Delta Air Lines Inc /De

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Delegation from China Southern Airlines Visits Detroit --Nonstop Beijing-Detroit Service Scheduled to Begin in March 2009

L.C. Smith Terminal • Mezzanine Detroit, MI 48242 News ph 734 942 3550 fax 734 942 3793 www.metroairport.com Release Released: December 19, 2007 Contact: Scott Wintner (734) 955-3745 Delegation from China Southern Airlines Visits Detroit --Nonstop Beijing-Detroit Service Scheduled to Begin in March 2009 The Chairman of China Southern Airlines recently led a delegation to Detroit to discuss the carrier’s new service between the airline’s Beijing hub and Detroit Metropolitan Wayne County Airport, scheduled to begin in March 2009. China Southern will operate one daily flight between Beijing and Detroit using its new Boeing 787 aircraft. “I’m very pleased that Detroit will be added to China Southern’s network beginning in 2009,” said China Southern Chairman Liu Shaoyong. “Detroit Metropolitan Airport is a world-class facility that will serve as an excellent gateway to North America for our customers.” According to an economic impact study commissioned by the Wayne County Airport Authority, China Southern’s nonstop Beijing–Detroit service will generate over $95 million in annual economic benefit to the region. “China Southern’s new service will certainly have a tremendous positive impact on our economy,” said Wayne County Airport Authority CEO Lester Robinson. “The nonstop service between Detroit and Beijing will not only increase business activity but will create new opportunities for trade and exchange.” Beijing currently ranks as Detroit’s second-largest market in China for passenger traffic behind Shanghai. Nonstop service between Detroit and Shanghai on Northwest Airlines will also begin in March 2009. Cargo is also expected to play an important role in the success of both flights. -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

100-150 Seat Large Civil Aircraft from Canada Conference 05-18-2017

UNITED STATES INTERNATIONAL TRADE COMMISSION In the Matter of: ) Investigation Nos.: 100-TO 150-SEAT LARGE CIVIL AIRCRAFT ) 701-TA-578 AND FROM CANADA ) 731-TTA-1368 (PRELIMINARY) Pages: 1 -289 Place: Washington, D.C. Date: Thursday, May 18, 2017 Ace-Federal Reporters, Inc. Stenotype Reporters 1625 I Street, NW Suite 790 Washington, D.C. 20006 202-347-3700 Nationwide Coverage www.acefederal.com 1 1 THE UNITED STATES INTERNATIONAL TRADE COMMISSION 2 In the Matter of: ) Investigation Nos.: 701-TA-578 3 100-TO 150-SEAT ) and 731-TA-1368 4 LARGE CIVIL AIRCRAFT ) (Preliminary) 5 FROM CANADA ) 6 7 Thursday, May 18, 2017 8 Main Hearing Room 9 U.S. International 10 Trade Commission 11 500 E Street, S.W. 12 Washington, D.C. 13 The meeting commenced, pursuant to notice, at 14 9:30 a.m., before the United States International Trade 15 Commission Investigative Staff. Michael Anderson, 16 Supervisory Investigator, presiding. 17 18 APPEARANCES: 19 On behalf of the International Trade Commission: 20 Michael Anderson, Director of Investigations, 21 (presiding) 22 Douglas Corkran, Supervisory Investigator 23 Carolyn Carlson, Investigator 24 Nannette Christ, International Economist 25 Ace‐Federal Reporters, Inc. 202‐347‐3700 2 1 APPEARANCES (Continued): 2 Charles Yost, Accountant/Auditor 3 Karl von Schriltz, Attorney/Advisor 4 Russell Duncan, Statistician 5 6 William R. Bishop, Supervisory Hearings and 7 Information Officer 8 Sharon Bellamy, Records Management Specialist 9 Tyrell Burch, Legal Document Assistant 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 Ace‐Federal Reporters, Inc. 202‐347‐3700 3 1 OPENING REMARKS: 2 Petitioners (Robert T. -

