Annual Report 2019 OVERVIEW

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Full Year Statutory Accounts

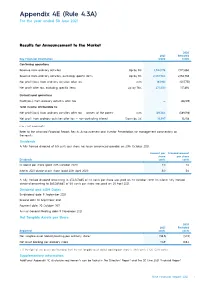

Appendix 4E (Rule 4.3A) For the year ended 30 June 2021 Results for Announcement to the Market 2020 2021 Restated Key Financial Information $’000 $’000 Continuing operations Revenue from ordinary activities Up by 8% 2,342,178 2,172,060 Revenue from ordinary activities, excluding specific items Up by 8% 2,332,984 2,156,785 Net profit/(loss) from ordinary activities after tax n/m 183,961 (507,751) Net profit after tax, excluding specific items Up by 76% 277,530 157,694 Discontinued operations Profit/(loss) from ordinary activities after tax — (66,189) Total income attributable to: Net profit/(loss) from ordinary activities after tax — owners of the parent n/m 169,364 (589,198) Net profit from ordinary activities after tax — non-controlling interest Down by 4% 14,597 15,258 n/m = not meaningful Refer to the attached Financial Report, Results Announcement and Investor Presentation for management commentary on the results. Dividends A fully franked dividend of 5.5 cents per share has been announced payable on 20th October 2021. Amount per Franked amount share per share Dividends cents cents Dividend per share (paid 20th October 2020) 2.0 2.0 Interim 2021 dividend per share (paid 20th April 2021) 5.0 5.0 A fully franked dividend amounting to $34,107,865 of 2.0 cents per share was paid on 20 October 2020. An interim fully franked dividend amounting to $85,269,663 of 5.0 cents per share was paid on 20 April 2021. Dividend and AGM Dates Ex-dividend date: 9 September 2021 Record date: 10 September 2021 Payment date: 20 October 2021 Annual General Meeting date: 11 November 2021 Net Tangible Assets per Share 2020 2021 Restated Reported cents cents Net tangible asset (deficit)/backing per ordinary share 1 (38.3) (40.9) Net asset backing per ordinary share 114.9 108.4 1. -

Presentation to Macquarie Conference

4 May 2021 ASX Markets Announcements Office ASX Limited 20 Bridge Street Sydney NSW 2000 PRESENTATION TO MACQUARIE CONFERENCE 4 May 2021: Attached is a copy of Nine’s presentation to the Macquarie Australia Conference 2021. Authorised for lodgment by Mike Sneesby, Chief Executive Officer. Further information: Nola Hodgson Victoria Buchan Head of Investor Relations Director of Communications +61 2 9965 2306 +61 2 9965 2296 [email protected] [email protected] nineforbrands.com.au Nine Sydney - 1 Denison Street, North Sydney, NSW, 2060 ABN 60 122 203 892 MIKE SNEESBY | CHIEF EXECUTIVE OFFICER Important Notice and Disclaimer as a result of reliance on this document. as a general guide only, and should not be relied on This document is a presentation of general as an indication or guarantee of future performance. background information about the activities of Nine Forward Looking Statements Forward looking statements involve known and unknown risks, uncertainty and other factors which Entertainment Co. Holdings Limited (“NEC”) current This document contains certain forward looking can cause NEC’s actual results to differ materially at the date of the presentation, (4 May 2021). The statements and comments about future events, from the plans, objectives, expectations, estimates information contained in this presentation is of including NEC’s expectations about the performance and intentions expressed in such forward looking general background and does not purport to be of its businesses. Forward looking statements can statements and many of these factors are outside complete. It is not intended to be relied upon as generally be identified by the use of forward looking the control of NEC. -

