The Assessment of Bermuda's National Money Laundering

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Telecommunications Amendment Act 2010

Q UO N T FA R U T A F E BERMUDA TELECOMMUNICATIONS AMENDMENT ACT 2010 2010 : 34 TABLE OF CONTENTS 1 Citation 2 Inserts new Part IVA 3 Amends section 40 4 Inserts sections 43A to 43C 4A Amends section 53 4B Amends section 54 5 Amends section 59 6 Transitional provision 7 Consequential amendment 8 Commencement WHEREAS it is expedient to amend the Telecommunications Act 1986 to require Carriers providing public telecommunications services to assist the Police in carrying out electronic surveillance and in intercepting communications for law enforcement purposes; Be it enacted by The Queen’s Most Excellent Majesty, by and with the advice and consent of the Senate and the House of Assembly of Bermuda, and by the authority of the same, as follows: Citation 1 This Act, which amends the Telecommunications Act 1986 (the “principal Act”), may be cited as the Telecommunications Amendment Act 2010. Inserts new Part IVA 2 The principal Act is amended by inserting immediately after Part IV the following— 1 TELECOMMUNICATIONS AMENDMENT ACT 2010 “PART IVA COMMUNICATIONS ASSISTANCE FOR LAW ENFORCEMENT Definitions 28C In this Part— “call-identifying information” means dialing or signalling information that identifies the origin, date, time, size, duration, direction, destination or termination of each communication generated or received by a subscriber by means of any telecommunication apparatus, facility or service of a Carrier; “commercial mobile service” means any mobile telecommunication service that is provided for profit and makes interconnected -

Equity Markets USD 47 Tn

19 January 2012 2011 WFE Market Highlights 2011 equity volumes remained stable despite a fall in market capitalization. Derivatives, bonds, ETFs, and securitized derivatives continued to grow strongly. Total turnover value remained stable in 2011 at USD 63 tn despite a sharp decrease of the global market capitalization (-13.6% at USD 47 tn). High volatility and global uncertainty created from the sovereign debt crisis affected volumes all year through and made August 2011 the most active month in terms of trading value, a highly unusual annual peak for markets. Despite overall unfavorable conditions for primary markets in several regions, WFE members increased their total listings by 1.7% totaling 45 953 companies listed. Total number of trades decreased by 6.4% at 112 tn. This trend combined with the stability of turnover value led to a small increase in the average size of transaction which was USD 8 700 in 2011. The high volatility and lack of confidence that affected financial markets globally probably drove the needs of hedging as derivatives contracts traded grew by 8.9%. WFE members continued to diversify their products range as other products such as bonds, ETFs, and securitized derivatives all had solid growth in 2011. Equity Markets Market capitalization USD 47 tn -13.6% Domestic market capitalization declined significantly in 2011 to USD 47 401 bn roughly back to the same level of end 2009. The decline affected almost all WFE members, as there were only four exchanges ending 2011 with a higher market capitalization. The magnitude of the decline is quite similar among the three time zones: -15.9% in Asia-Pacific, -15.2% in EAME and -10.8% in the Americas. -

United States Securities and Exchange Commission Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2019 OR o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number 001-36169 BLUE CAPITAL REINSURANCE HOLDINGS LTD. (Exact name of registrant as specified in its charter) Bermuda 98-1120002 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) Waterloo House 100 Pitts Bay Road Pembroke, Bermuda HM 08 (Address of principal executive offices) Registrant’s telephone number, including area code: (441) 278-0400 Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading symbol(s) Name of each exchange on which registered Common Shares, par value $1.00 per share BCRH New York Stock Exchange Common Shares, par value $1.00 per share BCRH.BH Bermuda Stock Exchange Securities registered pursuant to Section 12(g) of the Act None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ☒ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ☒ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, DC 20549

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 8-K CURRENT REPORT Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of Report (Date of earliest event reported): March 9, 2020 BLUE CAPITAL REINSURANCE HOLDINGS LTD. (Exact Name of Registrant as Specified in Its Charter) Bermuda 001-36169 98-1120002 (State or Other Jurisdiction of (Commission (I.R.S. Employer Incorporation or Organization) File Number) Identification No.) Waterloo House 100 Pitts Bay Road Pembroke HM 08 Bermuda (Address of Principal Executive Offices) Registrant’s telephone number, including area code: (441) 278-0400 Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: ☐ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ☐ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) ☐ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ☐ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Securities registered pursuant to Section 12(b) of the Act: Trading Name of each exchange Title of each class symbol(s) on which registered Common Shares, par value $1.00 per share BCRH New York Stock Exchange Common Shares, par value $1.00 per share BCRH.BH Bermuda Stock Exchange Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter). -