United States Court of Appeals for the DISTRICT of COLUMBIA CIRCUIT

USCA Case #11-1018 Document #1351383 Filed: 01/06/2012 Page 1 of 12 United States Court of Appeals FOR THE DISTRICT OF COLUMBIA CIRCUIT Argued November 8, 2011 Decided January 6, 2012 No. 11-1018 REPUBLIC AIRLINE INC., PETITIONER v. UNITED STATES DEPARTMENT OF TRANSPORTATION, RESPONDENT On Petition for Review of an Order of the Department of Transportation Christopher T. Handman argued the cause for the petitioner. Robert E. Cohn, Patrick R. Rizzi and Dominic F. Perella were on brief. Timothy H. Goodman, Senior Trial Attorney, United States Department of Transportation, argued the cause for the respondent. Robert B. Nicholson and Finnuala K. Tessier, Attorneys, United States Department of Justice, Paul M. Geier, Assistant General Counsel for Litigation, and Peter J. Plocki, Deputy Assistant General Counsel for Litigation, were on brief. Joy Park, Trial Attorney, United States Department of Transportation, entered an appearance. USCA Case #11-1018 Document #1351383 Filed: 01/06/2012 Page 2 of 12 2 Before: HENDERSON, Circuit Judge, and WILLIAMS and RANDOLPH, Senior Circuit Judges. Opinion for the Court filed by Circuit Judge HENDERSON. KAREN LECRAFT HENDERSON, Circuit Judge: Republic Airline Inc. (Republic) challenges an order of the Department of Transportation (DOT) withdrawing two Republic “slot exemptions” at Ronald Reagan Washington National Airport (Reagan National) and reallocating those exemptions to Sun Country Airlines (Sun Country). In both an informal letter to Republic dated November 25, 2009 and its final order, DOT held that Republic’s parent company, Republic Airways Holdings, Inc. (Republic Holdings), engaged in an impermissible slot-exemption transfer with Midwest Airlines, Inc. (Midwest). -

Aircraft Noise and Operations Report 2014 Bi-Annual Summary January – June

Aircraft Noise and Operations Report 2014 Bi-Annual Summary January – June Cincinnati/Northern Kentucky International Airport AIRCRAFT NOISE AND OPERATIONS REPORT 2014 BI-ANNUAL SUMMARY JANUARY - JUNE Table of Contents and Summary of Reports Aircraft Noise Report Page 1 This report details the locations of all complaints for the reporting period. Comparisons include state, county and areas within each county. Quarterly & Annual Comparison of Complaints Page 2 This report shows the trends of total complaints comparing the previous five years by quarter to the current year. Complaints by Category Page 3 Complaints received for the reporting period are further detailed by fourteen types of complaints, concerns or questions. A complainant may have more than one complaint, concern or question per occurrence. Complaint Locations and Frequent Complainants Page 4 This report shows the locations of the complainants on a map and the number of complaints made by the most frequent/repeat complainants for the reporting period. Total Runway Usage - All Aircraft Page 5 This report graphically shows the total number and percentage of departures and arrivals on each runway for the reporting period. Nighttime Usage by Large Jets Page 6 This report graphically shows the total number and percentage of large jet departures and arrivals on each runway during the nighttime hours of 10:00 p.m. to 7:00 a.m. for the reporting period. Nighttime Usage by Small Jets and Props Page 7 This report graphically shows the total number and percentage of small jet and prop departures and arrivals on each runway during the nighttime hours of 10:00 p.m. -

