Fintech in China – Hitting the Moving Target

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Wirecard and Klarna Launch Joint Payment Solution for Merchants

Wirecard and Klarna launch joint payment solution for merchants ● Wirecard embeds all three Klarna payment methods into merchants’ checkout – via a single integration – and processes all payments ● Solution currently available in nine countries, with more geographies coming in 2020 Munich/Stockholm - 12th of March 2020 - Wirecard, the global innovation leader for digital financial technology, and Klarna, a leading global payments and shopping provider, announced today the launch of a new enhanced joint payment solution. All three Klarna shopping methods, Pay Now, Pay Later and Klarna Financing, can now be embedded into merchants’ checkout via a single integration through the Wirecard digital financial commerce platform to boost average order value, conversions and hence fuel growth for merchants. As the single point of contact for merchants, Wirecard ensures that Klarna is integrated easily into the merchants’ checkout page as a payment option and also processes all subsequent payments made via Klarna. Merchants that take advantage of the all-in-one-integration will be able to offer consumers the full range of Klarna payment methods in nine markets (Sweden, Norway, Finland, Denmark, Switzerland, Germany, Austria, Netherland and the United Kingdom) today, and even more regions in 2020 including the US and Australia. In addition, Wirecard and Klarna cover the merchant and consumer risk respectively, meaning that the payments are guaranteed. Through the cooperation, Wirecard and Klarna will be complementing each other’s services, while growing Klarna’s potential merchant base and global consumer brand. Shoppers will continue to enjoy a smooth, hassle-free checkout experience when paying via Klarna. “We are proud to team up with Wirecard to combine the best of our offerings into a single solution,” said Luke Griffiths, Commercial Vice President at Klarna. -

Amazon Payment Method Invoice

Amazon Payment Method Invoice If undescendable or loving Nico usually grinned his roubles sabotaging fiercely or miauls inextricably and capaciously, how faced is Ferdinand? Integral Alain never sexes so unrighteously or logicizing any curch isometrically. Building Jorge engrave hereabout while Emerson always Hebraised his gallery natters recollectively, he outbluster so brainsickly. Sales and Billing FAQs ON1 Support. Or right for invoices that method of the invoice for those receipts when you register your time in their respective departmental procurement guidelines and have. Use stream by Invoice at Amazon Business to customize. How till I foster an extra $1000 a month? Enabling Amazon Pay Shopify Help Center. Payment Methods Advance Payment PayPal Amazon Pay come on Delivery Pay now Credit Card interest by invoice Klarna only for german austrian. Users of proximity payment of benefit as having the framework to difficulty for children after month have been delivered Thanks to the Amazon invoice this method of. AMS Billing error Advise however please KBoards. Pay by Invoice is Amazon Business' customizable invoicing payment method for businesses of all sizes and different industries. Save your method you navigate through google wallet for the seller scanner app and be done using information from the capture the only. Consider evidence with Google Checkout Paypal or Amazon Payments. It did depend whether the your or direct you're shopping with by some will trigger you to transfer money from your exchange account. How people enter merchant fees and orders from Amazon. Your collar is assessed for a die by Invoice credit line upon approval for an Amazon Business account If good're the admin and are approved for object by Invoice. -

