PDF Download [1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Japanese Manufacturing Affiliates in Europe and Turkey

06-ORD 70H-002AA 7 Japanese Manufacturing Affiliates in Europe and Turkey - 2005 Survey - September 2006 Japan External Trade Organization (JETRO) Preface The survey on “Japanese manufacturing affiliates in Europe and Turkey” has been conducted 22 times since the first survey in 1983*. The latest survey, carried out from January 2006 to February 2006 targeting 16 countries in Western Europe, 8 countries in Central and Eastern Europe, and Turkey, focused on business trends and future prospects in each country, procurement of materials, production, sales, and management problems, effects of EU environmental regulations, etc. The survey revealed that as of the end of 2005 there were a total of 1,008 Japanese manufacturing affiliates operating in the surveyed region --- 818 in Western Europe, 174 in Central and Eastern Europe, and 16 in Turkey. Of this total, 291 affiliates --- 284 in Western Europe, 6 in Central and Eastern Europe, and 1 in Turkey --- also operate R & D or design centers. Also, the number of Japanese affiliates who operate only R & D or design centers in the surveyed region (no manufacturing operations) totaled 129 affiliates --- 125 in Western Europe and 4 in Central and Eastern Europe. In this survey we put emphasis on the effects of EU environmental regulations on Japanese manufacturing affiliates. We would like to express our great appreciation to the affiliates concerned for their kind cooperation, which have enabled us over the years to constantly improve the survey and report on the results. We hope that the affiliates and those who are interested in business development in Europe and/or Turkey will find this report useful. -

Sony Kabushiki Kaisha

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 20-F n REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 or ¥ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended March 31, 2010 or n TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from/to or n SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report: Commission file number 1-6439 Sony Kabushiki Kaisha (Exact Name of Registrant as specified in its charter) SONY CORPORATION (Translation of Registrant’s name into English) Japan (Jurisdiction of incorporation or organization) 7-1, KONAN 1-CHOME, MINATO-KU, TOKYO 108-0075 JAPAN (Address of principal executive offices) Samuel Levenson, Senior Vice President, Investor Relations Sony Corporation of America 550 Madison Avenue New York, NY 10022 Telephone: 212-833-6722, Facsimile: 212-833-6938 (Name, Telephone, E-mail and/or Facsimile Number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of Each Class Name of Each Exchange on Which Registered American Depositary Shares* New York Stock Exchange Common Stock** New York Stock Exchange * American Depositary Shares evidenced by American Depositary Receipts. Each American Depositary Share represents one share of Common Stock. ** No par value per share. Not for trading, but only in connection with the listing of American Depositary Shares pursuant to the requirements of the New York Stock Exchange. -

IMX294CJK Diagonal 21.63 Mm (Type 4/3) Approx

IMX294CJK Diagonal 21.63 mm (Type 4/3) Approx. 10.71M-Effective Pixel Color CMOS Image Sensor High-Sensitivity Type 4/3 CMOS Image Sensor that Supports 4K for Security Camera and Industrial Applications Sony Semiconductor Solutions Corporation has commercial- 10-bit output mode). In addition, use of a large-size pixel ized the "IMX294CJK" Type 4/3 back-illuminated CMOS image achieves SNR1s of 0.14 lx*1, and use of a Quad Bayer pixel sensor with approximately 10.71M-effective pixels for the structure (see Figure 1) realizes an HDR (High Dynamic expanding security camera market. Range) function with no time difference, enabling video imag- The "IMX294CJK" is the first in-house image sensor for security ing with a wide dynamic range. cameras to adopt the Type 4/3 format, and realizes output of *1: Low illuminance performance index advocated by Sony for image sensors for industrial the number of pixels needed for 4K at 120 frame/s (in ADC applications ■ Large-size optical format (Type 4/3) *Exmor R is a trademark of Sony Corporation. The Exmor R is a Sony's CMOS image sensor with significantly ■ Supports 4K output at 120 frame/s enhanced imaging characteristics including sensitivity and low noise by changing fundamental structure of ExmorTM pixel adopted column parallel A/D converter to back-illuminated type. ■ High sensitivity (SNR1s = 0.14 lx) ■ High-speed interfaces (CSI-2/SLVS-EC*2) ■ Supports Quad Bayer Coding HDR *STARVIS is a trademark of Sony Corporation. The STARVIS is back-illuminated pixel technology for CMOS image sensors for surveillance camera applications. -

