Corporate Results Monitor

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Full Year Statutory Accounts

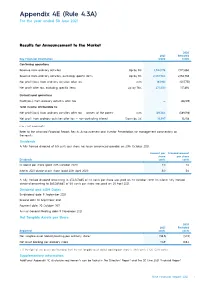

Appendix 4E (Rule 4.3A) For the year ended 30 June 2021 Results for Announcement to the Market 2020 2021 Restated Key Financial Information $’000 $’000 Continuing operations Revenue from ordinary activities Up by 8% 2,342,178 2,172,060 Revenue from ordinary activities, excluding specific items Up by 8% 2,332,984 2,156,785 Net profit/(loss) from ordinary activities after tax n/m 183,961 (507,751) Net profit after tax, excluding specific items Up by 76% 277,530 157,694 Discontinued operations Profit/(loss) from ordinary activities after tax — (66,189) Total income attributable to: Net profit/(loss) from ordinary activities after tax — owners of the parent n/m 169,364 (589,198) Net profit from ordinary activities after tax — non-controlling interest Down by 4% 14,597 15,258 n/m = not meaningful Refer to the attached Financial Report, Results Announcement and Investor Presentation for management commentary on the results. Dividends A fully franked dividend of 5.5 cents per share has been announced payable on 20th October 2021. Amount per Franked amount share per share Dividends cents cents Dividend per share (paid 20th October 2020) 2.0 2.0 Interim 2021 dividend per share (paid 20th April 2021) 5.0 5.0 A fully franked dividend amounting to $34,107,865 of 2.0 cents per share was paid on 20 October 2020. An interim fully franked dividend amounting to $85,269,663 of 5.0 cents per share was paid on 20 April 2021. Dividend and AGM Dates Ex-dividend date: 9 September 2021 Record date: 10 September 2021 Payment date: 20 October 2021 Annual General Meeting date: 11 November 2021 Net Tangible Assets per Share 2020 2021 Restated Reported cents cents Net tangible asset (deficit)/backing per ordinary share 1 (38.3) (40.9) Net asset backing per ordinary share 114.9 108.4 1. -

Gai Waterhouse “The Technology Is Very Innovative Yet Easy to Use. I Am Confident E-TRAKKA® Will Make a Significant Impact on the Racing Industry”

Gai Waterhouse “The technology is very innovative yet easy to use. I am confident E-TRAKKA® will make a significant impact on the racing industry”. Contents Invented by Trainers, for Trainers 2. How Does E-TRAKKA® Work? E-TRAKKA® was inspired by the needs of thoroughbred racehorse trainers to assess, monitor and remarkably 3. Equine Fitness for Trainers predict the performances of their elite and developing racehorses. 4. What is Fitness? By using state of the art heart rate monitoring and GPS ® Relationship of Heart Rate to Speed tracking systems, E-TRAKKA is able to generate charts which informs trainers about their horses’ fitness and ability 5. Understanding E-TRAKKA® Information to race. This revolutionary training tool was invented by Andrew 7. Using Charts to Identify Good and Bad Workouts Stuart, an experienced horseman whose credits include being an ex-jockey, assistant foreman for Bart Cummings Benefits of Building Profiles and racehorse trainer. Andrew’s invention recently featured on the popular television program ‘The New Inventors” and ® 9. Using E-TRAKKA to Identify Lameness won an esteemed episode award. 10. Take Over Target E-TRAKKA® was developed with a view to combine proven basic concepts to empower trainers. By using E-TRAKKA® 11. Using E-TRAKKA® Assess Recovery technology trainers now have the power to combine information on the horse’s fitness and racing potential with Success Story with E-TRAKKA® their invaluable practical skills as experienced horsemen. 13. Using E-TRAKKA® to Monitor Fitness Over Time The ‘cutting-edge’ information generated by E-TRAKKA® provides trainers with a simple informative ‘snap shot in 14. -

