Strategic Decisions and Shareholder Value: an Analysis of Conocophillips Michael Miller University of Arkansas, Fayetteville

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Women Led the Legal Departments of Some of the Best-Performing

FORTUNE 500 MCCA® LIST OF WOMEN GENERAL COUNSEL AT FORTUNE 500 COMPANIES (continued) MCCA® LIST OF WOMEN GENERAL COUNSEL AT FORTUNE 500 COMPANIES (continued) 2010 2009 Grouped 2010 2009 Grouped Company General Counsel Industry Company General Counsel Industry Rank Rank by Industry Rank Rank by Industry Gap Michelle Banks 162 178 Specialty Retailers E Starbucks Paula Boggs 241 261 Food Services J Goldman Sachs Group Esta Stecher³ 39 40 Commercial Banks F SunGard Data Systems Victoria Silbey 380 435 Information Technology Services A Health Net Angelee Bouchard² 146 165 Healthcare: Insurance and Managed Care I Sunoco Stacy L. Fox¹ 78 41 Petroleum Refining C Holly Denise McWatters 431 420 Petroleum Refining C Thrivent Financial for Lutherans Teresa Rasmussen 342 409 Insurance: Life, Health (Mutual) B Honeywell International Katherine Adams 74 63 Aerospace and Defense R TJX Ann McCauley 119 131 Specialty Retailers E Host Hotels & Resorts Elizabeth Abdoo 492 449 Hotels, Casinos, Resorts N TRW Automotive Holdings Robin Walker-Lee¹ 201 169 Motor Vehicles and Parts K International Paper Maura Abeln-Smith 104 97 Forest and Paper Products P Unisys Nancy Sundheim 452 456 Miscellaneous Z J.C. Penney Janet Dhillon 133 139 General Merchandisers E United Parcel Service Teri Plummer-McClure 43 43 Mail, Package, and Freight Delivery T Kindred Healthcare M. Suzanne Riedman 477 538 Healthcare: Medical Facilities I Valero Energy Kim Bowers 26 10 Petroleum Refining C Liberty Global Elizabeth Markowski 210 257 Telecommunications H VF Candace Cummings 310 335 -

Bakken Production Optimization Program Prospectus

Bakken Production Optimization Program BAKKEN PRODUCTION OPTIMIZATION PROGRAM 2.0 PROSPECTUS PROGRAM INTRODUCTION Led by the Energy & Environmental Research Center (EERC), the highly successful Bakken Production Optimization Program (BPOP), funded by its members and the North Dakota Industrial Commission, is continuing for the time frame of 2017–2020. The goal of this research program, BPOP 2.0, is to improve Bakken system oil recovery and reduce its environmental footprint. The results of the 3-year program will increase well productivity and the economic output of North Dakota’s oil and gas resources, decrease environmental impacts of wellsite operations, and reduce demand for infrastructure construction and maintenance. BPOP 1.0 PARTNERS A premier partnership program was recently completed which has been cited as an exemplary model by others nationwide. It has demonstrated that state lawmakers, state regulators, and industry can work together for positive results for shareholders and taxpayers alike. Phase I partners focused research on industry-driven challenges and opportunities. Continental Resources, Inc. ® Marathon Oil Corporation America’s Oil Champion Whiting Petroleum Corporation North Dakota Oil and Gas Research Program ConocoPhillips Company Nuverra Environmental Solutions Hitachi Hess Corporation Oasis Petroleum, Inc. SM Energy XTO Energy, Inc. BPOP 1.0 ACHIEVEMENTS (2013–2016) Continental’s Hawkinson Project Water Use and Handling Forecast Aimed at significantly increasing total production and A summary of trends in the Bakken, an estimation of production rates from North Dakota oil wells where oil future demand/disposal needs, an overview of treatment reserves of the second and third benches of the Three technologies, recycling/reuse considerations, and a Forks Formation, located just below the Bakken oil summary of implications for BPOP partners were created. -

Fortune 500® Partners List (As of October 29, 2018) This List Represents Green Power Partners That Also Appear on the Fortune 500® List

