raf DEWIL Cardiff School of Biosciences, Main Building, Museum Chemical Eng. Dept, Chemical & Biochem. Process Techn. & Avenue, Cardiff CF10 3TL UK Control Section, Katholieke Un. Leuven, Heverlee, BELGIUM Prof. Dr. Phil INESON Prof. Dr. Tay Joo HWA Stockholm Environment Institute, University of York, Environ. & Water Resources Engineering Division, of Civil & Heslington, York, YO10 5DD, UK Environ. Eng. School, Nanyang Techno. Un., SINGAPORE Prof. Dr. Lidia CRISTEA Dr. Somjai KARNCHANAWONG Romanian Sci. & Arts University, B-dul Energeticienilor, No.9- Environ. Engineering Dept, Faculty of Engineering Chiang Mai 11, Sec. 3, ZC 030796, Bucharest, ROMANIA University, THAILAND Prof. Dr. N. MODIRSHAHLA, Prof. Dr Hab. Boguslaw BUSZEWSK Department of Applied Chemistry, Islamic Azad University, Chemistry & Bioanalytics Environ., Chemistry Faculty, Tabriz Branch, IRAN Nicolaus Copernicus University, Torun, POLAND Prof. Dr. Victor A.DRYBAN, Prof. Dr. Azita Ahmadi-SÉNICHAULT Rock Pressure National Academy of Sciences of Ukraine, Arts et Métiers Paris Tech - Centre de Bordeaux, Esplanade Donetsk, UKRAINE des Arts et Metiers, FRANCE Prof.Dr. Rüdiger ANLAUF Osnabrueck University of Applied Sciences, Osnabrück, Prof. Dr. Irena BARANOWSKA GERMANY Analytical Chemistry Dept., Silesian Technical University, Gliwice, POLAND Prof. Dr. Amjad SHRAIM Chemistry & Earth Sciences Department, College of Arts & Prof. Dr. Indumathi M NAMBI Sciences, Qatar University, Doha, QATAR Indian Institute of Technology Madras, Civil Eng. Dept., Environ. & Water Resources Eng. Div., INDIA Prof. Dr. Massimo ZUCCHETTI Dipartimento di Energetica, Politecnico di Torino, Corso Duca Prof. -

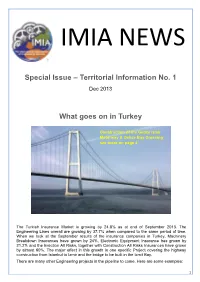

Special Issue – Territorial Information No. 1 What Goes on in Turkey

IMIA NEWS Special Issue – Territorial Information No. 1 Dec 2013 What goes on in Turkey Construction of the Gebze Izmir Motorway & Gebze Bay Crossing see more on page 4 More info p.2 The Turkish Insurance Market is growing by 24.8% as at end of September 2013. The Engineering Lines overall are growing by 37.7% when compared to the same period of time. When we look at the September results of the insurance companies in Turkey, Machinery Breakdown Insurances have grown by 24%, Electronic Equipment Insurance has grown by 21.2% and the Erection All Risks, together with Construction All Risks Insurances have grown by almost 60%. The major effect in this growth is one specific Project covering the highway construction from Istanbul to Izmir and the bridge to be built in the Izmit Bay. There are many other Engineering projects in the pipeline to come. Here are some examples: 1 THE THIRD BOSPHORUS BRIDGE Bridge of Firsts The 3rd Bridge, which is going to be built on the Bosphorus, Istanbul within the Northern Marmara Motorway Project executed by IC Ictas – Astaldi Consortium, is considered the future of transportation and commerce. The 3rd bridge, which is going to be built on the Bosphorus, Istanbul after the Bogazici Bridge, which started operating in 1972, and the Fatih Sultan Mehmet Bridge, which was completed in 1988, is regarded as the bridge of firsts. 8 lanes of motorway and 2 lanes of railway will be located at the same level on the 3rd Bosphorus Bridge, which will be a product of professional engineering and advanced technology built by a team, most of whom are Turkish engineers. -

