CVD System ALD System

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Panasonic Telephone Products Limited Warranty

GT15xx.book Page 103 Monday, June 4, 2007 8:52 AM Useful Information Warranty PANASONIC CONSUMER PANASONIC PUERTO RICO, INC. ELECTRONICS COMPANY, DIVISION San Gabriel Industrial Park, OF PANASONIC CORPORATION OF Ave. 65 de Infantería, Km. 9.5, NORTH AMERICA Carolina, Puerto Rico 00985 One Panasonic Way, Secaucus, New Jersey 07094 Panasonic Telephone Products Limited Warranty Limited Warranty Coverage If your product does not work properly because of a defect in materials or workmanship, Panasonic Consumer Electronics Company or Panasonic Puerto Rico, Inc. (collectively referred to as “the warrantor”) will, for the length of the period indicated on the chart below, which starts with the date of original purchase (“Limited Warranty period”), at its option either (a) repair your product with new or refurbished parts, or (b) replace it with a new or a refurbished product. The decision to repair or replace will be made by the warrantor. Parts Labor One (1) Year One (1) Year During the “Labor” Limited Warranty period there will be no charge for labor. During the “Parts” Limited Warranty period, there will be no charge for parts. You must mail-in your product prepaid during the Limited Warranty period. This Limited Warranty excludes both parts and labor for batteries, antennas, and cosmetic parts (cabinet). This Limited Warranty only applies to products purchased and serviced in the United States or Puerto Rico. This Limited ✄ Warranty is extended only to the original purchaser and only covers products purchased as new. Mail-In Service For assistance in the continental U.S.A. in obtaining repairs please ship the product prepaid to: Panasonic Service and Technology Company, Exchange Center, 4900 George McVay Drive, Suite B Door #12, McAllen, TX 78503 [email protected] When shipping the unit carefully pack, include all accessories, and send it prepaid, adequately insured and preferably in the original carton. -

Fujitsu to Split Off HDD Business in Reorganization

Fujitsu Limited Fujitsu to Split Off HDD Business in Reorganization Tokyo, May 21, 2009 – Fujitsu Limited (“Fujitsu”) today announced that it will split off its hard disk drive business (“HDD business”) and merge the business into its wholly owned subsidiary, Toshiba Storage Device Corporation (“Toshiba Storage Device”), through a simple absorption-type separation, on July 1, 2009. In a transaction scheduled for July 1, 2009, Fujitsu will then sell 80.1 percent of its shares of Toshiba Storage Device to Toshiba Corporation (“Toshiba”). By the end of December 2010, Fujitsu plans to sell its remaining 19.9 percent to Toshiba, at which point Toshiba Storage Device will become a wholly owned subsidiary of Toshiba. 1. Objectives of the Corporate Split On April 30, 2009, Fujitsu Limited signed a definitive agreement with Toshiba to transfer ownership of its HDD business. This corporate split is part of the implementation of the ownership transfer. 2. Outline of the Corporate Split (1) Schedule May 21, 2009 Signing of corporate split contract July 1, 2009 (scheduled) Effective date of corporate split This corporate split, pursuant to Article 784 (3) of the Corporate Law, will be executed without the requirement of the approval of a General Meeting of the Shareholders as stipulated under Article 783 (1) of the Corporate Law (Simple Absorption-type Separations). (2) Method Fujitsu will be the transferor company and Toshiba Storage Device will be the successor company (Simple Separation). (3) Decrease in Capital or Other, Resulting from the Corporate Split There will be no decrease in capital or other, resulting from the corporate split. -