Fortune 500® Partners List (as of October 29, 2018) This list represents Green Power Partners that also appear on the Fortune 500® list. EPA's list of Fortune 500 Partners consists of 76 companies using nearly 26 billion kilowatt-hours (kWh) of green power annually, which is equivalent to the electricity use of nearly 2.4 million average American homes. Partner Name Annual GP % of Organization Providers (listed in Green Green Total Type descending order by Power Power Electricity kWh supplied to Partner) Resources Usage Use* (kWh) 1. Microsoft 4,557,278,000 100% Technology & Sterling Planet°, Enbridge Solar, Wind Corporation Telecom LLC, EDF Renewable Energy, Black Hills Corp., Renewable Choice Energy°, Self-supply 2. Intel Corporation 4,152,034,623 100% Technology & Renewable Choice Energy°, Various Telecom 3Degrees°, Unknown, PNM, Self-supply 3. Google Inc. 2,409,051,735 53% Technology & MidAmerican Energy°, Biogas, Small- (Alphabet) Telecom NextEra Energy Resources°, hydro, Solar, Grand River Dam Authority°, Wind Northern Wasco County PUD, Enel Green Power North America, Exelon Generation, EDF Renewable Energy, Self-supply, Duke Energy, Unknown 4. Apple Inc. 1,650,398,166 107% Technology & Self-supply, 3 Phases Various Telecom Renewables°, Avangrid Renewables°, 3Degrees°, Cypress Creek Renewables, SunPower, Silicon Valley Power°, NC GreenPower°, Austin Energy°, Duke Energy, Sacramento Municipal Utility District°, Partner Name Annual GP % of Organization Providers (listed in Green Green Total Type descending order by Power Power Electricity kWh supplied to Partner) Resources Usage Use* (kWh) Salt River Project°, Carbon Solutions Group°, Homefield Energy, Silicon Valley Clean Energy°, Dynegy°, Xcel Energy°, Memphis Light, Gas and Water°, City of Palo Alto Utilities°, Louisville Gas & Electric Company, Capital Dynamics, Dominion Virginia Power°, Central Electric Cooperative, Huntsville Utilities°, Tampa Electric, Dominion Energy, City of Naperville, Avista Utilities, PNM°, Omaha Public Power District, Pacific Power°, NSTAR 5. -

Whiting Petroleum Corporation and Our Ability to Grow MMBOE: One Million BOE

Whiting Petroleum Corporation ANNUAL REPORT 8 0 0 2 NATU RAL HUM+AN Resources ABOUT THE COVER Having assembled a solid foundation of quality assets through acquisition, we are now more focused on organic drilling activity and on the development of previously acquired properties. We believe that our experienced team of management, engineering and geoscience professionals is generating superior results as evidenced by our reserves and production growth in the Bakken formation in North CONTENTS Dakota and our two CO 2 enhanced oil recovery projects. Corporate Profile 1 From our Bakken play in North Dakota, our average net daily production jumped 516% to 14,165 BOE in December 2008 Financial and Operations Summary 2 from 2,300 BOE in December 2007. We also completed Letter to the Shareholders 4 our first two infill wells in the Sanish field, which we believe Drilling and Operations Overview 7 adds a total of 78 potential infill well locations. Also of note was our first Three Forks horizontal well completion in the Northern Rockies 8 Sanish field. Production and pressure data from this well are Central Rockies 10 being analyzed to determine the viability of developing the Three Forks in the Sanish field. EOR Projects 12 Board of Directors 14 At our two EOR projects, our average net daily production Annual Report on Form 10-K 15 from the Postle and North Ward Estes fields increased 26% to 13,700 BOE in December 2008 from 10,900 BOE in Corporate Investor Information Inside back cover December 2007. We expect production from both EOR projects to continue to increase as 2009 progresses. -

