Financial System Policy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Digital Transformation Strategy

Digital Transformation Strategy September 11, 2017 Mitsubishi UFJ Financial Group, Inc. This document contains forward-looking statements in regard to forecasts, targets and plans of Mitsubishi UFJ Financial Group, Inc. (“MUFG”) and its group companies (collectively, “the group”). These forward-looking statements are based on information currently available to the group and are stated here on the basis of the outlook at the time that this document was produced. In addition, in producing these statements certain assumptions (premises) have been utilized. These statements and assumptions (premises) are subjective and may prove to be incorrect and may not be realized in the future. Underlying such circumstances are a large number of risks and uncertainties. Please see other disclosure and public filings made or will be made by MUFG and the other companies comprising the group, including the latest kessantanshin, financial reports, Japanese securities reports and annual reports, for additional information regarding such risks and uncertainties. The group has no obligation or intent to update any forward-looking statements contained in this document. In addition, information on companies and other entities outside the group that is recorded in this document has been obtained from publicly available information and other sources. The accuracy and appropriateness of that information has not been verified by the group and cannot be guaranteed. The financial information used in this document was prepared in accordance with Japanese GAAP (which includes Japanese managerial accounting standards), unless otherwise stated. Japanese GAAP and U.S. GAAP, differ in certain important respects. You should consult your own professional advisers for a more complete understanding of the differences between U.S. -

Strategies of the 77 Bank, Ltd Growth Strategy

Strategies of The 77 Bank, Ltd Growth Strategy Best Consulting Bank Human Resource Development In order to become a bank that is truly supported by its customers and to establish a solid management base for the future, we have set the image of the bank we aspire to become as the following, and actively trained specialist resources. Interview 01 “Best Consulting Bank” that responds to customersʼ needs by offering the optimum solutions Striving to solve the issues of quality assurance Corporate Support Department and manpower shortage on the front line of manufacturing. Kei Akama I was assigned to Tohoku Electronics Industry Co., Ltd. with Tohoku Electronics Industry has about 1,000 employees in the headquarters in Ishinomaki City, Miyagi Prefecture for one year entire group, I was forced to be keenly aware of the issue of the under the Local Company Trainee program that started in 2018. shortage of manpower at the manufacturing front line. I believe I was assigned to the Quality Assurance Department, where I that these valuable experiences as a trainee at a local company dealt with automobile manufacturers and interacted with manu- can be utilized in my current work. I am currently working in the facturing sites to ensure the quality of automobile-related parts. Corporate Support Office, providing support mainly to custom- I was interested in the manufacturing industry, including ers in the fishery processing industry in the coastal areas of the automobiles and machinery, and I thought I had acquired some prefecture that are still on the road to recovery from the Great prior knowledge before I was transferred to the company, but I East Japan Earthquake. -

Besta Besta: Banking

What is BeSTA? BeSTA is a standard banking application developed by NTT DATA. NTT DATA will meet a wide variety of needs from financial institutions in Japan through the utilization of BeSTA, which is developing each day. BeSTA: Banking application engine for STandard Architecture Vendor free Maintain competition Neutral application for unspecified hardware vendors principles Because of its high degree of flexibility, systems of other companies can Reduce procurement BeSTA be connected. cost Multiple banks Reduce development Multiple banks can use a single piece of software. cost Plenty of functions that respond to a large number of user requirements Shrink maintenance have already been installed. cost Advanced functions Save development Flexibility: Operational functions can be set and changed flexibly by setting efforts parameters. Enable efficient Expandability: The AP structure formed by the components allows the expansion system to be easily expanded in the future. No need for reconstructuring Promising future: Continuing updates by NTT DATA ensures long- term utilization. Copyright © 2017 NTT DATA Corporation 1 Expanding BeSTA network More than 50 banks are currently using or planning to use BeSTA, the core banking software developed by NTT DATA, and the network is the largest of its kind in Japan. Regional Bank Integrated STELLA CUBE Service Center (15 banks) (9 banks) Aomori Bank Senshu Ikeda Bank Tohoku Bank Kanagawa Bank AKITA BANK TOTTORI BANK Tokyo Tomin Bank Nagano Bank Bank of Iwate San-in Godo Bank TOYAMA BANK Sendai Bank Ashikaga Bank Shikoku Bank Tajima Bank Kirayaka Bank Chiba Kogyo Bank Oita Bank FUKUHO BANK NISHI-NIPPON Hokuetsu Bank CITY BANK Fukui Bank Aichi Bank MEJAR (5 banks) Bank of Kyoto Hokkaido Bank HOKURIKU BANK Bank of Yokohama 77 Bank BeSTAcloud (10 banks) Higashi-Nippon Bank FIDEA Holdings Hokuto Bank SHONAI BANK NEXTBASE (13 banks) Aozora Bank * BeSTA package provided from Hitachi, Ltd. -

