Corporate Results Monitor

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Full Year Statutory Accounts

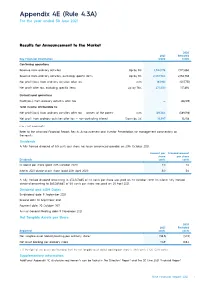

Appendix 4E (Rule 4.3A) For the year ended 30 June 2021 Results for Announcement to the Market 2020 2021 Restated Key Financial Information $’000 $’000 Continuing operations Revenue from ordinary activities Up by 8% 2,342,178 2,172,060 Revenue from ordinary activities, excluding specific items Up by 8% 2,332,984 2,156,785 Net profit/(loss) from ordinary activities after tax n/m 183,961 (507,751) Net profit after tax, excluding specific items Up by 76% 277,530 157,694 Discontinued operations Profit/(loss) from ordinary activities after tax — (66,189) Total income attributable to: Net profit/(loss) from ordinary activities after tax — owners of the parent n/m 169,364 (589,198) Net profit from ordinary activities after tax — non-controlling interest Down by 4% 14,597 15,258 n/m = not meaningful Refer to the attached Financial Report, Results Announcement and Investor Presentation for management commentary on the results. Dividends A fully franked dividend of 5.5 cents per share has been announced payable on 20th October 2021. Amount per Franked amount share per share Dividends cents cents Dividend per share (paid 20th October 2020) 2.0 2.0 Interim 2021 dividend per share (paid 20th April 2021) 5.0 5.0 A fully franked dividend amounting to $34,107,865 of 2.0 cents per share was paid on 20 October 2020. An interim fully franked dividend amounting to $85,269,663 of 5.0 cents per share was paid on 20 April 2021. Dividend and AGM Dates Ex-dividend date: 9 September 2021 Record date: 10 September 2021 Payment date: 20 October 2021 Annual General Meeting date: 11 November 2021 Net Tangible Assets per Share 2020 2021 Restated Reported cents cents Net tangible asset (deficit)/backing per ordinary share 1 (38.3) (40.9) Net asset backing per ordinary share 114.9 108.4 1. -

Agpasa, Brendon

29 January 2021 The Hon Paul Fletcher MP PO Box 6022 House of Representatives Parliament House Canberra ACT 2600 CHRIS (BRENDON) AGPASA SUBMISSION TO THE 2021-22 PRE-BUDGET SUBMISSIONS Dear Minister Fletcher, I write to request assistance had appropriate for media diversity to support digital radio and TV rollouts will continue in the federal funding, Brendon Agpasa was a student, radio listener and TV viewer. Paul Fletcher MP and the Morrison Government is supporting the media diversity including digital radio rollout, transition of community television to an online operating model, digital TV rollout, radio and TV services through regional media and subscription TV rollout we’re rolled out for new media landscape and it’s yours to towards a digital future of radio and TV broadcasting. We looking up for an expansion of digital radio rollout has been given consideration, the new digital spectrum to test a trial DRM30 and DRM+ with existing analogue (AM/FM) radio services, shortwave radio and end of spectrum (VHF NAS licences) will be adopted Digital Radio Mondiale services in Australia for the future plans. The radio stations Sydney’s 2GB, Melbourne’s 3AW, Brisbane’s Nova 106.9, Adelaide’s Mix 102.3, Perth’s Nova 93.7, Hit FM and Triple M ranks number 1 at ratings survey 8 in December 2020. Recently in December 2020, Nova Entertainment had launched it’s new DAB+ stations in each market, such as Nova Throwbacks, Nova 90s, Nova Noughties, Nova 10s, Smooth 80s and Smooth 90s to bring you the freshest hits, throwbacks and old classics all day everyday at Nova and Smooth FM. -

