Public Retirement Systems' Actuarial Committee

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Weekly Legislative Digest

Louisiana Federation of Teachers Weekly Legislative Digest May 1, 2015 Steve Monaghan, President * Les Landon, Editor 2015 Regular Legislative Session Now available on the Web at http://la.aft.org Panel votes to silence public employees Despite the best arguments of teachers, firefighters, police officers and other public servants, the House Labor and Industrial Relations Committee approved a bill that will make it inconvenient for employees to join and maintain membership in the union or association of their choice. The purpose of HB 418 by Rep. Stuart Bishop (R-Lafayette) is to weaken unions like the Louisiana Federation of Teachers and Louisiana Association of Educators. These are the groups that have raised questions about, and led the opposition to, so-called “reforms” backed by big business that all too often result in the privatization of education and diminution of the teaching profession. HB 418 would revoke the right of public employees to pay their union or association dues through payroll deduction. Since local governments currently have the authority to grant payroll deduction, the bill is seen by school boards and others as legislative meddling in their prerogatives. The bill is the brainchild of the Louisiana Association of Business and Industry, which has been twisting the arms of lawmakers to force its passage. The big business lobby recruited the Koch brothers backed Americans for Prosperity to publicly promote the bill. It is an example of what columnist Stephanie Grace, in another context, called “an ugly yet ascendant strain in American politics, a willingness to use any means necessary, no matter what chaos ensues or who gets hurt.” The vitriol motivating the bill’s supporters was on full display when an amendment was proposed to exempt the teacher unions from its prohibitions. -

The 2016 Legislature: Boomsday

Volume 42, Number 8 04/08/16 THE MISSION THE CORE VALUES of the LDAA is as follows: of LDAA members include: We believe that the Louisiana Constitution To improve Louisiana's justice system and the requires, and Louisiana citizens favor, locally- office of District Attorney by enhancing the elected, independent prosecutors. we believe that effectiveness and professionalism of Louisiana's prosecutor discretion must be protected from district attorneys and their staffs through interference through manipulative funding or education, legislative involvement, liaison and legislative restrictions. Finally, we believe that information sharing. prosecutors are the best and most trustworthy resource for legislative improvements to the criminal justice system. THE 2016 LEGISLATURE: BOOMSDAY The Governor's FY 16-17 budget is due to be released next Tuesday, April 12. When the numbers are available, we will know how the boom will be lowered concerning the DA line- item. Remember, this budget will be a worst-case scenario and will assume no additional revenues prior to July 1. The Louisiana Indigent Defender Board would be reorganized under a compromise version of HB 818. The Criminal Justice Committee approved a substitute bill, which will get a new number on the House floor. It reduces the number of Board members from 15 to 11; removes the four law professors; gives local PDs more input; and mandates that 65% of the appropriated funds be spent on local PDs. Look for LACDL and the boutique law firm, anti- death penalty gang to try to kill this in the Senate. Changing the Age of Juvenile Jurisdiction to include 17-year-olds is a major piece in the Governor's legislative agenda. -

13,000 Set Record at River Center Convention in Cleveland Sample Ballot July 18-21

Baton Rouge’s CAPITALCAPITAL CITYCITY Community Newspaper PresidentialPresidential CaucusCaucus •• PagePage 3-53-5 ® NEWSNEWSMarch 2016 • Vol. 25, No. 3 • 16 Pages • Circulation 14,000 copies • www.capitalcitynews.us • 225-261-5055 Louisiana Presidential Primary March 5, 2016 Louisiana to Test Trump Trump, Rubio Cruz Campaign For 45 Delegates From Louisiana BATON ROUGE — Fresh from a sweeping victory on Super Tuesday, Republican front-runner Donald Trump is carrying his campaign for President to Louisiana Sat- urday during its Presiden- tial Primary. His top chal- lengers are Sens. Marco Rubio of Flo- rida and Ted Cruz of Tex- as. The polls will open at Marco Rubio 7 a.m. and Photo by Woody Jenkins Woody by Photo close at 8 Republican Presidential candidate Donald Trump at Make America Great Rally at River Center in Baton Rouge p.m. At stake will be 45 delegates to the Republi- can National 13,000 Set Record at River Center Convention in Cleveland Sample Ballot July 18-21. Trump has Ted Cruz a strong but not commanding Saturday, March 5, 2016 lead nationwide. Both Trump On the Ballot in EBR and Cruz will speak in Loui- Presidential Primary siana Friday night. Also at Republican Party stake Saturday will be control of the governing bodies of the Ben Carson R Louisiana Republican Party Tim Cook R and the East Baton Rouge Ted Cruz R Parish Republican Party. John Kasich R For more on those party Peter Messina R elections, see Pages 3-5. Marco Rubio R Donald Trump R Donald Trump Republicans in Red are endorsed 6 p.m. -