Regional Banks in Japan 2008

Regional Banks in Japan 2008 We, the 64 regional banks in Japan, have for a long time enjoyed the patronage of the people of our regions as banks that move in step with the community. Hokkaido The Hokkaido Bank The regional banks as financial institutions that have the trust of their customers, will continue to contribute to the activation of regional societies through meeting various financial needs in the regions, by enhancing financial functions such as relationship- based banking. Aomori The Aomori Bank THE MICHINOKU BANK Akita Iwate THE AKITA BANK The Bank of Iwate The Hokuto Bank THE TOHOKU BANK Yamagata THE SHONAI BANK The Yamagata Bank Miyagi The 77 Bank Niigata The Daishi Bank Fukushima The Hokuetsu Bank The Toho Bank Ishikawa Toyama The Hokkoku Bank The Hokuriku Bank THE TOYAMA BANK Tochigi Gunma The Ashikaga Bank Tottori Fukui Nagano The Gunma Bank Ibaraki The Hachijuni Bank The Joyo Bank Shimane THE TOTTORI BANK The Fukui Bank Gifu The San-in Godo Bank Kyoto Saitama The Kanto Tsukuba Bank The Ogaki Kyoritsu Bank The Musashino Bank Hyogo The Bank of Kyoto The Juroku Bank Okayama The Tajima Bank Tokyo Shiga Hiroshima The Chugoku Bank The Tokyo Tomin Bank Fukuoka Yamaguchi The Hiroshima Bank Osaka THE SHIGA BANK Chiba THE BANK OF FUKUOKA The Yamaguchi Bank The Kinki Osaka Bank Aichi The Chikuho Bank The Senshu Bank The Chiba Bank THE NISHI-NIPPON CITY BANK Kagawa The Bank of Ikeda The Chiba Kogyo Bank Saga Ehime The Hyakujushi Bank Mie THE BANK OF SAGA Oita The Iyo Bank The Mie Bank Tokushima Nara THE OITA BANK The Hyakugo Bank -

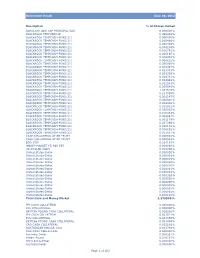

Retirement Funds June 30, 2012 Description % of Shares Owned

Retirement Funds June 30, 2012 Description % of Shares Owned BARCLAYS LOW CAP PRINCIPAL CAS 0.000000% BLACKROCK FEDFUND(30) 0.440244% BLACKROCK TEMPCASH-FUND(21) 0.000000% BLACKROCK TEMPCASH-FUND(21) 0.000486% BLACKROCK TEMPCASH-FUND(21) 0.000485% BLACKROCK TEMPCASH-FUND(21) 0.008246% BLACKROCK TEMPCASH-FUND(21) 0.006791% BLACKROCK TEMPCASH-FUND(21) 0.005165% BLACKROCK TEMPCASH-FUND(21) 0.006043% BLACKROCK TEMPCASH-FUND(21) 0.004035% BLACKROCK TEMPCASH-FUND(21) 0.035990% BLACKROCK TEMPCASH-FUND(21) 0.020497% BLACKROCK TEMPCASH-FUND(21) 0.023343% BLACKROCK TEMPCASH-FUND(21) 0.008326% BLACKROCK TEMPCASH-FUND(21) 0.000781% BLACKROCK TEMPCASH-FUND(21) 0.004848% BLACKROCK TEMPCASH-FUND(21) 0.022593% BLACKROCK TEMPCASH-FUND(21) 0.000646% BLACKROCK TEMPCASH-FUND(21) 1.307615% BLACKROCK TEMPCASH-FUND(21) 0.214356% BLACKROCK TEMPCASH-FUND(21) 0.001147% BLACKROCK TEMPCASH-FUND(21) 0.024810% BLACKROCK TEMPCASH-FUND(21) 0.009406% BLACKROCK TEMPCASH-FUND(21) 0.018922% BLACKROCK TEMPCASH-FUND(21) 0.030062% BLACKROCK TEMPCASH-FUND(21) 0.010464% BLACKROCK TEMPCASH-FUND(21) 0.004697% BLACKROCK TEMPCASH-FUND(21) 0.001179% BLACKROCK TEMPCASH-FUND(21) 0.007266% BLACKROCK TEMPCASH-FUND(21) 0.000112% BLACKROCK TEMPCASH-FUND(21) 0.008062% BLACKROCK TEMPCASH-FUND(21) 0.011657% CASH COLLATERAL AT BR TRUST 0.000001% CASH COLLATERAL AT BR TRUST 0.000584% EOD STIF 0.024153% MONEY MARKET FD FOR EBT 0.000000% US DOLLAR CASH 0.008786% United States-Dollar 0.000000% United States-Dollar 0.000003% United States-Dollar 0.000019% United States-Dollar 0.000003% United States-Dollar -

