EBA CLEARING Shareholders Meeting Report of the Board 14 Th June 2011 Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Elenco Collocatori Robeco Capital Growth Fund

ROBECO CAPITAL GROWTH FUNDS Società d’Investimento a Capitale Variabile – SICAV ELENCO DEI SOGGETTI INCARICATI DEL COLLOCAMENTO IN ITALIA Denominazione Soggetto Collocatore Classi Collocate Soggetto incaricato dei pagamenti Alpenbank AG Filiale Bolzano** D, DH, B, BH, E, EH Allfunds Bank S.A. Milan Branch Alto Adige Banca S.p.A.** D, DH, B, BH, E, EH Allfunds Bank S.A. Milan Branch Azimut Capital Management SGR S.p.a** D, DH, B, BH, E, EH Allfunds Bank S.A. Milan Branch Banca Aletti S.p.A.** D, DH, B, BH, E, EH Allfunds Bank S.A. Milan Branch Banca CARIGE S.p.A.** D, DH, B, BH, E, EH Allfunds Bank S.A. Milan Branch Banca Cesare Ponti S.p.A.** D, DH, B, BH, E, EH Allfunds Bank S.A. Milan Branch Banca del Monte di Lucca S.p.A.** D, DH, B, BH, E, EH Allfunds Bank S.A. Milan Branch Banca di Pisa e Fornacette S.C.P.A.** D, DH, B, BH, E, EH Allfunds Bank S.A. Milan Branch Banca Finnat Euramerica S.p.A** D, DH, B, BH, E, EH Allfunds Bank S.A. Milan Branch Banca Generali S.p.A.** D, DH, B, BH, E, EH Allfunds Bank S.A. Milan Branch Banca Ifigest S.p.A. D, DH, B, BH, E, EH Société Générale Securities Services S.p.A. Banca Leonardo S.p.A.* D, DH, B, BH, E, EH BNP Paribas Securities Services Banca Nazionale del Lavoro S.p.A. D, DH, B, BH, E, EH BNP Paribas Securities Services Banca Popolare del Lazio S.c.p.A.** D, DH, B, BH, E, EH Allfunds Bank S.A. -

Fitch Places 31 EMEA Bank ST Issuer Ratings Under Criteria Observation

5/7/2019 [ Press Release ] Fitch Places 31 EMEA Bank ST Issuer Ratings Under Criteria Observation Fitch Places 31 EMEA Bank ST Issuer Ratings Under Criteria Observation Fitch Ratings-London-07 May 2019: Fitch Ratings has placed 31 Short-Term (ST) Issuer Default Ratings (IDR) and related ST debt level ratings of EMEA-based banks Under Criteria Observation (UCO) following the publication of its cross-sector criteria for Short-Term Ratings on 2 May 2019. A full list of rating actions is below. Fitch intends to conclude full implementation of the criteria, and resolution of all UCO designations within six months of the designation. KEY RATING DRIVERS The ST ratings of the affected banks are determined primarily by correspondence tables linking short-term to long-term ratings. The new ST rating criteria introduced changes to our correspondence table between long-term and ST ratings. Two new cusp points at 'A' and 'BBB+' have been added to the existing three cusp points ('A+', 'A-' and 'BBB'), where baseline or higher ST ratings can be assigned. For banks with Long-Term IDRs driven by their standalone profile, as reflected by their Viability Ratings (VR), Fitch uses the funding and liquidity factor score as the principal determinant of whether the 'baseline' or 'higher' ST IDR is assigned at each cusp point. The ST IDRs and, where relevant, associated ST debt/deposit ratings of the following issuers have been placed UCO because the ratings could be upgraded by one notch under the new criteria. This is because the latest funding and liquidity scores that feed into their VRs are at least in line with the minimum levels required for a higher ST rating under the new criteria: - Banco Cooperativo Espanol, S.A. -