Deluxe Package

NSW DELUXE PACKAGE Unprecedented exposure for your premier property NSW DELUXE PACKAGE NSW DELUXE PACKAGE For the first time, Domain offers sellers this ultimate package – The cover of Domain in The Sydney Morning Herald and The Australian Financial Review, domain.com.au editorial exposure, a prime spot on the smh.com.au, domain.com.au, nine.com.au (NSW) 9news.com.au (NSW) homepages, plus extensive amplification through Domain’s leading social media platforms for your premier property. NSW DELUXE PACKAGE ELEMENTS Editorial • The cover of Domain in Saturday’s The SMH and Friday’s The AFR, plus cover story • Domain digital editorial article Magazine Advertising • Domain in The SMH and The AFR full page advertisement x 2 weeks • Domain Prestige in The AFR full page advertisement x 3 weeks Digital and Social Amplification • Domain Dream Homes on domain.com.au. smh.com.au, nine.com.au (NSW) and 9news.com.au (NSW) homepages • Listing showcased via Domain Facebook, Instagram and Twitter • Facebook Instant Experience INVESTMENT: $35,200 GST inclusive Cancellation of any portion of the NSW Deluxe Package that occurs after the first insertion / appearance date of any of the products outlined in the booking agreement will be billed at the total cost of the package. NSW Deluxe Packages are subject to availability. Editorial inclusion is subject to Editor approval. Online and magazine advertising terms and conditions: domain.com.au/group/agent-centre. Rates are for single resale properties only at the discretion of Domain and are not available for multiple dwelling buildings, projects or developments. Prices are subject to change without notice. -

Fairfax Media Ltd (Fxj) 16 August 2017

FAIRFAX MEDIA LTD (FXJ) 16 AUGUST 2017 RESULTS Full Year 2017 Full Year 2016 CHANGE Revenue ($m) 1,742.7 1830.5 -4.8% Bloomberg consensus ($m) 1,725.0 Domain EBITDA ($m) 113.1 120.0 -5.7% EBITDA ($m) 271.1 283.3 -4.3% Bloomberg consensus ($m) 263.8 Net profit (loss) after tax ($m) 83.9 (772.6) n/a Final Dividend ($) 0.02 0.02 no change Fairfax (FXJ) plans to spin-off Domain and trading to start in November Media group, Fairfax (FXJ) has returned to profitability, posting an improved $83.9m full year profit for the 12 months to June 30 and provided details on its planned Domain IPO. While underlying earnings (not including significant items) went backwards over the year, EBITDA came in ahead of market expectations. The result follows more than $900m in write-downs of its publishing assets which held back its FY16 result. While Domain has been its star performer for some time, its print business has been coming under pressure due to a slide in advertising dollars and a systemic change in the way Australians consume their news. FXJ confirmed it plans to spin-off its best performing asset, Domain and for trading in the real estate classifieds business to begin in mid to late November. The group intends to retain 60% of Domain with the remaining 40% to be distributed to FXJ shareholders. The split is still conditional on shareholder and regulatory approvals (including ASIC, ASX and ATO). Investors can expect the scheme booklet (which outlines all details of the separation) in late September 2017. -

Submission to the Inquiry Into Broadcasting, Online Content and Live Production to Rural and Regional Australia

SUBMISSION TO THE INQUIRY INTO BROADCASTING, ONLINE CONTENT AND LIVE PRODUCTION TO RURAL AND REGIONAL AUSTRALIA The Hon Bronwyn Bishop MP Chair Standing Committee on Communications and the Arts PO Box 6021 Parliament House CANBERRA ACT 2600 By email: [email protected] Introduction Thank you for the opportunity to make a submission to the House of Representatives Standing Committee on Communications and the Arts inquiry into broadcasting, online content and live production to rural and regional Australia. This letter is on behalf of the three major regional television providers, Prime Media Group (Prime Media), the WIN Network (WIN) and Southern Cross Austereo (SCA). Prime Media and SCA are members of Free TV Australia, the television peak body which has also made a submission to this inquiry on behalf of the industry. Prime Media broadcasts in northern New South Wales, southern New South Wales, the Australian Capital Territory, regional Victoria, Mildura, the Gold Coast area of south eastern Queensland and all of regional Western Australia. WIN broadcasts in southern New South Wales, the Australian Capital Territory, regional Queensland, regional Victoria, Tasmania, Griffith, regional WA, Mildura, Riverland and Mt Gambier in South Australia. SCA broadcasts in northern New South Wales, southern New South Wales, Queensland, the Australian Capital Territory, Griffith, regional Victoria, Tasmania, the Northern Territory and the Spencer Gulf region of South Australia. Through affiliation agreements, Prime Media, WIN and SCA purchase almost all of their programming from metropolitan networks1 and using more than 500 transmission towers located across the country, retransmit that programming into regional television licence areas. -

