A Semiparametric Approach Using Spatial Statistics

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Birmingham City Council Shard End Ward Meeting

BIRMINGHAM CITY COUNCIL SHARD END WARD MEETING MONDAY 13 NOVEMBER 2017 7PM AYLESFORD HALL 116 BRADLEY ROAD B34 6HE MEETING NOTES Present: Councillors Marje Bridle and Ian Ward Officers: Beverly Edmead – Community Governance Team Sgt Dan Turnbull – West Midlands Police Pat Whyte – Community Development & Support Unit There were approx. 70 residents present. Cllr M Bridle in the Chair 1. WELCOME AND INTRODUCTIONS Following introductions, Cllr Bridle, Ward Chair welcomed everyone to the meeting. 2. NOTICE OF RECORDING The Chair advised that members of the press/public may record and/or take photographs except where there were confidential or exempt items. 3. APOLOGIES An apology for absence was submitted on behalf of Cllr Cotton who was unable to attend the meeting due to illness. 4. LOCAL NEWS/INFORMATION UPDATES (i) West Midlands Police Sgt Dan Turnbull advised of the following:- - Off Road Bikes/Pedal Bikes Nuisance 30 warrants were executed at the pre-planned Halloween Ride Out event; 53 arrests were made, 7 of which were charged with serious offences. In addition, 14 bikes were seized, with several of these being from the Shard End ward. The intelligence gathered from local residents had been crucial in the success of the operation. Several young people, all of whom lived locally had been identified as the main perpetrators of pedal bikes nuisance as well as some from neighbouring Chelmsley Wood and Yorkswood. A number of partner agencies were involved with the families of the young people, and a number of conditions had been put in place to manage/change their behaviour. However, two young people were 1 still persistent in their offending and resistant to changing their behaviour. -

EAST TEAM Gps a to Z

EAST TEAM GPs A TO Z TEL FAX GP SURGERY GP NAME NUMBER NUMBER DN TEAM 0121 0121 WASHWOOD HEATH ALPHA MEDICAL PRACTICE ALVI 328 7010 328 7162 DNs 39 Alum Rock Rd, Alum Rock B8 1JA MUGHAL, DRS SPA 0300 555 1919 0121 0121 WASHWOOD HEATH ALUM ROCK MEDICAL PRACTICE AKHTAR, DR 328 9579 328 7495 DNs 27-28 Highfield RD, B8 3QD SPA 0300 555 1919 0121 0121 WASHWOOD HEATH AMAANAH MEDICAL PRACTICE IQBAL 322 8820 322 8823 DNs Saltley Health Centre KHAN & KHALID Cradock Rd B8 1RZ WAHEED, DRS 0121 0121 ASHFIELD SURGERY BLIGHT 351 3238 313 2509 WALMLEY HC DNs 8 Walmley Road COLLIER Sutton Coldfield B76 1QN LENTON, DRS ASHFURLONG MEDICAL 0121 0121 JAMES PRESTON CNT PRACTICE - SUTTON GROUP SPEAK 354 2032 321 1779 DNs MANOR PRACTICE RIMMER 233 Tamworth Road FLACKS Sutton Coldfield B75 6DX CAVE, DRS 0121 0121 BELCHERS LANE SURGERY AHMAD 722 0383 772 1747 RICHMOND DNs 197 Belchers Lane FARAAZ Bordersley Green B9 5RT KHAN & AZAM, DRS 0121 0121 BUCKLANDS END LANE SURGERY KUMAR 747 2160 747 3425 HODGE HILL DNs 36 Bucklands End Lane SINHA, DRS Castle Brom B34 6BP CASLTE VALE PRIMARY CARE 0121 0121 CENTRE ZAMAN 465 1500 465 1503 CASTLETON DNs 70 Tangmere Drive, Castle Vale B35 7QX SHAH, DRS 0121 0121 CHURCH LANE SURGERY ISZATT 783 2861 785 0585 RICHMOND DNs 113 Church Lane, Stechford B33 9EJ KHAN, DRS 0121 0121 WASHWOOD HEATH COTTERILLS LANE SAIGOL, DR 327 5111 327 5111 DNs 75-77 Cotterills Lane Alum Rock B8 2RZ 0121 0121 DOVE MEDICAL PRACTICE GABRIEL 465 5739 465 5761 DOVEDALE DNs 60 Dovedale Road KALLAN Erdington B23 5DD WRIGHT, DRS EATON WOOD MEDICAL CENTRE -