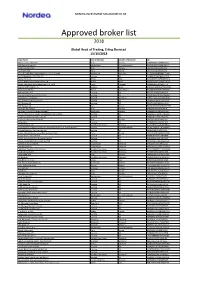

External Borkers List

NORDEA INVESTMENT MANAGEMENT AB Approved broker list 2018 Global Head of Trading, Erling Skorstad 15/10/2018 Legal Name City of Domicile Country of Domicile LEI ABG Sundal Collier ASA Oslo Norway 2138005DRCU66B8BNY04 ABN Amro Group NV Amsterdam The Netherlands BFXS5XCH7N0Y05NIXW11 Arctic Securities AS Oslo Norway 5967007LIEEXZX4RVS72 Aurel BGC SAS Paris France 5RJTDGZG4559ESIYLD31 Australia and New Zealand Banking Group Limited Melbourne Australia JHE42UYNWWTJB8YTTU19 AUTONOMOUS RESEARCH LLP London UK 213800LBM6PT85IGM996 Banca IMI S.p.A Milan Italy QV4Q8OGJ7OA6PA8SCM14 Banco Bilbao Vizcaya Argentaria S.A Bilbao Spain K8MS7FD7N5Z2WQ51AZ71 Banco Português de Investimento, S.A. (BPI) Porto Portugal 213800NGLJLXOSRPK774 BANCO SANTANDER S.A Madrid Spain 5493006QMFDDMYWIAM13 Bank Vontobel AG Zurich Switzerland 549300L7V4MGECYRM576 Barclays Bank PLC London UK G5GSEF7VJP5I7OUK5573 Barclays Capital Securities Limited London UK K9WDOH4D2PYBSLSOB484 Bayerische Landesbank Munich Germany VDYMYTQGZZ6DU0912C88 BCS Prime Brokerage Limited London UK 213800UU8AHE2B6QUI26 BGC Brokers LP London UK ZWNFQ48RUL8VJZ2AIC12 BNP Paribas SA Paris France R0MUWSFPU8MPRO8K5P83 Carnegie AS Norway Oslo Norway 5967007LIEEXZX57BC18 Carnegie Investment Bank AB (publ) Stockholm Sweden 529900BR5NZNQZEVQ417 China International Capital Corporation (UK) Limited London UK 213800STG3UV87MDGA96 Citigroup Global Markets Limited London UK XKZZ2JZF41MRHTR1V493 Clarksons Platou Securities AS Oslo Norway 5967007LIEEXZXA40G44 CLSA (UK) London UK 213800VZMAGVIU2IJA72 Commerzbank AG Frankfurt -

Nota Per Il Direttore Generale

PRESS RELEASE Fintech, ABI: Italian banks are working on blockchain pilot A first group of Italian banks has begun operative testing of a blockchain. Shortly, after an initial test phase, the pilot will be extended to a larger number of banks. ABI Lab, the technological laboratory supported by the Italian Banking Association (ABI), and the banks that are participating in the project are engaged in applying blockchain technology to interbank processes with the objective of attaining the benefits derived from data transparency and visibility, the increased speed in executing transactions and the possibility of performing checks and exchanges directly within the application. Blockchain technology allows for the creation and management of a large distributed database for managing transactions that can be shared across multiple nodes of a network. In other words, it is a database in which data is not stored on a single computer, but on multiple computers, called nodes, that are connected to one another. Without having to rely on a single centralised entity, this new concept of distributed databases, Distributed Ledger Technology (DLT), changes the way we think and design the relationships and the exchange of value between the participants. The scope of application is interbank reconciliation, which verifies the matching of correspondent accounts that involve two different banks that contain transactions executed between two customers of two banks. The project has also verified how the application of DLT technology can improve certain specific aspects of current operations that can result in discrepancies that are difficult for the banks to manage. Among these is the time needed to identify transactions between banks that do not match; the lack of a standard process and a single communications protocol; the limited visibility of the transactions between parties. -

Report of the Board Annual General Meeting 12Th June 2014 Contents

Report of the Board Annual General Meeting 12th June 2014 Contents Executive Summary 3 1. Report on EBA Activities in 2013 and outlook for 2014+ 5 1.1 Report on work streams 5 1.2 Marketing and communications 8 1.3 Changes in the Board of the Association 9 1.4 Changes in EBA membership 11 1.5 Outlook for 2014+ 11 2. Financial situation, P&L statement as of 31st December 2013 17 2.1 Overall expenses incurred in 2013 17 2.2 Revenues in 2013 18 2.3 Income tax and results for 2013 20 2.4 EBA budget for 2014 20 2.5 Projected revenues for 2014 21 Appendix 1: 23 Accounts as of 31st December 2013 23 Appendix 2: 24 List of EBA Full Members 24 List of EBA User Members 26 List of EBA Associate Members 29 layout: www.quadratpunkt.de photo credit: © fotolia.com / Julien Eichinger 2 Euro Banking Association ANNUAL GENERAL MEETING // 12th June 2014 // Report of the Board Executive Summary As a community of like-minded European payment practitioners, EBA continued to capture the demands of its members and the wider payments industry throughout 2013. The activities undertaken in pursuit of the overarching strategy for the Association evolved during the year to reflect changing market realities. The EBA has a very simple set of objectives. To serve its members by delivering value in three strategic pillars, each designed to deliver benefits to their wholesale and retail payment divisions. Each strategic pillar is reflective of specific work initiatives. 1. Thought Leadership – to help members develop policies, strategies and roadmaps for rapid and complex payments change. -