Deluxe Package

NSW DELUXE PACKAGE Unprecedented exposure for your premier property NSW DELUXE PACKAGE NSW DELUXE PACKAGE For the first time, Domain offers sellers this ultimate package – The cover of Domain in The Sydney Morning Herald and The Australian Financial Review, domain.com.au editorial exposure, a prime spot on the smh.com.au, domain.com.au, nine.com.au (NSW) 9news.com.au (NSW) homepages, plus extensive amplification through Domain’s leading social media platforms for your premier property. NSW DELUXE PACKAGE ELEMENTS Editorial • The cover of Domain in Saturday’s The SMH and Friday’s The AFR, plus cover story • Domain digital editorial article Magazine Advertising • Domain in The SMH and The AFR full page advertisement x 2 weeks • Domain Prestige in The AFR full page advertisement x 3 weeks Digital and Social Amplification • Domain Dream Homes on domain.com.au. smh.com.au, nine.com.au (NSW) and 9news.com.au (NSW) homepages • Listing showcased via Domain Facebook, Instagram and Twitter • Facebook Instant Experience INVESTMENT: $35,200 GST inclusive Cancellation of any portion of the NSW Deluxe Package that occurs after the first insertion / appearance date of any of the products outlined in the booking agreement will be billed at the total cost of the package. NSW Deluxe Packages are subject to availability. Editorial inclusion is subject to Editor approval. Online and magazine advertising terms and conditions: domain.com.au/group/agent-centre. Rates are for single resale properties only at the discretion of Domain and are not available for multiple dwelling buildings, projects or developments. Prices are subject to change without notice. -

Fairfax Media Ltd (Fxj) 16 August 2017

FAIRFAX MEDIA LTD (FXJ) 16 AUGUST 2017 RESULTS Full Year 2017 Full Year 2016 CHANGE Revenue ($m) 1,742.7 1830.5 -4.8% Bloomberg consensus ($m) 1,725.0 Domain EBITDA ($m) 113.1 120.0 -5.7% EBITDA ($m) 271.1 283.3 -4.3% Bloomberg consensus ($m) 263.8 Net profit (loss) after tax ($m) 83.9 (772.6) n/a Final Dividend ($) 0.02 0.02 no change Fairfax (FXJ) plans to spin-off Domain and trading to start in November Media group, Fairfax (FXJ) has returned to profitability, posting an improved $83.9m full year profit for the 12 months to June 30 and provided details on its planned Domain IPO. While underlying earnings (not including significant items) went backwards over the year, EBITDA came in ahead of market expectations. The result follows more than $900m in write-downs of its publishing assets which held back its FY16 result. While Domain has been its star performer for some time, its print business has been coming under pressure due to a slide in advertising dollars and a systemic change in the way Australians consume their news. FXJ confirmed it plans to spin-off its best performing asset, Domain and for trading in the real estate classifieds business to begin in mid to late November. The group intends to retain 60% of Domain with the remaining 40% to be distributed to FXJ shareholders. The split is still conditional on shareholder and regulatory approvals (including ASIC, ASX and ATO). Investors can expect the scheme booklet (which outlines all details of the separation) in late September 2017. -

Submission to the Inquiry Into Broadcasting, Online Content and Live Production to Rural and Regional Australia

SUBMISSION TO THE INQUIRY INTO BROADCASTING, ONLINE CONTENT AND LIVE PRODUCTION TO RURAL AND REGIONAL AUSTRALIA The Hon Bronwyn Bishop MP Chair Standing Committee on Communications and the Arts PO Box 6021 Parliament House CANBERRA ACT 2600 By email: [email protected] Introduction Thank you for the opportunity to make a submission to the House of Representatives Standing Committee on Communications and the Arts inquiry into broadcasting, online content and live production to rural and regional Australia. This letter is on behalf of the three major regional television providers, Prime Media Group (Prime Media), the WIN Network (WIN) and Southern Cross Austereo (SCA). Prime Media and SCA are members of Free TV Australia, the television peak body which has also made a submission to this inquiry on behalf of the industry. Prime Media broadcasts in northern New South Wales, southern New South Wales, the Australian Capital Territory, regional Victoria, Mildura, the Gold Coast area of south eastern Queensland and all of regional Western Australia. WIN broadcasts in southern New South Wales, the Australian Capital Territory, regional Queensland, regional Victoria, Tasmania, Griffith, regional WA, Mildura, Riverland and Mt Gambier in South Australia. SCA broadcasts in northern New South Wales, southern New South Wales, Queensland, the Australian Capital Territory, Griffith, regional Victoria, Tasmania, the Northern Territory and the Spencer Gulf region of South Australia. Through affiliation agreements, Prime Media, WIN and SCA purchase almost all of their programming from metropolitan networks1 and using more than 500 transmission towers located across the country, retransmit that programming into regional television licence areas. -