West Midlands Police Freedom of Information

West Midlands Police Freedom of Information Property Name Address 1 Address 2 Street Locality Town County Postcode Tenure Type 16 Summer Lane 16 Summer Lane Newtown Birmingham West Midlands B19 3SD Lease Offices Acocks Green 21-27 Yardley Road Acocks Green Birmingham West Midlands B27 6EF Freehold Neighbourhood Aldridge Anchor Road Aldridge Walsall West Midlands WS9 8PN Freehold Neighbourhood Anchorage Road Annexe 35-37 Anchorage Road Sutton Coldfield Birmingham West Midlands B74 2PJ Freehold Offices Aston Queens Road Aston Birmingham West Midlands B6 7ND Freehold Offices Balsall Heath 48 Edward Road Balsall Heath Birmingham West Midlands B12 9LR Freehold Neighbourhood Bell Green Riley Square Bell Green Coventry West Midlands CV2 1LR Lease Neighbourhood Billesley 555 Yardley Wood Road Billesley Birmingham West Midlands B13 0TB Freehold Neighbourhood Billesley Fire Station Brook Lane Billesley Birmingham West Midlands B13 0DH Lease Neighbourhood Bilston Police Station Railway Street Bilston Wolverhampton West Midlands WV14 7DT Freehold Neighbourhood Bloxwich Station Street Bloxwich West Midlands WS3 2PD Freehold Police Station Bournville 341 Bournville Lane Bournville Birmingham West Midlands B30 1QX Lease Police Station Bradford Street Bradford Street Digbeth Birmingham West Midlands B12 0JB Freehold Offices Brierley Hill Bank Street Brierley Hill West Midlands DY5 3DH Freehold Police Station Broadgate House Room 217 Broadgate House Broadgate Coventry West Midlands CV1 1NH License Neighbourhood Broadway School BO Aston Campus, Broadway -

Mapping of Race and Poverty in Birmingham

MAPPING OF RACE AND POVERTY IN BIRMINGHAM Alessio Cangiano – ESRC Centre on Migration, Policy and Society (COMPAS, University of Oxford) II Table of contents Executive Summary p. 1 1. Introduction p. 3 2. Population characteristics and demographic dynamics p. 3 3. Geographical patterns of deprivation across the city p. 5 4. Socio-economic outcomes of different ethnic groups at ward level p. 7 4.1. Access to and outcomes in the labour market p. 7 4.2. Social and health conditions p. 9 4.3. Housing p.10 5. Public spending for benefits, services and infrastructures p.11 5.1. Benefit recipients p.11 5.2. Strategic planning p.11 6. Summary and discussion p.13 6.1. Data gaps p.13 6.2. Deprivation across Birmingham wards p.14 6.3. Deprivation across ethnic groups p.14 6.4. Relationship between poverty and ethnicity p.15 6.5. Consequences of demographic trends p.15 6.6. Impact of benefits and local government’s spending p.16 References p.17 III List of figures Figure 1 – Population by ethnic group, Birmingham mid-2004 (%) p.18 Figure 2.1 – Population change, Birmingham 2001-2004 (thousand) p.18 Figure 2.2 – Population change, Birmingham 2001-2004 (Index number, 2001=100) p.19 Figure 3 – Foreign-born population by ethnic group, Birmingham 2001 (%) p.19 Figure 4 – Age pyramids of the main ethnic groups in Birmingham, 2001 (%) p.20 Figure 5 – Distribution of the major ethnic groups across Birmingham wards, 2001 (absolute numbers) p.25 Figure 6 – Population by ethnic group in selected Birmingham wards, 2001 (%) p.27 Figure 7 – Indices of Deprivation, -