Press Release Fitch Has Downgraded the Long Term

PRESS RELEASE FITCH HAS DOWNGRADED THE LONG TERM ISSUER DEFAULT RATINGS OF CREDITO VALTELLINESE AND THE SUBSIDIARY CREDITO ARTIGIANO FROM BBB TO BB+ OUTLOOK NEGATIVE Sondrio, 29 August 2012. Fitch Ratings has downgraded the Long-term Issuer Default Ratings (IDR) of Credito Valtellinese and its subsidiary Credito Artigiano as follows: LONG TERM IDR: form (BBB) to (BB+); Outlook Negative SHORT TERM IDR: from F3 to B VIABILITY RATING: from (bbb) to (bb+). The rating actions follow a periodic review of several mid-sized banking groups. The Negative Outlook on the banks’ Long-term IDRs reflects the pressure arising from the current challenges in the operating environment. The full text of Fitch Ratings press release follows. Company contacts Investor relations Media relations telephone + 39 02 80637471 telephone + 39 02 80637403 Email: [email protected] Email: [email protected] FITCH DOWNGRADES 7 ITALIAN MID-SIZED BANKS; AFFIRMS 2 Fitch Ratings-Milan/London-28 August 2012: Fitch Ratings has downgraded the Long-term Issuer Default Ratings (IDR) of Banca Popolare di Sondrio (BPSondrio) and Banco di Desio e della Brianza (BDB) to 'BBB+' from 'A-', and the Long-term IDR of Banca Popolare di Milano (BPMilano) to 'BBB-' from 'BBB'. The agency has also downgraded the Long-term IDRs of Banca Carige, Banca Popolare di Vicenza (BPVicenza), Credito Valtellinese (CreVal) and Veneto Banca to 'BB+' from 'BBB'. Simultaneously, Fitch has affirmed the Long-term IDRs of Banca Popolare dell'Emilia Romagna (BPER) at 'BBB' and of Credito Emiliano (Credem) at 'BBB+'. The Outlooks on all the banks' Long-term IDRs is Negative. A full list of rating actions is at the end of this rating action commentary. -

CREDITO VALTELLINESE S.P.A

BASE PROSPECTUS CREDITO VALTELLINESE S.p.A. (incorporated with limited liability under the laws of the Republic of Italy) €5,000,000,000 Euro Medium Term Note Programme Under the €5,000,000,000 Euro Medium Term Note Programme (the "Programme") described in this Base Prospectus, Credito Valtellinese S.p.A. ("Credito Valtellinese" or the "Issuer") may from time to time issue certain non-equity securities in bearer form, denominated in any currency and governed by English Law (the "English Law Notes") or by Italian Law (the "Italian Law Notes", and together with the English Law Notes, the "Notes"), as described in further detail herein. The terms and conditions for the English Law Notes are set out herein in “Terms and Conditions for the English Law Notes” and the terms and conditions for the Italian Law Notes are set out herein in “Terms and Conditions for the Italian Law Notes”. References to the “Notes” shall be to the English Law Notes and/or the Italian Law Notes, as appropriate and references to the “Terms and Conditions” or the “Conditions” shall be to the Terms and Conditions for the English Law Notes and/or the Terms and Conditions for the Italian Law Notes, as appropriate. For the avoidance of doubt, in “Terms and Conditions for the English Law Notes”, references to the “Notes” shall be to the English Law Notes, and in “Terms and Conditions for the Italian Law Notes”, references to the “Notes” shall be to the Italian Law Notes. This Base Prospectus has been approved by the Commission de Surveillance du Secteur Financier (the "CSSF") in its capacity as competent authority in Luxembourg as a base prospectus under article 8 of Regulation (EU) 2017/1129, as amended (the "Prospectus Regulation"). -