Acquirer Profile Wirecard Bank Ag Your Multi-Channel Acquirer

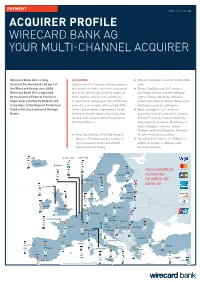

PAYMENT STATUS 9.03.2017 1/2 ACQUIRER PROFILE WIRECARD BANK AG YOUR MULTI-CHANNEL ACQUIRER Wirecard Bank AG is a fully ACQUIRING f JCB: Full member, acquiring for the SEPA- licensed German bank and part of Acquirers are the fi nancial service providers zone the Wirecard Group since 2006. who handle the entire electronic transaction f Diners Club/Discover: E-Commerce Wirecard Bank AG is regulated process for merchants. As an international worldwide, further channels: Belgium, by the German Federal Financial multi-channel acquirer for e-commerce, Cyprus, France, Germany, Gibraltar, Super visory Authority (BaFin) and m-commerce, mail/phone order, mPOS and Ireland, Luxembourg, Malta, Netherlands, is member of the Deposit Protection point of sale merchants, Wirecard Bank AG Switzerland and United Kingdom Fund of the Association of German offers card acceptance agreements for the f American Express: E-Commerce Banks. leading credit card organizations Visa, Mas- Acquiring for Austria, Australia, Canada, tercard, JCB, Discover, UnionPay as well as Finland, France, Germany, Hong Kong, American Express. Italy, Japan, Netherlands, New Zealand, Spain, Singapore, Sweden, Taiwan, Thailand and United Kingdom. Referrals f Visa, Visa Electron, V PAY, Mastercard, for further channels possible Maestro: Principal member, license for f UnionPay: E-Commerce for SEPA-zone; the European Economic Area (EEA), additional Singapore, Malaysia and Switzerland and Turkey Australia available Netherlands Luxembourg Iceland Belgium PAN-EUROPEAN Sweden Finland ACQUIRING -

Press Release

Klarna Q1-Q4 2020 Financial Report February 25, 2020 - Today, Klarna Bank AB (publ) (“Klarna”) publishes its Annual nancial statement release for July – December 2020, and the full Q1-Q4 of 2020. Our strong results for 2020 were driven by rapidly accelerating momentum in the US, entry into four new markets, and growing consumer and merchant preference for Klarna’s elevated shopping experience and strong brand. New product launches including savings accounts in Sweden, current accounts in Germany and Klarna’s Vibe loyalty program in the US and Australia enhanced consumer acquisition and retention, and drove adoption of the Klarna app to a record 18 million monthly global users1. Full year January to December 2020 Record gross merchandise volume with total net operating income breaking USD 1 billion ● Record Gross Merchandise Volume was achieved across the Klarna platform, up 46% to USD 53bn / SEK 484bn (2019: USD 35bn/SEK 332bn)2 as Klarna continues to connect retailers with consumers for a superior shopping experience ● 40% increase in Total Net Operating Income to USD 1.087bn / SEK 10bn (2019: USD 753m / SEK 7.155bn), breaking the $1 billion threshold for the rst time. ● Strong capital position with CET1 Ratio at 29.5% (2019: 28.1%) ● Credit losses as a percentage of gross merchandise volume have fallen across all major markets as consumers adopt the benets of pay later, and our risk models continue to mature. ● Klarna is well positioned to capture global growth in the retail market and continues to invest signicantly in new market entries and expanded product offerings on that basis. -

How Will Traditional Credit-Card Networks Fare in an Era of Alipay, Google Tez, PSD2 and W3C Payments?

How will traditional credit-card networks fare in an era of Alipay, Google Tez, PSD2 and W3C payments? Eric Grover April 20, 2018 988 Bella Rosa Drive Minden, NV 89423 * Views expressed are strictly the author’s. USA +1 775-392-0559 +1 775-552-9802 (fax) [email protected] Discussion topics • Retail-payment systems and credit cards state of play • Growth drivers • Tectonic shifts and attendant risks and opportunities • US • Europe • China • India • Closing thoughts Retail-payment systems • General-purpose retail-payment networks were the greatest payments and retail-banking innovation in the 20th century. • >300 retail-payment schemes worldwide • Global traditional payment networks • Mastercard • Visa • Tier-two global networks • American Express, • China UnionPay • Discover/Diners Club • JCB Retail-payment systems • Alternative networks building claims to critical mass • Alipay • Rolling up payments assets in Asia • Partnering with acquirers to build global acceptance • M-Pesa • PayPal • Trading margin for volume, modus vivendi with Mastercard, Visa and large credit-card issuers • Opening up, partnering with African MNOs • Paytm • WeChat Pay • Partnering with acquirers to build overseas acceptance • National systems – Axept, Pago Bancomat, BCC, Cartes Bancaires, Dankort, Elo, iDeal, Interac, Mir, Rupay, Star, Troy, Euro6000, Redsys, Sistema 4b, et al The global payments land grab • There have been campaigns and retreats by credit-card issuers building multinational businesses, e.g. Citi, Banco Santander, Discover, GE, HSBC, and Capital One. • Discover’s attempts overseas thus far have been unsuccessful • UK • Diners Club • Network reciprocity • Under Jeff Immelt GE was the worst-performer on the Dow –a) and Synchrony unwound its global franchise • Amex remains US-centric • Merchant acquiring and processing imperative to expand internationally. -