A. FALCONE, V. IACOMI – Archeologia Dell'acqua a Elaiussa

BOLLETTINO DI ARCHEOLOGIA ON LINE DIREZIONE GENERALE ARCHEOLOGIA, BELLE ARTI E PAESAGGIO XI, 2018/1 ANNALISA FALCONE*, VERONICA IACOMI* ARCHEOLOGIA DELL’ACQUA AD ELAIUSSA SEBASTE, CILICIA (TURCHIA): UN CONTESTO DI SCAVO DI ETA’ PROTOBIZANTINA NEL QUARTIERE RESIDENZIALE PRESSO IL PORTO SUD Elaiussa Sebaste (modern Ayaş, Akdeniz Bölgesı, southern Turkey) has been investigated since 1995 by the Italian Archaeological Mission of “Sapienza” University of Rome. Excavations brought to light large sectors of the Roman– Byzantine public area (theatre, agora, baths), necropoleis, two city harbours, the so called “Byzantine palace” and part of the domestic and handcraft quarters. The site was, during the Roman age, one of the most important cities of Cilicia Aspera and maintained its prestigious role as a significant trading port until the late empire and the early Byzantine age, when it became one of the most active centres of LR1 amphoras production. This contri- bution will focus on the “Cura Aquarum Project”, started in 2009 and aimed at identifying, positioning and doc- umenting all the structures related with the water supply of the site. Recognition works were carried out identifying large sections of the aqueduct’s truck, the connected water tanks and numerous cisterns disseminated across the city. Together with the surveys, the complete excavation of one of the cisterns entirely cut in the rock found in the domestic early-Byzantine quarter – luckily sealed just after the site abandonment – contributed to clarify the im- portance of the rainwater harvesting system, even after the aqueduct’s construction, providing a significant portrayal of the latest phase of Elaiussa’s occupation. -

Shankar Ias Academy Test 18 - Geography - Full Test - Answer Key

SHANKAR IAS ACADEMY TEST 18 - GEOGRAPHY - FULL TEST - ANSWER KEY 1. Ans (a) Explanation: Soil found in Tropical deciduous forest rich in nutrients. 2. Ans (b) Explanation: Sea breeze is caused due to the heating of land and it occurs in the day time 3. Ans (c) Explanation: • Days are hot, and during the hot season, noon temperatures of over 100°F. are quite frequent. When night falls the clear sky which promotes intense heating during the day also causes rapid radiation in the night. Temperatures drop to well below 50°F. and night frosts are not uncommon at this time of the year. This extreme diurnal range of temperature is another characteristic feature of the Sudan type of climate. • The savanna, particularly in Africa, is the home of wild animals. It is known as the ‘big game country. • The leaf and grass-eating animals include the zebra, antelope, giraffe, deer, gazelle, elephant and okapi. • Many are well camouflaged species and their presence amongst the tall greenish-brown grass cannot be easily detected. The giraffe with such a long neck can locate its enemies a great distance away, while the elephant is so huge and strong that few animals will venture to come near it. It is well equipped will tusks and trunk for defence. • The carnivorous animals like the lion, tiger, leopard, hyaena, panther, jaguar, jackal, lynx and puma have powerful jaws and teeth for attacking other animals. 4. Ans (b) Explanation: Rivers of Tamilnadu • The Thamirabarani River (Porunai) is a perennial river that originates from the famous Agastyarkoodam peak of Pothigai hills of the Western Ghats, above Papanasam in the Ambasamudram taluk. -

Global Turkey in Europe. Political, Economic, and Foreign Policy

ISSN 2239-2122 9 IAI Research Papers The EU is changing, Turkey too, and - above all - there is systemic change and crisis all G round, ranging from economics, the spread of democratic norms and foreign policy. LOBAL The IAI Research Papers are brief monographs written by one or N.1 European Security and the Future of Transatlantic Relations, This research paper explores how the EU and Turkey can enhance their cooperation in more authors (IAI or external experts) on current problems of inter- T edited by Riccardo Alcaro and Erik Jones, 2011 URKEY GLOBAL TURKEY national politics and international relations. The aim is to promote the political, economic, and foreign policy domains and how they can find a way out of the stalemate EU-Turkey relations have reached with the lack of progress in accession greater and more up to date knowledge of emerging issues and N. 2 Democracy in the EU after the Lisbon Treaty, IN trends and help prompt public debate. edited by Raaello Matarazzo, 2011 negotiations and the increasing uncertainty over both the future of the European project E after the Eurozone crisis and Turkey’s role in it. UROPE IN EUROPE N. 3 The Challenges of State Sustainability in the Mediterranean, edited by Silvia Colombo and Nathalie Tocci, 2011 A non-profit organization, IAI was founded in 1965 by Altiero Spinel- li, its first director. N. 4 Re-thinking Western Policies in Light of the Arab Uprisings, SENEM AYDIN-DÜZGIT is Assistant Professor at the Istanbul Bilgi University and Senior POLITICAL, ECONOMIC, AND FOREIGN POLICY edited by Riccardo Alcaro and Miguel Haubrich-Seco, 2012 Research Affiliate of the Istanbul Policy Centre (IPC). -