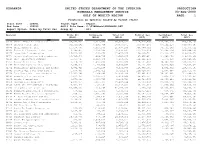

Ranking Operator by Gas 1999

PDRANKOP UNITED STATES DEPARTMENT OF THE INTERIOR PRODUCTION MINERALS MANAGEMENT SERVICE 03-AUG-2000 GULF OF MEXICO REGION PAGE: 1 Production by Operator Ranked by Volume (4120) Start Date : 199901 Report Type : Report End Date : 199912 ASCII File Name: C:\TIMSWork\PDRANKOP.DAT Report Option: Order by Total Gas Group By : All Operator Crude Oil Condensate Total Oil Natural Gas Casinghead Total Gas (BBLS) (BBLS) (BBLS) (MCF) (MCF) (MCF) 02140 Shell Deepwater Production Inc. 85,672,533 9,411,739 95,084,272 245,810,790 213,353,317 459,164,107 00078 Chevron U.S.A. Inc. 50,545,262 6,292,709 56,837,971 353,305,284 87,102,210 440,407,494 00689 Shell Offshore Inc. 15,438,780 6,417,500 21,856,280 300,789,310 30,544,202 331,333,512 00003 Union Oil Company of California 6,344,477 2,334,388 8,678,865 253,150,024 15,694,524 268,844,548 00276 Exxon Mobil Corporation 16,626,406 1,243,669 17,870,075 168,330,701 51,313,377 219,644,078 00771 Texaco Exploration and Production Inc 10,785,640 1,908,736 12,694,376 187,865,901 31,396,468 219,262,369 00114 Amoco Production Company 1,853,723 2,410,438 4,264,161 182,121,250 1,573,019 183,694,269 01855 Vastar Resources, Inc. 7,750,730 1,435,200 9,185,930 114,537,982 34,747,390 149,285,372 01364 Newfield Exploration Company 4,368,048 2,162,039 6,530,087 132,431,383 10,633,590 143,064,973 02332 PennzEnergy Exploration and Production 5,772,629 3,160,145 8,932,774 118,870,351 9,572,802 128,443,153 00491 Coastal Oil & Gas Corporation 1,038,860 1,682,412 2,721,272 119,028,667 2,687,097 121,715,764 02219 Kerr-McGee Oil & Gas Corporation 13,307,198 1,569,590 14,876,788 102,681,653 14,762,861 117,444,514 00185 Samedan Oil Corporation 2,673,355 2,285,513 4,958,868 104,938,141 7,424,318 112,362,459 00105 Apache Corporation 6,574,028 1,660,755 8,234,783 92,723,545 12,356,983 105,080,528 00059 Amerada Hess Corporation 9,001,254 7,825,335 16,826,589 76,749,036 23,640,310 100,389,346 00540 MOBIL OIL EXPLORATION & PRODUCING SOUT 8,967,820 1,142,597 10,110,417 88,168,916 11,699,694 99,868,610 01680 BP Exploration & Oil Inc. -

Marathon Oil Corporation Creates Value by Responsibly Producing Oil and Natural Gas Vital to Meeting Growing Global Energy Needs

Create, Grow, Sustain: BUSINESS ROUNDTABLE Celebrating Success 2014 SUSTAINABILITY REPORT Marathon Oil Corporation creates value by responsibly producing oil and natural gas vital to meeting growing global energy needs. In doing so, we act responsibly toward our shareholders and business partners, support those who work for us, and strive to improve the communities where we operate. www.marathonoil.com/lov2012/index.shtml Our goal is to be recognized as the premier independent exploration and production company, and to accomplish this, we must successfully execute the strategic imperatives that guide our efforts. These imperatives begin with an uncompromising focus on our long-standing core values of health and safety, environmental stewardship, honesty and integrity, corporate citizenship, and a high-performance team culture. Our values help us protect our license to operate and drive business performance. We believe that developing oil To achieve sustainable and profitable growth, Marathon Oil is accelerating activity in our U.S. and gas resources in a safe, unconventional resource assets — the South Texas Eagle Ford Shale, North Dakota Bakken Shale and Oklahoma resource basins. These resource plays are at the forefront of the technology-driven environmentally sound and renaissance in the American oil and gas industry, which is making vast hydrocarbon resources available for the economic growth and energy security of our nation. responsible way is not only We recognize that the same spirit of technological discovery and innovation that is driving the possible, but also vital to the renaissance in the oil and gas industry can and will drive our ability to develop these important energy resources with less impact on the environment. -