The Wizard of Invention and the Warrior of Innovation

VISIONS INNOVATORS AND INNOVATIONS 02 2006 THE WIZARD OF INVENTION AND THE WARRIOR OF INNOVATION A HISTORY OF TECHNOLOGY LEADERSHIP Toshiba has a proud tradition of achievement. In almost 130 In 1890, Hakunetsusha & Co., Ltd. was established by the years of operation, the company has recorded numerous firsts entrepreneur Ichisuke Fujioka as Japan’s first plant for electric and made many valuable contributions to technology and society. incandescent lamps. Subsequent diversification saw the compa- It is currently the world’s 9th largest integrated manufacturer of ny evolve as a manufacturer of consumer products. In 1899, the electric and electronic equipment, has some 161,000 employees company was renamed Tokyo Denki (Tokyo Electric Co.). worldwide, and enjoys consolidated annual sales of over US$53 billion. In 1939, these two companies, leaders in their respective fields, merged to form an integrated electric equipment manufacturer, Not surprisingly, Toshiba’s role as a leading innovator and Tokyo Shibaura Denki (Tokyo Shibaura Electric Co., Ltd.). The inventor of technology goes back to its earliest founders in the company was soon well known as ‘Toshiba’. 19th century. In 1875, Tanaka Seizo-sho (Tanaka Engineering Works), Japan’s first manufacturer of telegraphic equipment, was Today, Toshiba’s total commitment to people and to the future, its established. Its founder, Hisashige Tanaka, was well known from determination to help create a higher quality of life for all peo- his youth for inventions that included mechanical dolls and a ple, and its undaunted efforts to help ensure that technological perpetual clock. Under the name Shibaura Seisaku-sho (Shibaura progress continues within the world community finds its origins in Engineering Works), his company became one of Japan’s largest the life stories of Hisashige Tanaka and Ichisuke Fujioka. -

2020 Integrated Report

Integrated Report 2020 Year ended March 31, 2020 Basic Commitment of the Toshiba Group Committed to People, Committed to the Future. At Toshiba, we commit to raising the quality of life for people around The Essence of Toshiba the world, ensuring progress that is in harmony with our planet. Our Purpose The Essence of Toshiba is the basis for the We are Toshiba. We have an unwavering drive to make and do things that lead to a better world. sustainable growth of the Toshiba Group and A planet that’s safer and cleaner. the foundation of all corporate activities. A society that’s both sustainable and dynamic. A life as comfortable as it is exciting That’s the future we believe in. We see its possibilities, and work every day to deliver answers that will bring on a brilliant new day. By combining the power of invention with our expertise and desire for a better world, we imagine things that have never been – and make them a reality. That is our potential. Working together, we inspire a belief in each other and our customers that no challenge is too great, and there’s no promise we can’t fulfill. We turn on the promise of a new day. Our Values Do the right thing We act with integrity, honesty and The Essence of Toshiba comprises three openness, doing what’s right— not what’s easy. elements: Basic Commitment of the Toshiba Group, Our Purpose, and Our Values. Look for a better way We continually s trive to f ind new and better ways, embracing change With Toshiba’s Basic Commitment kept close to as a means for progress. -

CORPORATE DIRECTORY (As of June 28, 2000)

CORPORATE DIRECTORY (as of June 28, 2000) JAPAN TOKYO ELECTRON KYUSHU LIMITED TOKYO ELECTRON FE LIMITED Saga Plant 30-7 Sumiyoshi-cho 2-chome TOKYO ELECTRON LIMITED 1375-41 Nishi-Shinmachi Fuchu City, Tokyo 183-8705 World Headquarters Tosu City, Saga 841-0074 Tel: 042-333-8411 TBS Broadcast Center Tel: 0942-81-1800 District Offices 3-6 Akasaka 5-chome, Minato-ku, Tokyo 107-8481 Kumamoto Plant Osaka, Kumamoto, Iwate, Tsuruoka, Sendai, Tel: 03-5561-7000 2655 Tsukure, Kikuyo-machi Aizuwakamatsu, Takasaki, Mito, Nirasaki, Toyama, Fax: 03-5561-7400 Kikuchi-gun, Kumamoto 869-1197 Kuwana, Fukuyama, Higashi-Hiroshima, Saijo, Oita, URL: http://www.tel.co.jp/tel-e/ Tel: 096-292-3111 Nagasaki, Kikuyo, Kagoshima Regional Offices Ozu Plant Fuchu Technology Center, Osaka Branch Office, 272-4 Takaono, Ozu-machi TOKYO ELECTRON DEVICE LIMITED Kyushu Branch Office, Tohoku Regional Office, Kikuchi-gun, Kumamoto 869-1232 1 Higashikata-cho, Tsuzuki-ku Yamanashi Regional Office, Central Research Tel: 096-292-1600 Yokohama City, Kanagawa 224-0045 Laboratory/Process Technology Center Koshi Plant Tel: 045-474-7000 Sales Offices 1-1 Fukuhara, Koshi-machi Sales Offices Sendai, Nagoya Kikuchi-gun, Kumamoto 861-1116 Utsunomiya, Mito, Kumagaya, Kanda, Tachikawa, Tel: 096-349-5500 Yamanashi, Matsumoto, Nagoya, Osaka, Fukuoka TOKYO ELECTRON TOHOKU LIMITED Tohoku Plant TOKYO ELECTRON MIYAGI LIMITED TOKYO ELECTRON LEASING CO., LTD. 52 Matsunagane, Iwayado 1-1 Nekohazama, Nemawari, Matsushima-machi 30-7 Sumiyoshi-cho 2-chome Esashi City, Iwate 023-1101 Miyagi-gun, Miyagi -