General Assembly 1 June 1998

United Nations A/AC.109/2109 Distr.: General General Assembly 1 June 1998 Original: English Special Committee on the Situation with regard to the Implementation of the Declaration on the Granting of Independence to Colonial Countries and Peoples Bermuda Working paper prepared by the Secretariat Contents Paragraphs Page I. General .................................................................. 1–3 3 II. Constitutional and political developments .................................... 4–11 3 A. General ............................................................. 4–9 3 B. Political parties and elections ......................................... 10–11 3 III. Activities related to the withdrawal of military bases .......................... 12–15 3 IV. Economic conditions ...................................................... 16–47 4 A. General ............................................................. 16–21 4 B. Public finance ....................................................... 22–27 5 C. Banking ............................................................ 28–30 5 D. International business ................................................ 31–36 5 E. Transport and communications ........................................ 37–39 6 F. Tourism ............................................................ 40–47 6 V. Social conditions .......................................................... 48–56 7 A. Race relations ....................................................... 48–49 7 B. Labour ............................................................ -

Annual Report 2020 the Bank of N.T

ANNUAL REPORT 2020 THE BANK OF N.T. BUTTERFIELD & SON LIMITED ANNUAL REPORT 2020 REPORT ANNUAL Banking, trust, investments, by . Established as Bermuda’s first bank in 1858, Butterfield today offers a range of community banking and bespoke financial services from eight leading international financial centers, supported by centralized service centers in Canada and Mauritius. The Butterfield team comprises 1,314 employees working together to help our clients manage their wealth and protect it for future generations, while creating sustainable, long-term value for our shareholders. Vision Mission To be the leading independent offshore bank To build relationships and wealth. and trust company. Values APPROACHABLE COLLABORATIVE EMPOWERED IMPACTFUL We commit to We collaborate for We foster We celebrate personal service. effective teamwork. individual initiative. collective success. Locations The Bahamas Bermuda Jersey United Kingdom Cayman Islands Canada* Switzerland Mauritius* Singapore Guernsey *Non-client-facing service center. Results Core Net Income* (millions) Core Return on Average Tangible Total Assets (millions) $250 Common Equity* 30.0% $16,000 $13,922 $14,739 $197.0 $197.9 25.6% $14,000 $200 25.0% 22.4% 23.4% 20.5% $12,000 $11,103 $10,779 $10,773 $158.9 $154.5 20.0% $150 17.3% $10,000 $123.0 15.0% $8,000 $100 $6,000 10.0% $4,000 $50 5.0% $2,000 2016 2017 2018 2019 2020 2016 2017 2018 2019 2020 2016 2017 2018 2019 2020 Capital** 25.0% 22.4% 19.9% 19.6% 19.6% 19.8% 20.0% 19.4% 17.6% 18.2% 18.2% 17.3% 17.3% 16.1% 16.1% 15.3% 15.3% 15.0% -

Budget Statement in Support of the Estimates of Revenue and Expenditure 2006-2007. Presented By

BUDGET STATEMENT IN SUPPORT OF THE ESTIMATES OF REVENUE AND EXPENDITURE 2006/07 Presented by The Hon. Paula A. Cox, J.P., M.P. Minister of Finance To His Honour the Speaker and Members of the Honourable House of Assembly Mr. Speaker, Our objective is to build a strong economy and a fair society where there is opportunity and security for all. Our goal is to make the economy work for the people of Bermuda – consumers and business alike in a way that operates fairly and that benefits our young people and seniors. The National Budget 2006/07 ushers in a new wave – an ‘Age of Empowerment’, as we look to a better future. In every single year between 1998 and 2005, the Progressive Labour Party Government has framed economic and financial policies that have delivered positive GDP growth to the Bermuda economy for the benefit of Bermudians and residents alike. While we do not have final data for 2005, the signals from strategic sectors of the economy indicate a seventh successive year of economic growth in 2005. The National Budget 2006/07 builds upon the firm economic foundation that has been developed and fortified by successive Progressive Labour Party administrations. It will provide resources for programmes and initiatives that seek the following key objectives: 1. Strengthening social cohesion in our community; 2. Developing and training our Bermuda’s youth; 3. Improving the quality of life of our senior citizens; 4. Putting good quality homes within the economic reach of more Bermudian families; and 5. Stabilising, rejuvenating and encouraging business activity in all economic sectors. -