2018 Annual Report

CALIFORNIA RESOURCES CORPORATION 2018 ANNUAL REPORT FINANCIAL AND OPERATIONAL HIGHLIGHTS Amounts in millions, except per-share amounts as of and for the years ended December 31, Financial Highlights 2018 2017 2016 Total Revenue $ 3,064 $ 2,006 $ 1,547 Income (Loss) Before Income Taxes $ 429 $ (262) $ 201 Net Income Attributable to Noncontrolling Interests $ 101 $ (4) $ - Net Income (Loss) Attributable to Common Stock $ 328 $ (266) $ 279 Adjusted Net Income (Loss)(a) $ 61 $ (187) $ (317) Net Income (Loss) Attributable to Common Stock per Share – Basic and Diluted(b) $ 6.77 $ (6.26) $ 6.76 Adjusted Net Income (Loss) per Share – Basic and Diluted(b) $ 1.27 $ (4.40) $ (7.85) Net Cash Provided by Operating Activities $ 461 $ 248 $ 130 Capital Investments $ 690 $ 371 $ 75 Net Payments on Debt $ 26 $ 18 $ 73 Net Cash Provided (Used) by Financing Activities $ 692 $ 73 $ (69) Total Assets $ 7,158 $ 6,207 $ 6,354 Long-Term Debt $ 5,251 $ 5,306 $ 5,168 Deferred Gain and Issuance Costs, Net $ 216 $ 287 $ 397 Equity $ (247) $ (720) $ (557) Weighted-Average Shares Outstanding(b) 47.4 42.5 40.4 Year-End Shares 48.7 42.9 42.5 Operational Highlights 2018 2017 2016 Production: Oil (MBbl/d) 82 83 91 NGLs (MBbl/d) 16 16 16 Natural Gas (MMcf/d) 202 182 197 Total (MBoe/d)(c) 132 129 140 Average Realized Prices: Oil with hedge ($/Bbl) $ 62.60 $ 51.24 $ 42.01 Oil without hedge ($/Bbl) $ 70.11 $ 51.47 $ 39.72 NGLs ($/Bbl) $ 43.67 $ 35.76 $ 22.39 Natural Gas ($/Mcf) $ 3.00 $ 2.67 $ 2.28 Reserves: Oil (MMBbl) 530 442 409 NGLs (MMBbl) 60 58 55 Natural Gas (Bcf) 734 706 626 Total (MMBoe)(c) 712 618 568 Organic Reserve Replacement Ratio(a) 127% 119% 71% PV-10 of Proved Reserves(a) (in billions) $ 9.4 $ 4.5 $ 2.8 Net Mineral Acreage (in thousands): Developed 701 703 717 Undeveloped 1,539 1,550 1,614 Total 2,240 2,253 2,331 Closing Share Price $ 17.04 $ 19.44 $ 21.29 (a) See www.crc.com, Investor Relations for a discussion of these non-GAAP measures, including a reconciliation to the most closely related GAAP measure or information on the related calculations. -

Enterprise Risk Management in the Oil and Gas Industry: an Analysis of Selected Fortune 500 Oil and Gas Companies’ Reaction in 2009 and 2010 Violet C

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Clute Institute: Journals American Journal of Business Education – First Quarter 2016 Volume 9, Number 1 Enterprise Risk Management In The Oil And Gas Industry: An Analysis Of Selected Fortune 500 Oil And Gas Companies’ Reaction In 2009 And 2010 Violet C. Rogers, Stephen F. Austin State University, USA Jack R. Ethridge, Stephen F. Austin State University, USA ABSTRACT1 In 2009, four of the top ten Fortune 500 companies were classified within the oil and gas industry. Organizations of this size typically have an advanced Enterprise Risk Management system in place to mitigate risk and to achieve their corporations’ objectives. The companies and the article utilize the Enterprise Risk Management Integrated Framework developed by the Committee of Sponsoring Organizations (COSO) as a guide to organize their risk management and reporting. The authors used the framework to analyze reporting years 2009 and 2010 for Fortune 500 oil and gas companies. After gathering and examining information from 2009 and 2010 annual reports, 10-K filings, and proxy statements, the article examines how the selected companies are implementing requirements identified in the previously mentioned publications. Each section examines the companies’ Enterprise Risk Management system, risk appetite, and any other notable information regarding risk management. One observation was the existence or non-existence of a Chief Risk Officer or other Senior Level Manager in charge of risk management. Other observations included identified risks, such as changes in economic, regulatory, and political environments in the different countries where the corporations do business. -