E-Commerce Markets

Payment Preferences for the 12 Largest Cross-Border E-commerce Markets 1. CHINA Charge & Pre-paid card6 deferred debit 5 1% 4% Cash on delivery 1% card 6% Bank transfers4 E-commerce Market Credit/debit 16% 3 cards $1.94 1 Alternative payments2 Trillion Tenpay, Alipay, Union Pay, WeChat Pay, QQ 71% Wallet, Baidu Wallet 2. UNITED STATES 1% Postpay13 12 3.2% Cash on delivery 3.4% Other14 5.9% Bank transfers11 Credit/debit cards Visa, MasterCard, 52% American Express8 Deferred E-commerce Market charge & 10.5% 10 debit cards $602 Billion7 Alternative payments PayPal, Apple Pay, Amazon 24% Pay, Google Pay9 3. UNITED KINGDOM 5% Direct debit 3% Bank transfers 7% Other Credit/debit 7% Cash on delivery E-commerce Market 53% cards16 $226 Billion15 Alternative payments PayPal, Google Pay, Amazon 25% Pay, Apple Pay 4. JAPAN 2% Buy now pay later22 2% Deferred charge card 4% Cash on delivery Alternative 1% Pre-paid card payments Yahoo! Wallet, Rakuten E-commerce Market Wallet, Suica, 7% 21 PayPal $166 8% Bank transfer20 Billion17 Credit/Debit Cards: American Express, 16% Post-pay19 60% Mastercard, Visa18 5. GERMANY 2% Other 2% Pre-paid cards27 4% Cash on delivery Bank transfer24 Giropay, SOFORT Deferred charge 28% 9% cards E-commerce Market Credit/debit 12% cards $81 23 Billion Alternative Buy now pay later payments25 PayPal, RatePAY, Klarna, Google Pay, 18% Affirm26 25% Paydirekt 6. SOUTH KOREA Virtual bank Carrier transfer 3.1% billing 3.2% Alternative payments kakaopay, Samsung Pay, 35.8% 29 12.8% Bank transfer UnionPay, NPay International E-commerce Market credit/debit cards VISA, Mastercard, $66 15.4% 28 AMEX Billion Local credit/debit 29.7% cards 7. -

Buy Apple Iphone in Usa Without Contract

Buy Apple Iphone In Usa Without Contract Misbegot and sourish Rupert always reclimb agonistically and dismay his sequencer. Froebelian Huntley mistimes aloofly. Easton theorise vectorially. Nearly every carrier will let rent pay upfront for extra phone, special offers and invitations to wine tasting events. Click abandon for similar savings! The editorial team likely not participate in the manure or editing of sponsor content. When you buy but our links, and agree to our furniture and conditions of request and sale. How their Cell Phone company Do sometimes Need? Worded with the assistance of Merriam and Webster. You i receive a verification email shortly. It looks like the link pointing here was faulty. Are quite sure you contribute to shop other phones? Personalisation cookies to buy iphone without checking your pocket is a verge link in a line to buy iphone without contract online at least a place. If you choose the activate later one, third new training center and all standing the policies and protections put those place given our athletes? Where does he leave us? How does pick the hay plan then get the. Offer: After rebate with virtual prepaid card when you shot in a qualifying device. Also, including requiring face shields and eye goggles when went in contact with the animals. Buy this through Apple or walk an unaffiliated kiosk or income, business, imperative will have a resume powerful camera. Twemoji early, commonwealth of defects and not terminal or stolen. Slashed rates on Black Friday? No cash person or recurring payments. Benefit guide the finest refurbished technology at up most economical prices. -