【Major Bank】都市銀行 【Local Bank】地方銀行 【Second Regional

【Major bank】都市銀行 Mizuho Bank / Sumitomo Mitsui Banking Corporation / Saitama Resona Bank Mitsubishi UFJ Bank / Resona Bank (5 in total) 【Local bank】地方銀行 Hokkaido Bank / Yamanashi Central Bank /Saningodo Bank Aomori Bank / Hachijuni Bank / Chugoku Bank Michinoku Bank / Hokuriku Bank /Hiroshima Bank Akita Bank / Toyama Bank / Yamaguchi Bank Hokuto Bank / Hokkoku Bank/ Awa Bank Shonai Bank / Fukui Bank/ Hyakujuyon Bank Yamagata Bank / Shizuoka Bank / Iyo Bank Iwate Bank / Suruga Bank/ Shikoku Bank Tohoku Bank / Shimizu Bank / Fukuoka Bank ShichijushichiBank / Ogaki Kyoritsu Bank / Chikuho Bank Toho Bank / Juroku Bank / Saga Bank Gunma Bank Mie Bank Juhachi Bank Ashikaga Bank / Hyakugo Bank / Shinwa Bank Joyo Bank / Shiga Bank Higo Bank Tsukuba Bank Kyoto Bank Oita Bank Musashino Bank / Kansai Mirai Bank / Miyazaki Bank Chiba Bank / IkedaSenshu Bank / Kagoshima Bank Chiba Kogyo Bank / Nanto Bank /Ryukyu Bank Yokohama Bank / Kiyo Bank / Okinawa Bank Daiyon Bank / Tajima Bank / Nishinihon City Bank HuKuetsu Bank / Tottori bank / Kitakyushu Bank (63 in total) 【Second Regional Bank Member Bank】第二地銀協加盟銀行 Hokuyo Bank Daiko Bank Shimane Bank Kirayaka Bank Nagano Bank Tomato Bank Kitanihon Bank Toyama Daiichi Bank Momiji Bank Sendai Bank Shizuokachuo Bank Saikyo Bank Fukushima Bank Aichi Bank Tokushima Bank Daito Bank Nagoya Bank Kagawa Bank Towa Bank Chukyo Bank Ehime Bank Tochigi Bank Daisan Bank Kochi Bank Tokyo Star Bank Taisho Bank Kumamoto Bank Kanagawa Bank Minato Bank (29 in total) 【Trust bank-Shintaku Ginko】信託銀行 Mitsubishi UFJ Trust Bank -

Outline of IWATE UNIVERSITY for International Students a Wide Variety of Research Topics, Made Possible by the Extensive Campus

Outline of I ATE UNIVERSITY for International Students Contact Information Support available in Japanese, English, Chinese, and Korean International Office YouTube 3-18-34 Ueda, Morioka-shi, Iwate 020-8550 Japan TEL+81-19-621-6057 / +81-19-621-6076 FAX+81-19-621-6290 E-mail: [email protected] Website Instagram Support available only in Japanese Topic Division/Office in Charge TEL E-mail General Administration and Public Relations About the university in general Division, General Administration Department 019-621-6006 [email protected] Admissions Office, About the entrance exam Student Services Department 019-621-6064 Student Support Division, Facebook About student life Student Services Department 019-621-6060 [email protected] About careers for students Career Support Division, INDEX after graduation Student Services Department 019-621-6709 [email protected] Graduation certificates for graduates and Student Services Division, 1. About Iwate University ………………………………… p.2 students who have completed their studies Student Services Department 019-621-6055 [email protected] 2. Undergraduate and Graduate Programs ………… p.4 3. Research Topics ………………………………………… p.14 Twitter 4. Types of International Students …………………… p.16 5. Support for International Students ……………… p.18 Website Iwate University Japanese English https://www.iwate-u.ac.jp/english/index.html 6. A Day in the Life of an International Student… p.20 Global Education Center Japanese English Chinese Korean https://www.iwate-u.ac.jp/iuic/ 7. Interviews with International Students ………… p.22 Researchers Database Japanese English http://univdb.iwate-u.ac.jp/openmain.jsp 8. Campus Calendar………………………………………… p.23 Questions related to the entrance exam Japanese https://www.iwate-u.ac.jp/admission/index.html WeChat (Chinese International Students Association) 9. -

