Irish Examinership: Post-Eircom a Look at Ireland's Fastest and Largest

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Judgment Claims in Receivership Proceedings*

JUDGMENT CLAIMS IN RECEIVERSHIP PROCEEDINGS* JOHN K. BEACH Connecticuf Supreme Court of Errors In view of the importance of the subject it is unfortunate that so few of the reported cases on equitable receiverships of corporations have dealt in any comprehensive way with the principles underlying the administrating of the fund for the benefit of creditors. The result is that controversy has outstripped authoritative decision, and the subject is unsettled. To this generalization an exception must be noted in respect of the special topic of the application of current rail- way income to current expenses, before the payment of mortgage 1 indebtedness. On another disputed topic, the provability of imma.ure claims, the law, or at least the right principle of decision, has been settled, by the notable opinion of Judge Noyes in Pennsylvania Steel Company v. New York City Railway Company,2 followed and rein- forced by that of Mr. Justice Holmes in William Filene'sSons Company v. Weed.' Notwithstanding these important exceptions, the dearth of authority on the general subject is such that Judge Noyes refers to a case cited in his opinion as "almost the only case in which rules have "been formulated with respect to the provability of claims against "insolvent corporations."4 Upon the particular phase of the subject here discussed, the decisions are to some extent in conflict, and no attempt seems to have been made in text books or decisions to examine the question in the light of principle. Black, for example, dismisses the subject by saying it. is generally conceded that a receiver and the corporation whose property is under his charge "are so far in privity that a judgment against the * This paper deals only with judgments against the defendant in the receiver- ship, regarded as evidence of the validity and amount of the judgment creditor's claims for dividends to be paid out of the fund in the receiver's hands. -

All You Need to Know About Becoming an Insolvency Practitioner In

REMUNERATION OF INSOLVENCY PRACTITIONERS This time we bring you a real scoop. Insolvency law, legal status and remuneration of the insolvency practitioners, has completely changed in Poland! Judge Anna Hrycaj, who presented this subject at the ACC conference in Warsaw last year, and who was asked to adapt her presentation to the needs of our journal, was obliged to write a new article, because Poland was surprised a couple of weeks ago by a new law… So, we are proud to offer you an analysis of the new requirements for becoming an IP in Poland. If you have any questions, please write to [email protected] or [email protected] for further information. All you need to know about becoming an Insolvency Practitioner in Europe: Poland We have already looked at the legal status and remuneration of insolvency practitioners in France, Austria and Latvia. Here we discuss what happens in Poland The legal status of the Insolvency and the court does not deprive the • He/she has the full legal capacity to act; Practitioner (IP) in Poland is soon to be debtor of the right to administer the • He/she is under 65; regulated not only by the provisions of estate; • He/she received higher education the Bankruptcy and Rehabilitation Law, • The receiver ( zarz ądca ), who is qualifications and obtained an MA or 28 February 2003, but also by the appointed in the case of insolvency any other correspondent title in the provisions of the Polish law on IPs which with the possibility of making an member states mentioned above; was enacted by the Polish Parliament on arrangement with creditors, but the • He/she has an unblemished 9 May 2007. -

Self-Represented Creditor

UNITED STATES BANKRUPTCY COURT DISTRICT OF MASSACHUSETTS A GUIDE FOR THE SELF-REPRESENTED CREDITOR IN A BANKRUPTCY CASE June 2014 Table of Contents Subject Page Number Legal Authority, Statutes and Rules ....................................................................................... 1 Who is a Creditor? .......................................................................................................................... 1 Overview of the Bankruptcy Process from the Creditor’s Perspective ................... 2 A Creditor’s Objections When a Person Files a Bankruptcy Petition ....................... 3 Limited Stay/No Stay ..................................................................................................... 3 Relief from Stay ................................................................................................................ 4 Violations of the Stay ...................................................................................................... 4 Discharge ............................................................................................................................. 4 Working with Professionals ....................................................................................................... 4 Attorneys ............................................................................................................................. 4 Pro se ................................................................................................................................................. -