AF KL PPT Template Sales External

VISIT USA 2019 AIR FRANCE / KLM / DELTA 1 VISIT USA 2019 AIR FRANCE / KLM / DELTA 2 WE CONNECT SWITZERLAND TO THE WORLD UP TO 38 FLIGHTS AND 5,000 SEATS FROM SWITZERLAND – EVERY DAY Daily flights from Zurich: • 5x CDG, 6x AMS, 1x JFK (A330) 1x ATL (seasonally) Daily flights from Basel/Mulhouse: • 3x CDG, 3x ORY, 4x AMS Daily flights from Geneva: • 9x CDG, 6x AMS … and connect to destinations around the world: more than 200 destinations on Air France, 160 on KLM and 320 on Delta Air France & KLM & Delta Air Lines (& Virgin Atlantic, Alitalia) Biggest Airline Joint venture from/to North Atlantic All Carriers are combinable To all destinstions to North Atlantic AND world wide AMS NYC ZRH BSL PAR GVA VIRGIN ATLANTIC JOINS AF KL DL TRANSATLANTIC JOINT VENTURE • DL hält 49%, AF KL halten 31% Anteile an Virgin Atlantic (VS) • AF / KL / DL / VS ist der grösste Airline-Verbund zwischen Europa und Nordatlantik • 300 tägliche Flüge von/zu 60 Destinationen zwischen Europa und Nordatlantik 5 CDG HUB ZRH / GVA BSL AMS HUB At JFK airport – T4 • SkyPriority® Services : • Exclusive check-in areas • Priority boarding and baggage delivery • Priority service at ticket/transfer desks • Accelerated security and passport clearance • Delta Sky Club® lounge: • New Sky Deck terrace with unprecedented runway views • Free Wi-Fi • Personalized flight assistance • Refreshments and snacks • Magazines and newspapers NEW DESTINATIONS & ROUTES RAPIDLY EXPANDING GLOBAL NETWORK New KLM destinations (from AMS): • Boston (as of MAR19) • Las Vegas (as of JUN19) New Air France -

REFLECTIONS the Newsletter of the Northwest Airlines History Center Dedicated to Preserving the History of a Great Airline and Its People

Vol.15, no.4 nwahistory.org facebook.com/NorthwestAirlinesHistoryCenter December 2017 REFLECTIONS The Newsletter of the Northwest Airlines History Center Dedicated to preserving the history of a great airline and its people. NORTHWEST AIRLINES 1926-2010 ______________________________________________________________________________________________________ THE REVIEWS ARE IN! These are just some of the comments which visitors (including crews from other airlines!) to the Northwest Airlines History Center have written in our guest book since we opened to the public on September 28 in our new location in the Crowne Plaza Aire MSP Hotel. We had to hit the ground running, with two major events scheduled back to back in early October. Stories and photos about our first two months of operation begin on page 4. From the Executive Director THE NORTHWEST AIRLINES Pardon us for saying over and over how great it is for HISTORY CENTER, Inc. the Northwest Airlines History Center Museum to be Founder Henry V. “Pete” Patzke 1925-2012 open again! It’s gratifying to see our daily visitor log filled in with the names and home states of apprecia- Museum: Crowne Plaza Aire MSP tive visitors, and their positive comments about the Hotel museum’s new look. The Crowne Plaza Aire Hotel Two Appletree Square caters to so many types of airline-related employees Bloomington MN 55425 and travelers that it comes as no surprise that many of 952-876-9677 these visitors are so appreciative of a museum that speaks to them, regardless of their airline affiliation. In October, we recorded 117 visitors; in our former Archives and Administration: 10100 location it took an entire year to record 112 visitors. -