I, No:40 Sayılı Tebliği'nin 8'Nci Maddesi Gereğince, Hisse Senetleri

Sermaye Piyasas Kurulu’nun Seri :I, No:40 say l Teblii’nin 8’nci maddesi gereince, hisse senetleri Borsada i"lem gören ortakl klar n Kurul kayd nda olan ancak Borsada i"lem görmeyen statüde hisse senetlerinin Borsada sat "a konu edilebilmesi amac yla Merkezi Kay t Kurulu"u’na yap lan ba"vurulara ait bilgiler a"a da yer almaktad r. Hisse Kodu S ra Sat "a Konu Hisse Ünvan Grubu Yat r mc n n Ad -Soyad Nominal Tutar Tsp Sat " No Ünvan (TL)* 5"lemi K s t ** ** ADANA 1 ADANA Ç5MENTO E TANER BUGAY SANAY55 A.;. A GRUBU 2.235,720 ALTIN 2 ALTINYILDIZ MENSUCAT E 5SMA5L AYÇ5N VE KONFEKS5YON 0,066 FABR5KALARI A.;. ARCLK 3 ARÇEL5K A.;. E C5HAT YÜKSEKEL 31,344 ARCLK 4 ARÇEL5K A.;. E ERSAN OYMAN 19,736 ARCLK 5 ARÇEL5K A.;. E FER5DE SEZ5K 0,214 ARCLK 6 ARÇEL5K A.;. E F5L5Z EYÜPOHLU 209,141 ARCLK 7 ARÇEL5K A.;. E HANDE YED5DAL 28,180 ARCLK 8 ARÇEL5K A.;. E HAYRETT5N YAVUZ 0,206 ARCLK 9 ARÇEL5K A.;. E 5HSAN ERSEN 1.259,571 ARCLK 10 ARÇEL5K A.;. E 5RFAN ATALAY 195,262 ARCLK 11 ARÇEL5K A.;. E KEZ5BAN ONBE; 984,120 ARCLK 12 ARÇEL5K A.;. E RAFET SALTIK 23,514 ARCLK 13 ARÇEL5K A.;. E SELEN TUNÇKAYA 29,110 ARCLK 14 ARÇEL5K A.;. E YA;AR EMEK 1,142 ARCLK 15 ARÇEL5K A.;. E ZEYNEP ÖZDE GÖRKEY 2,351 ARCLK 16 ARÇEL5K A.;. E ZEYNEP SEDEF ELDEM 2.090,880 ASELS 17 ASELSAN ELEKTRON5K E ALAETT5N ÖZKÜLAHLI SANAY5 VE T5CARET A.;. -

The Green Movement in Turkey

#4.13 PERSPECTIVES Political analysis and commentary from Turkey FEATURE ARTICLES THE GREEN MOVEMENT IN TURKEY DEMOCRACY INTERNATIONAL POLITICS HUMAN LANDSCAPE AKP versus women Turkish-American relations and the Taner Öngür: Gülfer Akkaya Middle East in Obama’s second term The long and winding road Page 52 0Nar $OST .IyeGO 3erkaN 3eyMeN Page 60 Page 66 TURKEY REPRESENTATION Content Editor’s note 3 Q Feature articles: The Green Movement in Turkey Sustainability of the Green Movement in Turkey, Bülent Duru 4 Environmentalists in Turkey - Who are they?, BArë GenCer BAykAn 8 The involvement of the green movement in the political space, Hande Paker 12 Ecofeminism: Practical and theoretical possibilities, %Cehan Balta 16 Milestones in the Õght for the environment, Ahmet Oktay Demiran 20 Do EIA reports really assess environmental impact?, GonCa 9lmaZ 25 Hydroelectric power plants: A great disaster, a great malice, 3emahat 3evim ZGür GürBüZ 28 Latest notes on history from Bergama, Zer Akdemir 34 A radioactive landÕll in the heart of ÊXmir, 3erkan OCak 38 Q Culture Turkish television series: an overview, &eyZa Aknerdem 41 Q Ecology Seasonal farm workers: Pitiful victims or Kurdish laborers? (II), DeniZ DuruiZ 44 Q Democracy Peace process and gender equality, Ulrike Dufner 50 AKP versus women, Gülfer Akkaya 52 New metropolitan municipalities, &ikret TokSÇZ 56 Q International politics Turkish-American relations and the Middle East in Obama’s second term, Pnar DoSt .iyeGo 60 Q Human landscape Taner Öngür: The long and winding road, Serkan Seymen -