How to Become an Insolvency Practitioner In

REMUNERATION OF INSOLVENCY PRACTITIONERS The article is provided by Devorah Burns of the national organisation The Insolvency Service, based in London. The Insolvency Service operates under a statutory framework – mainly the Insolvency Acts 1986 and 2000, the Company Directors Disqualifications Act 1986 and the Employment Rights Act 1996. If you have any questions on this article, please send them to the author at Devorah.Burns @insolvency.gsi.gov.uk or [email protected] We welcome further contributions to this series, so if you would like to inform our readers of the regulations for becoming an IP in your jurisdiction, please contact the editors. All you need to know about becoming an Insolvency Practitioner: Great Britain The latest in our series of articles on the legal status and remuneration of insolvency practitioners examines the British rules and regulations Access to to pay an annual fee, which covers the costs Insolvency Practitioners in the profession associated with authorisation and England, Wales & Scotland. regulation. The Insolvency Service is responsible for The Secretary of State (SoS) may authorise EU Directive 2005/36 provides for the the regulation of insolvency practitioners insolvency practitioners, as may seven recognition of professional qualifications working in Great Britain (i.e. England, professional bodies (the RPBs). The RPBs throughout the relevant states and The Wales & Scotland) and the Department for represent accountants, lawyers and those European Communities (Recognition of Enterprise, Trade & Investment in Northern who only work as insolvency practitioners. Professional Qualifications) Regulations Ireland is responsible for the regulation Most insolvency practitioners are 2007 (The Regulations) make provision of insolvency practitioners who work in authorised by one of the RPBs. -

What a Creditor Needs to Know About Liquidating an Insolvent BVI Company

What a creditor needs to know about liquidating GUIDE an insolvent BVI company Last reviewed: October 2020 Contents Introduction 3 When is a company insolvent? 3 What is a statutory demand? 3 Written request for payment 3 Is it essential to serve a statutory demand? 3 What must a statutory demand say? 3 Setting aside a statutory demand 4 How may a company be put into liquidation? 4 Qualifying resolution 4 Appointment 4 Liquidator's powers 4 Court order 5 Who may apply? 5 Application 5 Debt should be undisputed 5 When does a company's liquidation start? 5 What are the consequences of a company being put into liquidation? 5 Assets do not vest in liquidator 5 Automatic consequences 5 Restriction on execution and attachment 6 Public documents 6 Other consequences 6 Effect on contracts 6 How do creditors claim in a company's liquidation? 7 Making a claim 7 Currency 7 Contingent debts 7 Interest 7 Admitting or rejecting claims 7 What is a creditors' committee? 7 Establishing the committee 7 2021934/79051506/1 BVI | CAYMAN ISLANDS | GUERNSEY | HONG KONG | JERSEY | LONDON mourant.com Functions 7 Powers 8 What is the order of distribution of the company's assets? 8 Pari passu principle 8 Excluded assets 8 Order of application 8 How are secured creditors affected by a company's liquidation? 8 General position 8 Liquidator challenge 8 Claiming in the liquidation 8 Who are preferential creditors? 9 Preferential creditors 9 Priority 9 What are the claims of current and past shareholders? 9 Do shareholders have to contribute towards the company's debts? -

How Should Property Be Valued in a Cram Down?

Mercer Law Review Volume 49 Number 3 Article 16 5-1998 How Should Property Be Valued In a Cram Down? Mark E. Beatty Follow this and additional works at: https://digitalcommons.law.mercer.edu/jour_mlr Part of the Bankruptcy Law Commons Recommended Citation Beatty, Mark E. (1998) "How Should Property Be Valued In a Cram Down?," Mercer Law Review: Vol. 49 : No. 3 , Article 16. Available at: https://digitalcommons.law.mercer.edu/jour_mlr/vol49/iss3/16 This Comment is brought to you for free and open access by the Journals at Mercer Law School Digital Commons. It has been accepted for inclusion in Mercer Law Review by an authorized editor of Mercer Law School Digital Commons. For more information, please contact [email protected]. Comments How Should Property Be Valued In a Cram Down? I. INTRODUCTION One of the most intriguing topics in bankruptcy law is the valuation of property in cram down cases, specifically Chapter 13 cases. This article will first present and discuss the different methods of valuation employed by the circuit courts before Associates Commercial Corp. v. Rash (Rash II)' was decided by the Supreme Court and the reasoning behind these methods. The next section will discuss the opinion in Rash and the chosen method of valuation in Chapter 13 cram down cases. The third section will discuss the implications of the decision in Rash. The Article will conclude with a proposed solution to the problems presented by the decision. 1. 117 S. Ct. 1879 (1997). 891 892 MERCER LAW REVIEW [Vol. 49 II. THE CIRcurr COURTS A. -