Climate and Energy Benchmark in Oil and Gas

Climate and Energy Benchmark in Oil and Gas Total score ACT rating Ranking out of 100 performance, narrative and trend 1 Neste 57.4 / 100 8.1 / 20 B 2 Engie 56.9 / 100 7.9 / 20 B 3 Naturgy Energy 44.8 / 100 6.8 / 20 C 4 Eni 43.6 / 100 7.3 / 20 C 5 bp 42.9 / 100 6.0 / 20 C 6 Total 40.7 / 100 6.1 / 20 C 7 Repsol 38.1 / 100 5.0 / 20 C 8 Equinor 37.9 / 100 4.9 / 20 C 9 Galp Energia 36.4 / 100 4.3 / 20 C 10 Royal Dutch Shell 34.3 / 100 3.4 / 20 C 11 ENEOS Holdings 32.4 / 100 2.6 / 20 C 12 Origin Energy 29.3 / 100 7.3 / 20 D 13 Marathon Petroleum Corporation 24.8 / 100 4.4 / 20 D 14 BHP Group 22.1 / 100 4.3 / 20 D 15 Hellenic Petroleum 20.7 / 100 3.7 / 20 D 15 OMV 20.7 / 100 3.7 / 20 D Total score ACT rating Ranking out of 100 performance, narrative and trend 17 MOL Magyar Olajes Gazipari Nyrt 20.2 / 100 2.5 / 20 D 18 Ampol Limited 18.8 / 100 0.9 / 20 D 19 SK Innovation 18.6 / 100 2.8 / 20 D 19 YPF 18.6 / 100 2.8 / 20 D 21 Compania Espanola de Petroleos SAU (CEPSA) 17.9 / 100 2.5 / 20 D 22 CPC Corporation, Taiwan 17.6 / 100 2.4 / 20 D 23 Ecopetrol 17.4 / 100 2.3 / 20 D 24 Formosa Petrochemical Corp 17.1 / 100 2.2 / 20 D 24 Cosmo Energy Holdings 17.1 / 100 2.2 / 20 D 26 California Resources Corporation 16.9 / 100 2.1 / 20 D 26 Polski Koncern Naftowy Orlen (PKN Orlen) 16.9 / 100 2.1 / 20 D 28 Reliance Industries 16.7 / 100 1.0 / 20 D 29 Bharat Petroleum Corporation 16.0 / 100 1.7 / 20 D 30 Santos 15.7 / 100 1.6 / 20 D 30 Inpex 15.7 / 100 1.6 / 20 D 32 Saras 15.2 / 100 1.4 / 20 D 33 Qatar Petroleum 14.5 / 100 1.1 / 20 D 34 Varo Energy 12.4 / 100 -

Fortune 500 Women General Counsel Fifth Time in Six Years,” Apr

Fortune 500 Women General Counsel Fifth Time in Six Years,” Apr. 16, 2007, at 5. MCCA could not confirm the career path www.timeinc.net/fortune/ for three of the new arrivals on the Fortune continued from page 40 information/presscenter/fortune/ 1000 list through published sources. press_releases/20070416_f500.html. 6. See “Fortune 500 2008: Top Performers— Notes 4. As we went to press, MCCA learned that Most Profitable Companies: Profits” at 1. See Geoff Colvin, “Why the Party’s Over,” Ms. Iglesias was no longer associated with money.cnn.com/magazines/fortune/ Fortune, May 5, 2008. Nordstrom as of mid-June 2008. She is fortune500/2008/performers/companies/ 2. The term “Fortune 1000” refers to counted as general counsel in this year’s profits/. companies ranked among Fortune’s 501 to survey because she served in that role 7. See Conor Dougherty, “Deborah Siegel, 1000 companies. through 2007, which is the baseline year General Counsel, Guess, Inc.,” in Who’s Who for determination of this year’s Fortune 3. See Colvin, supra note 1; see also in Law, Los Angeles Business Journal, March 3, 500 companies. “Wal-Mart Unseats Exxon Mobil for Top 2003, at http://findarticles.com/ Spot on Fortune 500 List; Ranks No. 1 for p/articles/mi_m5072/is_9_25/ai_98945800/ pg_5. MCCA® 2007 FORTUNE 501–1000 8. “Fortune 500 2008: ConocoPhillips— Women General Counsel COP,” at money.cnn.com/magazines/ fortune/fortune500/2008/snapshots/ By Industry* 327.html. Number Percentage 9. “Fortune 500 2008: Goldman Sachs Group Electronics, Office Equipment (A) 8 10 – GS,” at money.cnn.com/ Insurance: All (B) 4 5 magazines/fortune/fortune500/2008/snap- shots/10777.html. -