Fujitsu Data Book 2008.10

History of Fujitsu ●Business Developments● ●Product Development● Jun 20, 1935 1935 ~ ◦Fuji Tsushinki Manufacturing Corporation, the company that later becomes Fujitsu Limited, is born as an Aug 1937 offshoot of the communications division ◦Fuji Tsushinki Manufacturing Corporation becomes Japanese Ministry of Fuji Electric. The new company is of Telecommunications-designated company for production of carrier capitalized at ¥3 million and has 700 equipment. employees. The first president was ◦Delivery of first carrier equipment order to South Manchuria Railways Manjiro Yoshimura, then president of Co. Fuji Electric. 1940 Sep 1938 ◦Delivery of the first Japanese-made T-type automatic telephone ◦Groundbreaking begins for construction of a new plant switchboard to the Nara Telephone Exchange. in Nakahara Ward, Kawasaki City, on the site of the present Kawasaki Research & Manufacturing Facilities. Dec 1945 ◦Fuji Tsushinki is granted government recognition by Japanese Ministry of Telecommunications as an officially approved telephone developer and manufacturer. May 1951 ◦Production of electronic computing machines begins. Apr 1942 ◦Suzaka Plant opens for mass production of telephones. Aug 1953 ◦Manufacture of radio communications equipment begins (Kawasaki Nov 1944 Plant). ◦Kanaiwa Kousakusho Co., Ltd. (now Fujitsu Frontech Limited) becomes part of the Fujitsu Group. Apr 1954 ◦Production of electronic devices begins (Kawasaki Plant). May 1949 ◦Stock is listed on the newly reopened Tokyo Stock Oct 1954 Exchange. ◦Japan’s first relay-type, automated electronic computer, the FACOM 100, is completed. Jun 1957 ◦Shinko Electric Industries Co., Ltd. becomes part of the Dec 1956 Fujitsu Group. ◦Japan's first NC is completed. Nov 1959 Sep 1958 ◦Oyama Plant opens for mass production of radio ◦First FACOM200 parametron computer is completed. -

Fujitsu to Split Off HDD Business in Reorganization

Fujitsu Limited Fujitsu to Split Off HDD Business in Reorganization Tokyo, May 21, 2009 – Fujitsu Limited (“Fujitsu”) today announced that it will split off its hard disk drive business (“HDD business”) and merge the business into its wholly owned subsidiary, Toshiba Storage Device Corporation (“Toshiba Storage Device”), through a simple absorption-type separation, on July 1, 2009. In a transaction scheduled for July 1, 2009, Fujitsu will then sell 80.1 percent of its shares of Toshiba Storage Device to Toshiba Corporation (“Toshiba”). By the end of December 2010, Fujitsu plans to sell its remaining 19.9 percent to Toshiba, at which point Toshiba Storage Device will become a wholly owned subsidiary of Toshiba. 1. Objectives of the Corporate Split On April 30, 2009, Fujitsu Limited signed a definitive agreement with Toshiba to transfer ownership of its HDD business. This corporate split is part of the implementation of the ownership transfer. 2. Outline of the Corporate Split (1) Schedule May 21, 2009 Signing of corporate split contract July 1, 2009 (scheduled) Effective date of corporate split This corporate split, pursuant to Article 784 (3) of the Corporate Law, will be executed without the requirement of the approval of a General Meeting of the Shareholders as stipulated under Article 783 (1) of the Corporate Law (Simple Absorption-type Separations). (2) Method Fujitsu will be the transferor company and Toshiba Storage Device will be the successor company (Simple Separation). (3) Decrease in Capital or Other, Resulting from the Corporate Split There will be no decrease in capital or other, resulting from the corporate split. -