Louisiana State University Student Government

Louisiana State University Student Government Dear LSU Students and Friends, Students in the state of Louisiana are more relevant than ever before. Before the release of the first Higher Education Report Card, students pursuing a degree were not valued in the state of Louisiana—proven by the 41% cut to higher education over the past 8 years. Contrary to popular belief, investment in higher education is the best societal investment that our state lawmakers can make. Because of our initial report card, leaders in the legislature are listening. The Higher Education Report Card is a huge step forward in ensuring that students are heard in the state of Louisiana. The requests are clear. We want stability in higher education and a sincere commitment to invest in the future of our students. We extend our sincerest gratitude to the governor and lawmakers for their work during the longest legislative session in the history of the state. Unfortunately, a session ending in a fully funded higher education and a partially funded TOPS is not ideal for Louisiana’s students. My hope is that the Higher Education Report Card can shed light onto the difficult votes that our lawmakers made during these sessions to ensure that our education would be fully funded. At the same time, I hope students will see that some of their own lawmakers are still not valuing our education as much as they can. We also hope that students will continue to be involved with the affairs of our state capitol by participating in marches and making calls to their legislators. -

Membership in the Louisiana House of Representatives

MEMBERSHIP IN THE LOUISIANA HOUSE OF REPRESENTATIVES 1812 - 2024 Revised – July 28, 2021 David R. Poynter Legislative Research Library Louisiana House of Representatives 1 2 PREFACE This publication is a result of research largely drawn from Journals of the Louisiana House of Representatives and Annual Reports of the Louisiana Secretary of State. Other information was obtained from the book, A Look at Louisiana's First Century: 1804-1903, by Leroy Willie, and used with the author's permission. The David R. Poynter Legislative Research Library also maintains a database of House of Representatives membership from 1900 to the present at http://drplibrary.legis.la.gov . In addition to the information included in this biographical listing the database includes death dates when known, district numbers, links to resolutions honoring a representative, citations to resolutions prior to their availability on the legislative website, committee membership, and photographs. The database is an ongoing project and more information is included for recent years. Early research reveals that the term county is interchanged with parish in many sources until 1815. In 1805 the Territory of Orleans was divided into counties. By 1807 an act was passed that divided the Orleans Territory into parishes as well. The counties were not abolished by the act. Both terms were used at the same time until 1845, when a new constitution was adopted and the term "parish" was used as the official political subdivision. The legislature was elected every two years until 1880, when a sitting legislature was elected every four years thereafter. (See the chart near the end of this document.) The War of 1812 started in June of 1812 and continued until a peace treaty in December of 1814. -

Advocacy Toolkit

Advocacy Day Toolkit April 11, 2018 Welcome! Thank you for joining us at the 2018 Justice for Louisiana Women Advocacy Day, where you’ll learn about key issues affecting women across our state, the impacts of proposed legislation, and ways you can influence the legislative process. Today, a variety of organizations and advocates are demanding better outcomes and justice for women in our state by uniting across social justice issues—including economic justice, reproductive justice, criminal justice, environmental justice, affordable healthcare, violence prevention, and more. Throughout the day you will hear from leaders and legislators about key issues and how they affect Louisiana’s women, their children, and their communities. We will also discuss proposed legislation, its potential impacts on Louisiana’s women, and ways you can influence state policies. Our goal is for you to learn more about the legislative process and to have opportunities to speak with your legislators. To that end, we are providing you with this toolkit that you can use to make your voice heard on these issues today and in the future. We hope you will enjoy this opportunity to network with other advocates, will gain deeper insights into how all of these social justice issues affect women across our state, and will take charge of your power to influence state policies. Most of all, we hope that you will leave here today with more knowledge, new skills, and a steadfast determination to stay engaged in the legislative process to demand justice for all of Louisiana’s -