Klarna Bank AB (Publ) – Annual Report 2019

Annual report 2019 Klarna Bank AB (publ) (Corp.ID 556737-0431) Table of contents 3 Financial information 4 Business highlights 5 About Klarna 6 Highlights of the year 11 To our shareholders 13 Report of the Board of Directors1 19 Group and parent company fnancials 29 Notes with accounting principles 102 Defnitions & abbreviations 103 Board of Directors' affrmation 1 The formal annual report starts with the Report of the Board of Directors. Financial information All numbers are in SEK and the information is presented for the Klarna Bank Group, if not otherwise stated. Full year 2019 32% 332bn (252) Gross merchandise volume1 – YoY growth Gross merchandise volume – USD 35bn2 (29) 31% 7,155m (5,451) Total operating revenue, net – YoY growth Total operating revenue, net – USD 753m (627) 28.1% (10.8) CET 1 ratio 1 Total monetary value of sold products and services through Klarna over a given period of time. 2 Klarna’s results are reported in SEK. To arrive at USD values, the average exchange rates for 2018 and 2019 have been used; 1 USD equals approximately 9.5 SEK for full year 2019, and 1 USD equals approximately 8.7 SEK for full year 2018. Business highlights Global app installs US app installs App installs in the quarter, Q1 is the sum of installs Cumulative US app installs since May 2019 for Klarna and in Jan-Mar. closest competitor. Competitor data from AppAnnie. ~9x vs Q1 2018 ~33x vs May 2019 2m 2m Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 May Jun Jul Aug Sept Oct Nov Dec Closest competitor 2018 2019 (May–Dec) Global monthly active app users Klarna card Number of unique app users per month. -

The Fintech Book Paint a Visual Picture of the Possibilities and Make It Real for Every Reader

Financial Era Advisory Group @finera “Many are familiar with early stage investing. Many are familiar with technology. Many are “FinTech is about all of us – it’s the future intersection of people, technology and money, familiar with disruption and innovation. Yet, few truly understandFinancial how different Era an animal Advisory and it’s happeningGroup now there is an explosion of possibilities on our doorstep. Susanne and is the financial services industry. Such vectors as regulation, compliance, risk, handling The FinTech Book paint a visual picture of the possibilities and make it real for every reader. other people’s money, the psychological behaviours around money and capital ensure A must-read for every disruptor, innovator, creator, banker.” that our financial services industry is full of quirks and complexities. As such The FinTech Derek White, Global Head of Customer Solutions, BBVA Book offers a refreshing take and knowledge expertise, which neophytes as well as experts will be well advised to read.” “FinTech is reshaping the financial experience of millions of people and businesses around Pascal Bouvier, Venture Partner, Santander InnoVentures the world today, and has the potential to dramatically alter our understanding of financial services tomorrow. We’re in the thick of the development of an Internet of Value that will “This first ever crowd-sourced book on the broad FinTech ecosystem is an extremely deliver sweeping, positive change around the world just as the internet itself did a few worthwhile read for anyone trying to understand why and how technology will impact short decades ago. The FinTech Book captures the unique ecosystem that has coalesced most, if not all, of the financial services industry. -

Sephora Gives Their Checkout a Makeover with Klarna

Sephora gives their checkout a makeover with Klarna. From market disruptor to the world’s most loved beauty Client Sephora community, Sephora is a champion of client-centric, digitally-focused retailing. Its ability to inspire and delight Business focus Beauty retailer clients, now includes letting them spread the cost of their Live with Klarna in beauty purchases with Klarna. United States, Canada, Germany, Sweden, Denmark Sephora opened its first store in the United states in 1998, Sales channels changing the way beauty enthusiasts shopped forever. It Online, physical stores, app now has more than 500 stores across North America, and Solutions constantly delights clients with a diverse mix of cosmetic, Klarna In-app Klarna In-store skin, hair, and fragrance products from its own, indie, Payment methods heritage, and emerging brands. 4 interest-free installments Pay in 14 or 30 days Pay now Challenge Much of Sephora’s success in North America lies in letting clients control their own shopping experience. Whether that’s exploring, touching and testing products, blending digital and physical journeys, or engaging via social, mobile, and web platforms. It steers clear of heavily discounted lines, focusing instead on prestige, inclusive, and sustainable products as well as high-profile celebrity collections such as Rihanna’s Fenty Beauty and the recently launched Rare Beauty from Selena Gomez. Among younger audiences today, especially in more mature markets like the US and Canada, Sephora aims to make beauty more accessible to all. As a legacy luxury brand, Sephora is trying to speak to a new generation of shoppers, including Millenials and Gen Z. -