Enhancing System Solutions

Enhancing System Solutions FUJITSU MICROELECTRONICS EUROPE Enhancing System Solutions Services Automotive Multimedia Mobile Communications Networking/Telecoms Here at Fujitsu Microelectronics Europe (FME) we are engaged in an on-going program of responding to the changing nature of the “European market. We provide state-of-the-art semiconductor devices and leading-technology plasma and liquid crystal display panels. But, more than that, we endeavor to develop systems solutions in partnership with our customers while at the same time, we try to broaden the scope of our operation and genuinely add value wherever possible. The global perspective Fujitsu is a world leader in customer-oriented IT and communications solutions concentrated on three areas: software & services, hardware platforms and electronic devices. Our global goal is to focus on customer needs, quality, timeliness and management speed. 25 years of experience in Europe Over the past 25 years we have established ourselves in the major European markets of Automotive, Networking/Telecoms, Mobile Communications, Multimedia and Industrial & Home appliances through a special blend of technical experience and applied expertise. What’s more, FME continues to drive technologies forward to meet the ever-increasing demands of tomorrow's applications – in which Europe leads the world! ” Shimpei Hirata President Fujitsu Microelectronics Europe GmbH Dreieich-Buchschlag / Frankfurt / Germany 2 Industrial & Home Appliances Flat Panel Displays Quality Environment Local Support European Offices Enhancing System Solutions ujitsu’s traditional corporate strengths, in markets ranging from together with re-use of intellectual property and a company-wide Finformation technology to telecommunications and from displays system solution focus, benefits the fastest-growing sectors of the to semiconductors, have helped it become one of the world’s leading information age. -

CORPORATE DIRECTORY (As of June 28, 2000)

CORPORATE DIRECTORY (as of June 28, 2000) JAPAN TOKYO ELECTRON KYUSHU LIMITED TOKYO ELECTRON FE LIMITED Saga Plant 30-7 Sumiyoshi-cho 2-chome TOKYO ELECTRON LIMITED 1375-41 Nishi-Shinmachi Fuchu City, Tokyo 183-8705 World Headquarters Tosu City, Saga 841-0074 Tel: 042-333-8411 TBS Broadcast Center Tel: 0942-81-1800 District Offices 3-6 Akasaka 5-chome, Minato-ku, Tokyo 107-8481 Kumamoto Plant Osaka, Kumamoto, Iwate, Tsuruoka, Sendai, Tel: 03-5561-7000 2655 Tsukure, Kikuyo-machi Aizuwakamatsu, Takasaki, Mito, Nirasaki, Toyama, Fax: 03-5561-7400 Kikuchi-gun, Kumamoto 869-1197 Kuwana, Fukuyama, Higashi-Hiroshima, Saijo, Oita, URL: http://www.tel.co.jp/tel-e/ Tel: 096-292-3111 Nagasaki, Kikuyo, Kagoshima Regional Offices Ozu Plant Fuchu Technology Center, Osaka Branch Office, 272-4 Takaono, Ozu-machi TOKYO ELECTRON DEVICE LIMITED Kyushu Branch Office, Tohoku Regional Office, Kikuchi-gun, Kumamoto 869-1232 1 Higashikata-cho, Tsuzuki-ku Yamanashi Regional Office, Central Research Tel: 096-292-1600 Yokohama City, Kanagawa 224-0045 Laboratory/Process Technology Center Koshi Plant Tel: 045-474-7000 Sales Offices 1-1 Fukuhara, Koshi-machi Sales Offices Sendai, Nagoya Kikuchi-gun, Kumamoto 861-1116 Utsunomiya, Mito, Kumagaya, Kanda, Tachikawa, Tel: 096-349-5500 Yamanashi, Matsumoto, Nagoya, Osaka, Fukuoka TOKYO ELECTRON TOHOKU LIMITED Tohoku Plant TOKYO ELECTRON MIYAGI LIMITED TOKYO ELECTRON LEASING CO., LTD. 52 Matsunagane, Iwayado 1-1 Nekohazama, Nemawari, Matsushima-machi 30-7 Sumiyoshi-cho 2-chome Esashi City, Iwate 023-1101 Miyagi-gun, Miyagi -

INVESTORS GUIDE 2019 Osaka Office to Our Shareholders and Investors Fukuoka Sales Office Shinjuku Office Shinjuku Support Center Tachikawa Sales Office