Ward Meetings and Ward Plans Update

Date updated: 23.02.2021 Ward Meetings and Ward Plans Update 1. Ward Forum Meetings 1.1 Number of Virtual Meetings and Attendance (April 2020-March 2021) *Meeting arranged but not yet taken place **The NDSU YouTube Channel was set up in November 2020 (Q3) Year Meetings Total Average Number of Total Average (2020- that were YouTube YouTube Meetings Attendance Attendance 2021) joint Views** Views Q1 (Apr- 7 230 33 145 21 Jun) Q2 (Jul- 23 1 587 27 235 11 Sep) Q3 (Oct- 31 6 723 23 811 29 Dec) Q4 (Jan- 21 & 20* 1 & 4* 601 29 977 75 Mar) Grand 102 12 2,141 26 2,168 31 Total (82 & 20*) (8 & 4*) 1.2 Total Number of Meetings by Ward *Meeting arranged but not yet taken place ***Meeting arranged but not completed (technology error) April 2020- May 2018-April May 2019- Ward March 2021 2019 March 2020 (Virtual) Acocks Green 4 5 2 & 1* Allens Cross 2 1 1 Alum Rock 3 0 2 & 1* Aston 2 2 1 Balsall Heath West 3 5 1 & 1* Bartley Green 3 3 0 Billesley 1 1 1* Birchfield 5 4 2 & 1* Bordesley & Highgate 1 0 2 Bordesley Green 1 0 1* Bournbrook & Selly Park 3 1 2 Bournville & Cotteridge 3 3 2 & 1* Brandwood & Kings Heath 3 2 0 Bromford & Hodge Hill 5 2 6 Date updated: 23.02.2021 April 2020- May 2018-April May 2019- Ward March 2021 2019 March 2020 (Virtual) Castle Vale 2 0 0 Druids Heath & Monyhull 5 3 2 & 1* Edgbaston 2 3 0 Erdington 3 1 1 Frankley Great Park 2 1 2 Garretts Green 2 0 1 Glebe Farm & Tile Cross 6 2 1 Gravelly Hill 3 3 1 & 1* Hall Green North 4 4 2 & 1* Hall Green South 2 1 0 Handsworth 4 3 3 Handsworth Wood 4 3 1* Harborne 4 2 2*** & 1 Heartlands -

NHS Birmingham and Solihull Clinical Commissioning Group Primary

NHS Birmingham and Solihull Clinical Commissioning Group Primary Care Networks April 2021 PCN Name ODS CODE Practice Name Name of Clinical GP Provider Alignment/ Director Federation Alliance of Sutton Practices M85033 The Manor Practice Dr Fraser Hewett Our Health Partnership PCN M85026 Ashfield Surgery M85175 The Hawthorns Surgery Balsall Heath, Sparkhill and M85766 Balsall Heath Health Centre – Dr Raghavan Dr Aman Mann SDS My Healthcare Moseley PCN M85128 Balsall Heath Health Centre – Dr Walji M85051 Firstcare Health Centre M85116 Fernley Medical Centre Y05826 The Hill General Practice M85713 Highgate Medical Centre M85174 St George's Surgery (Spark Medical Group) M85756 Springfield Medical Practice Birmingham East Central M85034 Omnia Practice Dr Peter Thebridge Independent PCN M85706 Druid Group M85061 Yardley Green Medical Centre M85113 Bucklands End Surgery M85013 Church Lane Surgery Bordesley East PCN Y02893 Iridium Medical Practice Dr Suleman Independent M85011 Swan Medical Practice M85008 Poolway Medical Centre M85694 Garretts Green M85770 The Sheldon Practice Bournville and Northfield M85047 Woodland Road Dr Barbara King Our Health Partnership PCN M85030 St Heliers M85071 Wychall Lane Surgery M85029 Granton Medical Centre NHS Birmingham and Solihull Clinical Commissioning Group Primary Care Networks April 2021 Caritas PCN M88006 Cape Hill Medical Centre Dr Murtaza Master Independent M88645 Hill Top Surgery (SWB CCG) M88647 Rood End Surgery (SWB CCG) Community Care Hall Green Y00159 Hall Green Health Dr Ajay Singal Independent -