Nine Network Australia Selects Intelsat to Distribute Domestic Television Programming

Nine Network Australia Selects Intelsat to Distribute Domestic Television Programming October 24, 2016 Intelsat will provide satellite connectivity and global fiber services via the IntelsatOne network to bring news content from around the world to Australia LUXEMBOURG--(BUSINESS WIRE)--Oct. 24, 2016-- Intelsat (NYSE: I), operator of the world’s first Globalized Network, powered by its leading satellite backbone, today announced a contract with Nine Network Australia to distribute programming to the company’s six domestic television stations as well as provide global satellite and fiber connectivity using the IntelsatOne terrestrial network to bring news content and special events from around the world to Australia for its network affiliates. Nine Network Australia (NNA) is one of the country’s top-rated commercial television networks, with local stations in Sydney, Melbourne, Brisbane, Adelaide, Perth and Darwin, along with a regional broadcaster, NBN. The network also has news bureaus in Canberra, London and Los Angeles. NNA is a subsidiary of Nine Entertainment Co., one of Australia’s leading media companies. Intelsat initially is providing services via the Australia/New Zealand Ku-Band beam on Intelsat 19 for the network’s broadcasting requirement. Under the agreement, Intelsat’s network support will extend well into the next decade. “Our Globalized Network allows us to meet NNA’s needs today and to increase our level of support if the network expands over time to meet the demands of multi-platform coverage,” said Terry Bleakley, Regional Vice President, Asia Pacific Sales, Intelsat. “NNA will also benefit from Intelsat’s global coverage for international contribution and distribution requirements.” NNA previously used Intelsat for its domestic and international occasional use requirements. -

Corporate Results Monitor

Corporate Results Monitor FNArena's All-Year Round Australian Corporate Results Monitor. Currently monitoring August 2019. TOTAL STOCKS: 272 Total Rating Upgrades: 61 Beats In Line Misses Total Rating Downgrades: 66 61 140 71 Simple average net target price change: 2.40% 22.4% 51.5% 26.1% Beat/Miss Ratio: 0.86 Latest Prev New Company Result Upgrades Downgrades Buy/Hold/Sell Brokers Target Target ABC - ADELAIDE BRIGHTON IN LINE 0 0 0/2/4 3.28 3.13 6 While Adelaide Brighton's result matched fresh guidance provided following a profit warning in July, it did still exceed most broker forecasts. FY20 guidance is bleak, given the housing construction downturn has as yet no end in sight and increased infrastructure construction is not sufficient to offset. The suspension of the dividend also came as no shock, but an intent to acquire and build out an integrated, infrastructure-oriented business model carries risk and reduces dividend prospects near-term. APT - AFTERPAY TOUCH BEAT 0 0 2/0/0 30.43 33.43 2 Afterpay Touch's FY19 net loss was slightly less than Morgans expected. The results suggest continuing strong sales momentum and stable margins across the business. Morgans downgrades FY20-21 earnings estimates, factoring in higher investment expenditure associated with offshore expansion. Traction in the US is strong but the key for Ord Minnett in the FY19 result were the initial customer acquisitions in the UK, which were well above expectations. Average merchant fees were slightly ahead of expectations, particularly in the US. AOG - AVEO IN LINE 0 1 0/2/0 2.15 2.15 2 Aveo Group's FY19 net profit was in line with recently downgraded guidance. -

