Pdf 504.7 Kb

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Australian Diurnal Raptors and Airports

Australian diurnal raptors and airports Photo: John Barkla, BirdLife Australia William Steele Australasian Raptor Association BirdLife Australia Australian Aviation Wildlife Hazard Group Forum Brisbane, 25 July 2013 So what is a raptor? Small to very large birds of prey. Diurnal, predatory or scavenging birds. Sharp, hooked bills and large powerful feet with talons. Order Falconiformes: 27 species on Australian list. Family Falconidae – falcons/ kestrels Family Accipitridae – eagles, hawks, kites, osprey Falcons and kestrels Brown Falcon Black Falcon Grey Falcon Nankeen Kestrel Australian Hobby Peregrine Falcon Falcons and Kestrels – conservation status Common Name EPBC Qld WA SA FFG Vic NSW Tas NT Nankeen Kestrel Brown Falcon Australian Hobby Grey Falcon NT RA Listed CR VUL VUL Black Falcon EN Peregrine Falcon RA Hawks and eagles ‐ Osprey Osprey Hawks and eagles – Endemic hawks Red Goshawk female Hawks and eagles – Sparrowhawks/ goshawks Brown Goshawk Photo: Rik Brown Hawks and eagles – Elanus kites Black‐shouldered Kite Letter‐winged Kite ~ 300 g Hover hunters Rodent specialists LWK can be crepuscular Hawks and eagles ‐ eagles Photo: Herald Sun. Hawks and eagles ‐ eagles Large ‐ • Wedge‐tailed Eagle (~ 4 kg) • Little Eagle (< 1 kg) • White‐bellied Sea‐Eagle (< 4 kg) • Gurney’s Eagle Scavengers of carrion, in addition to hunters Fortunately, mostly solitary although some multiple strikes on aircraft Hawks and eagles –large kites Black Kite Whistling Kite Brahminy Kite Frequently scavenge Large at ~ 600 to 800 g BK and WK flock and so high risk to aircraft Photo: Jill Holdsworth Identification Beruldsen, G (1995) Raptor Identification. Privately published by author, Kenmore Hills, Queensland, pp. 18‐19, 26‐27, 36‐37. -

5B99d384092a4e9cbc7545b9

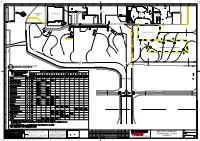

TERMINAL RFDS PARKING RFDS HANGER AREA SHELL AIR BP 5 EQUIPMENT STORAGE EQUIPMENT STORAGE EQUIPMENT BE20 PC12 BE20 BAY 5 BAY BAY 5 2 1 E170 E190 F100 E190 E170 BAY BAY B734/7-8 A321 A320 REFUELLING AREA 2 1 4 3 ENTRY NO 4 E170 E190 F100 E190 E170 A320 B734-7-8 A320 DH8A/C SF34 E110 BE20 SW4 PC12 3 SW4 PC12 SF34 PC12 SW4 SECURITY RESTRICTED AREA RESTRICTED SECURITY DH8A/C BE20 E110 BE20 DH8A/C BE20 SW4 PC12 SW4 BE20 F100 E170 E190 F100 E190 E170 DH8A-D G3 G2 1A B350 B350 BAY BAY G4 G2 G3 REFUELLING TAXILANE BAY ONLY G1 G1 CODE B GENERAL AVIATION APRON BAY SW4 G4 B350 WINGSPAN AREA RESTRICTED SECURITY MAX 18M 4 G4 G1 G2 G3 G1-G4 3 2 WINGSPAN MAX. 24m 3-5 1 MAX 29M WINGSPAN AIRCRAFT PARKING APRON 2-6 SCALE 1:500 TAXIWAY 'B' TAXIWAY 'A' TAXIWAY 'A' x This plan has been compiled from precision survey data and the digitising This document is the property of the Queensland Airports K 27.02.15 ADDITION OF GA BAYS & LEGEND UPDATE D.Brugman of any applicable 1:250 or 1:500 Survey Detail Sheet. Limited, and is COPYRIGHT. All information contained in J 09.02.15 ADDITION OF B712 BAYS 1 & 2 A.Coghill x All heights shown are based on A.H.D. (Australian Height Datum). it vests with Queensland Airports Limited. The information MOUNT ISA AIRPORT 1:500 is CONFIDENTIAL and is provided for the use of the party I 16.09.14 MGA CO-ORDINATES D.Brugman LIMITED WARNING to whom this document has been issued by the Company 1077 H 15.07.14 CHANGES TO GA AREA A.Coghill AIRCRAFT PARKING POSITIONS Underground services, if shown on this plan, are those known to exist and are for a specific purpose. -