KODAK Service and Support Offers Advanced Service Package for Users of CANON, FUJITSU and PANASONIC Document Scanners

KODAK Service and Support Offers Advanced Service Package for Users of CANON, FUJITSU And PANASONIC Document Scanners ROCHESTER, N.Y., Nov. 30—New KODAK Care Kits make it easier for customers with other manufacturers’ scanners to keep their document capture hardware up and running. Advanced maintenance options, including Advance Unit Repair (AUR) for select models of CANON, FUJITSU and PANASONIC Document Scanners, are now available from KODAK Service and Support through newly formulated two-year KODAK Care Kits. “With digital workflows becoming the standard for many industries, including healthcare and government, document imaging technology hugely impacts the efficiency of sharing electronic information and applications,” said Karen Sherrill, Director, Worldwide Service, Document Imaging, Kodak’s Business Solutions and Services Group, and recent recipient of the 2009 Customer Service Executive of the Year, International Business Awards, STEVIE Awards. “With a KODAK Care Kit AUR, users can rely upon the expertise and capabilities of an ISO certified support team.” Kodak’s AUR option for CANON, FUJITSU and PANASONIC Scanners provides users with next-day product replacement and unlimited phone support. For value added resellers (VARs) and value added distributors (VADs), this new capability enhances their ability to meet customer needs and ensure top service performance. Many VARs and VADs currently find that service represents a significant portion of customer revenue. Supported FUJITSU Scanners include the FUJITSU fi-6140 Scanner, the FUJITSU fi- 6240 Scanner, the FUJITSU fi-6130 Scanner, the FUJITSU 6230 Scanner and the FUJITSU fi-6010NS Scanner. Supported CANON Scanners include the CANON DR- 2580C and the CANON DR-3010C. Supported PANASONIC Scanners include the PANASONIC KV-S1025C. -

INVESTORS GUIDE 2019 Osaka Office to Our Shareholders and Investors Fukuoka Sales Office Shinjuku Office Shinjuku Support Center Tachikawa Sales Office

TOKYO ELECTRON DEVICE LIMITED Securities code: 2760 Business Locations (As of July 1, 2019) Business Location Domestic Subsidiary Omiya Sales Office Matsumoto Sales Office Sendai Sales Office Tsukuba Sales Office Iwaki Sales Office Nagoya Sales Office Mito Sales Office Kyoto Sales Office INVESTORS GUIDE 2019 Osaka Office To Our Shareholders and Investors Fukuoka Sales Office Shinjuku Office Shinjuku Support Center Tachikawa Sales Office Engineering Center Headquarters (Yokohama) FAST CORPORATION (Yamato-city, Kanagawa prefecture) TOKYO ELECTRON DEVICE Mishima Sales Office NAGASAKI LTD. Hamamatsu Sales Office (Isahaya-city, Nagasaki prefecture) Business/Marketing location Overseas Design and development location Dalian Yokohama Ottawa Seoul Silicon Valley Shanghai Taipei Shenzhen Bangkok Wuxi Hong Kong Singapore Philippines Note on forward-looking statements This Investors Guide was prepared on July 1, 2019. Forward looking statements, including business strategies and business forecasts, were made by the Company’s management, based on information available at that time, and may be revised due to changes in the business environment. Therefore, please be advised that the Company cannot guarantee the accuracy or the reliability of the statements. For the latest information, please refer to our information releases or our website. Note also that product and service names remain the trademarks of their respective owners. Corporate Communications Dept. https://www.teldevice.co.jp World Headquarters Yokohama East Square, 1-4 Kinko-cho, Kanagawa-ku,Yokohama -

ISSM2020 –International Symposium on Semiconductor Manufacturing SPONSORSHIP December 15-16, 2020, Tokyo, Japan