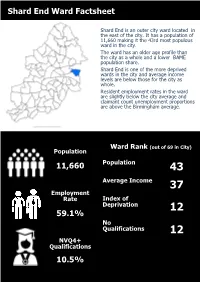

Shard End Ward Factsheet

Shard End Ward Factsheet Shard End is an outer city ward located in the east of the city. It has a population of 11,660 making it the 43rd most populous ward in the city. The ward has an older age profile than the city as a whole and a lower BAME population share. Shard End is one of the more deprived wards in the city and average income levels are below those for the city as whole. Resident employment rates in the ward are slightly below the city average and claimant count unemployment proportions are above the Birmingham average. Ward Rank (out of 69 in City) Population Population 11,660 43 Average Income 37 Employment Rate Index of Deprivation 12 59.1% No Qualifications 12 NVQ4+ Qualifications 10.5% Demography Shard End Age Structure Source: 2011 Census Age Shard End No Shard End % Birmingham % England % All Residents 11,660 - - - 16-64 7,117 61.0% 64.3% 64.8% Under18 2,988 25.6% 25.5% 21.4% 18-24 1,084 9.3% 12.1% 9.4% 25-44 3,124 26.8% 28.7% 27.5% 45-64 2,598 22.3% 20.7% 25.4% 65+ 1,866 16.0% 12.9% 16.3% 16.0% Under 18s 25.6% 25.6% Under 18 18-24 Age (25.5% B’ham) 25-44 22.3% Group 45-64 9.3% Over 65s 65+ 16.0% 26.8% (12.9% B’ham) Shard End Ethnicity Source: 2011 Census Ethnic Group Shard End No Shard End % Birmingham % England % White Total 9,993 85.7% 57.9% 85.4% British 9,691 83.1% 53.1% 79.8% Irish 183 1.6% 2.1% 1.0% Other White 119 1.0% 2.7% 4.7% Mixed or Multiple Ethnicity 721 6.2% 4.4% 2.3% Asian Total 358 3.1% 26.6% 7.8% Indian 36 0.3% 6.0% 2.6% Pakistani 199 1.7% 13.5% 2.1% Bangladeshi 33 0.3% 3.0% 0.8% Chinese 20 0.2% 1.2% -

Title Birmingham Community Safety Partnership Annual Report (2018

Title Birmingham Community Safety Partnership Annual Report (2018-19) Date 26th September 2019 Report Cllr John Cotton (Chair, Birmingham Community Safety Partnership/ Cabinet Author Member – Social Inclusion, Community Safety and Equalities) Chief Superintendent John Denley (Vice Chair, Birmingham Community Safety Partnership/ NPU Commander, Birmingham West) 1. Purpose 1.1 This annual report provides an overview of Birmingham Community Safety Partnership (BCSP) activity and impact during 2018-19. However, the report will refer to more recent information and activity to provide a more up to date context for the Committee. 1.2 Additional and more detailed information can be provided to the Committee on individual areas of business, if required. 2. Background 2.1 The Crime and Disorder Act (1997) mandated all local authority areas to establish Crime and Disorder Partnerships. In Birmingham, this partnership is referred to as the Birmingham Community Safety Partnership (BCSP). 2.2 The core membership of the BCSP includes all Responsible Authorities. These include: Birmingham City Council; Birmingham Children’s Trust; West Midlands Police; West Midlands Fire Service; National Probation Service; Community Rehabilitation Company and Birmingham and Solihull Clinical Commissioning Group. Co-opted members are Birmingham Social Housing Partnership and Birmingham and Solihull Mental Health Trust. 2.3 2.3 The BCSP has responsibility for discharging the following statutory requirements: Work together to form and implement strategies to prevent and reduce crime and anti-social behaviour, and the harm caused by drug and alcohol misuse. This will include producing an annual plan. Produce plans to reduce reoffending by adults and young people Manage the Community Trigger process Commission Domestic Homicide Reviews Serious Violence – this is a new duty and we are waiting for further information from Government on how this will be delivered. -

