Marathon Oil Corp

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bakken Production Optimization Program Prospectus

Bakken Production Optimization Program BAKKEN PRODUCTION OPTIMIZATION PROGRAM 2.0 PROSPECTUS PROGRAM INTRODUCTION Led by the Energy & Environmental Research Center (EERC), the highly successful Bakken Production Optimization Program (BPOP), funded by its members and the North Dakota Industrial Commission, is continuing for the time frame of 2017–2020. The goal of this research program, BPOP 2.0, is to improve Bakken system oil recovery and reduce its environmental footprint. The results of the 3-year program will increase well productivity and the economic output of North Dakota’s oil and gas resources, decrease environmental impacts of wellsite operations, and reduce demand for infrastructure construction and maintenance. BPOP 1.0 PARTNERS A premier partnership program was recently completed which has been cited as an exemplary model by others nationwide. It has demonstrated that state lawmakers, state regulators, and industry can work together for positive results for shareholders and taxpayers alike. Phase I partners focused research on industry-driven challenges and opportunities. Continental Resources, Inc. ® Marathon Oil Corporation America’s Oil Champion Whiting Petroleum Corporation North Dakota Oil and Gas Research Program ConocoPhillips Company Nuverra Environmental Solutions Hitachi Hess Corporation Oasis Petroleum, Inc. SM Energy XTO Energy, Inc. BPOP 1.0 ACHIEVEMENTS (2013–2016) Continental’s Hawkinson Project Water Use and Handling Forecast Aimed at significantly increasing total production and A summary of trends in the Bakken, an estimation of production rates from North Dakota oil wells where oil future demand/disposal needs, an overview of treatment reserves of the second and third benches of the Three technologies, recycling/reuse considerations, and a Forks Formation, located just below the Bakken oil summary of implications for BPOP partners were created. -

Whiting Petroleum Corporation and Our Ability to Grow MMBOE: One Million BOE

Whiting Petroleum Corporation ANNUAL REPORT 8 0 0 2 NATU RAL HUM+AN Resources ABOUT THE COVER Having assembled a solid foundation of quality assets through acquisition, we are now more focused on organic drilling activity and on the development of previously acquired properties. We believe that our experienced team of management, engineering and geoscience professionals is generating superior results as evidenced by our reserves and production growth in the Bakken formation in North CONTENTS Dakota and our two CO 2 enhanced oil recovery projects. Corporate Profile 1 From our Bakken play in North Dakota, our average net daily production jumped 516% to 14,165 BOE in December 2008 Financial and Operations Summary 2 from 2,300 BOE in December 2007. We also completed Letter to the Shareholders 4 our first two infill wells in the Sanish field, which we believe Drilling and Operations Overview 7 adds a total of 78 potential infill well locations. Also of note was our first Three Forks horizontal well completion in the Northern Rockies 8 Sanish field. Production and pressure data from this well are Central Rockies 10 being analyzed to determine the viability of developing the Three Forks in the Sanish field. EOR Projects 12 Board of Directors 14 At our two EOR projects, our average net daily production Annual Report on Form 10-K 15 from the Postle and North Ward Estes fields increased 26% to 13,700 BOE in December 2008 from 10,900 BOE in Corporate Investor Information Inside back cover December 2007. We expect production from both EOR projects to continue to increase as 2009 progresses. -