2015 SWM Annual Report

ABN 91 053 480 845 Delivering the future of content. Anywhere. Any screen. Anytime. Annual Report 2015 Seven West Media cares about the environment. By printing 2000 copies of this Annual Report on ecoStar Silk and ecoStar Offset the environmental impact was reduced by*: 1,185kg 171kg 1,707km of landfill of CO2 and travel in the average greenhouse gases European car 26,982 2,486kWh 1,926kg litres of water of energy of wood Source: European BREF data (virgin fibre paper). Carbon footprint data evaluated by Labelia Conseil in accordance with the Bilan Carbone® methodology. Results are obtained according to technical information and are subject to modification. *compared to a non-recycled paper. Delivering the future of content. Anywhere. Any screen. Anytime. Annual Report 2015 Contents What We Do 4 The Future of Us 44 Our Brands 6 Board of Directors 46 Our Strategy 8 Corporate Governance Statement 49 Our Strategic Framework 10 Directors’ Report 60 Letter from the Chairman 12 Remuneration Report 64 Letter from the Managing Director & CEO 14 Auditor’s Independence Declaration 83 Performance Dashboard 16 Financial Statements 84 Performance of the Business 18 Directors’ Declaration 134 Group Performance 20 Independent Auditor’s Report 135 Television 26 Company Information 137 Newspapers 32 Investor Information 138 Magazines 36 Shareholder Information 139 Other Business and New Ventures 40 Risk, Environment and Social Responsibility 42 2 Seven West Media Annual Report 2015 ABN 91 053 480 845 Contents The right people creating great content across television, digital, mobile and newspaper and magazine publishing. Delivering the future of content 3 What We Do We are achieving growth in the delivery of our content across our portfolio of integrated media platforms. -

Asia Property Market Sentiment Report H2 2016

TABLE OF CONTENTS CEO’s Note………………………………………………………………….…….....2 Executive Summary…………………………………………...……………….……3 Methodology, Assumptions and Caveats………………………………………....4 Results Analysis, Asia Overview………………………………….…………….…5 Malaysia……………………………...……………………………………..….…….6 Demographics…………………………………..…..…………….….……..11 Sentiments………………………………………………...…………..…….30 Overseas Property……………………………..………………….………..47 Indonesia……………………………………………….………………………......59 Demographics……………………………………….………………..…....64 Sentiments…………………………………………………...……………..91 Overseas Property……………………………….…..….…………..…….95 Singapore………………………………………………………………………….102 Demographics…………………………………………………………….106 Sentiments………….……………………………………………………..131 Overseas Property ……………………………………………………….153 Hong Kong………………………………………………………………………...166 Demographics………………………………………………..……..….....169 Sentiments………………………………………………………………...182 Overseas Property…………………………………………………...…...202 Conclusion –Outlook for 2016 H2…………………….……………………...….214 1 CEO’S NOTE We are once again pleased to share with you the findings of our tenth iProperty.com Asia Property Market Sentiment Report. This survey report reveals sentiments for the second half of 2016 in all the countries the iProperty Group operates in. The survey was conducted over a month, from 5th July to 8th August 2016, across our market-leading network of property portals and gathered responses from 15,000 respondents. Similar to previous survey findings, affordability continues to remain a major concern in all the countries surveyed. This is just one of -