Questionnaire for Official Committee of Unsecured Creditors*

QUESTIONNAIRE FOR OFFICIAL COMMITTEE OF UNSECURED CREDITORS* In Re: Please Type or Print Clearly. I am willing to serve on a Committee of Unsecured Creditors. Yes ( ) No ( ) A. Unsecured Creditor's Name and Contact Information: Name: ___________________________________________ Phone: __________________ Address: ___________________________________________ Fax: __________________ ___________________________________________ E-mail: _____________________________________________________________________________ B. Counsel (If Any) for Creditor and Contact Information: Name: ___________________________________________ Phone: __________________ Address: ___________________________________________ Fax: __________________ ___________________________________________ E-mail: _____________________________________________________________________________ C. If you have been contacted by a professional person(s) (e.g., attorney, accountant, or financial advisor) regarding the formation of this committee, please provide that individual’s name and/or contact information: _____________________________________ _____________________________________ _____________________________________ D. Amount of Unsecured Claim (U.S. $) __________________________ E. Name of each debtor against whom you hold a claim: ____ __________________________________ ___________________________________________________________________________________ ___________________________________________________________________________________ ∗ Note: This is not a proof of claim form. Proof -

UK (England and Wales)

Restructuring and Insolvency 2006/07 Country Q&A UK (England and Wales) UK (England and Wales) Lyndon Norley, Partha Kar and Graham Lane, Kirkland and Ellis International LLP www.practicallaw.com/2-202-0910 SECURITY AND PRIORITIES ■ Floating charge. A floating charge can be taken over a variety of assets (both existing and future), which fluctuate from 1. What are the most common forms of security taken in rela- day to day. It is usually taken over a debtor's whole business tion to immovable and movable property? Are any specific and undertaking. formalities required for the creation of security by compa- nies? Unlike a fixed charge, a floating charge does not attach to a particular asset, but rather "floats" above one or more assets. During this time, the debtor is free to sell or dispose of the Immovable property assets without the creditor's consent. However, if a default specified in the charge document occurs, the floating charge The most common types of security for immovable property are: will "crystallise" into a fixed charge, which attaches to and encumbers specific assets. ■ Mortgage. A legal mortgage is the main form of security interest over real property. It historically involved legal title If a floating charge over all or substantially all of a com- to a debtor's property being transferred to the creditor as pany's assets has been created before 15 September 2003, security for a claim. The debtor retained possession of the it can be enforced by appointing an administrative receiver. property, but only recovered legal ownership when it repaid On default, the administrative receiver takes control of the the secured debt in full. -

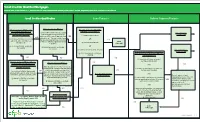

QM Small Creditor Flow Chart

SSmmaallll CCrreeddiittoorr QQuuaalliiffiieedd MMoorrttggaaggeess RReefflleeccttss rruulleess iinn eeffffeecctt oonn MMaarrcchh 11,, 22002211 bbuutt ddooeess nnoott rreefflleecctt aammeennddmmeennttss mmaaddee bbyy tthhee EEccoonnoommiicc GGrroowwtthh,, RReegguullaattoorryy RReelliieeff,, aanndd CCoonnssuummeerr PPrrootteeccttiioonn AAcctt.. Type of Compliance Presumption: SmSmaallll CCrreeddiitotorr QQuuaalliifificcaatitioonn Loan Features Balloon Payment Features Underwriting Points and Fees Portfolio Higher-Priced Loan Did you do ALL of the following?: Did you and your affiliates: Did you and your affiliates who Does the loan have ANY of the Rebuttable Presumption At the time of consummation: are creditors that extended following characteristics?: (1) Consider and verify the consumer’s YES Applies Extend 2,000 or fewer first-lien, closed- Does the loan amount fall within the following covered transactions during the Potential Small debt obligations and income or assets? STOP end residential mortgages that are points-and-fees limits? Was the loan subject to forward last calendar year have: (1) negative amortization; Creditor QM [via § 1026.43(c)(7), (e)(2)(v)]; = Non-Small Creditor QM (QM is presumed to comply subject to ATR requirements in the last YES commitment? AND YES YES = Non-Balloon-Payment QM with ATR requirements if calendar year? You can exclude loans Points-and-fees caps (adjusted annually) Assets below $2 billion (as annually OR AND it’s a higher-priced loan, but YES [§ 1026.43(e)(5)(i)(C), (f)(1)(v)] that you originated and kept in portfolio consumers can rebut the adjusted) at the end of the last STOP If Loan Amount ≥ $100,000, then = 3% of total or that your affiliate originated and kept (2) interest-only features; (2) Calculate the consumer’s monthly presumption by showing calendar year? = Non-QM If $100,000 > Loan Amount ≥ $60,000, then = $3,000 in portfolio. -