55 Bus Time Schedule & Line Route

55 bus time schedule & line map 55 Birmingham - Chelmsley Wood via Ward End View In Website Mode The 55 bus line (Birmingham - Chelmsley Wood via Ward End) has 2 routes. For regular weekdays, their operation hours are: (1) Birmingham: 4:42 AM - 11:46 PM (2) Chelmsley Wood: 3:55 AM - 11:30 PM Use the Moovit App to ƒnd the closest 55 bus station near you and ƒnd out when is the next 55 bus arriving. Direction: Birmingham 55 bus Time Schedule 52 stops Birmingham Route Timetable: VIEW LINE SCHEDULE Sunday 7:01 AM - 11:46 PM Monday 4:42 AM - 11:46 PM Chelmsley Interchange Chelmsley Circle, Birmingham Tuesday 4:42 AM - 11:46 PM Chelmsley Rd, Chelmsley Wood Wednesday 4:42 AM - 11:46 PM Lambeth Close, Bacon's End Thursday 4:42 AM - 11:46 PM Friday 4:42 AM - 11:46 PM Waterloo Avenue, Bacon's End Forth Drive, Birmingham Saturday 4:42 AM - 11:46 PM Bangor House, Bacon's End Fordbridge Infant School, Bacon's End 55 bus Info Oakthorpe Drive, Kingshurst Direction: Birmingham Stops: 52 Overgreen Drive, Kingshurst Trip Duration: 47 min Marston Drive, Birmingham/Wolverhampton/Walsall/Dudley Line Summary: Chelmsley Interchange , Chelmsley Rd, Chelmsley Wood, Lambeth Close, Bacon's End, Kingshurst Way, Kingshurst Waterloo Avenue, Bacon's End, Bangor House, Bacon's End, Fordbridge Infant School, Bacon's End, Gilwell Road, Kingshurst Oakthorpe Drive, Kingshurst, Overgreen Drive, Kingshurst, Kingshurst Way, Kingshurst, Gilwell Road, Kingshurst, Kitsland Rd, Shard End, Hurst Kitsland Rd, Shard End Lane, Shard End, Kitsland Rd, Shard End, Yorkswood Scout Camp, -

Harlequin Surgery

HARLEQUIN SURGERY 160 Shard End Crescent Shard End Birmingham B34 7BP. Telephone: 0121 747 8291 Fax: 0121 749 5497 www.harlequinsurgery.co.uk OPENING TIMES Monday 8.30am 6.00pm Tuesday 8.30am 6.00pm Wednesday 8.30am–12.30pm 2.30–6.00pm Thursday 8.30am 6.00pm Friday 8.30am 6.00pm PRACTICE MANAGER SECRETARIES SENIOR RECEPTIONISTS Sharon Dainty Michele Daniels Nicky Butler Jill Kitsell Carol Nicholas PARTNERS Dr J Heritage MB BS 1984 London ADMINISTRATION RECEPTIONISTS Dr R Pankhania MB ChB 1991 Birmingham Joan Clarke Sue Aherne Karen Green Sandra Facer DOCTORS Edward Heritage Lorraine Griffiths Dr R Kitson MB ChB 2004 Leicester Michele Kavanagh Sam Henry Dr S Pallan MB ChB 2006 Birmingham Josie McCutcheon Hayley Hilton Dr M Wilkinson MB ChB 1982 Birmingham Elaine Sumpter Dr O Ali MB ChB 2008 Birmingham Dr H Mohyuddin MB BS 1999 Karachi REGISTRATION Dr R Nazar MB BS 2005 London Please bring your medical card to the surgery if possible. All newly-registered patients aged five and over are required to attend a New Patient Health Check, a NURSE PRACTITIONERS simple medical examination with a Health Care Assistant, to have a urine test Mailing Pettitt RGN, MSc Advanced Clinical Practice, and their blood pressure, height and weight measured. Independent Prescriber Patients have a right to express their preference to be seen by their preferred Lesley Hilton RGN, MSc Advanced Clinical Practice, practitioner. The practice will make a reasonable attempt to meet your preference based on availability of the practitioner. Independent Prescriber Luke Richardson RGN DipHE, BSc (Hons.) Primary Care, DISABLED ACCESS PGDip (Advanced Practice), The practice has full disabled access, parking and toilet facilities. -

