Original.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Full Year Statutory Accounts

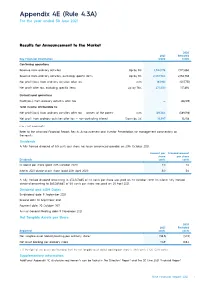

Appendix 4E (Rule 4.3A) For the year ended 30 June 2021 Results for Announcement to the Market 2020 2021 Restated Key Financial Information $’000 $’000 Continuing operations Revenue from ordinary activities Up by 8% 2,342,178 2,172,060 Revenue from ordinary activities, excluding specific items Up by 8% 2,332,984 2,156,785 Net profit/(loss) from ordinary activities after tax n/m 183,961 (507,751) Net profit after tax, excluding specific items Up by 76% 277,530 157,694 Discontinued operations Profit/(loss) from ordinary activities after tax — (66,189) Total income attributable to: Net profit/(loss) from ordinary activities after tax — owners of the parent n/m 169,364 (589,198) Net profit from ordinary activities after tax — non-controlling interest Down by 4% 14,597 15,258 n/m = not meaningful Refer to the attached Financial Report, Results Announcement and Investor Presentation for management commentary on the results. Dividends A fully franked dividend of 5.5 cents per share has been announced payable on 20th October 2021. Amount per Franked amount share per share Dividends cents cents Dividend per share (paid 20th October 2020) 2.0 2.0 Interim 2021 dividend per share (paid 20th April 2021) 5.0 5.0 A fully franked dividend amounting to $34,107,865 of 2.0 cents per share was paid on 20 October 2020. An interim fully franked dividend amounting to $85,269,663 of 5.0 cents per share was paid on 20 April 2021. Dividend and AGM Dates Ex-dividend date: 9 September 2021 Record date: 10 September 2021 Payment date: 20 October 2021 Annual General Meeting date: 11 November 2021 Net Tangible Assets per Share 2020 2021 Restated Reported cents cents Net tangible asset (deficit)/backing per ordinary share 1 (38.3) (40.9) Net asset backing per ordinary share 114.9 108.4 1. -

Deluxe Package

NSW DELUXE PACKAGE Unprecedented exposure for your premier property NSW DELUXE PACKAGE NSW DELUXE PACKAGE For the first time, Domain offers sellers this ultimate package – The cover of Domain in The Sydney Morning Herald and The Australian Financial Review, domain.com.au editorial exposure, a prime spot on the smh.com.au, domain.com.au, nine.com.au (NSW) 9news.com.au (NSW) homepages, plus extensive amplification through Domain’s leading social media platforms for your premier property. NSW DELUXE PACKAGE ELEMENTS Editorial • The cover of Domain in Saturday’s The SMH and Friday’s The AFR, plus cover story • Domain digital editorial article Magazine Advertising • Domain in The SMH and The AFR full page advertisement x 2 weeks • Domain Prestige in The AFR full page advertisement x 3 weeks Digital and Social Amplification • Domain Dream Homes on domain.com.au. smh.com.au, nine.com.au (NSW) and 9news.com.au (NSW) homepages • Listing showcased via Domain Facebook, Instagram and Twitter • Facebook Instant Experience INVESTMENT: $35,200 GST inclusive Cancellation of any portion of the NSW Deluxe Package that occurs after the first insertion / appearance date of any of the products outlined in the booking agreement will be billed at the total cost of the package. NSW Deluxe Packages are subject to availability. Editorial inclusion is subject to Editor approval. Online and magazine advertising terms and conditions: domain.com.au/group/agent-centre. Rates are for single resale properties only at the discretion of Domain and are not available for multiple dwelling buildings, projects or developments. Prices are subject to change without notice. -