By House District

House District* Current GO Recipients AY 2018‐19 (as of 3‐7‐19) 1 Jim Morris 102 2 Sam Jenkins 158 3 Barbara Norton 179 4 Cedric Glover 186 5 Alan Seabaugh 183 6 Thomas Carmody 167 7 Larry Bagley 139 8 Raymond Crews 149 9 Dodie Horton 154 10 Wayne McMahen 114 11 Patrick Jefferson 193 12 Christopher Turner 159 13 Jack McFarland 116 14 Jay Morris 173 15 Frank Hoffmann 147 16 Katrina Jackson 231 17 Vacant 191 18 Vacant 92 19 Charles Chaney 129 20 Steve Pylant 104 21 Andy Anders 97 22 Terry Brown 119 23 Kenny Cox 166 24 Frank Howard 136 25 Lance Harris 146 26 Vacant 214 27 Vacant 173 28 Robert Johnson 94 29 Edmond Jordan 188 30 James Armes 128 31 Nancy Landry 130 32 Dorothy Hill 78 33 Stuart Moss 114 34 A.B. Franklin 179 35 Stephen Dwight 130 36 Mark Abraham 163 37 John Guinn 115 38 Bernard LeBas 88 39 Julie Emerson 154 40 Dustin Miller 137 41 Phillip DeVillier 102 42 John Stefanski 94 43 Stuart Bishop 144 44 Vincent Pierre 161 45 Jean‐Paul Coussan 165 House District* Current GO Recipients AY 2018‐19 (as of 3‐7‐19) 46 Mike Huval 113 47 Vacant 86 48 Taylor Barras 143 49 Blake Miguez 120 50 Sam Jones 147 51 Beryl Amedee 176 52 Jerome Zeringue 152 53 Tanner Magee 152 54 Jerry Gisclair 108 55 Jerome Richard 207 56 Greg Miller 199 57 Randal Gaines 273 58 Ken Brass 155 59 Tony Bacala 149 60 Chad Brown 141 61 Denise Marcelle 193 62 Vacant 125 63 Barbara Carpenter 247 64 Valarie Hodges 150 65 Barry Ivey 169 66 Rick Edmonds 290 67 Patricia Smith 204 68 Steve Carter 154 69 Paula Davis 162 70 Franklin Foil 166 71 Rogers Pope 136 72 Robby Carter 108 -

Legislative Audit Advisory Council

LEGISLATIVE AUDIT ADVISORY COUNCIL Minutes of Meeting December 17, 2020 House Committee Room 5 State Capitol Building The items listed on the Agenda are incorporated and considered to be part of the minutes herein. Representative Barry Ivey called the Legislative Audit Advisory Council (Council) meeting to order at 11:15 a.m. Ms. Liz Martin called the roll confirming quorum was present. Members Present: Representative Barry Ivey Chairman Senator Jay Luneau, Vice Chairman Senator Louie Bernard Senator Jimmy Harris Senator Beth Mizell Representative Edmond Jordan Representative Rodney Schamerhorn Members Absent: Senator Fred Mills Representative Aimee A. Freeman Representative Stephanie Hilferty Also Present: Daryl G. Purpera, CPA, CFE, Louisiana Legislative Auditor (LLA) Approval of Minutes Representative Schamerhorn offered the motion to approve the minutes of the November 16, 2020 meeting and with no opposition, the motion was approved. Extension Requests (Video Archive Time 1:53) Mr. Bradley Cryer, Director of Local Government Services, presented two extension lists and briefly detailed the reasons for the agencies’ extension requests including Hurricanes Laura, Delta and Zeta as well as COVID-19 impact. Council members questioned LLA processes for approval and Mr. Cryer explained the steps taken and contact made to allow the entities ample opportunity to submit their reports and vet their excuses for extensions. Representative Schamerhorn made the motion to approve the list of Emergency Extensions – Greater than 90 Days and with no objections, the motion was approved. Representative Schamerhorn made the motion to confirm the list of Emergency Extensions – 90 Days or Less and with no objections, the motion was approved. Reliability of Data in the Sex Offender and Child Predator Registry (Registry) – Performance Audit Issued September 3, 2020 (Video Archive Time 14:45) Chris Magee, Performance Audit Data Analytics Manager, and Irina Hampton, Senior Performance Auditor, presented a summary of the audit. -

Barry Ivey Elected to Louisiana House

Baton Rouge’s CAPITALCAPITAL CITYCITY Community Newspaper ForFor NewsNews Updates,Updates, ‘Like’‘Like’ CapitalCapitalon® FACEBOOK CityCity NewsNews NEWSNEWS® Thursday, March 7, 2013 • Vol. 22, No. 4 • 16 Pages • www.capitalcitynews.us • Phone 225-261-5055 Capital Radio Wars — Part II — Country Country Radio War Country Music: Radio Format That’s Uniquely All-American Woody Jenkins Editor, Capital City News BATON ROUGE — While classical music, opera, and rock and roll are worldwide phenomena, country music is uniquely an American invention. Country music is “Made in the USA!” and Photo by Woody Jenkins Woody by Photo country music fans love the Jenkins Woody by Photo Red, White, and Blue. In 1962, a crusty conser- Sam McQuire at WYNK, 101.5 vative businessman named Gordy Rush of The Tiger 100.7 and Country Legends Bob McGregor launched WYNK, the first country Since 1962, WYNK Has music radio station in the Guaranty Offers Market Baton Rouge market. Today, country music is Been BR Country Giant probably the most popular Two BR Country Stations BATON ROUGE — Bob sively stronger each year. format on radio, and that is BATON ROUGE — For still comes to work at the McGregor launched WYNK Sam McQuire, the mas- also true in Baton Rouge. nearly 50 years, Guaranty company’s headquarters on in 1962 and brought along termind behind much of Baton Rouge has three Broadcasting — now Guar- Government Street — the his conservative values and WYNK’s current success, country music stations — anty Media Ventures — has old Baton Rouge General love of country music. Ba- says the goal of the station WYNK, now owned by been a force in Baton Rouge Hospital. -