California Resources Corporation (The “Company”) Believes Will Or May Occur in the Future Are Forward-Looking Statements

FINANCIAL AND OPERATING HIGHLIGHTS Dollar and share amounts in millions, except per-share amounts as of and for the years ended December 31, 2015 2014 2013 Financial Highlights Revenues $ 2,403 $ 4,173 $ 4,284 Income / (Loss) Before Income Taxes $ (5,476 ) $ (2,421 ) $ 1,447 Net Income / (Loss) $ (3,554 ) $ (1,434 ) $ 869 Adjusted Net Income / (Loss) (a) $ (311) $ 650 $ 869 EPS – Basic and Diluted (b) $ (9.27 ) $ (3.75 ) $ 2.24 Adjusted EPS – Basic and Diluted (b) $ (0.81) $ 1.67 $ 2.24 Net Cash Provided by Operating Activities $ 403 $ 2,371 $ 2,476 Capital Investments $ (401 ) $ (2,089 ) $ (1,669 ) Proceeds from Debt, Net $ 379 $ 6,360 — Cash Dividends to Occidental — $ (6,000 ) — Net Cash Provided (Used) by Financing Activities $ 352 $ (45) $ (763) Total Assets $ 7,053 $ 12,429 $ 14,297 Long-Term Debt – Principal Amount $ 6,043 $ 6,360 — Deferred Gain and Issuance Costs, Net $ 491 $ (68 ) — Equity / Net Investment $ (916) $ 2,611 $ 9,989 Weighted Average Shares Outstanding 383.2 381.9 — Year-End Shares 388.2 385.6 — Operational Highlights 2015 2014 2013 Production: Crude Oil (MBbl/d) 104 99 90 NGLs (MBbl/d) 18 19 20 Natural Gas (MMcf/d) 229 246 260 Total (MBoe/d) 160 159 154 Average Realized Prices: Crude with hedge ($/Bbl) $ 49.19 $ 92.30 $ 104.16 Crude without hedge ($/Bbl) $ 47.15 $ 92.30 $ 104.16 NGLs ($/Bbl) $ 19.62 $ 47.84 $ 50.43 Natural Gas with hedge ($/Mcf) $ 2.66 $ 4.39 $ 3.73 Reserves: Crude Oil (MMBbl) 466 551 532 NGLs (MMBbl) 59 85 71 Natural Gas (Bcf) 715 790 844 Total (MBoe/d) 644 768 744 Acreage (in thousands): Net Developed 736 716 701 Net Undeveloped 1,653 1,691 1,604 Total 2,389 2,407 2,305 Closing Share Price $ 2.33 $ 5.51 (a) For discussion of, or reconciliation to the most closely-related GAAP measure, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Results,” in our Form 10-K. -

Ford Motor Company: Sustainability

Copyright 2008. No quotation or citation without attribution. IR/PS CSR Case #08-06 Ford Motor Company: Sustainability By: Sun Mi Ha GRADUATE SCHOOL OF INTERNATIONAL RELATIONS AND PACIFIC STUDIES UNIVERSITY OF CALIFORNIA, SAN DIEGO Prepared for Professor Peter Gourevitch Edited by Kristen Parks Corporate Social Responsibility Fall 2008 Copyright 2008. No quotation or citation without attribution. 2 Table of Contents Corporate Overview ......................................................................................................... 3 Ford Motor Company...................................................................................................... 3 Corporate Social Responsibility (CSR)........................................................................... 4 View of Company ............................................................................................................ 4 View of Consumers.......................................................................................................... 6 Motor Industry and CSR ................................................................................................. 7 Ford Motor Company’s CSR........................................................................................... 9 Climate Change............................................................................................................. 10 Mobility ......................................................................................................................... 12 Road Safety Project..................................................................................................