ISSM2020 –International Symposium on Semiconductor Manufacturing SPONSORSHIP December 15-16, 2020, Tokyo, Japan Shozo Saito Chairman, ISSM2020 Organizing Committee Device & System Platform Development Center Co., Ltd. Shuichi Inoue, ATONARP INC. It is our great pleasure to announce that The 28th annual International Symposium on Semiconductor Manufacturing (ISSM) 2020 will be held on December 15-16, 2020 at KFC Hall, Ryogoku, Tokyo in cooperation with e-Manufacturing & Design Collaboration Symposium (eMDC) which is sponsored by TSIA with support from SEMI and GSA. The program will feature keynote speeches by world leading speakers, timely and highlighted topics and networking sessions focusing on equipment/materials/software/services with suppliers' exhibits. ISSM continues to contribute to the growth of the semiconductor industry through its infrastructure for networking, discussion, and information sharing among the world's professionals. We would like you to cooperate with us by supporting the ISSM 2020. Please see the benefit of ISSM2020 sponsorship. Conference Overview Date: December 15-16, 2020 Location: KFC (Kokusai Fashion Center) Hall 1-6-1 Yokoami Sumidaku, Tokyo 130-0015 Japan +81-3-5610-5810 Co-Sponsored by: IEEE Electron Devices Society Minimal Fab Semiconductor Equipment Association of Japan (SEAJ) Semiconductor Equipment and Materials International (SEMI) Taiwan Semiconductor Industry Association (TSIA) Endorsement by: The Japan Society of Applied Physics Area of Interest: Fab Management Factory Design & Automated Material -

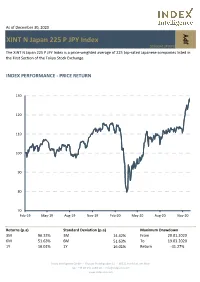

XINT N Japan 225 P JPY Index

As of December 30, 2020 XINT N Japan 225 P JPY Index JPY DE000A13PWP8 The XINT N Japan 225 P JPY Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. INDEX PERFORMANCE - PRICE RETURN 130 120 110 100 90 80 70 Feb-19 May-19 Aug-19 Nov-19 Feb-20 May-20 Aug-20 Nov-20 Returns (p.a) Standard Deviation (p.a) Maximum Drawdown 3M 96.33% 3M 14.42% From 20.01.2020 6M 51.63% 6M 51.63% To 19.03.2020 1Y 16.01% 1Y 16.01% Return -31.27% Index Intelligence GmbH - Grosser Hirschgraben 15 - 60311 Frankfurt am Main Tel.: +49 69 247 5583 50 - [email protected] www.index-int.com Top 10 Constituents FFMV (JPYm) Weight % Industry Sector Fast Retailing Co Ltd 5 12.13 Retail SoftBank Group Corp 2 6.34 Telecommunications Tokyo Electron Ltd 2 5.04 Technology FANUC Corp 1 3.33 Industrial Goods & Services M3 Inc 1 3.07 Health Care Daikin Industries Ltd 1 3.01 Construction & Materials KDDI Corp 1 2.41 Telecommunications Shin-Etsu Chemical Co Ltd 1 2.37 Chemicals Terumo Corp 1 2.26 Health Care Chugai Pharmaceutical Co Ltd 1 2.17 Health Care Total 16 42.13 This information has been prepared by Index Intelligence GmbH (“IIG”). All information is provided "as is" and IIG makes no express or implied warranties, and expressly disclaims all warranties of merchantability or fitness for a particular purpose or use with respect to any data included herein. -

