Dealing with Debt How to Wind up Your Own Company Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

All You Need to Know About Becoming an Insolvency Practitioner In

REMUNERATION OF INSOLVENCY PRACTITIONERS This time we bring you a real scoop. Insolvency law, legal status and remuneration of the insolvency practitioners, has completely changed in Poland! Judge Anna Hrycaj, who presented this subject at the ACC conference in Warsaw last year, and who was asked to adapt her presentation to the needs of our journal, was obliged to write a new article, because Poland was surprised a couple of weeks ago by a new law… So, we are proud to offer you an analysis of the new requirements for becoming an IP in Poland. If you have any questions, please write to [email protected] or [email protected] for further information. All you need to know about becoming an Insolvency Practitioner in Europe: Poland We have already looked at the legal status and remuneration of insolvency practitioners in France, Austria and Latvia. Here we discuss what happens in Poland The legal status of the Insolvency and the court does not deprive the • He/she has the full legal capacity to act; Practitioner (IP) in Poland is soon to be debtor of the right to administer the • He/she is under 65; regulated not only by the provisions of estate; • He/she received higher education the Bankruptcy and Rehabilitation Law, • The receiver ( zarz ądca ), who is qualifications and obtained an MA or 28 February 2003, but also by the appointed in the case of insolvency any other correspondent title in the provisions of the Polish law on IPs which with the possibility of making an member states mentioned above; was enacted by the Polish Parliament on arrangement with creditors, but the • He/she has an unblemished 9 May 2007. -

CVA" Stands for a Number of Things, Including "Cerebro

COMPANY VOLUNTARY ARRANGEMENTS Michael Howlin, Q.C. Hastie Stable, Edinburgh 1. Introduction 1.1 The abbreviation "CVA" stands for a number of things, including "cerebro- vascular accident" (i.e., a stroke), "Creative Video Associations" (a company which recycles videotape), an organisation called "Croydon Voluntary Action", "credit value adjustment" (or indeed "counterparty valuation adjustment") in the context of banking, and a device known as a "controlled valve actuator". It also stands for "company voluntary arrangement", which is the subject-matter of this talk. 1.2 Recent high-profile examples of CVAs include those proposed by (the late) JJB Sports (for the second time), Blacks, Clinton Cards, PT McWilliams (a Northern Ireland engineering company), Oddbins (no explanation needed), Carvill Group (a Northern Ireland construction company) and McTavish 2 Ramsay, the Dundee door manufacturers. Even more recently, we have had the failed Glasgow Rangers CVA and CVAs for Travelodge and Fitness First. 2. The General Statutory Background 2.1 CVAs were created by the Insolvency Act 1986, which devoted all of seven sections to them. Since 2003, they have been governed by slightly expanded primary statutory provisions1 and a new Schedule (Schedule A1) to which I shall return shortly. There are also provisions in Part I of the Insolvency (Scotland) Rules 1986, as amended. 2.2 Section 1(1) defines a voluntary arrangement simply as "a composition in satisfaction of [the company's] debts or a scheme of arrangement of its affairs2". In practice, a CVA is a very flexible affair, the details of which will vary from case to case. Examples of what can be achieved by a CVA include: (1) unconditional foregiveness of debts, or certain classes of debts; (2) pro rata reduction (or partial reduction) of liabilities, or certain classes of liabilities; (3) other variations of liabilities (e.g. -

How to Become an Insolvency Practitioner In

REMUNERATION OF INSOLVENCY PRACTITIONERS The article is provided by Devorah Burns of the national organisation The Insolvency Service, based in London. The Insolvency Service operates under a statutory framework – mainly the Insolvency Acts 1986 and 2000, the Company Directors Disqualifications Act 1986 and the Employment Rights Act 1996. If you have any questions on this article, please send them to the author at Devorah.Burns @insolvency.gsi.gov.uk or [email protected] We welcome further contributions to this series, so if you would like to inform our readers of the regulations for becoming an IP in your jurisdiction, please contact the editors. All you need to know about becoming an Insolvency Practitioner: Great Britain The latest in our series of articles on the legal status and remuneration of insolvency practitioners examines the British rules and regulations Access to to pay an annual fee, which covers the costs Insolvency Practitioners in the profession associated with authorisation and England, Wales & Scotland. regulation. The Insolvency Service is responsible for The Secretary of State (SoS) may authorise EU Directive 2005/36 provides for the the regulation of insolvency practitioners insolvency practitioners, as may seven recognition of professional qualifications working in Great Britain (i.e. England, professional bodies (the RPBs). The RPBs throughout the relevant states and The Wales & Scotland) and the Department for represent accountants, lawyers and those European Communities (Recognition of Enterprise, Trade & Investment in Northern who only work as insolvency practitioners. Professional Qualifications) Regulations Ireland is responsible for the regulation Most insolvency practitioners are 2007 (The Regulations) make provision of insolvency practitioners who work in authorised by one of the RPBs. -