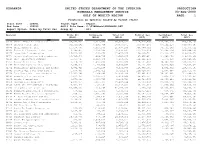

Ranking Operator by Gas 1999

PDRANKOP UNITED STATES DEPARTMENT OF THE INTERIOR PRODUCTION MINERALS MANAGEMENT SERVICE 03-AUG-2000 GULF OF MEXICO REGION PAGE: 1 Production by Operator Ranked by Volume (4120) Start Date : 199901 Report Type : Report End Date : 199912 ASCII File Name: C:\TIMSWork\PDRANKOP.DAT Report Option: Order by Total Gas Group By : All Operator Crude Oil Condensate Total Oil Natural Gas Casinghead Total Gas (BBLS) (BBLS) (BBLS) (MCF) (MCF) (MCF) 02140 Shell Deepwater Production Inc. 85,672,533 9,411,739 95,084,272 245,810,790 213,353,317 459,164,107 00078 Chevron U.S.A. Inc. 50,545,262 6,292,709 56,837,971 353,305,284 87,102,210 440,407,494 00689 Shell Offshore Inc. 15,438,780 6,417,500 21,856,280 300,789,310 30,544,202 331,333,512 00003 Union Oil Company of California 6,344,477 2,334,388 8,678,865 253,150,024 15,694,524 268,844,548 00276 Exxon Mobil Corporation 16,626,406 1,243,669 17,870,075 168,330,701 51,313,377 219,644,078 00771 Texaco Exploration and Production Inc 10,785,640 1,908,736 12,694,376 187,865,901 31,396,468 219,262,369 00114 Amoco Production Company 1,853,723 2,410,438 4,264,161 182,121,250 1,573,019 183,694,269 01855 Vastar Resources, Inc. 7,750,730 1,435,200 9,185,930 114,537,982 34,747,390 149,285,372 01364 Newfield Exploration Company 4,368,048 2,162,039 6,530,087 132,431,383 10,633,590 143,064,973 02332 PennzEnergy Exploration and Production 5,772,629 3,160,145 8,932,774 118,870,351 9,572,802 128,443,153 00491 Coastal Oil & Gas Corporation 1,038,860 1,682,412 2,721,272 119,028,667 2,687,097 121,715,764 02219 Kerr-McGee Oil & Gas Corporation 13,307,198 1,569,590 14,876,788 102,681,653 14,762,861 117,444,514 00185 Samedan Oil Corporation 2,673,355 2,285,513 4,958,868 104,938,141 7,424,318 112,362,459 00105 Apache Corporation 6,574,028 1,660,755 8,234,783 92,723,545 12,356,983 105,080,528 00059 Amerada Hess Corporation 9,001,254 7,825,335 16,826,589 76,749,036 23,640,310 100,389,346 00540 MOBIL OIL EXPLORATION & PRODUCING SOUT 8,967,820 1,142,597 10,110,417 88,168,916 11,699,694 99,868,610 01680 BP Exploration & Oil Inc. -

Adams Natural Resources Fund

ADAMS NATURAL RESOURCES FUND FIRST QUARTER REPORT MARCH 31, 2021 GET THE LATEST NEWS AND INFORMATION adamsfunds.com/sign-up L ETTER TO S HAREHOLDERS Dear Fellow Shareholders, Every new year brings with it the opportunity for a fresh start, resolutions for change, and hope for the future. No year in recent history has held greater expectations than 2021. We all hope to put the pandemic behind us and get back to normal. The year began with a new President in the White House and multiple vaccines already starting to be distributed. As the quarter progressed, we made significant strides towards vaccinating the most vulnerable. While we are moving closer to a return to normalcy as the availability of vaccines continues to grow, new COVID-19 variants threaten to slow progress. The economy continued to show signs of recovering as employers added more jobs in the first quarter and the unemployment rate declined to 6.0%. In February, consumer sentiment rose to its highest level since March 2020, when the COVID-19 shutdowns were just beginning. Over the past year, household savings have grown significantly and should begin to flow through the Energy was the best economy as it reopens. performing sector in the S&P 500 as oil prices The passage of a $1.9 trillion stimulus package and a rebounded. commitment of continued support from the Federal Reserve helped drive the stock market higher in the first quarter. The S&P 500 ended the quarter up 6.2%. Improved growth prospects pushed yields on 10-year Treasury notes higher and raised some concerns that the size of the stimulus could lead to higher inflation. -

Marathon Oil Corporation Creates Value by Responsibly Producing Oil and Natural Gas Vital to Meeting Growing Global Energy Needs