Genealogy of the Concept of Securitization and Minority Rights

THE KURD INDUSTRY: UNDERSTANDING COSMOPOLITANISM IN THE TWENTY-FIRST CENTURY by ELÇIN HASKOLLAR A Dissertation submitted to the Graduate School – Newark Rutgers, The State University of New Jersey in partial fulfillment of the requirements for the degree of Doctor of Philosophy Graduate Program in Global Affairs written under the direction of Dr. Stephen Eric Bronner and approved by ________________________________ ________________________________ ________________________________ ________________________________ Newark, New Jersey October 2014 © 2014 Elçin Haskollar ALL RIGHTS RESERVED ABSTRACT OF THE DISSERTATION The Kurd Industry: Understanding Cosmopolitanism in the Twenty-First Century By ELÇIN HASKOLLAR Dissertation Director: Dr. Stephen Eric Bronner This dissertation is largely concerned with the tension between human rights principles and political realism. It examines the relationship between ethics, politics and power by discussing how Kurdish issues have been shaped by the political landscape of the twenty- first century. It opens up a dialogue on the contested meaning and shape of human rights, and enables a new avenue to think about foreign policy, ethically and politically. It bridges political theory with practice and reveals policy implications for the Middle East as a region. Using the approach of a qualitative, exploratory multiple-case study based on discourse analysis, several Kurdish issues are examined within the context of democratization, minority rights and the politics of exclusion. Data was collected through semi-structured interviews, archival research and participant observation. Data analysis was carried out based on the theoretical framework of critical theory and discourse analysis. Further, a discourse-interpretive paradigm underpins this research based on open coding. Such a method allows this study to combine individual narratives within their particular socio-political, economic and historical setting. -

A Study of the Political, Economical and Cultural

SIT Graduate Institute/SIT Study Abroad SIT Digital Collections Independent Study Project (ISP) Collection SIT Study Abroad Fall 2004 The Return of the Sick Man of Europe: A study of the political, economical and cultural grounds for/ against the entrance of Turkey to the European Union as viewed by Turkish Immigrants and Germans living in Berlin Ursula A. Arno SIT Study Abroad Follow this and additional works at: https://digitalcollections.sit.edu/isp_collection Part of the Political Science Commons Recommended Citation Arno, Ursula A., "The Return of the Sick Man of Europe: A study of the political, economical and cultural grounds for/against the entrance of Turkey to the European Union as viewed by Turkish Immigrants and Germans living in Berlin" (2004). Independent Study Project (ISP) Collection. 514. https://digitalcollections.sit.edu/isp_collection/514 This Unpublished Paper is brought to you for free and open access by the SIT Study Abroad at SIT Digital Collections. It has been accepted for inclusion in Independent Study Project (ISP) Collection by an authorized administrator of SIT Digital Collections. For more information, please contact [email protected]. The Return of the Sick Man of Europe: A study of the political, economical and cultural grounds for/against the entrance of Turkey to the European Union as viewed by Turkish Immigrants and Germans living in Berlin Ursula A. Arno 10 December 2004 School for International Training Advisor: Dr. Helga Ernst Central Europe 2004: Culture, Ethnicity and Nationalism Arno 2 Table of Contents I. Introduction a. Background of European Union (EU) b. Enlargement Policy of the EU c. -