Fairfax Media Ltd (Fxj) 16 August 2017

FAIRFAX MEDIA LTD (FXJ) 16 AUGUST 2017 RESULTS Full Year 2017 Full Year 2016 CHANGE Revenue ($m) 1,742.7 1830.5 -4.8% Bloomberg consensus ($m) 1,725.0 Domain EBITDA ($m) 113.1 120.0 -5.7% EBITDA ($m) 271.1 283.3 -4.3% Bloomberg consensus ($m) 263.8 Net profit (loss) after tax ($m) 83.9 (772.6) n/a Final Dividend ($) 0.02 0.02 no change Fairfax (FXJ) plans to spin-off Domain and trading to start in November Media group, Fairfax (FXJ) has returned to profitability, posting an improved $83.9m full year profit for the 12 months to June 30 and provided details on its planned Domain IPO. While underlying earnings (not including significant items) went backwards over the year, EBITDA came in ahead of market expectations. The result follows more than $900m in write-downs of its publishing assets which held back its FY16 result. While Domain has been its star performer for some time, its print business has been coming under pressure due to a slide in advertising dollars and a systemic change in the way Australians consume their news. FXJ confirmed it plans to spin-off its best performing asset, Domain and for trading in the real estate classifieds business to begin in mid to late November. The group intends to retain 60% of Domain with the remaining 40% to be distributed to FXJ shareholders. The split is still conditional on shareholder and regulatory approvals (including ASIC, ASX and ATO). Investors can expect the scheme booklet (which outlines all details of the separation) in late September 2017. -

Corporate Results Monitor

Corporate Results Monitor FNArena's All-Year Round Australian Corporate Results Monitor. Currently monitoring August 2019. TOTAL STOCKS: 272 Total Rating Upgrades: 61 Beats In Line Misses Total Rating Downgrades: 66 61 140 71 Simple average net target price change: 2.40% 22.4% 51.5% 26.1% Beat/Miss Ratio: 0.86 Latest Prev New Company Result Upgrades Downgrades Buy/Hold/Sell Brokers Target Target ABC - ADELAIDE BRIGHTON IN LINE 0 0 0/2/4 3.28 3.13 6 While Adelaide Brighton's result matched fresh guidance provided following a profit warning in July, it did still exceed most broker forecasts. FY20 guidance is bleak, given the housing construction downturn has as yet no end in sight and increased infrastructure construction is not sufficient to offset. The suspension of the dividend also came as no shock, but an intent to acquire and build out an integrated, infrastructure-oriented business model carries risk and reduces dividend prospects near-term. APT - AFTERPAY TOUCH BEAT 0 0 2/0/0 30.43 33.43 2 Afterpay Touch's FY19 net loss was slightly less than Morgans expected. The results suggest continuing strong sales momentum and stable margins across the business. Morgans downgrades FY20-21 earnings estimates, factoring in higher investment expenditure associated with offshore expansion. Traction in the US is strong but the key for Ord Minnett in the FY19 result were the initial customer acquisitions in the UK, which were well above expectations. Average merchant fees were slightly ahead of expectations, particularly in the US. AOG - AVEO IN LINE 0 1 0/2/0 2.15 2.15 2 Aveo Group's FY19 net profit was in line with recently downgraded guidance. -

Asia Property Market Sentiment Report H2 2016

TABLE OF CONTENTS CEO’s Note………………………………………………………………….…….....2 Executive Summary…………………………………………...……………….……3 Methodology, Assumptions and Caveats………………………………………....4 Results Analysis, Asia Overview………………………………….…………….…5 Malaysia……………………………...……………………………………..….…….6 Demographics…………………………………..…..…………….….……..11 Sentiments………………………………………………...…………..…….30 Overseas Property……………………………..………………….………..47 Indonesia……………………………………………….………………………......59 Demographics……………………………………….………………..…....64 Sentiments…………………………………………………...……………..91 Overseas Property……………………………….…..….…………..…….95 Singapore………………………………………………………………………….102 Demographics…………………………………………………………….106 Sentiments………….……………………………………………………..131 Overseas Property ……………………………………………………….153 Hong Kong………………………………………………………………………...166 Demographics………………………………………………..……..….....169 Sentiments………………………………………………………………...182 Overseas Property…………………………………………………...…...202 Conclusion –Outlook for 2016 H2…………………….……………………...….214 1 CEO’S NOTE We are once again pleased to share with you the findings of our tenth iProperty.com Asia Property Market Sentiment Report. This survey report reveals sentiments for the second half of 2016 in all the countries the iProperty Group operates in. The survey was conducted over a month, from 5th July to 8th August 2016, across our market-leading network of property portals and gathered responses from 15,000 respondents. Similar to previous survey findings, affordability continues to remain a major concern in all the countries surveyed. This is just one of -