TOKYO ELECTRON DEVICE LIMITED Securities code: 2760 Business Locations (As of July 1, 2019) Business Location Domestic Subsidiary Omiya Sales Office Matsumoto Sales Office Sendai Sales Office Tsukuba Sales Office Iwaki Sales Office Nagoya Sales Office Mito Sales Office Kyoto Sales Office INVESTORS GUIDE 2019 Osaka Office To Our Shareholders and Investors Fukuoka Sales Office Shinjuku Office Shinjuku Support Center Tachikawa Sales Office Engineering Center Headquarters (Yokohama) FAST CORPORATION (Yamato-city, Kanagawa prefecture) TOKYO ELECTRON DEVICE Mishima Sales Office NAGASAKI LTD. Hamamatsu Sales Office (Isahaya-city, Nagasaki prefecture) Business/Marketing location Overseas Design and development location Dalian Yokohama Ottawa Seoul Silicon Valley Shanghai Taipei Shenzhen Bangkok Wuxi Hong Kong Singapore Philippines Note on forward-looking statements This Investors Guide was prepared on July 1, 2019. Forward looking statements, including business strategies and business forecasts, were made by the Company’s management, based on information available at that time, and may be revised due to changes in the business environment. Therefore, please be advised that the Company cannot guarantee the accuracy or the reliability of the statements. For the latest information, please refer to our information releases or our website. Note also that product and service names remain the trademarks of their respective owners. Corporate Communications Dept. https://www.teldevice.co.jp World Headquarters Yokohama East Square, 1-4 Kinko-cho, Kanagawa-ku,Yokohama -

ISSM2020 –International Symposium on Semiconductor Manufacturing SPONSORSHIP December 15-16, 2020, Tokyo, Japan

ISSM2020 –International Symposium on Semiconductor Manufacturing SPONSORSHIP December 15-16, 2020, Tokyo, Japan Shozo Saito Chairman, ISSM2020 Organizing Committee Device & System Platform Development Center Co., Ltd. Shuichi Inoue, ATONARP INC. It is our great pleasure to announce that The 28th annual International Symposium on Semiconductor Manufacturing (ISSM) 2020 will be held on December 15-16, 2020 at KFC Hall, Ryogoku, Tokyo in cooperation with e-Manufacturing & Design Collaboration Symposium (eMDC) which is sponsored by TSIA with support from SEMI and GSA. The program will feature keynote speeches by world leading speakers, timely and highlighted topics and networking sessions focusing on equipment/materials/software/services with suppliers' exhibits. ISSM continues to contribute to the growth of the semiconductor industry through its infrastructure for networking, discussion, and information sharing among the world's professionals. We would like you to cooperate with us by supporting the ISSM 2020. Please see the benefit of ISSM2020 sponsorship. Conference Overview Date: December 15-16, 2020 Location: KFC (Kokusai Fashion Center) Hall 1-6-1 Yokoami Sumidaku, Tokyo 130-0015 Japan +81-3-5610-5810 Co-Sponsored by: IEEE Electron Devices Society Minimal Fab Semiconductor Equipment Association of Japan (SEAJ) Semiconductor Equipment and Materials International (SEMI) Taiwan Semiconductor Industry Association (TSIA) Endorsement by: The Japan Society of Applied Physics Area of Interest: Fab Management Factory Design & Automated Material -

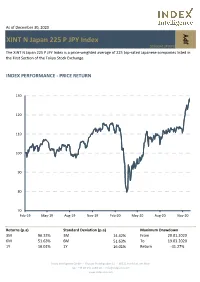

XINT N Japan 225 P JPY Index

As of December 30, 2020 XINT N Japan 225 P JPY Index JPY DE000A13PWP8 The XINT N Japan 225 P JPY Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. INDEX PERFORMANCE - PRICE RETURN 130 120 110 100 90 80 70 Feb-19 May-19 Aug-19 Nov-19 Feb-20 May-20 Aug-20 Nov-20 Returns (p.a) Standard Deviation (p.a) Maximum Drawdown 3M 96.33% 3M 14.42% From 20.01.2020 6M 51.63% 6M 51.63% To 19.03.2020 1Y 16.01% 1Y 16.01% Return -31.27% Index Intelligence GmbH - Grosser Hirschgraben 15 - 60311 Frankfurt am Main Tel.: +49 69 247 5583 50 - [email protected] www.index-int.com Top 10 Constituents FFMV (JPYm) Weight % Industry Sector Fast Retailing Co Ltd 5 12.13 Retail SoftBank Group Corp 2 6.34 Telecommunications Tokyo Electron Ltd 2 5.04 Technology FANUC Corp 1 3.33 Industrial Goods & Services M3 Inc 1 3.07 Health Care Daikin Industries Ltd 1 3.01 Construction & Materials KDDI Corp 1 2.41 Telecommunications Shin-Etsu Chemical Co Ltd 1 2.37 Chemicals Terumo Corp 1 2.26 Health Care Chugai Pharmaceutical Co Ltd 1 2.17 Health Care Total 16 42.13 This information has been prepared by Index Intelligence GmbH (“IIG”). All information is provided "as is" and IIG makes no express or implied warranties, and expressly disclaims all warranties of merchantability or fitness for a particular purpose or use with respect to any data included herein. -