Semi-Annual Italian NPL Performance Report: 60% Of

28 July 2021 Structured Finance Semi-annual Italian NPL performance report: sector will under-perform into the medium term Semi-annual Italian NPL performance report: sector will under-perform into the medium term Italian NPL collection volumes look to be stabilising at 25% below average pre-pandemic levels. Performance has deteriorated slightly Analysts since Scope’s last report: 60% of transactions were performing below servicers’ original expectations in the second quarter of 2021, Rossella Ghidoni against 56% previously (based on Q3 2020 data1). The outlook is weak and risks remain to the downside. +39 02 94758 746 Indeed, weakness in the underlying market is reflected by the NPL Performance Index. The NPI, which tracks cumulative collections against [email protected] servicers’ original projections, stands at 94 and Scope expects it to remain below the baseline of 100 into the medium term. Meanwhile, notes are Paula Lichtensztein expected to amortise in six to eight years, based on the Scope NPL Dynamic Coverage Index (SCI), which tracks the speed of note amortisation. +49 30 27891 224 [email protected] The share of positions closed by servicers remains low and on those positions that have closed, median profitability has been 87%, below Scope expectations at closing. Vittorio Maniscalco +39 02 94758 456 Scope believes the Italian NPL sector will continue to under-perform into the medium term as the consequences of the pandemic have not yet worked [email protected] themselves through the economy. By the fourth quarter of 2021, Scope estimates that the share of transactions with collection volumes lagging Antonio Casado servicers’ forecasts will align with second quarter 2021 figures. -

Prospetto Informativo

PROSPETTO INFORMATIVO Relativo all’offerta in opzione agli azionisti di massimo n. 330.600 azioni ordinarie della Banca Popolare Sant’Angelo S.c.p.A. (con “Bonus Share”) e successiva offerta ai terzi delle eventuali azioni rimaste inoptate Emittente e soggetto incaricato della raccolta delle sottoscrizioni: Banca Popolare Sant’Angelo S.c.p.A. Prospetto informativo depositato presso la CONSOB in data 28/09/2009 in conformità alla nota di comunicazione dell’avvenuto rilascio dell’autorizzazione da parte della CONSOB stessa del giorno 22/09/2009 prot. n. 9083160 e messo a disposizione del pubblico presso: • la sede sociale della Banca Popolare Sant’Angelo S.c.p.A. in Corso Vittorio Emanuele 10, 92027 Licata; • tutti gli sportelli della Banca Popolare Sant’Angelo S.c.p.A.; • il sito Internet www.bancasantangelo.com. L’adempimento di pubblicazione del presente Prospetto Informativo non comporta alcun giudizio della CONSOB sull’opportunità dell’investimento proposto e sul merito dei dati e delle notizie allo stesso relativi. Prospetto Informativo Banca Popolare Sant’Angelo S.c.p.A. AVVERTENZA Le Azioni oggetto dell’Offerta presentano gli elementi di rischio propri di un investimento in strumenti finanziari non quotati in un mercato regolamentato, per i quali potrebbero insorgere difficoltà di disinvestimento. Per difficoltà di disinvestimento si intende che i sottoscrittori potrebbero avere difficoltà nel negoziare gli strumenti finanziari oggetto della presente Offerta, in quanto le richieste di vendita potrebbero non trovare adeguate contropartite. 1 Prospetto Informativo Banca Popolare Sant’Angelo S.c.p.A. INDICE GLOSSARIO DELLE PRINCIPALI DEFINIZIONI ........................................................................................ 7 NOTA DI SINTESI ......................................................................................................................................... 9 Avvertenze ................................................................................................................................................... 9 A. -

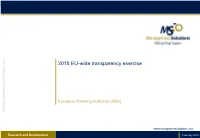

2018 EU-Wide Transparency Exercise

2018 EU-wide transparency exercise European Banking Authority (EBA) © Management Solutions 2019. All reserved All rights Solutions 2019. Management© www.managementsolutions.com Research and Development © Management Solutions 2019. Todos los derechos reservadosFebruary Página 2019 1 Index Introduction Aggregated results Results per country Outlook and recommendations Annex © Management Solutions 2019. All rights reserved Page 2 Introduction Context and objective In December 2018 the EBA published the results of the 2018 EU-wide transparency exercise, which provide detailed information on, among others, capital, leverage, risk weighted assets (RWA), P&L, credit risk, market risk, or asset quality Introduction • The EBA has been conducting transparency exercises at the EU-wide level on an annual basis since 2011. These exercises are part of the EBA's ongoing efforts to foster transparency and market discipline in the EU financial market, and complements banks' own Pillar 3 disclosures, as laid down in the CRD IV. • Further, the transparency exercises are, unlike the stress tests, disclosure exercises where only bank-by-bank data are published and no shocks are applied to the actual data. • In this context, the EBA has published the results of the EU-wide 2018 transparency exercise1, which will facilitate the consistent comparison and assessment of the resilience of banks across time and at a country and a bank-by-bank level. In particular, this document assesses the results relative to the potential impact on: • Capital (CET1 phase-in and -