What a Creditor Needs to Know About Liquidating an Insolvent BVI Company

What a creditor needs to know about liquidating GUIDE an insolvent BVI company Last reviewed: October 2020 Contents Introduction 3 When is a company insolvent? 3 What is a statutory demand? 3 Written request for payment 3 Is it essential to serve a statutory demand? 3 What must a statutory demand say? 3 Setting aside a statutory demand 4 How may a company be put into liquidation? 4 Qualifying resolution 4 Appointment 4 Liquidator's powers 4 Court order 5 Who may apply? 5 Application 5 Debt should be undisputed 5 When does a company's liquidation start? 5 What are the consequences of a company being put into liquidation? 5 Assets do not vest in liquidator 5 Automatic consequences 5 Restriction on execution and attachment 6 Public documents 6 Other consequences 6 Effect on contracts 6 How do creditors claim in a company's liquidation? 7 Making a claim 7 Currency 7 Contingent debts 7 Interest 7 Admitting or rejecting claims 7 What is a creditors' committee? 7 Establishing the committee 7 2021934/79051506/1 BVI | CAYMAN ISLANDS | GUERNSEY | HONG KONG | JERSEY | LONDON mourant.com Functions 7 Powers 8 What is the order of distribution of the company's assets? 8 Pari passu principle 8 Excluded assets 8 Order of application 8 How are secured creditors affected by a company's liquidation? 8 General position 8 Liquidator challenge 8 Claiming in the liquidation 8 Who are preferential creditors? 9 Preferential creditors 9 Priority 9 What are the claims of current and past shareholders? 9 Do shareholders have to contribute towards the company's debts? -

The Insolvency Service Annual Plan 2019-2020

Annual Plan 2019-2020 Contents Chief Executive’s Foreword .................................................... 5 Chair of the Board’s Foreword ................................................ 6 1. Delivery framework .............................................................. 8 1.1 Strategic delivery ..................................................................................................................8 2. Ministerial targets .............................................................. 13 3. Delivering economic confidence ...................................... 14 3.1 Objectives ...........................................................................................................................14 3.2 Targets ................................................................................................................................15 4. Supporting those in financial distress .............................. 16 4.1 Objectives ...........................................................................................................................16 4.2 Targets ................................................................................................................................17 4.3 Change portfolio milestones ..............................................................................................17 5. Tackling financial wrongdoing .......................................... 18 5.1 Objectives ...........................................................................................................................18 -

UK (England and Wales)

Restructuring and Insolvency 2006/07 Country Q&A UK (England and Wales) UK (England and Wales) Lyndon Norley, Partha Kar and Graham Lane, Kirkland and Ellis International LLP www.practicallaw.com/2-202-0910 SECURITY AND PRIORITIES ■ Floating charge. A floating charge can be taken over a variety of assets (both existing and future), which fluctuate from 1. What are the most common forms of security taken in rela- day to day. It is usually taken over a debtor's whole business tion to immovable and movable property? Are any specific and undertaking. formalities required for the creation of security by compa- nies? Unlike a fixed charge, a floating charge does not attach to a particular asset, but rather "floats" above one or more assets. During this time, the debtor is free to sell or dispose of the Immovable property assets without the creditor's consent. However, if a default specified in the charge document occurs, the floating charge The most common types of security for immovable property are: will "crystallise" into a fixed charge, which attaches to and encumbers specific assets. ■ Mortgage. A legal mortgage is the main form of security interest over real property. It historically involved legal title If a floating charge over all or substantially all of a com- to a debtor's property being transferred to the creditor as pany's assets has been created before 15 September 2003, security for a claim. The debtor retained possession of the it can be enforced by appointing an administrative receiver. property, but only recovered legal ownership when it repaid On default, the administrative receiver takes control of the the secured debt in full. -