Listings Advisory: ESG & Green Bonds

Global Legal and Professional Services ADVISORY Industry Information Listings Advisory: ESG & Green Bonds July 2020 If ever there was a year when ESG bonds would come to the fore, 2020 has proven to be such a year. As international capital markets respond to the Covid-19 pandemic, we have witnessed a renewed focus on the social element of ESG bonds reflecting strong investor appetite for ESG issuance, particularly where the proceeds of such issuance may have a beneficial societal impact during this crisis. Walkers has been pleased to act as listing agent on a number of recent ESG issuances and we expect to see increased demand from capital markets participants for ESG products during 2020 and beyond. Alongside increased investor demand for ESG & green bonds, we’ve seen the development and promotion of ESG & Green market segments on many international stock exchanges including Euronext Dublin, the Cayman Islands Stock Exchange (CSX), The International Stock Exchange (TISE), Vienna MTF and the Bermuda Stock Exchange (BSX) for whom Walkers acts as a recognised listing agent. This advisory aims to provide clients with a flavour of our listing expertise alongside the options available when choosing to list ESG & Green Bonds. Listing ESG & Green Bonds on a Recognised Stock Exchange At Walkers we offer issuers a choice of market on which to list your securities with the added attraction of recognised ESG & Green segments. The process for listing ESG and Green Bonds follows the standard listing process with the additional benefit of boosting the profile of your bond through its admission to the green/ESG segment of an internationally recognised stock market. -

POLICE 2003 Cover Visual

strength, determination + perseverance 2003 ANNUAL REPORT Vision Statement The Bermuda Police Service, focusing on its core functions, is operating at full strength and is support- ed by an effective and efficient Human Resources Department and civilianisation process. Facilities are specifically built or adapted to meet the unique demands of modern policing. Proven technological and support equipment as well as the required financial resources are utilised. Its highly trained and respected Bermudian Commissioner is heading an effective, apolitical management team that is practicing shared leadership of a disciplined Service. Consistent application of policies reflects its values, mission and vision. Effective training and development programmes continuously enhance job performance and meet individual and organisational needs. The communication process is open, honest and respectful. It flows effectively, both internally and exter- nally. It is working in partnership with the community and other agencies to provide the necessary edu- cation and information that enhances these relationships. There is a safe, practical and healthy work environment for all. An effective welfare policy and enforced code of conduct promote openness, trust and unity. Its members have access to legal representation and funding when a complaint has been lodged. The Hon. Randolph Through unified representation, all members are covered by an equitable medical policy and are pro- Horton, JP, MP vided with similar benefits. Minister of Labour, Home Affairs and Public Safety Introduction Section 62 (1) (c) and (d) of the Bermuda Constitution set out the responsibilities of the Governor of Bermuda for the internal security of Bermuda and the Bermuda Police Service. The operational control of the Bermuda Police Service (BPS) is vested in the Commissioner of Police by virtue of the Police Act 1974. -

Racism, Oligarchy and Contentious Politics in Bermuda Andrea Dean [email protected]

Western University Scholarship@Western MA Research Paper Sociology Department September 2017 Racism, Oligarchy and Contentious Politics in Bermuda Andrea Dean [email protected] Follow this and additional works at: https://ir.lib.uwo.ca/sociology_masrp Part of the Politics and Social Change Commons Recommended Citation Dean, Andrea, "Racism, Oligarchy and Contentious Politics in Bermuda" (2017). MA Research Paper. 16. https://ir.lib.uwo.ca/sociology_masrp/16 This Dissertation/Thesis is brought to you for free and open access by the Sociology Department at Scholarship@Western. It has been accepted for inclusion in MA Research Paper by an authorized administrator of Scholarship@Western. For more information, please contact [email protected], [email protected]. Racism, Oligarchy and Contentious Politics in Bermuda by Andrea S. Dean A research paper accepted in partial fulfilment of the requirements for the degree of Master of Arts Department of Sociology The University of Western Ontario London, Ontario, Canada Supervisor: Dr. Anton Allahar 2017 ABSTRACT In 1959, ‘blacks’ in Bermuda boycotted the island’s movie theatres and held nightly protests over segregated seating practices. By all accounts the 1959 Theatre Boycott was one of the most significant episodes of contentious politics in contemporary Bermuda, challenging social norms that had been in existence for 350 years. While the trajectory and outcomes of ‘black’ Bermudians’ transgressive social protests could not have been predicted, this analysis uses racism, oligarchy and contentious politics as conceptual tools to illuminate the social mechanisms and processes that eventually led to the end of formal racial segregation in Bermuda after less than three weeks of limited and non-violent collective action. -