Create, Grow, Sustain: BUSINESS ROUNDTABLE Celebrating Success 2014 SUSTAINABILITY REPORT Marathon Oil Corporation creates value by responsibly producing oil and natural gas vital to meeting growing global energy needs. In doing so, we act responsibly toward our shareholders and business partners, support those who work for us, and strive to improve the communities where we operate. www.marathonoil.com/lov2012/index.shtml Our goal is to be recognized as the premier independent exploration and production company, and to accomplish this, we must successfully execute the strategic imperatives that guide our efforts. These imperatives begin with an uncompromising focus on our long-standing core values of health and safety, environmental stewardship, honesty and integrity, corporate citizenship, and a high-performance team culture. Our values help us protect our license to operate and drive business performance. We believe that developing oil To achieve sustainable and profitable growth, Marathon Oil is accelerating activity in our U.S. and gas resources in a safe, unconventional resource assets — the South Texas Eagle Ford Shale, North Dakota Bakken Shale and Oklahoma resource basins. These resource plays are at the forefront of the technology-driven environmentally sound and renaissance in the American oil and gas industry, which is making vast hydrocarbon resources available for the economic growth and energy security of our nation. responsible way is not only We recognize that the same spirit of technological discovery and innovation that is driving the possible, but also vital to the renaissance in the oil and gas industry can and will drive our ability to develop these important energy resources with less impact on the environment. -

EDITED TRANSCRIPT Q1 2021 Occidental Petroleum Corp Earnings Call

REFINITIV STREETEVENTS EDITED TRANSCRIPT Q1 2021 Occidental Petroleum Corp Earnings Call EVENT DATE/TIME: MAY 11, 2021 / 5:00PM GMT REFINITIV STREETEVENTS | www.refinitiv.com | Contact Us 1 ©2021 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. 'Refinitiv' and the Refinitiv logo are registered trademarks of Refinitiv and its affiliated companies. MAY 11, 2021 / 5:00PM GMT, Q1 2021 Occidental Petroleum Corp Earnings Call CORPORATE PARTICIPANTS Jeff Alvarez Occidental Petroleum Corporation - VP of IR Rob Peterson Occidental Petroleum Corporation - Senior VP & CFO Vicki Hollub Occidental Petroleum Corporation - President, CEO & Director CONFERENCE CALL PARTICIPANTS Dan Boyd Mizuho Securities USA LLC, Research Division - MD & Senior Energy Equity Research Analyst Devin McDermott Morgan Stanley, Research Division - VP, Commodity Strategist for Power Markets & Equity Analyst of Power and Utilities Research Team Doug Leggate BofA Securities, Research Division - MD and Head of US Oil & Gas Equity Research Jeanine Wai Barclays Bank PLC, Research Division - Research Analyst Leo Mariani KeyBanc Capital Markets Inc., Research Division - Analyst Neal Dingmann Truist Securities, Inc., Research Division - MD Neil Mehta Goldman Sachs Group, Inc., Research Division - VP and Integrated Oil & Refining Analyst Paul Cheng Scotiabank Global Banking and Markets, Research Division - Analyst Raphaël DuBois Societe Generale Cross Asset Research - Equity Analyst PRESENTATION Operator Good afternoon, and welcome to the Occidental's First Quarter 2021 Earnings Conference Call. (Operator Instructions) Please note this event is being recorded. I would now like to turn the conference over to Jeff Alvarez, Vice President of Investor Relations. -