HEADLINE NEWS • 6/18/07 • PAGE 2 of 7

Indian Vale to Delaware or HEADLINE Saratoga? p.7 NEWS For information about TDN, DELIVERED EACH NIGHT BY FAX AND FREE BY E-MAIL TO SUBSCRIBERS OF call 732-747-8060. www.thoroughbreddailynews.com MONDAY, JUNE 18, 2007 GETTING READY FOR ROYAL ASCOT WINNING WITH FLARE Royal Ascot gets underway tomorrow, with the fields Indian Flare (Cherokee Run) showed her determina- for an explosive first day drawn yesterday. Much focus tion and versatility to hold off classy challenger Oprah has been placed on the quartet of Australian sprinters Winney (Royal Academy) in the GII Vagrancy H. at heading for the G2 Belmont Park Sunday. Installed the lukewarm 5-2 favor- King=s Stand S. at ite in her first start in over two five furlongs. The months, the five-year-old Royal Ascot media broke well and settled in a guide emphasizes the stalking third, tucked in along meeting=s place in the the rail behind early leaders Global Sprint Chal- Any Limit (Limit Out) and Mary lenge. It played a piv- Delaney (Hennessy). Oprah otal role in the Chal- Winney found her stride turn- lenge 12 months ago ing into the stretch and made Takeover Target HKJC Photo when the eventual Indian Flare Adam Coglianese it to the front for a brief mo- champion Takeover ment, but Indian FlareBwho Target (Aus) (Celtic Swing {GB}) collected the King=s was pinned along the rail--proved unrelenting and bat- Stand en route. Ex-cabbie Joe Janiak=s star veteran is tled back late to forge ahead and win by a half length. -

Nine Network Australia Selects Intelsat to Distribute Domestic Television Programming

Nine Network Australia Selects Intelsat to Distribute Domestic Television Programming October 24, 2016 Intelsat will provide satellite connectivity and global fiber services via the IntelsatOne network to bring news content from around the world to Australia LUXEMBOURG--(BUSINESS WIRE)--Oct. 24, 2016-- Intelsat (NYSE: I), operator of the world’s first Globalized Network, powered by its leading satellite backbone, today announced a contract with Nine Network Australia to distribute programming to the company’s six domestic television stations as well as provide global satellite and fiber connectivity using the IntelsatOne terrestrial network to bring news content and special events from around the world to Australia for its network affiliates. Nine Network Australia (NNA) is one of the country’s top-rated commercial television networks, with local stations in Sydney, Melbourne, Brisbane, Adelaide, Perth and Darwin, along with a regional broadcaster, NBN. The network also has news bureaus in Canberra, London and Los Angeles. NNA is a subsidiary of Nine Entertainment Co., one of Australia’s leading media companies. Intelsat initially is providing services via the Australia/New Zealand Ku-Band beam on Intelsat 19 for the network’s broadcasting requirement. Under the agreement, Intelsat’s network support will extend well into the next decade. “Our Globalized Network allows us to meet NNA’s needs today and to increase our level of support if the network expands over time to meet the demands of multi-platform coverage,” said Terry Bleakley, Regional Vice President, Asia Pacific Sales, Intelsat. “NNA will also benefit from Intelsat’s global coverage for international contribution and distribution requirements.” NNA previously used Intelsat for its domestic and international occasional use requirements. -