Economic Regulation of Airport Services

Productivity Commission Inquiry into the Economic Regulation of Airport Services Submission by Queensland Airports Limited June 2011 Productivity Commission Inquiry - Economic Regulation of Airport Services 1. INTRODUCTION Queensland Airports Limited (QAL) owns Gold Coast Airport Pty Ltd, Mount Isa Airport Pty Ltd and Townsville Airport Pty Ltd, the airport lessee companies for the respective airports. QAL owns Aviation Ground Handling Pty Ltd (AGH) which has ground handling contracts for airlines at Gold Coast, Sunshine Coast, Gladstone, Rockhampton, Mackay and Townsville Airports and Worland Aviation Pty Ltd, an aircraft maintenance, repair and overhaul company based in the Northern Australian Aerospace Centre of Excellence at Townsville Airport. QAL specialises in providing services and facilities at regional airports in Australia and is a 100% Australian owned company. The majority of its shares are held by fund managers on behalf of Australian investors such as superannuation funds. 2. PRODUCTIVITY COMMISSION INQUIRY RESPONSE QAL makes this submission to the Productivity Commission Inquiry as an investor/operator whose airports have experienced little or no formal pricing or quality of service regulation over the last decade. We feel our experience demonstrates that this light handed regulatory environment has been instrumental in generating significant community and shareholder benefits. In this submission we seek to illustrate where our experience in this environment has been effective in achieving the Government’s desired outcomes -

Airport Categorisation List

UNCLASSIFIED List of Security Controlled Airport Categorisation September 2018 *Please note that this table will continue to be updated upon new category approvals and gazettal Category Airport Legal Trading Name State Category Operations Other Information Commencement CATEGORY 1 ADELAIDE Adelaide Airport Ltd SA 1 22/12/2011 BRISBANE Brisbane Airport Corporation Limited QLD 1 22/12/2011 CAIRNS Cairns Airport Pty Ltd QLD 1 22/12/2011 CANBERRA Capital Airport Group Pty Ltd ACT 1 22/12/2011 GOLD COAST Gold Coast Airport Pty Ltd QLD 1 22/12/2011 DARWIN Darwin International Airport Pty Limited NT 1 22/12/2011 Australia Pacific Airports (Melbourne) MELBOURNE VIC 1 22/12/2011 Pty. Limited PERTH Perth Airport Pty Ltd WA 1 22/12/2011 SYDNEY Sydney Airport Corporation Limited NSW 1 22/12/2011 CATEGORY 2 BROOME Broome International Airport Pty Ltd WA 2 22/12/2011 CHRISTMAS ISLAND Toll Remote Logistics Pty Ltd WA 2 22/12/2011 HOBART Hobart International Airport Pty Limited TAS 2 29/02/2012 NORFOLK ISLAND Norfolk Island Regional Council NSW 2 22/12/2011 September 2018 UNCLASSIFIED UNCLASSIFIED PORT HEDLAND PHIA Operating Company Pty Ltd WA 2 22/12/2011 SUNSHINE COAST Sunshine Coast Airport Pty Ltd QLD 2 29/06/2012 TOWNSVILLE AIRPORT Townsville Airport Pty Ltd QLD 2 19/12/2014 CATEGORY 3 ALBURY Albury City Council NSW 3 22/12/2011 ALICE SPRINGS Alice Springs Airport Pty Limited NT 3 11/01/2012 AVALON Avalon Airport Australia Pty Ltd VIC 3 22/12/2011 Voyages Indigenous Tourism Australia NT 3 22/12/2011 AYERS ROCK Pty Ltd BALLINA Ballina Shire Council NSW 3 22/12/2011 BRISBANE WEST Brisbane West Wellcamp Airport Pty QLD 3 17/11/2014 WELLCAMP Ltd BUNDABERG Bundaberg Regional Council QLD 3 18/01/2012 CLONCURRY Cloncurry Shire Council QLD 3 29/02/2012 COCOS ISLAND Toll Remote Logistics Pty Ltd WA 3 22/12/2011 COFFS HARBOUR Coffs Harbour City Council NSW 3 22/12/2011 DEVONPORT Tasmanian Ports Corporation Pty. -