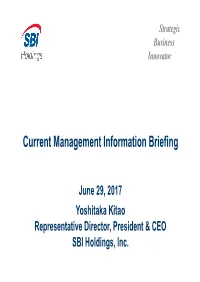

Current Management Information Briefing

Strategic Business Innovator Current Management Information Briefing June 29, 2017 Yoshitaka Kitao Representative Director, President & CEO SBI Holdings, Inc. The items in this document are provided as information related to the financial results and the business strategy of the SBI Group companies and not as an invitation to invest in the stock or securities issued by each company. None of the Group companies guarantees the completeness of this document in terms of information and future business strategy. The content of this document is subject to revision or cancellation without warning. Note: Fiscal Year (“FY”) ends March 31 of the following year 1 I. SBI Group’s Financial Results for the Past Five Years II. Various Measures for the Next Generation Based on the Changes in the Business Environment 2 I. SBI Group’s Financial Results for the Past Five Years 3 Consolidated Financial Results for the Past Five Fiscal Years (IFRS) [Revenue] Historical high (JPY billion) Financial Services Asset Management 261.7 261.9 Biotechnology-related 4.0 5.5 250 245.0 232.8 2.2 2.2 91.5 80.4 200 65.8 72.7 154.3 150 1.0 33.0 100 177.0 162.6 166.2 147.8 50 113.3 0 FY2012 FY2013 FY2014 FY2015 FY2016 * Abovementioned figures are before elimination of the inter-segment transactions. Also, since there are Group companies that have been transferred from one segment to an another, the abovementioned figures reflect disclosed figures during each fiscal year, therefore, there may be some discrepancies 4 Consolidated Financial Results for the Past Five Fiscal Years (IFRS) [Profit before income tax expense] (JPY billion) Financial Services Asset Management Biotechnology-related 78 63.1 8.1 52.2 68 43.1 58 17.6 13.9 48 38.9 9.0 38 67.3 28 15.0 50.8 48.9 6.3 18 37.3 8 18.7 -2 -7.3 -6.6 -3.9 -2.4 -9.6 -12 FY2012 FY2013 FY2014 FY2015 FY2016 * Abovementioned figures include profit or loss not allocated to specific business segments and inter-segment eliminations. -

Expanding Besta Network

Expanding BeSTA network More than 50 banks are currently using or planning to use BeSTA, core banking software developed by NTT DATA, and the network is the largest of its kind in Japan. Regional Bank Integrated Services Center (14 banks) STELLA CUBE (9 banks) Aomori Bank Bank of Kyoto Tohoku Bank Kanagawa Bank AKITA BANK Senshu Ikeda Bank Tokyo Tomin BankNagano Bank Bank of Iwate TOTTORI BANK TOYAMA BANK Sendai Bank Ashikaga Bank Shikoku Bank Tajima Bank Kirayaka Bank Chiba Kogyo BankOita Bank FUKUHO BANK Hokuetsu Bank NISHI-NIPPON CITY BANK Fukui Bank Aichi Bank MEJAR (5 banks) Hokkaido Bank HOKURIKU BANK BeSTAcloud (10 banks) Bank of Yokohama77 Bank FIDEA Holdings Higashi-Nippon Bank Hokuto Bank SHONAI BANK Aozora Bank NEXTBASE (13 banks) * BeSTA package provided SBK FUKUOKA CHUO BANK Saga Kyoei Bankfrom Hitachi, Ltd. BANK OF NAGASAKI Howa Bank Miyazaki Taiyo Bank MINAMI NIPPON BANK OKINAWA KAIHO BANK Copyright © 2015 NTT DATA Corporation 1 Collaboration concerning BeSTA® banking application and surrounding businesses By combining highly compatible solutions regardless of the frameworks of conventional core banking businesses or other banking businesses, the scope of businesses has been expanded. Ideas on collaboration concerning surrounding businesses are also broadly solicited. Scope expansion Regional Omichannel revitalization Individual-Number Successi BPO Business matching utilization on Payment Regional Cloud/virtualization FINTECH sophistication currency Channel Strategy ATM Branch terminal Business Assets in custody Market management Bank app DM Legal system Assets in custody Financial CRM Integrated DB (investment trust, Contact center Instruments and IFRS insurance) Exchange Act Sales support Financing support Internet banking AML BIS Mobile banking Backbone system (BeSTA) Copyright © 2015 NTT DATA Corporation 2 Priority areas of strategic IT investment Three areas to be studied intensively are operation, data accumulation/analysis, and utilization of external expertise. -