Monte Titoli

Monte Titoli PARTECIPANTI AL SERVIZIO DI RISCONTRO E RETTIFICA GIORNALIERO X-TRM - 30 settembre 2014 PARTICIPANTS IN THE X-TRM - DAILY MATCHING AND ROUTING SERVICE - 30 th September 2014 CODICE CED CODICE ABI DESCRIZIONE ANAGRAFICA INTERMEDIARIO PARTECIPANTE CED CODE ABI CODE INTERMEDIARY 2331 1003 BANCA D'ITALIA 425 1005 BANCA NAZIONALE DEL LAVORO SPA 339 1010 SANPAOLO BANCO DI NAPOLI 382 1015 BANCO DI SARDEGNA SPA 3319 1025 INTESA SANPAOLO SPA 357 1030 BANCA MONTE DEI PASCHI DI SIENA SPA 1550 2008 UNICREDIT BANCA SPA 564 3011 HIPO ALPE ADRIA BANK SPA 2187 3015 BANCA FINECO SPA 2470 3017 INVEST BANCA SPA 2281 3025 BANCA PROFILO SPA 8664 3030 DEXIA CREDIOP SPA 302 3032 CREDITO EMILIANO SPA 7504 3041 UBS (ITALIA) SPA 4197 3043 BANCA INTERMOBILIARE INV. GESTIONI SPA 1994 3045 BANCA AKROS SPA 3301 3048 BANCA DEL PIEMONTE SPA 303 3051 BARCLAYS BANK PLC 3892 3058 CHEBANCA! 3049 3059 BANCA CIS SPA 1740 3062 BANCA MEDIOLANUM SPA 1105 3069 INTESA SANPAOLO SPA 547 3075 BANCA GENERALI SPA 4690 3081 UNICREDIT BANK AG 644 3084 BANCA CESARE PONTI SPA 560 3087 BANCA FINNAT EURAMERICA SPA 5937 3089 CREDIT SUISSE (ITALY) SPA 580 3102 BANCA ALETTI E C. SPA 308 3104 DEUTSCHE BANK SPA 315 3111 UNIONE DI BANCHE ITALIANE SCPA 2657 3124 BANCA DEL FUCINO SPA 1050 3126 GRUPPO BANCA LEONARDO SPA 3964 3127 UNIPOL BANCA SPA 1210 3138 BANCA REALE 3768 3141 BANCA DI TREVISO S.p.A. 3636 3151 HYPO TIROL BANK AG SUCCURSALE ITALIA 1862 3158 BANCA SISTEMA SPA 1847 3162 MORGAN STANLEY BANK INTERNATIONAL LIMITED - MILAN BRANCH 1770 3163 STATE STREET BANK S.p.A. -

Elenco Dei Soggetti Richiedenti Che Operano Con Il Fondo, Con Specifica

Elenco dei soggetti richiedenti che operano con il Fondo – account abilitati all’utilizzo della procedura telematica - Ottobre 2020 (informativa ai sensi del Piano della Trasparenza - parte X delle Disposizioni operative) DENOMINAZIONE SOGGETTO RICHIEDENTE COGNOME NOME E-MAIL TELEFONO AAREAL BANK MAZZA ANTONIO [email protected] 0683004228 AAREAL BANK CIPOLLONE LORELLA [email protected] 0683004305 AGFA FINANCE ITALY SPA CRIPPA ANTONELLA [email protected] 023074648 AGFA FINANCE ITALY SPA BUSTI FILIPPO [email protected] AGRIFIDI ZAPPA GIUSEPPE [email protected] 3371066673 AGRIFIDI EMILIA ROMAGNA TEDESCHI CARLO ALBERTO [email protected] 05211756120 AGRIFIDI MODENA REGGIO FERRARA TINCANI ENNIO EMANUELE [email protected] 059208524 AGRIFIDI UNO EMILIA ROMAGNA EVANGELISTI CARLOTTA [email protected] 0544271787 AGRIFIDI UNO EMILIA ROMAGNA MONTI LUCA [email protected] 0544271787 A-LEASING SPA LOMBARDO CLAUDIO [email protected] 0422409820 ALLIANZ BANK FINANCIAL ADVISORS PISTARINO FRANCA [email protected] 0131035420 ALLIANZ BANK FINANCIAL ADVISORS CORIGLIANO FABIO [email protected] 0272168085 ALLIANZ BANK FINANCIAL ADVISORS CHIARI STEFANO [email protected] 0272168518 ALLIANZ BANK FINANCIAL ADVISORS CANNIZZARO FEDERICO [email protected] 3421650350 ALLIANZ BANK FINANCIAL ADVISORS KOFLER SAMUEL [email protected] 3466001059 ALLIANZ BANK FINANCIAL ADVISORS FERRARI PIERO [email protected] 3477704188 ALLIANZ