Agpasa, Brendon

29 January 2021 The Hon Paul Fletcher MP PO Box 6022 House of Representatives Parliament House Canberra ACT 2600 CHRIS (BRENDON) AGPASA SUBMISSION TO THE 2021-22 PRE-BUDGET SUBMISSIONS Dear Minister Fletcher, I write to request assistance had appropriate for media diversity to support digital radio and TV rollouts will continue in the federal funding, Brendon Agpasa was a student, radio listener and TV viewer. Paul Fletcher MP and the Morrison Government is supporting the media diversity including digital radio rollout, transition of community television to an online operating model, digital TV rollout, radio and TV services through regional media and subscription TV rollout we’re rolled out for new media landscape and it’s yours to towards a digital future of radio and TV broadcasting. We looking up for an expansion of digital radio rollout has been given consideration, the new digital spectrum to test a trial DRM30 and DRM+ with existing analogue (AM/FM) radio services, shortwave radio and end of spectrum (VHF NAS licences) will be adopted Digital Radio Mondiale services in Australia for the future plans. The radio stations Sydney’s 2GB, Melbourne’s 3AW, Brisbane’s Nova 106.9, Adelaide’s Mix 102.3, Perth’s Nova 93.7, Hit FM and Triple M ranks number 1 at ratings survey 8 in December 2020. Recently in December 2020, Nova Entertainment had launched it’s new DAB+ stations in each market, such as Nova Throwbacks, Nova 90s, Nova Noughties, Nova 10s, Smooth 80s and Smooth 90s to bring you the freshest hits, throwbacks and old classics all day everyday at Nova and Smooth FM. -

Sydney Program Guide

Page 1 of 42 Sydney Program Guide Sun Mar 14, 2021 06:00 EASY EATS Captioned HD WS G Nutritious & Delicious In this episode of Easy Eats, everything is gorgeous and guilt-free. Dishes like Lamb Stir Fry, Vegie Strudel, and Sweet Corn Soup are low in fat but high in flavour. There's even a low fat version of Hummingbird Cake which is perfect for those watching their waistline. 07:00 WEEKEND TODAY Captioned Live HD WS NA Join the Weekend Today team as they bring you the latest in news, current affairs, sports, politics, entertainment, fashion, health and lifestyle. 10:00 SPORTS SUNDAY Captioned Live HD WS PG Featuring Australia's leading sports personalities, Sports Sunday presents a frank and open debate about all the issues in the week of sport, with the promise of heated opinion and a few laughs along the way. 11:00 SUNDAY FOOTY SHOW Captioned Live HD WS PG Join hosts Peter Sterling, Erin Molan and Brad Fittler, with regular special guests to discuss all things NRL. 13:00 WOMEN'S FOOTY Captioned HD WS PG Join Bianca Chatfield for the 5th Season of Women's Footy for the latest news, opinion and analysis from in and around the AFLW - Each week, a raft of the AFLW's biggest names will join the show to discuss the weekend's action. 14:00 DAVID ATTENBOROUGH'S DYNASTIES Captioned Repeat HD WS PG The Making of Dynasties Follow five of the world's most celebrated, yet endangered animals: penguins, chimpanzees, lions, painted wolves and tigers, as they fight for their own survival and for the future of their dynasties. -

Deluxe Package

NSW DELUXE PACKAGE Unprecedented exposure for your premier property NSW DELUXE PACKAGE NSW DELUXE PACKAGE For the first time, Domain offers sellers this ultimate package – The cover of Domain in The Sydney Morning Herald and The Australian Financial Review, domain.com.au editorial exposure, a prime spot on the smh.com.au, domain.com.au, nine.com.au (NSW) 9news.com.au (NSW) homepages, plus extensive amplification through Domain’s leading social media platforms for your premier property. NSW DELUXE PACKAGE ELEMENTS Editorial • The cover of Domain in Saturday’s The SMH and Friday’s The AFR, plus cover story • Domain digital editorial article Magazine Advertising • Domain in The SMH and The AFR full page advertisement x 2 weeks • Domain Prestige in The AFR full page advertisement x 3 weeks Digital and Social Amplification • Domain Dream Homes on domain.com.au. smh.com.au, nine.com.au (NSW) and 9news.com.au (NSW) homepages • Listing showcased via Domain Facebook, Instagram and Twitter • Facebook Instant Experience INVESTMENT: $35,200 GST inclusive Cancellation of any portion of the NSW Deluxe Package that occurs after the first insertion / appearance date of any of the products outlined in the booking agreement will be billed at the total cost of the package. NSW Deluxe Packages are subject to availability. Editorial inclusion is subject to Editor approval. Online and magazine advertising terms and conditions: domain.com.au/group/agent-centre. Rates are for single resale properties only at the discretion of Domain and are not available for multiple dwelling buildings, projects or developments. Prices are subject to change without notice. -