2018 Annual Report

CALIFORNIA RESOURCES CORPORATION 2018 ANNUAL REPORT FINANCIAL AND OPERATIONAL HIGHLIGHTS Amounts in millions, except per-share amounts as of and for the years ended December 31, Financial Highlights 2018 2017 2016 Total Revenue $ 3,064 $ 2,006 $ 1,547 Income (Loss) Before Income Taxes $ 429 $ (262) $ 201 Net Income Attributable to Noncontrolling Interests $ 101 $ (4) $ - Net Income (Loss) Attributable to Common Stock $ 328 $ (266) $ 279 Adjusted Net Income (Loss)(a) $ 61 $ (187) $ (317) Net Income (Loss) Attributable to Common Stock per Share – Basic and Diluted(b) $ 6.77 $ (6.26) $ 6.76 Adjusted Net Income (Loss) per Share – Basic and Diluted(b) $ 1.27 $ (4.40) $ (7.85) Net Cash Provided by Operating Activities $ 461 $ 248 $ 130 Capital Investments $ 690 $ 371 $ 75 Net Payments on Debt $ 26 $ 18 $ 73 Net Cash Provided (Used) by Financing Activities $ 692 $ 73 $ (69) Total Assets $ 7,158 $ 6,207 $ 6,354 Long-Term Debt $ 5,251 $ 5,306 $ 5,168 Deferred Gain and Issuance Costs, Net $ 216 $ 287 $ 397 Equity $ (247) $ (720) $ (557) Weighted-Average Shares Outstanding(b) 47.4 42.5 40.4 Year-End Shares 48.7 42.9 42.5 Operational Highlights 2018 2017 2016 Production: Oil (MBbl/d) 82 83 91 NGLs (MBbl/d) 16 16 16 Natural Gas (MMcf/d) 202 182 197 Total (MBoe/d)(c) 132 129 140 Average Realized Prices: Oil with hedge ($/Bbl) $ 62.60 $ 51.24 $ 42.01 Oil without hedge ($/Bbl) $ 70.11 $ 51.47 $ 39.72 NGLs ($/Bbl) $ 43.67 $ 35.76 $ 22.39 Natural Gas ($/Mcf) $ 3.00 $ 2.67 $ 2.28 Reserves: Oil (MMBbl) 530 442 409 NGLs (MMBbl) 60 58 55 Natural Gas (Bcf) 734 706 626 Total (MMBoe)(c) 712 618 568 Organic Reserve Replacement Ratio(a) 127% 119% 71% PV-10 of Proved Reserves(a) (in billions) $ 9.4 $ 4.5 $ 2.8 Net Mineral Acreage (in thousands): Developed 701 703 717 Undeveloped 1,539 1,550 1,614 Total 2,240 2,253 2,331 Closing Share Price $ 17.04 $ 19.44 $ 21.29 (a) See www.crc.com, Investor Relations for a discussion of these non-GAAP measures, including a reconciliation to the most closely related GAAP measure or information on the related calculations. -

Occidental Petroleum Corporation

Occidental Petroleum Corporation Angela Zivkovich HSE Advisor This confidential information presentation (the "Overview") has been prepared by or on behalf of Occidental Petroleum Corporation (the "Company") solely for informational purposes. This Overview is being furnished to the recipient in connection with assessing interest in a potential transaction involving the Company or one or more of its subsidiaries or their respective assets or businesses (the "Potential Transaction"). None of the Company, its affiliates or any of their respective employees, directors, officers, contractors, advisors, members, successors, representatives or agents makes any representation or warranty as to the accuracy or completeness of this Overview, and shall have no liability for this Overview or for any representations (expressed or implied) contained in, or for any omissions from, this Overview or any other written or oral communications transmitted to the recipient in the course of its evaluation of the Potential Transaction. This Overview does not purport to contain all of the information that may be required or desirable to evaluate all of the factors that might be relevant to a potential investor, and any recipient hereof should conduct its own due diligence investigation and analysis in order to make an independent determination of the suitability and consequences of any action, including submission of a bid, in connection with the Potential Transaction. The Company reserves the right to amend, update or replace all or part of the information in this Overview at any time, but the Company shall not be under any obligation to provide any recipient of this Overview with any amended, updated or replacement information or to correct any inaccuracies herein which may become apparent. -