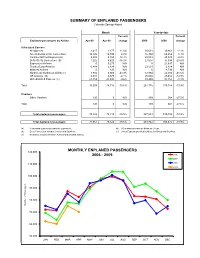

APR 2009 Stats Rpts

SUMMARY OF ENPLANED PASSENGERS Colorado Springs Airport Month Year-to-date Percent Percent Enplaned passengers by Airline Apr-09 Apr-08 change 2009 2008 change Scheduled Carriers Allegiant Air 2,417 2,177 11.0% 10,631 10,861 -2.1% American/American Connection 14,126 14,749 -4.2% 55,394 60,259 -8.1% Continental/Cont Express (a) 5,808 5,165 12.4% 22,544 23,049 -2.2% Delta /Delta Connection (b) 7,222 8,620 -16.2% 27,007 37,838 -28.6% ExpressJet Airlines 0 5,275 N/A 0 21,647 N/A Frontier/Lynx Aviation 6,888 2,874 N/A 23,531 2,874 N/A Midwest Airlines 0 120 N/A 0 4,793 N/A Northwest/ Northwest Airlink (c) 3,882 6,920 -43.9% 12,864 22,030 -41.6% US Airways (d) 6,301 6,570 -4.1% 25,665 29,462 -12.9% United/United Express (e) 23,359 25,845 -9.6% 89,499 97,355 -8.1% Total 70,003 78,315 -10.6% 267,135 310,168 -13.9% Charters Other Charters 120 0 N/A 409 564 -27.5% Total 120 0 N/A 409 564 -27.5% Total enplaned passengers 70,123 78,315 -10.5% 267,544 310,732 -13.9% Total deplaned passengers 71,061 79,522 -10.6% 263,922 306,475 -13.9% (a) Continental Express provided by ExpressJet. (d) US Airways provided by Mesa Air Group. (b) Delta Connection includes Comair and SkyWest . (e) United Express provided by Mesa Air Group and SkyWest. -

2012 Investor Day Setting the Scene Transform 2015

2012 Investor Day Setting the scene Transform 2015 Setting targets Net debt January 2012 Cost reduction Implementing immediate measures Capacity 2012 and beyond Capex Cost reduction Securing structural cost reductions New labor agreements From 2013 Industrial projects Initiating a new revenue dynamic From 2013 2012 Investor Day 3 Transform 2015: end 2014 objectives Reduction in net debt: €2bn Reduction in unit costs*:10% Renegotiation of collective agreements Limited capacity growth Medium-haul restructuring Investment plan revised down Cargo turnaround Cost-saving measures Improvement in long-haul and maintenance profitability * Unit cost per EASK ex fuel 2012 Investor Day 4 Our overarching target: deleveraging the balance sheet 6.5 6.1 6.1 5.6 € billions 4.4 4.4 4.5 3.8 Net debt 2.7 March March March March March Dec Dec Dec Dec Dec Dec Dec Dec 2005 2006 2007 2008 2009 2009 2010 2011 2012 2013 2014 2015 2016 Net debt/ 2.6 0.9 4.8 <2 EBITDA 3.0 3.0 2.7 2.2 1.6 1.7 1.3 EBITDA 0.4 (last twelve months) March March March March March Dec Dec Dec Dec Dec Dec Dec Dec 2005 2006 2007 2008 2009 2009 2010 2011 2012 2013 2014 2015 2016 2012 Investor Day 5 Improvement in operating cash flows the primary source of net debt reduction Capex adjusted to cash generation Limit sale and lease-back operations Less than €100m per year planned for 2013, 2014 and beyond Focus on cost reduction rather than asset disposals Hedging operation on 1/3 of remaining Amadeus stake (7.5%) within framework of our risk management strategy 2012 Investor Day 6 -