Annual Report 2020 Contents

Annual Report 2020 Contents Business Performance Overview 2 Chairman’s Report 4 CEO’s Report 6 Corporate Social Responsibility 10 Directors' Report 19 Remuneration Report 26 Corporate Governance Statement 45 Management Discussion and Analysis Report 59 Auditor’s Independence Declaration 62 2020 Financial Report 63 Shareholder Information 117 Corporate Directory 120 Inspiring confidence for all of life’s property decisions We are a leading property technology and services business that is home to one of the largest portfolios of property brands in Australia. Domain helps agents and consumers at every step in the property lifecycle – renting, buying, selling, investing, financing, insurance and utilities. The Domain Group is home to Domain, Allhomes, Commercial Real Estate, and CommercialView. Our portfolio also includes agent products Homepass, Pricefinder and Real Time Agent. Our consumer solutions products include Domain Loan Finder and Domain Insure. As a customer-centric property marketplace, we are committed to making the property journey easier, more enjoyable and connected at every stage. Annual Report 2020 1 Business Performance Overview Core Digital Residential by COVID-19’s impact on key advertising Residential generates revenue through categories in H2. The Developer market listings of ‘for sale’ and rental properties was impacted by the deferral of high rise across its desktop, mobile and social apartment projects resulting from lower platforms. Premium (depth) listing investor demand and COVID-19 impacts products account for the largest on immigration. Activity in smaller, proportion of revenue, with monthly boutique projects was stronger, however these require lower levels of marketing * subscriptions contributing the balance. $227.0m support. Commercial Real Estate (CRE) FY20 Revenue Residential revenue reduced 7%, a delivered solid revenue growth for the solid performance in an environment year. -

NSW Telco Authority Annual Report 2019/2020 Cover Photo: Tower Delivered Under the Critical Communications Enhancement Program at Jolly Nose Near Port Macquarie

NSW Telco Authority Annual Report 2019/2020 Cover photo: Tower delivered under the Critical Communications Enhancement Program at Jolly Nose near Port Macquarie. Tower under construction as part of the Critical Communications Enhancement Program at Ballina. 03 Contents Letter to the Minister ______________________________________________________ 05 Chairperson’s report _______________________________________________________ 06 Managing Director’s report _________________________________________________ 08 NSW Telco Authority highlights ______________________________________________10 About the NSW Telco Authority ______________________________________________ 11 Functions, structure and strategic priorities _____________________________________ 13 Customers _______________________________________________________________ 19 Operational performance ____________________________________________________22 Operational reviews _______________________________________________________ 26 Participation in Inquiries and consultations _____________________________________27 Major Programs ___________________________________________________________ 31 Governance _____________________________________________________________ 36 A Great Place to Work _____________________________________________________ 40 Cyber Security Attestation__________________________________________________ 42 Internal Auditors Report ___________________________________________________ 43 Financial statements ______________________________________________________ 46 Matters included -

COLLABORATIVE COMPUTATIONAL TECHNOLOGIES for BIOMEDICAL RESEARCH Wiley Series on Technologies for the Pharmaceutical Industry Sean Ekins , Series Editor