Annual Report 2020 Contents

Annual Report 2020 Contents Business Performance Overview 2 Chairman’s Report 4 CEO’s Report 6 Corporate Social Responsibility 10 Directors' Report 19 Remuneration Report 26 Corporate Governance Statement 45 Management Discussion and Analysis Report 59 Auditor’s Independence Declaration 62 2020 Financial Report 63 Shareholder Information 117 Corporate Directory 120 Inspiring confidence for all of life’s property decisions We are a leading property technology and services business that is home to one of the largest portfolios of property brands in Australia. Domain helps agents and consumers at every step in the property lifecycle – renting, buying, selling, investing, financing, insurance and utilities. The Domain Group is home to Domain, Allhomes, Commercial Real Estate, and CommercialView. Our portfolio also includes agent products Homepass, Pricefinder and Real Time Agent. Our consumer solutions products include Domain Loan Finder and Domain Insure. As a customer-centric property marketplace, we are committed to making the property journey easier, more enjoyable and connected at every stage. Annual Report 2020 1 Business Performance Overview Core Digital Residential by COVID-19’s impact on key advertising Residential generates revenue through categories in H2. The Developer market listings of ‘for sale’ and rental properties was impacted by the deferral of high rise across its desktop, mobile and social apartment projects resulting from lower platforms. Premium (depth) listing investor demand and COVID-19 impacts products account for the largest on immigration. Activity in smaller, proportion of revenue, with monthly boutique projects was stronger, however these require lower levels of marketing * subscriptions contributing the balance. $227.0m support. Commercial Real Estate (CRE) FY20 Revenue Residential revenue reduced 7%, a delivered solid revenue growth for the solid performance in an environment year. -

Annual Report to Shareholders

create distribute engage ifc The Year in Brief 2 Chairman’s Address 4 Chief Executive Officer’s Address 6 Divisional Results 8 Operational Review 16 Nine Cares create 17 Governance 18 Board of Directors 20 Directors’ Report distribute 25 Remuneration Report 44 Operating and Financial Review 48 Financial Report engage 108 Shareholder Information ibc Corporate Directory During FY17, Nine achieved its goal of turning the Network performance around, after a disappointing year in FY16. Momentum in Free To Air TV turned positive for Nine in Q2, and this improvement continued throughout the remainder of the financial year. The success of Nine’s broadcast content has, in turn, driven take-up and use of 9Now which has grown exponentially to over 4 million registered users, and is becoming a valuable contributor to the P&L. Nine’s Subscription Video on Demand platform Stan, has matured significantly over the past 12 months and now holds a clear number 2 position in the market. Nine’s digital publishing business has been successfully repositioned post the Microsoft relationship, laying the foundations for growth into the future. All of Nine’s businesses are built around the key content verticals of news, sport, lifestyle and entertainment. Result In Brief In FY17, on a revenue decline of 4%, Nine reported Group EBITDA of $206 million, up 2% on FY16. Driving this growth was an underlying cost decrease of 1%, and a reported cost decrease of 4% which included the Government regulated licence fee relief of $33 million. Net Profit after Tax increased by 3% to $123.6 million compared to the Pro Forma FY16 result. -

Weekly Audience Pack As at 19 May, 2020 Summary

Weekly Audience Pack As at 19 May, 2020 Summary Linear TV BVOD Digital & Publishing Radio The Nine Network continues to be the 9Now continues to be the leading This week the focus is on lifestyle Audiences continue to turn to Nine preferred primetime network for all key CFTA BVOD platform with a year-to- content with social restrictions being Radio for trusted voices and platforms demographics for the calendar year-to- date share of 48% in total minutes. lifted Australians are reconnecting with where they can share their date, with a 39.7% commercial share their love of travel content. opinions. The second GfK Radio Survey among P25-54. 9Now has experienced year-on- of 2020 has seen 2GB, 3AW, 4BC and year minutes growth for key Nine’s Traveller had double-digit week- 6PR post significant audience growth Engagement for the Nine Network is demographics include P25-54 (+33%) on-week growth in users (+44%), during the COVID-19 crisis. increasing year-on-year across all key and P18-39 (+34%). sessions (+46%) and page views (+43%). demographics. P25-54 are spending an Readers are also in travel planning Nine digital radio continues to see year- additional +2.78 minutes per day viewing As viewers continue to turn to mode, with week-on-week growth in on-year growth, with 4BC in Brisbane primetime content. entertainment for an escape during Traveller’s planning section across users delivering +17% in live streaming week- the current global pandemic, (+80%), sessions (+92%) and page views on-week. More listeners are tuning in The LEGO Masters season final viewers are choosing family favourite (+79%).