Acmasphere Issue 62

acma investigations Broadcasting investigations, October to December 2010 � This summary is of ACMA broadcasting investigations completed in the three months from 1 October to 31 December 2010. There is also, with the cooperation of Free TV Australia and Commercial Radio Australia (CRA), a three-month report of the number and substance of complaints made directly to the commercial broadcasters. The broadcasting Complaints about possible breaches Most investigation reports (with the complaints process of program standards (children’s exception of community non-breach Primary responsibility for the resolution television, Australian content, captioning investigation reports) are published of broadcasting code-related and disclosure), provisions of the BSA on the ACMA website at complaints rests with the licensees. and licence conditions may be made www.acma.gov.au (go to About The Broadcasting Services Act 1992 directly to the ACMA. Complainants ACMA: Publications & research > (the BSA) lays down a general procedure are not obliged to contact a licensee Publications > Broadcasting publications for complaints-handling whereby a first in these instances. > Broadcasting investigations reports). complainant is required to approach a licensee first, who in turn is obliged The ACMA may find that a licensee to respond. has breached a broadcasting code of practice or a licensee may admit However, if a complainant does not to a breach of a code. Breaches of receive a response within 60 days, the codes are not breaches of the or considers the response received BSA, although the ACMA may make to be inadequate, the matter may then compliance with a code a condition be referred to the ACMA for investigation. -

AFG-Autumn19-Final.Pdf

TriedTried and trusted Manage harvest timing Increase fruit size Increase fruit firmness Improve storage ability Simple to apply Reduced pre harvest fruit drop wwww.sumitomo-chem.com.au.sumitomo-che.sumitomo-chem.com.au Scan here to see more information ReTTain®ain® is a registereedd trademarks of Valent BioSciences LLC, aboutbout ReTTainain a Delaware limited liability company. CONTENTS Australian Fruitgrower Publisher From the CEO . .4 Apple and Pear Australia Limited (APAL) is National netting program . .5 a not-for-profit organisation that supports and provides services to Australia’s commercial Pre-conditioning pears . .7 apple and pear growers. 08 Suite G01, 128 Jolimont Road, East Melbourne VIC 3002 LABOUR t: (03) 9329 3511 f: (03) 9329 3522 Fair treatment just smart business . .8 w: www.apal.org.au MARKETING Managing Editor Alison Barber Marketing to millennials . .14 e: [email protected] Positive trends for apple and pear sales . .16 State Roundup . 18 Technical Editor Angus Crawford BUSINESS e: [email protected] Capitalising on retail competition . .21 Advertising Packaging in a war on waste world . .25 The publisher accepts no responsibility for the contents of advertisements. All advertisements are Juice adds value at Huon Valley . .28 accepted in good faith and the liability of advertising content is the responsibility of the advertiser. Procurement for beginners . .30 Gypsy Media Introducing Future Business . .32 m: 0419 107 143 | e: [email protected] BRAND NEWS Graphic Design 28 ® Vale Graphics Red Moon licensed for Australia . .33 e: [email protected] FRUIT MATURITY Copyright Harvest timing key to quality . .34 All material in Australian Fruitgrower is copyright. -

Fairfax Media Ltd (Fxj) 16 August 2017

FAIRFAX MEDIA LTD (FXJ) 16 AUGUST 2017 RESULTS Full Year 2017 Full Year 2016 CHANGE Revenue ($m) 1,742.7 1830.5 -4.8% Bloomberg consensus ($m) 1,725.0 Domain EBITDA ($m) 113.1 120.0 -5.7% EBITDA ($m) 271.1 283.3 -4.3% Bloomberg consensus ($m) 263.8 Net profit (loss) after tax ($m) 83.9 (772.6) n/a Final Dividend ($) 0.02 0.02 no change Fairfax (FXJ) plans to spin-off Domain and trading to start in November Media group, Fairfax (FXJ) has returned to profitability, posting an improved $83.9m full year profit for the 12 months to June 30 and provided details on its planned Domain IPO. While underlying earnings (not including significant items) went backwards over the year, EBITDA came in ahead of market expectations. The result follows more than $900m in write-downs of its publishing assets which held back its FY16 result. While Domain has been its star performer for some time, its print business has been coming under pressure due to a slide in advertising dollars and a systemic change in the way Australians consume their news. FXJ confirmed it plans to spin-off its best performing asset, Domain and for trading in the real estate classifieds business to begin in mid to late November. The group intends to retain 60% of Domain with the remaining 40% to be distributed to FXJ shareholders. The split is still conditional on shareholder and regulatory approvals (including ASIC, ASX and ATO). Investors can expect the scheme booklet (which outlines all details of the separation) in late September 2017. -