PROXY MEMORANDUM To: Occidental Petroleum Shareholders

PROXY MEMORANDUM To: Occidental Petroleum Shareholders Subject: 2016 Proxy Statement – Item No. 5: Stockholder Proposal Regarding Carbon Legislation Impact Assessment Date: March 31, 2016 Contact: Anita Green, Wespath Investment Management, 847-866-5287, [email protected] or Laura Campos, Nathan Cummings Foundation, 212-787-7300, [email protected] Wespath Investment Management (Wespath) and the Nathan Cummings Foundation co-filed Proxy Item No. 5, Stockholder Proposal Regarding Carbon Legislation Impact Assessment. The proposal will be voted on at the April 29, 2016 Annual Meeting of Occidental Petroleum Corporation (Occidental). Resolved Shareholders request that commencing in 2016 Occidental Petroleum Corporation, with board oversight, publishes an annual assessment of long-term portfolio impacts of public climate change policies, at reasonable cost and omitting proprietary information. The report should explain how current capital planning processes and business strategies incorporate analyses of the short- and long-term financial risks of a lower carbon economy. Specifically, the report should outline how the company is evaluating the impacts of fluctuating demand and price scenarios on the company’s existing reserves and resource portfolio - including the International Energy Agency’s “450 Scenario,” which sets out an energy pathway consistent with the internationally recognized goal of limiting the global increase in temperature to 2 degrees Celsius. Wespath and the Nathan Cummings Foundation encourage shareholders -

Climate and Energy Benchmark in Oil and Gas

Climate and Energy Benchmark in Oil and Gas Total score ACT rating Ranking out of 100 performance, narrative and trend 1 Neste 57.4 / 100 8.1 / 20 B 2 Engie 56.9 / 100 7.9 / 20 B 3 Naturgy Energy 44.8 / 100 6.8 / 20 C 4 Eni 43.6 / 100 7.3 / 20 C 5 bp 42.9 / 100 6.0 / 20 C 6 Total 40.7 / 100 6.1 / 20 C 7 Repsol 38.1 / 100 5.0 / 20 C 8 Equinor 37.9 / 100 4.9 / 20 C 9 Galp Energia 36.4 / 100 4.3 / 20 C 10 Royal Dutch Shell 34.3 / 100 3.4 / 20 C 11 ENEOS Holdings 32.4 / 100 2.6 / 20 C 12 Origin Energy 29.3 / 100 7.3 / 20 D 13 Marathon Petroleum Corporation 24.8 / 100 4.4 / 20 D 14 BHP Group 22.1 / 100 4.3 / 20 D 15 Hellenic Petroleum 20.7 / 100 3.7 / 20 D 15 OMV 20.7 / 100 3.7 / 20 D Total score ACT rating Ranking out of 100 performance, narrative and trend 17 MOL Magyar Olajes Gazipari Nyrt 20.2 / 100 2.5 / 20 D 18 Ampol Limited 18.8 / 100 0.9 / 20 D 19 SK Innovation 18.6 / 100 2.8 / 20 D 19 YPF 18.6 / 100 2.8 / 20 D 21 Compania Espanola de Petroleos SAU (CEPSA) 17.9 / 100 2.5 / 20 D 22 CPC Corporation, Taiwan 17.6 / 100 2.4 / 20 D 23 Ecopetrol 17.4 / 100 2.3 / 20 D 24 Formosa Petrochemical Corp 17.1 / 100 2.2 / 20 D 24 Cosmo Energy Holdings 17.1 / 100 2.2 / 20 D 26 California Resources Corporation 16.9 / 100 2.1 / 20 D 26 Polski Koncern Naftowy Orlen (PKN Orlen) 16.9 / 100 2.1 / 20 D 28 Reliance Industries 16.7 / 100 1.0 / 20 D 29 Bharat Petroleum Corporation 16.0 / 100 1.7 / 20 D 30 Santos 15.7 / 100 1.6 / 20 D 30 Inpex 15.7 / 100 1.6 / 20 D 32 Saras 15.2 / 100 1.4 / 20 D 33 Qatar Petroleum 14.5 / 100 1.1 / 20 D 34 Varo Energy 12.4 / 100 -

Strategic Decisions and Shareholder Value: an Analysis of Conocophillips Michael Miller University of Arkansas, Fayetteville