Premailer Middle East 2021

Bonds, Loans Shangri-La Bosphorus, Istanbul & Sukuk Turkey 2021 Turkey’s largest capital markets event www.bondsloansturkey.com 93% 50+ 20% 250+ DIRECTOR LEVEL OR ABOVE REGIONAL & INTERNATIONAL SOVEREIGN, CORPORATE & INDUSTRY EXPERT SPEAKERS BANKS ATTENDED FI BORROWERS Bonds, Loans & Sukuk Turkey has become the meeting point of all important players in finance through the correct mix of its participants, and its reliability with continuity of successful organisations in the last consecutive years Selahattin BİLGEN, IGA Airport PLATINUM SPONSOR GOLD SPONSOR BRONZE SPONSORS WELCOME TO THE ANNUAL MEETING PLACE FOR TURKEY’S FINANCE PROFESSIONALS Bonds, Loans & Sukuk Turkey is the country’s largest capital markets event. It is the only event to combine discussions across the Bond, Loans and Sukuk markets, making it a “must attend” event for the country’s leading CEOs, CFOs and Treasurers. With over 65% of the audience representing issuers and borrowers and over 93% being director level or above, it is the place where live deals are discussed and mandates are won each year. As a speaker, I had a dynamic discussion which was a great experience. Overall, the organisation was great and attracted an invaluable list of attendees. Orhan Kaya, ICBC Turkey SAVE YOURSELF SHOWCASE YOUR INCREASE TIME AND MONEY EXPERTISE IN THE REGION AWARENESS get the attendee list 2 weeks by presenting a case study by taking an exhibition space before the event so you can to a room full of potential and demonstrating your pre-arrange meetings. clients. products and services. WIN MORE INCREASE YOUR BUSINESS BRANDS PRESENCE packages include a number through the numerous of staff passes so you can branding opportunities cover more clients. -

Public-Private Partnership Experience in the International Arena: Case of Turkey

Public-Private Partnership Experience in the International Arena: Case of Turkey Asli Pelin Gurgun, Ph.D.1; and Ali Touran, Ph.D., P.E., F.ASCE2 Abstract: Public-private partnership (PPP) models are frequently used in construction projects worldwide. The experiences of developed and developing countries vary depending on existing legal, economical, social, and political environments. Although there are some common challenges, risks, limitations, and success factors, practicing PPP framework is also dependent on country-specific factors. In this paper, first the state of the art in frequent PPP practicing regions/countries such as Europe, the U.K., and China are summarized; and a review of PPP experience in the U.S. is presented. Then, Turkey, where different PPP models have been used for nearly three decades, is analyzed in more depth as an example for developing countries. A new PPP law has been drafted to expand the legal context and types of models and overcome the existing limitations since the first introduction of PPP projects in Turkey in early 1980s. An intensive PPP literature survey has been made to present the common success factors, risks, limitations, and challenges in Europe, the U.K., China, U.S., and Turkey as well as under- standing the differences in the implementations. A viable economic environment, proper contractual arrangements for appropriate risk allocation, well-established legal basis, public support, transparency, and a central unit to standardize the procedures are determined to be major factors for successful PPP projects. DOI: 10.1061/(ASCE)ME.1943-5479.0000213. © 2014 American Society of Civil Engineers. Author keywords: Public-Private Partnerships (PPP); Turkey; Developing countries; Project delivery; Risk. -

Template Report

REPUBLIC OF TURKEY PRIME MINISTRY Investment Support and Promotion Agency of Turkey TRANSPORTATION & LOGISTICS INDUSTRY REPORT DECEMBERJANUARY 2010 2009 CONTENTS 1. Executive Summary 3 2. Sector Overview 4 2.1 Global Sector 4 2.2 Domestic Sector 5 2.2.1 Overview 5 2.2.2 Road Transport 7 2.2.3 Railway Transport 8 2.2.4 Air Transport 10 2.2.5 Maritime Transport 12 2.2.6 RoRo Transport 13 2.2.7 International Trade 13 2.3 Main Players 14 2.4 Sector Outlook and Trends 15 2.5 SWOT Analysis 16 2.6 Investment Opportunities 17 2.7 Sector Establishments and Institutions 19 LIST OF FIGURES 20 ABBREVIATIONS 21 2 1. Executive Summary The transportation and logistics sector, broadly defined to include airlines and airfreight, shipping, road and rail transport and the associated infrastructure and services, generated US$ 3.4 trillion of revenue globally in 2007. It has grown with a CAGR of 6.2% between 2003 and 2007. By 2012, the global transportation industry is forecast to reach US$ 4.5 trillion growing with a CAGR of 5.4%.1 The share of the logistics sector (broadly defined to include all transport as above) in Turkey’s GDP is estimated between 8-12%.2 Thus the size of the sector can be estimated as being around US$ 65-95 billion in 2008. The size of Turkish transportation & logistics industry is determined as US$ 59 billion, while the share of the logistics service supplier market is estimated as US$ 22 billion in “Turkey Logistics Industry Survey 2008”.