Dictionary of Insolvency Terms in EU Member States DICTIONARY of INSOLVENCY TERMS in EU MEMBER STATES

Dictionary of Insolvency Terms in EU Member States DICTIONARY OF INSOLVENCY TERMS IN EU MEMBER STATES Contents Introduction......................................................................3 Lithuania.........................................................................97 Austria...............................................................................4 Luxembourg..................................................................104 Belgium..............................................................................9 Malta..............................................................................111 Bulgaria...........................................................................14 Netherlands..................................................................120 Croatia.............................................................................19 Poland............................................................................125 Cyprus..............................................................................26 Portugal.........................................................................135 Czech Republic................................................................33 Romania........................................................................141 Denmark..........................................................................38 Slovakia.........................................................................147 Estonia.............................................................................42 Slovenia.........................................................................152 -

Creditor Control of Corporations Operating Receiverships Corporate Reorganizations Chester Rohrlich

Cornell Law Review Volume 19 Article 3 Issue 1 December 1933 Creditor Control of Corporations Operating Receiverships Corporate Reorganizations Chester Rohrlich Follow this and additional works at: http://scholarship.law.cornell.edu/clr Part of the Law Commons Recommended Citation Chester Rohrlich, Creditor Control of Corporations Operating Receiverships Corporate Reorganizations, 19 Cornell L. Rev. 35 (1933) Available at: http://scholarship.law.cornell.edu/clr/vol19/iss1/3 This Article is brought to you for free and open access by the Journals at Scholarship@Cornell Law: A Digital Repository. It has been accepted for inclusion in Cornell Law Review by an authorized administrator of Scholarship@Cornell Law: A Digital Repository. For more information, please contact [email protected]. CREDITOR CONTROL OF CORPORATIONS; OPERATING RECEIVERSHIPS; COR- PORATE REORGANIZATIONS* CHESTER RoHRmicnt A corporation is, on a smaller scale (in some instances on a larger scale), like the political state, in that beneath the cloak of its unity there is a continuous, at times active but more frequently passive, struggle for power among the various groups in interest. Some of these groups, such as the public that deals with it or the employees who work for it, have as yet achieved only the the barest minimum of legal right to control its destinies.' In the arena of the law, the traditional conflict is between the stockholders2 and the creditors. There is an increasing convergence of interest between these two groups as the former become more and more "investors" rather than entrepreneurs, and the latter less and less inclined, or able, to stand on the letter of their bond'3 both are in the last analysis dependent *This article is the substance of one of the chapters of the author's forthcoming book THE LAW AND PRACTICE OF CORPORATE CONTROL. -

Bankruptcy a Guide for Unsecured Creditors Association Ofbusiness Recoveryprofessionals BANKRUPTCY BANKRUPTCY

Bankruptcy a guide for unsecured creditors Association ofBusiness RecoveryProfessionals BANKRUPTCY BANKRUPTCY Who can be made bankrupt? Bankruptcy An individual Only individuals can be made bankrupt. Bankruptcy does not apply to companies or partnerships, although individual members of a is made bankrupt as a result partnership can be made bankrupt. of a petition presented to How is an individual made bankrupt? Only individuals An individual is made bankrupt as a result of a can be made the court, usually because petition presented to the court, usually because bankrupt he cannot pay his debts. The debtor, one or more of his creditors or the supervisor of a he cannot pay his debts. voluntary arrangement, amongst others, may present a bankruptcy petition. A licensed insolvency practitioner has given you this The purpose of the bankruptcy order is to appoint a responsible because you, or your business, may be owed money person who has a duty to collect the bankrupt's assets and by a private individual or a sole trader who has distribute them to his creditors in accordance with the law. become bankrupt. This guide aims to help you understand your rights Who is appointed to deal with the bankrupt’s estate? as a creditor and to describe how best these rights Once a bankruptcy order is made, the court will usually appoint the Official Receiver to administer a bankrupt’s estate. The Official can be exercised. It is intended to relate only to Receiver is a civil servant and an officer of the court. The Official England and Wales. It is not an exhaustive statement Receiver must then decide within twelve weeks of the bankruptcy of the relevant law or a substitute for specific order whether to call a meeting of creditors to appoint a licensed professional or legal advice.