Queensland Airports Limited Submission, September 2018

Productivity Commission, Economic Regulation of Airports Queensland Airports Limited submission, September 2018 1 Contents 1.0 Executive Summary ........................................................................................................................... 3 2.0 Introduction ....................................................................................................................................... 4 3.0 Background ........................................................................................................................................ 5 4.0 The current system ............................................................................................................................ 7 4.1 The Queensland market and influence ......................................................................................... 7 South east Queensland and Northern NSW market and Gold Coast Airport .................................. 7 Townsville, Mount Isa and Longreach airports ............................................................................... 7 4.2 General factors .............................................................................................................................. 8 Airport charges ................................................................................................................................ 8 Airport leasing conditions ................................................................................................................ 9 4.3 Airport and airline negotiations.................................................................................................. -

Annual Report 2018 002 003

ANNUAL REPORT 2018 002 003 Our vision 04 Our history 06 Highlights 08 About us 10 TABLE OF Shareholder value 18 Customer experience 24 CONTENTS Social responsibility 34 High performing workforce 42 Accomplished operators 46 Media highlights 56 Looking ahead 58 QAL Annual Report 2018 QAL Annual Report 2018 004 005 Our Values Integrity Innovation OUR We value honesty, respect We think differently and fairness We are creative and flexible We do what we say We share our experience to build VISION We act in the best interests new ideas Engaging customers. Teamwork Accountability Together we succeed We take responsibility for our actions Connecting communities. Everyone is a customer We lead by example We are inclusive and support Safety and social responsibility Exceptional experiences. each other are priorities Passion Excellence We are enthusiastic We have high performance standards We care about what we deliver We add value and deliver quality We take pride in our work We embrace change and deliver outcomes Our Strategic We fulfill our vision by: Pillars • Growing our airports through collaboration with our partners Shareholder value • Providing seamless, high quality experiences for our customers • Connecting, and being connected to, the communities in which we operate Customer experience • Fostering growth within our communities Social responsibility • Investing in our people and empowering them to help achieve our vision • Elevating and setting the industry standard through innovation and creative thinking. High performing workforce Accomplished operators QAL Annual Report 2017/20182018 QAL AnnualQAL Annual Report Report 2017/2018 2018 006 007 Our History 2018 marked an important milestone in the business, celebrating 20 years since privatisation of Gold Coast, Townsville and Mount Isa airports. -

Document Is for Informational Purposes Only

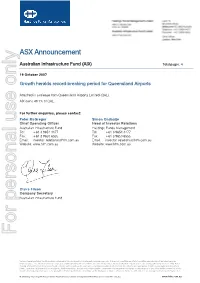

ASX Announcement Australian Infrastructure Fund (AIX) Total pages: 4 19 October 2007 Growth heralds record-breaking period for Queensland Airports Attached is a release from Queensland Airports Limited (QAL). AIX owns 49.1% of QAL. For further enquiries, please contact: Peter McGregor Simon Ondaatje Chief Operating Officer Head of Investor Relations Australian Infrastructure Fund Hastings Funds Management Tel: +61 3 9654 4477 Tel: +61 3 9654 4477 Fax: +61 3 9650 6555 Fax: +61 3 9650 6555 Email: [email protected] Email: [email protected] Website: www.hfm.com.au Website: www.hfm.com.au Claire Filson Company Secretary Australian Infrastructure Fund For personal use only Unless otherwise stated, the information contained in this document is for informational purposes only. It does not constitute an offer of securities and should not be relied upon as financial advice. The information has been prepared without taking into account the investment objectives, financial situation or particular needs of any particular person or entity. Before making an investment decision you should consider, with or without the assistance of a financial adviser, whether any investments are appropriate in light of your particular investment needs, objectives and financial circumstances. Neither Hastings, nor any of its related parties, guarantees the repayment of capital or performance of any of the entities referred to in this document and past performance is no guarantee of future performance. Hastings, as the Manager or Trustee of various -