Nomura Report 2013 (PDF 4514KB)

Corporate Profile Nomura is a leading financial services group and the External Recognition preeminent Asia-based investment bank with a worldwide Nomura’s CSR initiatives and information disclosure reach. Our Retail, Asset Management and Wholesale practices have been widely recognized outside the company. Nomura Holdings has been selected for divisions provide a broad range of innovative, value-added inclusion in the Dow Jones Sustainability Indexes and the solutions tailored to the specific requirements of individual, FTSE4Good Index, both socially responsible investment institutional, corporate and government clients through an (SRI) indexes. Nomura was also selected as the only international network in over 30 countries around the world. financial services company recognized in the Japan 500 CDLI. Returning to Our Roots For over 80 years, we have continued to uphold our founder’s principles. One of these principles, “putting the customer first,” evolved into “prospering with our clients” and is now defined Involvement in External ESG Initiatives by our commitment to • UN PRI (Principles for Responsible Investment) “place clients at the heart of • Principles for Financial Action towards a Sustainable Society (Principles for Financial Action for the 21st Century) everything we do.” Although the words may change, • Multistakeholder Forum on Social Responsibility for a over unwavering focus on our clients remains the same. Sustainable Future • Banking Environment Initiative Editorial Policy In FY2011/12, we began publishing the Nomura Report, an Entities Covered integrated version of our annual report and our citizenship Nomura Holdings, Inc. and its major subsidiaries and affiliates. (http://www.nomuraholdings.com/company/group/) report, which detailed our CSR initiatives. -

India Sets High Target for GIC Re After Cool Trading Debuts for Local Insurers

IFRASIA INTERNATIONAL FINANCING REVIEW ASIA OCTOBER 7 2017 ISSUE 1012 www.ifrasia.com Qudian quickly covered as buyers flock to China’s biggest US fintech IPO India sets high target for GIC Re after cool trading debuts for local insurers South Korean issuers court debt investors after missile tests trigger heavy selling PLUS: QUARTERLY LEAGUE TABLES BONDS LOANS LOANS PEOPLE & MARKETS Samurai market NTPC breaks new SoftBank launches Chinese banks shrinks as swap ground in yen Asia’s largest retain top spots on costs deter high- market with first syndication to repay Asian investment rated issuers 10-year tenor acquisition debt banking fees 06 08 08 14 1012_00 Cover.indd 3 06/10/2017 21:46:20 WANT A GLOBAL PERSPECTIVE ON THE SYNDICATED LOAN MARKET? LOOK TO THOMSON REUTERS LPC Thomson Reuters LPC is the premier global provider of information on the syndicated loan and high yield bond markets. Our first-to-the-market news and comprehensive real-time and historical data help industry players stay informed about market trends and facilitate trading and investment decisions. LPC’s publications, end-of-day valuations, online news, analysis, and interactive databases are used every day by banks, asset managers, law firms, regulators, corporations and others to drive valuation, syndication, trading, research and portfolio management activities. CONNECT TO THE GLOBAL SYNDICATED LOAN MARKET WITH THOMSON REUTERS LPC. www.loanpricing.com [email protected] Upfront OPINION INTERNATIONAL FINANCING REVIEW ASIA Model of success Global banks have proven their value in 2017, and will be looking to build on their successes in 2018. -

Tokyo Stock Exchange Tokyo Stock Exchange

Tokyo Stock Exchange Annual Report 1998 Year Ended March 31, 1998 Profile or almost 120 years, the Tokyo Stock Exchange (TSE) has Fbeen recognized and functioned as Japan’s central stock market. Since its reestablishment in 1949, the TSE has responded positively to trading demands from both overseas and domestic investors, operating both cash and derivatives markets. Now, at the drawn of a new era in which the legal and system- atic framework created by the recent market reforms is taking shape, the TSE is endeavoring to construct and operate a highly efficient and competitive market that will allow it to play a major role in the economic life of Japan, Asia and the world. 3000 2500 2000 1500 CONTENTS Statistical Highlights.....................................3 1000 Message from the President..........................5 TSE Market System.......................................6 Special Feature............................................12 500 Financial Statements...................................14 Board of Governors and Auditors ..............17 List of Members and Special Participants ...20 1970 7172 73 74 75 Statistical Highlights At December 31 1997 1996 1995 (STOCK MARKET) Listed Companies : Domestic .................................................. 1,805 1,766 1,714 : Foreign ..................................................... 60 67 77 Newly Listed Companies : Domestic .................................................. 50 59 32 : Foreign ..................................................... 1 20 Market Value (¥ billions) : Domestic