Maine Alumnus, Volume 57, Number 2, Winter 1976

The University of Maine DigitalCommons@UMaine University of Maine Alumni Magazines University of Maine Publications Winter 1976 Maine Alumnus, Volume 57, Number 2, Winter 1976 General Alumni Association, University of Maine Follow this and additional works at: https://digitalcommons.library.umaine.edu/alumni_magazines Part of the Higher Education Commons, and the History Commons Recommended Citation General Alumni Association, University of Maine, "Maine Alumnus, Volume 57, Number 2, Winter 1976" (1976). University of Maine Alumni Magazines. 308. https://digitalcommons.library.umaine.edu/alumni_magazines/308 This publication is brought to you for free and open access by DigitalCommons@UMaine. It has been accepted for inclusion in University of Maine Alumni Magazines by an authorized administrator of DigitalCommons@UMaine. For more information, please contact [email protected]. V A / Winter is here ... time to enjoy a Bar Harbor Airlines Winters' Holiday in needn’t be City Winter Holiday. There’s ’’^Wrtiuch to do. fantastic Quebec City. ’* „ m F restaurants. History and atmosphere * * Ski at fabulous Mont Ste. Anne, with its mile-plus trails and Eastern oozing throughout the Canada’s only gondola. Novice skiers can start right from the top of this Send for our Quebec City Winter Brochure beautiful mountain on the shores of the St. Lawrence River. Expert skiers Bar Harbor Airlines Winter Brochure are welcome to try the famed World Cup trail. It truly is a mountain for all Bangor International Airport skiers. Nearby Lac Beauport offers family skiing night and day just fifteen Bangor, Maine 04401 minutes from Quebec City. bm/m/wh? Daily Service Connecting BOSTON—PORTLAND—AUGUSTA—BANGOR—BAR HARBOR—PRESQUE ISLE-QUEBEC CITY Volume 57 Number 2 Winter 1976 publisher The Maine Alumnus Lester J. -

1 Transcript of 2019 Nine Entertainment AGM Sydney

1 Transcript of 2019 Nine Entertainment AGM Sydney, November 12, 2019 Chairman Peter Costello Good morning ladies and gentleman. As your Chairman, it's my pleasure to welcome you to the 2019 AGM of Nine Entertainment Company. My name is Peter Costello. Before opening the meeting, I refer you to the disclaimer here on the screen behind me and available through our ASX lodgement. It is now shortly after 10am and I am advised that this is a properly constituted meeting. There's a quorum of at least two shareholders present so I declare the 2019 Annual General Meeting open. Unless there are any objections, I propose to take the Notice of Meeting as read. Copies of the Notice of Meeting are available from the registration desk outside should you require them. Let me now introduce the people who are with us this morning. To my immediate left is Rachel Launders, our General Counsel and Company Secretary. Then Hugh Marks, our Chief Executive Officer, who will address the meeting a little later. Next to Hugh is Nick Falloon, the Independent, Non-Executive Director and Deputy Chair and Member of the People and Remuneration Committee. Then we have Patrick Alloway, Independent, Non-Executive Director and a member of the Audit and Risk Management Committee. Next to Patrick is Sam Lewis, Independent, Non-Executive Director, Chair of the Audit and Risk Committee and a Member of the People and Remuneration Committee. Then we have Mickie Rosen, Independent, Non-Executive Director. At the far end, we have Catherine West, Independent, Non-Executive Director, the Chair of the People and Remuneration Committee and a member of the Audit and Risk Committee. -