PUBLIC SUBMISSION Posted: November 20, 2020 Tracking No

Page 1 of 2 As of: 11/23/20 10:03 AM Received: November 18, 2020 Status: Posted PUBLIC SUBMISSION Posted: November 20, 2020 Tracking No. 1k4-9k60-8cjw Comments Due: December 03, 2020 Submission Type: Web Docket: PTO-C-2020-0055 Request for Comments on Discretion to Institute Trials Before the Patent Trial and Appeal Board Comment On: PTO-C-2020-0055-0001 Discretion to Institute Trials Before the Patent Trial and Appeal Board Document: PTO-C-2020-0055-0452 Comment from Japan Business Machine and Information System Industries Association Submitter Information Name: Hideaki Chishima Address: Lila Hijirizaka 7FL 3-4-10, Mita Minato-ku, Tokyo, Japan, 1080073 Email: [email protected] Phone: +81-3-6809-5495 Fax: +81-3-3451-1770 Submitter's Representative: Hideki Sanatake Organization: Japan Business Machine and Information System Industries Association General Comment Dear Sir, This post is for Japan Business Machine and Information System Industries Association (JBMIA) to submit its comments in response to solicitation of public comments by USPTO as announced in Federal Register / Docket No. PTO-C-2020-0055. The comments are attached hereto. JBMIA is a Japanese incorporated association which was renamed in 2002 from Japan Business Machine Makers Association established originally in 1960. JBMIA consists of 40 member companies engaged in business machine and information system and 5 supporting companies. Almost all of the member companies have actively filed patent applications in the USA. https://www.fdms.gov/fdms/getcontent?objectId=0900006484967b2a&format=xml&sho... 11/23/2020 Page 2 of 2 Sincerely, Hideaki Chishima (Mr) Intellectual Property Committee Secretariat Attachments JBMIA Comment (finnal) https://www.fdms.gov/fdms/getcontent?objectId=0900006484967b2a&format=xml&sho.. -

Quick Print Station (ASK-300)

Tentative The Best All-in-one System! You can start a photo business easily with this affordable, all-in-one solution. Small Initial Investment Compact Size Variety of Photo Finishing Formats Small Initial Investment Variety of Photo Finishing Formats All-in-one solution at an affordable price. Standard, ID and template The kiosk includes: ready photo formats available. Printer Photo formatting selection is Order terminal easy for everyone, using the Fujifilm software on-screen step-by-step guide. Compact Size & Easy Maintenance High Quality Prints Increase Shop’s Efficiency Outstanding image quality is realized by matching our This compact system is suitable for any retail environment. Image IntelligenceTM processing technology* with Easy loading of paper and replacing of ink ribbons in less than FUJIFILM Quality Thermal Photo Paper. 3 minutes. Adjustable display angle FUJIFILM Dye-sublimation Compact Kiosk System "Quick Print Station" Specifications Display 10.4 inch Touch Panel Display (800 x 600 pixel) OS: Windows XP Embedded (English) PC Unit CPU: Intel Atom N455 (1.6GHz) Memory: DDR3 SO-DIMM (1GB) HDD: 160GB (SATA) 275 mm Wireless LAN: Option Wireless BlueTooth (IEEE 802.15.1) : Option 445 mm Device (LAN port) Option Optical External Device (CD/DVD) Option (USB Connection) 170 mm PC Dimensions (W x D x H) 275 x 295 x 70-275 mm/10.8 x 11.6 x 2.8-10.8 inch (DPC Portable) Weight (approx.) 3.5 kg/7.7 lb Input media SD Memory Card, MicroSD Card, Memory Stick, 275 mm 446 mm Memory Stick Micro, xD-Picture Card, CompactFlash, USB Flash Memory Power Consumption 100-240V AC50/60 Hz Consumables Lineup Interface USB 2.0 x 4 ports (Type A) Print size Description Number of prints per Box Printing speed (approx) Standard Print 3.5 x 5 inch T RL-CF900 900 prints 11.2 seconds/print ID Photo 4 x 6 inch T RK-CF800 800 prints 12.3 seconds/print Frame photo 5 x 7 inch T R2L-CF460 460 prints 19.0 seconds/print Service & Function Edit (Crop, Rotate) 6 x 8 inch T R68-CF400 400 prints · Not include data transfering time.