Annual Report 2015 /16

Annual Report 2015 /16 1 / QUEENSLAND AIRPORTS PTY LTD 2015/16 ANNUAL REPORT Contents 03 Our Vision 07 Chairman’s Message 08 CEO’s Message 09 Our Stakeholders 10 QAL Board 15 QAL Management 19 Shareholder Value 24 Customer Experience 28 Social Responsibility 34 High Performing Workforce 36 Accomplished Operators 38 Investing in Tomorrow 39 Contact QUEENSLAND AIRPORTS PTY LTD 2015/16 ANNUAL REPORT Our Vision Engaging customers, connecting communities, exceptional experiences. We will fulfill our vision by • Growing our airports through collaboration with our partners • Providing seamless, high quality experiences for our customers • Connecting (and being connected to) the communities in which we operate • Fostering growth within our communities • Investing in our people and empowering them to help achieve our vision • Elevating and setting the industry standard through innovation and creative thinking 3 / QUEENSLAND AIRPORTS PTY LTD 2015/16 ANNUAL REPORT Our Strategic Pillars Our pillars help us translate our vision into everything we do Shareholder Value Customer Experience Social Responsibility High Performing Workforce Accomplished Operators Our Values INTEGRITY We act honestly, we do the right thing TEAMWORK We have a collaborative environment that values diversity PASSION We are enthusiastic, we love what we do INNOVATION We challenge the status quo, we do things differently ACCOUNTABILITY We take responsibility EXCELLENCE We strive to be the best, we challenge ourselves LEADERSHIP We have a clear vision, we are empowered 4 / QUEENSLAND AIRPORTS PTY LTD 2015/16 ANNUAL REPORT Wholly Owned Airport NAACEX Townsville Mount Isa Longreach About Us Gold Coast Queensland Airports Australian owned and managed, OUR SHAREHOLDERS QAL has operated airports since 1998. -

Safetaxi Australia Coverage List - Cycle 21S5

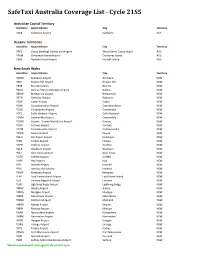

SafeTaxi Australia Coverage List - Cycle 21S5 Australian Capital Territory Identifier Airport Name City Territory YSCB Canberra Airport Canberra ACT Oceanic Territories Identifier Airport Name City Territory YPCC Cocos (Keeling) Islands Intl Airport West Island, Cocos Island AUS YPXM Christmas Island Airport Christmas Island AUS YSNF Norfolk Island Airport Norfolk Island AUS New South Wales Identifier Airport Name City Territory YARM Armidale Airport Armidale NSW YBHI Broken Hill Airport Broken Hill NSW YBKE Bourke Airport Bourke NSW YBNA Ballina / Byron Gateway Airport Ballina NSW YBRW Brewarrina Airport Brewarrina NSW YBTH Bathurst Airport Bathurst NSW YCBA Cobar Airport Cobar NSW YCBB Coonabarabran Airport Coonabarabran NSW YCDO Condobolin Airport Condobolin NSW YCFS Coffs Harbour Airport Coffs Harbour NSW YCNM Coonamble Airport Coonamble NSW YCOM Cooma - Snowy Mountains Airport Cooma NSW YCOR Corowa Airport Corowa NSW YCTM Cootamundra Airport Cootamundra NSW YCWR Cowra Airport Cowra NSW YDLQ Deniliquin Airport Deniliquin NSW YFBS Forbes Airport Forbes NSW YGFN Grafton Airport Grafton NSW YGLB Goulburn Airport Goulburn NSW YGLI Glen Innes Airport Glen Innes NSW YGTH Griffith Airport Griffith NSW YHAY Hay Airport Hay NSW YIVL Inverell Airport Inverell NSW YIVO Ivanhoe Aerodrome Ivanhoe NSW YKMP Kempsey Airport Kempsey NSW YLHI Lord Howe Island Airport Lord Howe Island NSW YLIS Lismore Regional Airport Lismore NSW YLRD Lightning Ridge Airport Lightning Ridge NSW YMAY Albury Airport Albury NSW YMDG Mudgee Airport Mudgee NSW YMER Merimbula -