Lesson 13: Dissolution, Liquidation and Extinction of Companies

LESSON 13: DISSOLUTION, LIQUIDATION AND EXTINCTION OF COMPANIES SUMMARY: 1.-Dissolution a) Causes b) Requirements and procedure c) Advertising 2.-Liquidation a) Liquidation bodies b) Procedure 3.-Extinction 4.- Vocabulary 1.-Dissolution A company can be considered, on one hand, a contract signed by at least two people and, on the other hand, a legal person which has several legal relationships with third parties. In order to protect those third parties, as well as the company itself and its partners, the final extinction of a company should go through two different stages. The first one would be dissolution, in which the company continues to be a legal person but ceases its commercial purpose and starts the liquidation. The second one would be liquidation, in which the company compensates its credits and debts vis-à-vis third parties and distributes the corporate assets resulting from the liquidation among all shareholders. Once the liquidation procedure is finished, the registered entries of the dissolved company will be cancelled. From this moment, the company will be extinguished. CAUSES: Three different types of causes can be distinguished: a) Causes which lead to an automatic dissolution of the company (art. 360 LSC) Expiry of the term established in the articles of association of the company. In order to avoid dissolution in this case, a general meeting resolution will be required to extend the duration of the company agreement. When the company has not been converted, dissolved or its capital share has not been increased within a year after being obligated to reduce its share capital below the minimum amount established by law. -

Department for Business, Enterprise and Regulatory Reform (BERR) and the Department for Innovation, Universities and Skills (DIUS)

James Davies Clerk of the Committee Business Innovation and Skills Committee House of Commons 7 Millbank London SW1P 3JA 7 July 2010 Dear James Main Estimates Memorandum 2010-11 I am enclosing the Department for Business Innovation and Skills (BIS’s) Memorandum for the forthcoming Main Estimate. This Memorandum has been prepared in accordance with the “Guide to Preparing Estimate Memoranda” and has been approved by the Departmental Accounting Officer. Presentation and publication of the Main Estimate was made on 21 June 2010. I recognise that, as this is a new Committee, some of this information may require fuller explanation to bring members fully up to speed with the Department’s activities and funding. I will be happy to provide any additional information which may be required. Yours sincerely Howard Orme Director General, Finance and Commercial Finance and Commercial, 1 Victoria Street, London SW1H 0ET www.bis.gov.uk Direct Line +44 (0)20 7215 5936 | Fax +44 (0)20 7215 3248 | Mincom +44 (0)020 7215 6740 Enquiries +44 (0)20 7215 5000 | Email [email protected] 1 Department for Business Innovation and Skills Main Estimate 2010-11 Select Committee Memorandum 1. This is the first Main Estimate for the Department for Business Innovation and Skills (BIS). The principal activities of the Department relate to the funding, policy and support of Innovation, Business and Enterprise; Further and Higher education and Skills; and Science and Research. 2. The Main Estimate for 2010-11 seeks the necessary resources and cash to support the functions of the Department and its Non Departmental Public Bodies (NDPBs). -

Company Voluntary Arrangements: Evaluating Success and Failure May 2018

Company Voluntary Arrangements: Evaluating Success and Failure May 2018 Professor Peter Walton, University of Wolverhampton Chris Umfreville, Aston University Dr Lézelle Jacobs, University of Wolverhampton Commissioned by R3, the insolvency and restructuring trade body, and sponsored by ICAEW This report would not have been possible without the support and guidance of: Allison Broad, Nick Cosgrove, Giles Frampton, John Kelly Bob Pinder, Andrew Tate, The Insolvency Service Company Voluntary Arrangements: Evaluating Success and Failure About R3 R3 is the trade association for the UK’s insolvency, restructuring, advisory, and turnaround professionals. We represent insolvency practitioners, lawyers, turnaround and restructuring experts, students, and others in the profession. The insolvency, restructuring and turnaround profession is a vital part of the UK economy. The profession rescues businesses and jobs, creates the confidence to trade and lend by returning money fairly to creditors after insolvencies, investigates and disrupts fraud, and helps indebted individuals get back on their feet. The UK is an international centre for insolvency and restructuring work and our insolvency and restructuring framework is rated as one of the best in the world by the World Bank. R3 supports the profession in making sure that this remains the case. R3 raises awareness of the key issues facing the UK insolvency and restructuring profession and framework among the public, government, policymakers, media, and the wider business community. This work includes highlighting both policy issues for the profession and challenges facing business and personal finances. 2 Company Voluntary Arrangements: Evaluating Success and Failure Executive Summary • The biggest strength of a CVA is its flexibility. • Assessing the success or failure of CVAs is not straightforward and depends on a number of variables. -