2015 SWM Annual Report

ABN 91 053 480 845 Delivering the future of content. Anywhere. Any screen. Anytime. Annual Report 2015 Seven West Media cares about the environment. By printing 2000 copies of this Annual Report on ecoStar Silk and ecoStar Offset the environmental impact was reduced by*: 1,185kg 171kg 1,707km of landfill of CO2 and travel in the average greenhouse gases European car 26,982 2,486kWh 1,926kg litres of water of energy of wood Source: European BREF data (virgin fibre paper). Carbon footprint data evaluated by Labelia Conseil in accordance with the Bilan Carbone® methodology. Results are obtained according to technical information and are subject to modification. *compared to a non-recycled paper. Delivering the future of content. Anywhere. Any screen. Anytime. Annual Report 2015 Contents What We Do 4 The Future of Us 44 Our Brands 6 Board of Directors 46 Our Strategy 8 Corporate Governance Statement 49 Our Strategic Framework 10 Directors’ Report 60 Letter from the Chairman 12 Remuneration Report 64 Letter from the Managing Director & CEO 14 Auditor’s Independence Declaration 83 Performance Dashboard 16 Financial Statements 84 Performance of the Business 18 Directors’ Declaration 134 Group Performance 20 Independent Auditor’s Report 135 Television 26 Company Information 137 Newspapers 32 Investor Information 138 Magazines 36 Shareholder Information 139 Other Business and New Ventures 40 Risk, Environment and Social Responsibility 42 2 Seven West Media Annual Report 2015 ABN 91 053 480 845 Contents The right people creating great content across television, digital, mobile and newspaper and magazine publishing. Delivering the future of content 3 What We Do We are achieving growth in the delivery of our content across our portfolio of integrated media platforms. -

Unemployment Insurance and Takeovers*

Unemployment Insurance and Takeovers* Lixiong Guo† University of Alabama Jing Kong‡ Michigan State University Ronald W. Masulis§ University of New South Wales December 11, 2019 Abstract We examine whether unemployment insurance (UI) mitigates shareholder-employee conflicts of interest and improves takeover market efficiency. Exploiting within state changes in UI benefits, we find that increased target state UI benefits raise acquisition likelihoods, expected deal synergies, and gains to both acquirer and target shareholders. UI effects on acquisition likelihood are stronger in highly unionized industries, in firms with concentrated employee ownership, and in firms with employee friendly boards. The passage of directors’ duties laws increases the UI effect on acquisition likelihood. Lastly, increased acquirer state UI benefits raise acquirer returns and likelihood of acquirers making within-industry acquisitions. JEL Classification: G32, G34, G38, J65 Keywords: Unemployment Insurance, Labor, Takeovers, Mergers and Acquisitions, Synergy, Stakeholders, Unemployment Risk. * We are grateful to Shai Bernstein, Oleg Chuprinin, Andrey Golubov (discussant), Vidhan Goyal, Chang-Mo Kang, Hao Liang (discussant), Shawn Mobbs, Hernan Ortiz-Molina (discussant), Peter Swan, Li Yang, Xianming Zhou, and seminar participants at UNSW Sydney, Deakin University, University of Alabama, and conference participants at the 2017 NFA Conference in Halifax, 2017 FMA Conference in Boston, 2017 AsianFA Conference in Seoul, and 2017 FIRN Corporate Conference in Adelaide for helpful discussions and valuable comments. All errors are our own. † Lixiong Guo is with the University of Alabama. Address: Culverhouse College of Business, University of Alabama, 232 Alston Hall, 361 Stadium Drive, Tuscaloosa, Alabama, 35487-0224. Electronic Mail: [email protected]. ‡ Jing Kong is with the Michigan State University. -