Vebraalto.Com

11 Walsham Croft, Birmingham, West Midlands, B34 7PA 3 Bed House - End Terrace Offers In Excess Of £210,000 Receptions 1 Bedrooms 3 Bathrooms 1 • WELL PRESENTED THREE BEDROOM PROPERTY • FAMILY BATHROOM • GOOD SIZED BREAKFAST KITCHEN • GREAT FAMILY HOME • LOUNGE DINER • CLOSE TO LOCAL AMENITIES INC SHOPS & SCHOOLS • ADJACENT TO OPEN PARKLAND • COMMUNAL PARKING AVAILABLE • CUL DE SAC LOCATION • HD WALKTHROUGH VIDEO TOUR AVAILABLE Ferndown Estates - Independent Sales / Lettings / Conveyancing / Mortgages 11 Walsham Croft, Birmingham, West Midlands, B34 7PA A SPACIOUS AND WELL PRESENTED THREE BEDROOM Entrance Hallway FAMILY HOME, set in a cul de sac location and close to open parkland. This property is a very attractive purchase for a range of buyers due to the quiet location and local amenities within easy reach. With convenient parking in the cul de sac the property offers: Porch, Breakfast Kitchen, Spacious Lounge Diner, Three Bedrooms with fitted wardrobes and a rear garden that backs onto parkland Overview & Approach Having ceiling light point and gas radiator, laminate flooring, Built in storage cupboard which houses the meters, stairs rising to first floor Kitchen Diner nearby schools and to be within easy reach of major transport links. Shard End is a sought-after district of East Birmingham due to the local schools which have high Ofsted Ratings and the nearby train stations, which offer regular train journeys into Birmingham City Centre and Birmingham International Train Station, Airport and the extremely popular Resorts world Walsham Croft is a three bedroom end terrace house approached via a pathway that leads to an enclosed porch with a front door leading into entrance hallway. -

Birmingham City Council Shard End Ward Meeting Monday 26 March 2018 7Pm Mackadown Sports & Social Club Mackadown Lane B33 0J

BIRMINGHAM CITY COUNCIL SHARD END WARD MEETING MONDAY 26 MARCH 2018 7PM MACKADOWN SPORTS & SOCIAL CLUB MACKADOWN LANE B33 0JG MEETING NOTES Present: Councillors Marje Bridle, John Cotton and Ian Ward Officers: Beverly Edmead – Community Governance Team Sgt Dan Turnbull – West Midlands Police There were 17 residents present. Cllr M Bridle in the Chair 1. WELCOME AND INTRODUCTIONS Following introductions, Cllr Bridle, Ward Chair welcomed everyone to the meeting. 2. NOTICE OF RECORDING The Chair advised that members of the press/public may record and/or take photographs except where there were confidential or exempt items. 3. APOLOGIES An apology for absence was submitted on behalf of Pt Whyte, Neighbourhood Development and Support Officer. 4. LOCAL NEWS/INFORMATION UPDATES (i) West Midlands Police Sgt Dan Turnbull advised of the following:- - Shard End Police Station was earmarked for closure in late 2020 as part of the premises review carried out by West Midlands Police. The building had a low occupancy rate and WMP was looking to secure a more cost friendly venue locally, including a possible building share with another appropriate organisation. The Neighbourhood Policing team would still continue to be locally based however there would e o puli aess or frot desk for residets to e ale to report a crime/incident to. Residents should continue to use the 101 or 999 telephone numbers to report non-emergency or emergency calls. Stechford Police Station would be the main station with public access for the East of the city. Residents expressed concerns regarding the future closure plans for the station and felt that the local base should be kept if the police were to remain a vital part of the community and a focal point for flag bearing civic events like the 1 Remembrance Day Parade.