Insolvency Review Insolvency Review

the Insolvency Review Insolvency Insolvency Review Sixth Edition Editor Donald S Bernstein Sixth Edition Sixth lawreviews © 2018 Law Business Research Ltd Insolvency Review Sixth Edition Reproduced with permission from Law Business Research Ltd This article was first published in November 2018 For further information please contact [email protected] Editor Donald S Bernstein lawreviews © 2018 Law Business Research Ltd PUBLISHER Tom Barnes SENIOR BUSINESS DEVELOPMENT MANAGER Nick Barette BUSINESS DEVELOPMENT MANAGERS Thomas Lee, Joel Woods SENIOR ACCOUNT MANAGER Pere Aspinall ACCOUNT MANAGERS Jack Bagnall, Sophie Emberson, Katie Hodgetts PRODUCT MARKETING EXECUTIVE Rebecca Mogridge RESEARCHER Keavy Hunnigal-Gaw EDITORIAL COORDINATOR Gavin Jordan HEAD OF PRODUCTION Adam Myers PRODUCTION EDITOR Martin Roach SUBEDITOR Helen Smith CHIEF EXECUTIVE OFFICER Paul Howarth Published in the United Kingdom by Law Business Research Ltd, London 87 Lancaster Road, London, W11 1QQ, UK © 2018 Law Business Research Ltd www.TheLawReviews.co.uk No photocopying: copyright licences do not apply. The information provided in this publication is general and may not apply in a specific situation, nor does it necessarily represent the views of authors’ firms or their clients. Legal advice should always be sought before taking any legal action based on the information provided. The publishers accept no responsibility for any acts or omissions contained herein. Although the information provided is accurate as of September 2018, be advised that this is -

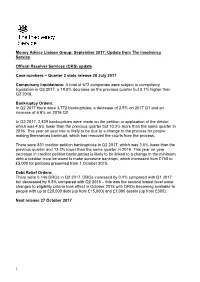

Update from the Insolvency Service

Money Advice Liaison Group: September 2017: Update from The Insolvency Service Official Receiver Services (ORS) update Case numbers – Quarter 2 stats release 28 July 2017 Compulsory liquidations: A total of 672 companies were subject to compulsory liquidation in Q2 2017, a 19.8% decrease on the previous quarter but 0.1% higher than Q2 2016. Bankruptcy Orders: In Q2 2017 there were 3,772 bankruptcies, a decrease of 2.5% on 2017 Q1 and an increase of 4.6% on 2016 Q2. In Q2 2017, 2,839 bankruptcies were made on the petition or application of the debtor, which was 4.6% lower than the previous quarter but 10.3% more than the same quarter in 2016. This year on year rise is likely to be due to a change to the process for people making themselves bankrupt, which has removed the courts from the process. There were 831 creditor petition bankruptcies in Q2 2017, which was 3.6% lower than the previous quarter and 13.3% lower than the same quarter in 2016. This year on year decrease in creditor petition bankruptcies is likely to be linked to a change in the minimum debt a creditor must be owed to make someone bankrupt, which increased from £750 to £5,000 for petitions presented from 1 October 2015. Debt Relief Orders: There were 6,146 DROs in Q2 2017. DROs increased by 0.4% compared with Q1 2017 but decreased by 8.8% compared with Q2 2016 – this was the second lowest level since changes to eligibility criteria took effect in October 2015 with DROs becoming available to people with up to £20,000 debt (up from £15,000) and £1,000 assets (up from £300). -

Department for Business, Enterprise and Regulatory Reform Annual Report and Accounts 2007-08

Department for Business, Enterprise and Regulatory Reform Annual Report and Accounts 2007-08 Including the Annual Departmental Report and Consolidated Resource Accounts for the year ended 31 March 2008 Presented to Parliament pursuant to the Government Resources and Accounts Act 2000 c.20, s.6 (4) Ordered by the House of Commons to be printed 21 July 2008 London: The Stationery Office HC 757 £33.45 © Crown Copyright 2008 The text in this document (excluding the Royal Arms and other departmental or agency logos) may be reproduced free of charge in any format or medium providing it is reproduced accurately and not used in a misleading context. The material must be acknowledged as Crown copyright and the title of the document specified. Where we have identified any third party copyright material you will need to obtain permission from the copyright holders concerned. For any other use of this material please write to Office of Public Sector Information, Information Policy Team, Kew, Richmond, Surrey TW9 4DU or e-mail: [email protected] ISBN: 978 0 10295 7112 3 Contents Foreword from the Secretary of State 5 Executive Summary 7 About this report 9 Chapter 1: Introducing the Department 1.1 The Department for Business, Enterprise and Regulatory Reform 11 1.2 Structure and Ministerial responsibilities 12 1.3 Strategy and objectives 13 1.4 Being the Voice for Business across Government 16 Chapter 2: Performance Report 2.1 Introduction 19 2.2 Summary of performance 21 2.3 Raising the productivity of the UK economy 25 2.4 Promoting the creation