CFA Institute Research Challenge Atlanta Society of Finance And

CFA Institute Research Challenge Hosted by Atlanta Society of Finance and Investment Professionals Team J Team J Industrials Sector, Airlines Industry This report is published for educational purposes only by New York Stock Exchange students competing in the CFA Research Challenge. Delta Air Lines Date: 12 January 2017 Closing Price: $50.88 USD Recommendation: HOLD Ticker: DAL Headquarters: Atlanta, GA Target Price: $57.05 USD Investment Thesis Recommendation: Hold We issue a “hold” recommendation for Delta Air Lines (DAL) with a price target of $57 based on our intrinsic share analysis. This is a 11% potential premium to the closing price on January 12, 2017. Strong Operating Leverage Over the past ten years, Delta has grown its top-line by 8.8% annually, while, more importantly, generating positive operating leverage of 60% per annum over the same period. Its recent growth and operational performance has boosted Delta’s investment attractiveness. Management’s commitment to invest 50% of operating cash flows back into the company positions Delta to continue to sustain profitable growth. Growth in Foreign Markets Delta has made an initiative to partner with strong regional airlines across the world to leverage its world-class service into new branding opportunities with less capital investment. Expansion via strategic partnerships is expected to carry higher margin growth opportunities. Figure 1: Valuation Summary Valuation The Discounted Cash Flows (DCF) and P/E analysis suggest a large range of potential share value estimates. Taking a weighted average between the two valuations, our bullish case of $63 suggests an attractive opportunity. However, this outcome presumes strong U.S. -

2015 Fourth Quarter Management Discussion and Analysis

POINTS INTERNATIONAL LTD. MANAGEMENT'S DISCUSSION AND ANALYSIS INTRODUCTION The following management’s discussion and analysis (‘‘MD&A’’) of the performance and financial condition of Points International Ltd. and its subsidiaries (which are also referred to herein as “Points” or the “Corporation”) should be read in conjunction with the Corporation’s audited consolidated financial statements (including the notes thereto) for the years ended December 31, 2015 and 2014. Further information, including the Annual Information Form (“AIF”) and Form 40-F for the year ended December 31, 2015, may be accessed at www.sedar.com or www.sec.gov. All financial data herein has been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) and all dollar amounts herein are in thousands of United States dollars unless otherwise specified. This MD&A is dated as of March 2, 2016 and was reviewed by the Audit Committee and approved by the Corporation’s Board of Directors. FORWARD-LOOKING STATEMENTS This MD&A contains or incorporates forward-looking statements within the meaning of United States securities legislation and forward-looking information within the meaning of Canadian securities legislation (collectively, “forward-looking statements”). These forward-looking statements relate to, among other things, revenue, earnings, changes in costs and expenses, capital expenditures and other objectives, strategic plans and business development goals, and may also include other statements that are predictive in nature, or that depend upon or refer to future events or conditions, and can generally be identified by words such as “may”, “will”, “expects”, “anticipates”, “intends”, “plans”, “believes”, “estimates” or similar expressions. -

New Expanded Joint Venture

Press Release The Power of Choice for Cargo Customers as Air France-KLM, Delta and Virgin Atlantic launch trans-Atlantic Joint Venture AMSTERDAM/PARIS, ATLANTA and LONDON: February 3rd, 2020 – Air France-KLM Cargo, Delta Air Lines Cargo and Virgin Atlantic Cargo are promising cargo customers more connections, greater shipment routing flexibility, improved trucking options, aligned services and innovative digital solutions with the launch of their expanded trans-Atlantic Joint Venture (JV). The new partnership, which represents 23% of total trans-Atlantic cargo capacity or more than 600,000 tonnes annually, will enable the airlines to offer the best-ever customer experience, and a combined network of up to 341 peak daily trans-Atlantic services – a choice of 110 nonstop routes with onward connections to 238 cities in North America, 98 in Continental Europe and 16 in the U.K. More choice and convenience for customers Customers will be able to leverage an enhanced network built around the airlines’ hubs in Amsterdam, Atlanta, Boston, Detroit, London Heathrow, Los Angeles, Minneapolis, New York-JFK, Paris, Seattle and Salt Lake City. It creates convenient nonstop or one-stop connections to every corner of North America, Europe and the U.K., giving customers the added confidence of delivery schedules being met by a wide choice of options. The expanded JV enables greater co-operation between the airlines, focused on delivering world class customer service and reliability on both sides of the Atlantic achieved through co-located facilities, joint trucking options as well as seamless bookings and connected service recovery. The airlines already co-locate at warehouses in key U.S., U.K.