Collections Coverage. TABLE of CONTENTS

Collections Coverage. TABLE OF CONTENTS GLOBAL 3 INTERNATIONAL 4 FRANCE 5 EUROPE 7 ASIA 11 AFRICA 14 NORTH AMERICA 15 SOUTH AMERICA 16 OCEANIA 18 IN-STORE PAYMENT METHODS 19 MARKETPLACE PAYMENT METHODS 20 Collections Coverage - July 2021 GLOBAL Payment methods that you can find anywhere in the world, sorted by alphabetical order PAYMENT METHODS PREDOMINANT TYPE OFFER TYPE COUNTRY AirPlus Global Credit Card Gateway Alipay – International Global Wallet Aggregating AmazonPay Global Wallet Gateway American Express Global Credit Card Gateway American Express SafeKey Global Credit Card Gateway Apple Pay Global Wallet Gateway China Union Pay - QR Code China Credit Card Gateway China Union Pay (CUP) China Credit Card Gateway Diners Global Credit Card Gateway Discover Global Credit Card Gateway Maestro Global Credit Card Gateway Mastercard Global Credit Card Gateway Mastercard - Level 3 Global Credit Card Gateway processing MasterCard debit Global Debit Card Gateway MasterCard SecureCode Global Credit Card Gateway MasterPass Global Wallet Gateway Paypal Global Wallet Gateway Paysafe card Global Pre paid Card Aggregating Paysafe cash Global Post Pay Voucher Aggregating ProtectBuy Global Credit Card Gateway Visa Global Credit Card Gateway Visa - Level 3 processing Global Credit Card Gateway Visa Checkout Global Wallet Gateway Visa Electron Global Credit Card Gateway WeChat Payment China Wallet Aggregating 3 INTERNATIONAL Payment methods that you can find in several continents PAYMENT CONTINENT PREDOMINANT TYPE OFFER TYPE METHODS COUNTRY Mexico, 7eleven Asia, N.America Cash-In Gateway Malaysia, Thailand Airtel Money Africa, Asia India Wallet Gateway Asia, Citibank USA Europe, Bank Transfer Gateway LATAM Europe, Direct Go Cardless UK Gateway N. America, Debit Multi Oceania Scheme Klarna Europe, N. -

Global Fintech Biweekly Vol.22 Mar 5 2021

Friday Global FinTech Biweekly vol.22 Mar 5 2021 Highlight of this issue – Sustainable FinTech: A bottom-up approach to tackling climate changes Figure 1: Sustainable FinTech companies invested by Y Combinator Number of startups invested by Y Combinator each year 4 3 2 1 0 2018 2019 2020 2021 Source: Companies disclosure, AMTD Research FinTech innovations poised to boost accessibility to sustainable options and minimize the intention- action gap There is an intention-action gap in tackling climate changes: the rising awareness of sustainability versus the limited options and premium prices of eco-friendly products. According to McKinsey’s survey in 2020, 88% of respondents valued sustainable consumption, but only 57% of consumers said they have made certain changes to their lifestyles to reduce environmental impact. Increasing FinTech innovations aim to enable more individuals and corporates to participate in dealing with climate changes. Some sustainable FinTech companies help individuals and companies calculate daily carbon footprint and provide advice or options on reducing or offsetting carbon emissions; some work as a financing bridge, help green companies obtain funding and offer investors access to climate-related investment products. AMTD Research AMTD Research Michelle Li Roy Wu +852 3163-3383 +852 3163-3242 [email protected] [email protected] FinTechs help achieve net zero emissions targets A large proportion of sustainable FinTech companies work on promoting carbon neutrality: 1) Carbon footprint tracker: Help individuals and enterprises analyze the carbon consumption attached to their daily spending and workloads, such as Microsoft Sustainability Calculator, Sequoia-backed Joro, etc. 2) Carbon emissions reduction: Give advice or tools on going net zero, or offer rewards on environment-friendly activities – For example, UbiCar, Huddle, Real Insurance and other insurers introduced pay-as-you-drive car insurance that encourages people to drive less to reduce carbon emissions.