COLLABORATIVE COMPUTATIONAL TECHNOLOGIES FOR BIOMEDICAL RESEARCH Wiley Series on Technologies for the Pharmaceutical Industry Sean Ekins , Series Editor Editorial Advisory Board Dr. Ren é e J.G. Arnold (ACT LLC, USA) Dr. David D. Christ (SNC Partners LLC, USA) Dr. Michael J. Curtis (Rayne Institute, St Thomas ’ Hospital, UK) Dr. James H. Harwood (Delphi BioMedical Consultants, USA) Dr. Maggie A.Z. Hupcey (PA Consulting, USA) Dr. Dale Johnson (Emiliem, USA) Prof. Tsuguchika Kaminuma, (Tokyo Medical and Dental University, Japan) Dr. Mark Murcko, (Vertex, USA) Dr. Peter W. Swaan (University of Maryland, USA) Dr. Ana Szarfman (FDA, USA) Dr. David Wild (Indiana University, USA) Computational Toxicology: Risk Assessment for Pharmaceutical and Environmental Chemicals Edited by Sean Ekins Pharmaceutical Applications of Raman Spectroscopy Edited by Slobodan Š a š i c´ Pathway Analysis for Drug Discovery: Computational Infrastructure and Applications Edited by Anton Yuryev Drug Effi cacy, Safety, and Biologics Discovery: Enmerging Technologies and Tools Edited by Sean Ekins and Jinghai J. Xu The Engines of Hippocrates: From the Dawn of Medicine to Medical and Pharmaceutical Informatics Barry Robson and O.K. Baek Pharmaceutical Data Mining: Applications for Drug Discovery Edited by Konstantin V. Balakin The Agile Approach to Adaptive Research: Optimizing Effi ciency in Clinical Development Michael J. Rosenberg Pharmaceutical and Biomedical Project Management in a Changing Global Environment Scott D. Babler COLLABORATIVE COMPUTATIONAL TECHNOLOGIES FOR -

RATINGS SNAPSHOT: 9NOW DOMINATES COMMERCIAL PREMIUM DIGITAL VIDEO MARKET May 3, 2021

RATINGS SNAPSHOT: 9NOW DOMINATES COMMERCIAL PREMIUM DIGITAL VIDEO MARKET May 3, 2021 The 9Network’s live and on-demand platform 9Now has dominated the first four months of 2021 following the ratings success of Married at First Sight and LEGO Masters. As of April 30, 2021, 9Now had recorded a massive 50% share of minutes consumed between January and the end of April among Total People. In the key demographics, 9Now has a 53% share among both 18-39s and 25-54s. In the live streaming space, 9Now was also the clear dominant platform with a 54% share following the success of the Australian Open. This equates to 1.5 billion live minutes, 61% more than its nearest competitor. Married at First Sight was also the No.1 on-demand program against all BVOD platforms with more than 880 million minutes of long-form catch-up content streamed, 3.7 times more than its nearest competitor. So far this year Nine’s Married at First Sight has eight of the Top 10 in on-demand programs and nine of the Top 10 live BVOD programs, while LEGO Masters also continues to perform strongly in the weekly BVOD ratings. Hamish Turner, Nine’s Program Director, said: “9Now has strengthened its position as the clear No.1 in the digital and BVOD market. Nine has a suite of content offerings in the Australian Open, Married at First Sight and LEGO Masters which have all perform strongly on both linear and digital platforms. nineforbrands.com.au Nine Sydney - 1 Denison Street, North Sydney, NSW, 2068 ABN 60 122 203 892 “We continue to see strong growth across the BVOD category and expect our digital momentum to continue throughout the year with Beauty and The Geek, Love Island Australia and UK and The Block still to come, in addition we have created catalogue depth through deals with Warner Brother, NBC and Discovery.” Nick Young, Nine’s Director of Sales – Publishing and Digital, said: “It has been an extraordinary quarter for 9Now. -

Corporate Results Monitor

Corporate Results Monitor FNArena's All-Year Round Australian Corporate Results Monitor. Currently monitoring August 2021. TOTAL STOCKS: 345 Total Rating Upgrades: 50 Beats In Line Misses Total Rating Downgrades: 70 117 153 75 Total target price movement in aggregate: 4.60% 33.9% 44.3% 21.7% Average individual target price change: 3.29% Beat/Miss Ratio: 1.56 Previous Corporate Results Updates Prev New Company Result Upgrades Downgrades Buy/Hold/Sell Brokers Target Target A2M - a2 Milk Co MISS 1 0 3/0/2 6.43 6.09 5 a2 Milk's result came in at the low end of guidance but more disturbing for Macquarie (Sell) was management commentary suggesting a weak FY22. No specific guidance was offered. Credit Suisse (Sell) believes the main reason investors will be lowering FY22-24 earnings estimates is due to Chinese 2020-21 births being relatively low. Citi is encouraged by the resolution of the excess and dated inventory position, restructured distributor agreements, and improved inventory tracking and traceability systems, and upgrades to Buy. UBS (Buy) anticipates a meaningful recovery in both daigou and CBEC infant formula sales over the next three years. ABP - Abacus Property BEAT 0 0 0/3/0 3.12 3.34 3 Abacus Property's result beat forecasts, driven by a stronger storage operating performance and development contribution. No guidance was offered but recent acquisitions offer FY22 upside, and the balance sheet is set for further acquisitions. The REIT plans to wind down its "non-core" development business, which shifts the risk focus. That, and the headwinds facing office assets, has Macquarie more cautious. -