OKI Implements Sarnoff's Takecharge On-Chip ESD Protection in High

Also available on Business Wire 08/26/05 For Immediate Release OKI® Implements Sarnoff’s Takecharge® On-Chip ESD Protection In High-Voltage ICs Design Approach for On-Chip ESD Protection Successfully Implemented in High-Voltage Chips TOKYO, JAPAN / PRINCETON, NJ, USA / GISTEL, BELGIUM (August 26, 2005) – Oki® Electric Industry Co., Ltd. (TSE: 6703, www.oki.com) of Tokyo, Japan, has successfully produced ICs in 0.5um/43V, 0.35um/16.5V, and 0.25um/25V process technologies using TakeCharge® design technology from Sarnoff Europe of Gistel, Belgium. Sarnoff is a diversified technology & services company with a long history of semiconductor innovations. “Under a technology transfer agreement, Oki has licensed silicon-proven TakeCharge devices customized specifically for our high-voltage processes. Our goal is to ensure that we can consistently manufacture chips that perform at high voltages with full electrostatic discharge (ESD) and latch-up protection,” said Mr. Shiratori, Deputy General Manager, Display Driver Division of Oki’s Silicon Solution Company. “We have implemented these TakeCharge devices in our various high volume products, such as LCD and OLED driver devices, where they deliver substantial added value for Oki and its customers.” TakeCharge technology is a design approach to on-chip ESD circuitry. It reduces the size of the I/O section on IC dies, while maintaining or improving on- chip protection against ESD. Implementing robust ESD protection devices is an important part of IC design. “We’re very pleased that an industry leader like Oki has chosen TakeCharge for its new line of high-voltage ICs,” said Koen Verhaege, Managing Director of Sarnoff”s Integrated Circuit Systems & Services business unit and Executive Director of Sarnoff Europe. -

Roundtable Meeting with Stakeholders Reducing the Environmental Impact of Semiconductor Production Equipment

H ighlights Roundtable Meeting with Stakeholders Reducing the Environmental Impact of Semiconductor Production Equipment The Tokyo Electron Group regards reducing the environmental impact of its semiconductor production equipment delivered to customers’ factories as one of its major social responsibilities. We invited three people from semiconductor manufacturers who are our customers to attend a roundtable meeting with our employees engaged in sales and equipment development. At the meeting, participants discussed the Group’s challenges and expectations from its customers, focusing on energy-saving equipment. Sharing Information with Semiconductor it contributed to energy efficiency and yield at your factory? Manufacturers Is Essential for Developing Energy- Mr. Kagino: Certainly there is a question of whether or not you can Saving Equipment obtain that kind of information, and even if you did, other semi- Mr. Ibuka (TEL): In recent years, environment-conscious design conductor manufacturers might not accept the same improve- has been attracting much attention. In particular, there are strong ment method. There have been cases where an improvement ini- demands for improvements in energy efficiency, and so the Tokyo tiative that worked well at Factory A for a certain semiconductor man- Electron Group is trying to contribute to the earth and society by pro- ufacturer did not work or was not accepted at the same manufac- viding more energy-efficient equipment. Today, we would like to ask turer‘s Factory B. As the background to this, semiconductor pro- you, the users of our equipment, for your honest opinions. We duction equipment is customized for each customer. However, I think will incorporate your opinions into future product development. -

NOTICE of FISCAL YEAR 2018 (The 55Th FY) ANNUAL GENERAL MEETING of SHAREHOLDERS

㻝㻌 World Headquarters 3-1 Akasaka 5-chome, Minato-ku Tokyo 107-6325, Japan ISIN JP3571400005 Tel:+81-3-5561-7000 SEDOL 6895675 TSE 8035 May 28, 2018 NOTICE OF FISCAL YEAR 2018 (the 55th FY) ANNUAL GENERAL MEETING OF SHAREHOLDERS To Our Shareholders: We are pleased to announce that the 55th Annual General Meeting of Shareholders (the “AGM”) of Tokyo Electron Ltd. (“TEL”) will be held on Tuesday, June 19, 2018, at 10:00 a.m. Japan standard time, at PALACE HOTEL TOKYO, located at 1-1 Marunouchi 1-chome, Chiyoda-ku, Tokyo. Shareholders will also be asked to vote upon the following Agenda: 1: Election of Twelve Corporate Directors 2: Payment of Bonuses to Corporate Directors for the 55th Fiscal Year 3: Issuance of Share Subscription Rights as Stock-Based Compensation to Corporate Directors 4: Issuance of Share Subscription Rights as Stock-Based Compensation to Executives of the Company and its Subsidiaries 5: Introduction of a Stock Compensation System as Medium-term Performance-linked Compensation for Corporate Directors of the Company As part of our ongoing effort to improve the quality of communications with our foreign investors and to increase the participation of those investors and to exercise your voting rights at the AGM, Tokyo Electron Ltd. has appointed IR Japan, Inc. as our Global Information Agent in connection with the shareholder meeting. We realize that many shareholders do not vote at Japanese Shareholders Meeting due to the volume of meetings and timing concerns. Therefore, we attach special importance to your vote, and hope that you will continue to distinguish yourselves from many institutions, who, unfortunately, do not participate.