Innovation and Excellence Recognised at AAA National Airport Industry Awards

16 November 2017 Innovation and excellence recognised at AAA National Airport Industry Awards The Australian Airports Association (AAA) hosted its 2017 National Airport Industry Awards last night, recognising innovation and excellence across a range of categories. AAA Chief Executive Officer Caroline Wilkie said the awards showcased the many ways airports are transforming the customer experience for the 154 million passengers travelling through Australia’s airports each year. “Australia’s airports are busier than ever as they invest to deliver a great customer experience for our growing number of passengers,” Ms Wilkie said. “This year’s award winners include Australian airport firsts, significant investments in capacity and innovative new approaches to meeting changing customer needs. “The awards highlight the airport industry’s commitment to investing in our aviation sector to drive growth and build our tourism economy.” Ms Wilkie said the judging panel noted the high standard of submissions, reflecting the wide range of projects and initiatives underway at Australia’s airports. Airport of the Year awards were announced across five categories, with Sydney Airport, Launceston Airport, Coffs Harbour Regional Airport, Tennant Creek Airport and Bendigo Regional Airport taking home the honours. A wide range of Innovation and Excellence Awards were also up for grabs, recognising key projects and initiatives across customer service, commercial, development, operations, environmental management and technology. Sydney Airport Managing Director and CEO Kerrie Mather was also honoured at the event, receiving the Outstanding Contribution to the Airport Industry Award. “All of our winners reflect the passion and dedication of airport staff to lead their industry and create great experiences for the travelling public,” Ms Wilkie said. -

Copperstring Draft

CopperString 2.0 Assessment of the impact to aviation Volume 3 Appendix Y July 2020 AVIATION IMPACT ASSESSMENT COPPERSTRING 2.0 PROJECT Prepared for GHD Pty Ltd DOCUMENT CONTROL Document Title: CopperString 2.0 Project - Aviation Impact Assessment Reference: 063702-01 Prepared by: G Holmes Reviewed by: P Davidyuk/ K Tonkin Released by: G Holmes Revision History Version Description Transmitted Reviewed by Date 0.1 First Draft 18 March 2020 N Govha, M Barnett, P Bradley 8 April 2020 0.2 Second Draft 09 April 2020 GHD 14 July 2020 1.0 Final 17 July 2020 COPYRIGHT AND DISCLAIMER NOTICE This document and the information contained herein should be treated as commercial-in-confidence. No part of this work may be reproduced or copied in any form or by any means (graphic, electronic or mechanical, including photocopying, recording, taping or information retrieval system) or otherwise disclosed to any other party whatsoever, without the prior written consent of Aviation Projects Pty Ltd. This report has been prepared for the benefit solely of the Client, and is not to be relied upon by any other person or entity without the prior written consent of Aviation Projects Pty Ltd. © Aviation Projects Pty Ltd, 2020. All rights reserved 063702-01 COPPERSTRING 2.0 PROJECT – AVIATION IMPACT ASSESSMENT i TABLE OF CONTENTS Document Control ____________________________________________________________________________ i Copyright and Disclaimer Notice ________________________________________________________________ i Table of Contents ____________________________________________________________________________ -

Un-Fare, Un-Australian - Why Is It So? Submission from the Mount Isa City Council

Un-Fare, Un-Australian - Why is it so? Submission from the Mount Isa City Council Australian Senate Inquiry into Regional Air Services 1 February 2018 1 Contact Sharon Ibardolaza Acting Chief Executive Officer Mount Isa City Council Phone 07 4747 3200 | Fax 07 4747 3209 Email [email protected] PO BOX 815 | Mount Isa Qld 4825 2 / 32 Table of Contents EXECUTIVE SUMMARY ............................................................................................................................ 4 RECOMMENDED ACTIONS ...................................................................................................................... 5 INTRODUCTION ........................................................................................................................................ 6 ABOUT MOUNT ISA ................................................................................................................................... 6 IMPACTS OF HIGH AIRFARES ................................................................................................................. 8 Poor service standards ............................................................................................................................... 9 Airfares ........................................................................................................................................................ 9 NATIONAL TRENDS IN AUSTRALIAN AVIATION .................................................................................. 10 Trends at Mount Isa ..................................................................................................................................12