Annual Report 2019 OVERVIEW

Annual Report 2019 OVERVIEW During FY19, Nine completed the merger with Fairfax Media, creating Australia’s leading integrated media business. Nine today has a clearly diversified earnings base, with four key operational pillars — Broadcasting, Digital and Publishing, Stan as well as a 59% stake in Domain. These businesses are all at different stages of their evolution, and are all scale businesses in their own right. In FY19, on a Pro Forma basis, the traditional Broadcasting business contributed just over half of Group revenue, down from 84% in FY18, marking a real change in the drivers of Nine for the future. Result in brief In FY19, Nine reported Group EBITDA of $350 million, up 36% on FY18, driven by a 40% increase in Group Revenues to $1.8 billion, reflecting the impact of the merger with Fairfax from 7 December. On a continuing business basis, Statutory Net Profit after Tax and Specific Items, which were predominately accounting led non-cash items, was $217 million, up 3%. On a Pro Forma basis, NEC reported Group EBITDA of $424 million, up 10% on FY18, on revenue of $2.3 billion. Net Profit after Tax and minority interests increased by 16% to $198 million compared to the FY18 result. Earnings per share was 11.6 cents, (+16%) and a full-year dividend of 10c per share, fully franked, was declared. Revenue1 split FY19 10% Pro Forma EBITDA growth driven by 300 7% 250 -11% 9% 200 150 +56% 100 54% -17% 30% 50 0 +48% -50 +56% +48% -100 FY18 FY19 Broadcasting Domain Digital & Publishing Stan Broadcasting Digital & Publishing Domain Stan -

Nine Entertainment Co. H1 Fy19 Results

NINE ENTERTAINMENT CO. H1 FY19 RESULTS 21 February 2019: Nine Entertainment Co. (ASX: NEC) has released its H1 FY19 results for the six months to December 2018. On a Statutory basis, Nine reported a Net Profit After Tax of $172m, down 1% on the previous corresponding period. On a Pro Forma, Continuing Business and pre Specific Item basis, Nine reported Group EBITDA growth of 6% to $252m, on Revenue of $1,204m (-3%) and Net Profit After Tax and Minority Interests of $126m (+5%). Highlights include: Strong FTA share and double digit cost reduction, offsetting weakness in the FTA market 39% growth in Digital & Publishing EBITDA underpinned by >50% growth in both Metro Media and 9Now Broadly flat contribution from Domain (ex Consumer Solutions businesses) in a cyclical housing market c1.5m active subscribers at Stan, growth of more than 60% over the 12 months, with Stan expected to move into profit from Q4 Hugh Marks, Chief Executive Officer of Nine Entertainment Co. said: “The merger with Fairfax has created Australia’s pre-eminent media company, with a diverse suite of assets that now reach more Australians each week than those of any other local media company. This half year result is a testimony to the new Nine. With around 55% of our revenue coming from a stable base of broadcasting and 45% coming from businesses that are in strong long term growth markets. Meaning we’ve been able to grow EBITDA through a more demanding operating environment, at the same time investing for the future of our business. Nine is now uniquely positioned through the combination of the operating strength of our traditional media assets as well as an increasing exposure to the continued transition of the market towards digital media assets.” For personal use only Accounting impact of the merger with Fairfax The implementation date of the merger was 7 December 2018.