("Conditions of Entry") Schedule Promotion: the Block Promoter: Nine Network Australia Pty Ltd ABN 88 008 685 407, 24 Artarmon Road, Willoughby, NSW 2068, Australia

NBN The Block Competition Terms & Conditions ("Conditions of Entry") Schedule Promotion: The Block Promoter: Nine Network Australia Pty Ltd ABN 88 008 685 407, 24 Artarmon Road, Willoughby, NSW 2068, Australia. Ph: (02) 9906 9999 Promotional Period: Start date: 09/10/16 at 09:00 am AEDT End date: 19/10/16 at 12:00 pm AEDT Eligible entrants: Entry is only open to residents of NSW and QLD only who are available to travel to Melbourne between 29/10/16 and 30/10/16. How to Enter: To enter the Promotion, the entrant must complete the following steps during the Promotional Period: (a) visit www.nbntv.com.au; (b) follow the prompts to the Promotion tab; (c) input the requested details in the Promotion entry form including their full name, address, daytime contact phone number, email address and code word (d) submit the fully completed entry form. Entries permitted: Entrants may enter multiple times provided each entry is submitted separately in accordance with the entry instructions above. The entrant is eligible to win a maximum of one (1) prize only. By completing the entry method, the entrant will receive one (1) entry. Total Prize Pool: $2062.00 Prize Description Number of Value (per prize) Winning Method this prize The prize is a trip for two (2) adults to Melbourne between 1 Up to Draw date: 29/10/2016 – 30/10/2016 and includes the following: AUD$2062.00 20/10/16 at 10:00 1 night standard twin share accommodation in am AEDT Melbourne (min 3.5 star) (conditions apply); return economy class flights for 2 adults from either Gold Coast or Newcastle to Melbourne); a guided tour of The Block apartments return airport and hotel transfers in Melbourne Prize Conditions: No part of the prize is exchangeable, redeemable or transferable. -

Harvester 6/8 Row Operator's Manual

OPERATING MANUAL 2009 WIC HARVESTER 2800 7TH Avenue North Fargo, ND 58102 Phone: (701) 232-4199 Fax: (701) 234-1716 www.amitytech.com MOHE59-9JUN08 MOHE59-9JUN08 MOHE59-9JUN08 CONTENTS INTRODUCTION………………………………………i OPERATING THE HARVESTER…………………. 8-1 Manufacturer's Guarantee Policy…………………. ii Raise Boom…………………………………………. 8-1 Start Up……………………………………………… 8-2 SAFETY……………………………………………… 1-1 Shut Down…………………………………………… 8-3 Break In……………………………………………… 8-3 SAFETY DECALS………………………………….. 2-1 Lifter Struts………………………………………….. 8-3 Digging Depth……………………………………….. 8-4 RECOMMENDED TRACTOR SPECIFICATIONS 3-1 Pinch Point Spacing……………………………….. 8-4 Minimum Tractor Horsepower……………………… 3-1 Pinch Point Position……………………………….. 8-5 PTO Output……………………………………………3-1 Paddles……………………………………………….8-6 Drawbar Weight Capacity……………………………3-1 Apron Chain…………………………………………. 8-7 Hydraulic Capacity Options…………………………3-2 Grabroll Bed…………………………………………. 8-8 Traction………………………………………………. 3-2 Field Cleaning………………………………………..8-9 Scrub Chain…………………………………………. 8-9 PREPARING THE TRACTOR…………………….. 4-1 Scrub Chain Tension…………………………………8-10 Adjusting the Drawbar……………………………..…4-1 Leveling Adjustments………………………………. 8-10 Tire Spacing and Inflation……………………………4-1 Row Finder……………………………………………8-11 Three Point Hitch Position………………………..…4-2 Wheel Fillers………………………………………… 8-11 Shaft Monitor/Control Box Location……………..…4-2 Attaching the Control Box………………………….. 4-3 LUBRICATION AND MAINTENANCE…………... 9-1 Alternate Wiring……………………………………... 4-3 Greasing………………………………………….……9-1 PTO RPM Setting…………………………………… 4-4 U-Joints…………………………………………...……9-2