University of Arkansas, Fayetteville ScholarWorks@UARK Accounting Undergraduate Honors Theses Accounting 5-2012 Strategic decisions and shareholder value: an analysis of ConocoPhillips Michael Miller University of Arkansas, Fayetteville Follow this and additional works at: http://scholarworks.uark.edu/acctuht Part of the Finance and Financial Management Commons Recommended Citation Miller, Michael, "Strategic decisions and shareholder value: an analysis of ConocoPhillips" (2012). Accounting Undergraduate Honors Theses. 3. http://scholarworks.uark.edu/acctuht/3 This Thesis is brought to you for free and open access by the Accounting at ScholarWorks@UARK. It has been accepted for inclusion in Accounting Undergraduate Honors Theses by an authorized administrator of ScholarWorks@UARK. For more information, please contact [email protected], [email protected]. Strategic Decisions and Shareholder Value: An Analysis of ConocoPhillips By Michael Cameron Miller Advisor: Ms. Susan Bristow An Honors Thesis in partial fulfillment of the requirements for the degree Bachelor of Science in Business Administration in Accounting Sam M. Walton College of Business University of Arkansas Fayetteville, Arkansas May 11, 2012 Table of Contents INTRODUCTION ..................................................................................................................................................... 2 METHODOLOGY .................................................................................................................................................... -

California Resources Corporation (The “Company”) Believes Will Or May Occur in the Future Are Forward-Looking Statements

FINANCIAL AND OPERATING HIGHLIGHTS Dollar and share amounts in millions, except per-share amounts as of and for the years ended December 31, 2015 2014 2013 Financial Highlights Revenues $ 2,403 $ 4,173 $ 4,284 Income / (Loss) Before Income Taxes $ (5,476 ) $ (2,421 ) $ 1,447 Net Income / (Loss) $ (3,554 ) $ (1,434 ) $ 869 Adjusted Net Income / (Loss) (a) $ (311) $ 650 $ 869 EPS – Basic and Diluted (b) $ (9.27 ) $ (3.75 ) $ 2.24 Adjusted EPS – Basic and Diluted (b) $ (0.81) $ 1.67 $ 2.24 Net Cash Provided by Operating Activities $ 403 $ 2,371 $ 2,476 Capital Investments $ (401 ) $ (2,089 ) $ (1,669 ) Proceeds from Debt, Net $ 379 $ 6,360 — Cash Dividends to Occidental — $ (6,000 ) — Net Cash Provided (Used) by Financing Activities $ 352 $ (45) $ (763) Total Assets $ 7,053 $ 12,429 $ 14,297 Long-Term Debt – Principal Amount $ 6,043 $ 6,360 — Deferred Gain and Issuance Costs, Net $ 491 $ (68 ) — Equity / Net Investment $ (916) $ 2,611 $ 9,989 Weighted Average Shares Outstanding 383.2 381.9 — Year-End Shares 388.2 385.6 — Operational Highlights 2015 2014 2013 Production: Crude Oil (MBbl/d) 104 99 90 NGLs (MBbl/d) 18 19 20 Natural Gas (MMcf/d) 229 246 260 Total (MBoe/d) 160 159 154 Average Realized Prices: Crude with hedge ($/Bbl) $ 49.19 $ 92.30 $ 104.16 Crude without hedge ($/Bbl) $ 47.15 $ 92.30 $ 104.16 NGLs ($/Bbl) $ 19.62 $ 47.84 $ 50.43 Natural Gas with hedge ($/Mcf) $ 2.66 $ 4.39 $ 3.73 Reserves: Crude Oil (MMBbl) 466 551 532 NGLs (MMBbl) 59 85 71 Natural Gas (Bcf) 715 790 844 Total (MBoe/d) 644 768 744 Acreage (in thousands): Net Developed 736 716 701 Net Undeveloped 1,653 1,691 1,604 Total 2,389 2,407 2,305 Closing Share Price $ 2.33 $ 5.51 (a) For discussion of, or reconciliation to the most closely-related GAAP measure, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Results,” in our Form 10-K.