Asia Property Market Sentiment Report H2 2016

TABLE OF CONTENTS CEO’s Note………………………………………………………………….…….....2 Executive Summary…………………………………………...……………….……3 Methodology, Assumptions and Caveats………………………………………....4 Results Analysis, Asia Overview………………………………….…………….…5 Malaysia……………………………...……………………………………..….…….6 Demographics…………………………………..…..…………….….……..11 Sentiments………………………………………………...…………..…….30 Overseas Property……………………………..………………….………..47 Indonesia……………………………………………….………………………......59 Demographics……………………………………….………………..…....64 Sentiments…………………………………………………...……………..91 Overseas Property……………………………….…..….…………..…….95 Singapore………………………………………………………………………….102 Demographics…………………………………………………………….106 Sentiments………….……………………………………………………..131 Overseas Property ……………………………………………………….153 Hong Kong………………………………………………………………………...166 Demographics………………………………………………..……..….....169 Sentiments………………………………………………………………...182 Overseas Property…………………………………………………...…...202 Conclusion –Outlook for 2016 H2…………………….……………………...….214 1 CEO’S NOTE We are once again pleased to share with you the findings of our tenth iProperty.com Asia Property Market Sentiment Report. This survey report reveals sentiments for the second half of 2016 in all the countries the iProperty Group operates in. The survey was conducted over a month, from 5th July to 8th August 2016, across our market-leading network of property portals and gathered responses from 15,000 respondents. Similar to previous survey findings, affordability continues to remain a major concern in all the countries surveyed. This is just one of -

Annual Report 2020 Contents

Annual Report 2020 Contents Business Performance Overview 2 Chairman’s Report 4 CEO’s Report 6 Corporate Social Responsibility 10 Directors' Report 19 Remuneration Report 26 Corporate Governance Statement 45 Management Discussion and Analysis Report 59 Auditor’s Independence Declaration 62 2020 Financial Report 63 Shareholder Information 117 Corporate Directory 120 Inspiring confidence for all of life’s property decisions We are a leading property technology and services business that is home to one of the largest portfolios of property brands in Australia. Domain helps agents and consumers at every step in the property lifecycle – renting, buying, selling, investing, financing, insurance and utilities. The Domain Group is home to Domain, Allhomes, Commercial Real Estate, and CommercialView. Our portfolio also includes agent products Homepass, Pricefinder and Real Time Agent. Our consumer solutions products include Domain Loan Finder and Domain Insure. As a customer-centric property marketplace, we are committed to making the property journey easier, more enjoyable and connected at every stage. Annual Report 2020 1 Business Performance Overview Core Digital Residential by COVID-19’s impact on key advertising Residential generates revenue through categories in H2. The Developer market listings of ‘for sale’ and rental properties was impacted by the deferral of high rise across its desktop, mobile and social apartment projects resulting from lower platforms. Premium (depth) listing investor demand and COVID-19 impacts products account for the largest on immigration. Activity in smaller, proportion of revenue, with monthly boutique projects was stronger, however these require lower levels of marketing * subscriptions contributing the balance. $227.0m support. Commercial Real Estate (CRE) FY20 Revenue Residential revenue reduced 7%, a delivered solid revenue growth for the solid performance in an environment year. -

HEADLINE NEWS • 1/20/07 • PAGE 2 of 3

MISS FINLAND TO DUBAI? HEADLINE ...p3 NEWS For information about TDN, DELIVERED EACH NIGHT BY FAX AND FREE BY E-MAIL TO SUBSCRIBERS OF call 732-747-8060. www.thoroughbreddailynews.com SATURDAY, JANUARY 20, 2007 ISLAND IN THE SUN SALES COMPANIES CALL FOR STEROID POLICY Friendly Island (Crafty Friend) may be enjoying the The Keeneland Association Inc. and Fasig-Tipton California sunshine this winter, but it will be a working Company, Inc., yesterday issued a statement advocat- holiday for the New York-bred six-year-old. Freshened ing the development of a policy re- after running second as a garding the use of anabolic steroids 56-1 outsider in the GI Breed- in sales horses. The sales companies ers= Cup Sprint at Churchill have formed a commitee comprised Downs Nov. 4, he returns to of their own representatives, as well action against three rivals in as authorities on steroids and drug the GII Palos Verdes H. at testing, members of the Consignors Santa Anita this afternoon. and Commercial Breeders Association The Anstu Stables color- and veterinarians, to establish guide- bearer won six of his first lines for appropriate steroid use and for testing. Nick Nicholson, president Friendly Island Adam Coglianese nine career starts, including the Hudson H. in October of and CEO of Keeneland, and Walt 2005, and capped that season with a fourth in the GI Robertson, president of Fasig-Tipton, Horsephotos were jointly quoted in the statement, De Francis Dash. He picked up checks in the GIII Mr. which read, AWe both agree that the use of anabolic Prospector H.