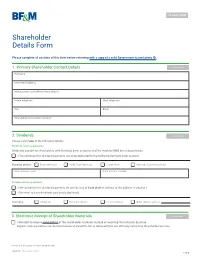

Shareholder Update Form

Shareholder Details Form Please complete all sections of this form before returning with a copy of a valid Government-issued photo ID. 1. Primary Shareholder Contact Details Full name Residential address Mailing address (if different from above) Home telephone Work telephone Cell Email Shareholder registration name(s)* 2. Dividends Please select one of the following options: Bermuda currency payments: Dividends payable to shareholders with Bermuda bank accounts shall be made by BMD direct deposit only. I/We authorise that dividend payments are to be deposited to the following Bermuda bank account. Banking details: Butterfield Bank HSBC Bank Bermuda Clarien Bank Bermuda Commercial Bank Bank account name: Bank account number: Foreign currency payments: I/We authorise that dividend payments be sent by way of bank draft as follows to the address in Section 1. I/We elect to have dividends paid yearly (optional). Currency: US Dollars Canadian Dollars Pounds Sterling Other (please specify): 3. Electronic Receipt of Shareholder Materials I/We elect to receive HARD COPIES of the shareholder materials instead of receiving the materials by email. Reports and newsletters can be found online at www.bfm.bm or obtained from our office by contacting Shareholder Services. * Name as it will appear on the share certificate. LGL100 / December 2020 1 of 3 4. Compliance Details Please complete the following for each named shareholder, including joint shareholders and minors/beneficiaries. Please include all nationalities and countries of residence. Type of -

Perceptions of Bermudian Leaders About the Philosophies, Major

East Tennessee State University Digital Commons @ East Tennessee State University Electronic Theses and Dissertations Student Works 5-2011 Perceptions of Bermudian Leaders About the Philosophies, Major Purposes, and Effectiveness of the Public School System in Bermuda Since 1987 Vincent Sinclair Williams Jr. East Tennessee State University Follow this and additional works at: https://dc.etsu.edu/etd Part of the Educational Leadership Commons Recommended Citation Williams, Vincent Sinclair Jr., "Perceptions of Bermudian Leaders About the Philosophies, Major Purposes, and Effectiveness of the Public School System in Bermuda Since 1987" (2011). Electronic Theses and Dissertations. Paper 1220. https://dc.etsu.edu/etd/1220 This Dissertation - Open Access is brought to you for free and open access by the Student Works at Digital Commons @ East Tennessee State University. It has been accepted for inclusion in Electronic Theses and Dissertations by an authorized administrator of Digital Commons @ East Tennessee State University. For more information, please contact [email protected]. Perceptions of Bermudian Leaders About the Philosophies, Major Purposes, and Effectiveness of the Public School System in Bermuda Since 1987 __________________ A dissertation presented to the faculty of the Department of Educational Leadership and Policy Analysis East Tennessee State University In partial fulfillment of the requirements for the degree Doctor of Education in Educational Leadership __________________ by Vincent Sinclair Williams, Jr. August 2011 __________________ Dr. Terrence Tollefson, Chair Dr. William Douglas Burgess, Jr. Dr. Eric Glover Dr. Pamela Scott Keywords: Bermuda public education, Bermuda private education, Bermuda education reform, Bermuda philosophy of education, Bermuda secondary school graduation rates, Education and Bermuda ABSTRACT Perceptions of Bermudian Leaders About the Philosophies, Major Purposes, and Effectiveness of the Public School System in Bermuda Since 1987 by Vincent Sinclair Williams, Jr.