2019 Outstanding Family Advocates to Receive the Outstanding Family Advocate Award, a Legislator Must Have Earned a 100% Rating on the 2019 LFF Annual Scorecard

2019 Outstanding Family Advocates To receive the Outstanding Family Advocate Award, a Legislator must have earned a 100% rating on the 2019 LFF Annual Scorecard. LFF awards their courage with a specifically commissioned bust of Patrick Henry, the founding father who famously shouted, “Give me liberty, or give me death!” Senators Jack Donahue Beth Mizell Dale Erdey Neil Riser Jim Fannin Francis Thompson Ryan Gatti Mike Walsworth Gerald Long Mack “Bodi” White John Milkovich Representatives Mark Abraham Frank Hoffman Blake Miguez Beryl Amedee Mike Huval Gregory Miller Raymond Crews Barry Ivey Rogers Pope Rick Edmonds Mike Johnson Jerome Richard Raymond Garofalo Sherman Mack Alan Seabaugh Lance Harris Jack McFarland Valarie Hodges Wayne McMahen 2019 Family Advocates To receive the Family Advocate Award, a Legislator must have achieved more than an 80% rating on the 2019 LFF Annual Scorecard. Senators Sharon Hewitt Rick Ward Representatives Tony Bacala Dodie Horton Larry Bagley Christopher Leopold Taylor Barras Tanner Magee John Berthelot James “Jim” Morris Ryan Bourriaque John “Jay” Morris Stephen Carter Stuart Moss Charles “Bubba” Chaney Nicholas Muscarello Jean-Paul Coussan Steve Pylant Phillip DeVillier Clay Schexnayder Stephen Dwight John Stefanski Reid Falconer Kirk Talbot John Guinn Polly Thomas Cameron Henry Chris Turner Stephanie Hilferty Mark Wright Paul Hollis Jerome “Zee” Zeringue 2019 Life & Liberty Awards Senators Regina Barrow John Milkovich Beth Mizell Life and Liberty Awards are presented each year to legislators who authored and successfully passed key legislation that promotes life and liberty. Representatives Raymond Crews Frank Hoffman Valarie Hodges Katrina Jackson Sharon Hewitt Rick Ward Gladiator Award The Gladiator Award is given to an individual or organization who goes above and beyond the call of duty to preserve the freedoms upon which this nation was founded. -

GREATER BATON ROUGE – STATE REPRESENTATIVES Edmond

GREATER BATON ROUGE – STATE REPRESENTATIVES Edmond Jordan Stephen F. Carter Representative / House District No. 29 / D Representative / House District No. 68 / R 5763 Hooper Rd., Ste. B 3115 Old Forge Baton Rouge, LA 70811-2420 Baton Rouge, LA 70808 (225) 359-9480 225-362-5305 [email protected] [email protected] Franklin Foil Rick Edmonds Representative / House District No. 70 / R Representative / House District No. 66 / R 412 N. 4th St. Suite 220 3931 S. Sherwood Forest Blvd. Suite 200 Baton Rouge, LA 70802 Baton Rouge, La 70816 225-382-3264 225-295-9240 [email protected] [email protected] Barbara Carpenter Denise Marcelle Representative / House District No. 63 / D Representative / House District No. 61 / D 1975 Harding Blvd. 1824 N. Acadian Thruway W. Baton Rouge, LA 70807 Baton Rouge, LA 70802 225-771-5674 225-359-9362 [email protected] [email protected] Tony Bacala Kenny Harvard Representative / House District No. 59 / R Representative / House District No. 62 / R 15482 Airline Highway P.O. Box 217 Prairieville, LA 70769 Jackson, LA 70748 225-677-8020 225-634-7470 [email protected] [email protected] Paula Davis Rogers Pope Representative / House District No. 69 / R Representative / House District No. 71 / R 7902Wrenwood Blvd. Post Office Box 555 Baton Rouge, LA 70809 Denham Springs, LA 70727-0555 225-362-5301 (225) 667-3588 [email protected] [email protected] Ted James John Berthelot Representative / House District No. 101 / D Representative / House District No. 88 / R 445 N. 12th St. 1024 S. -

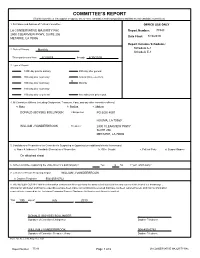

Committee's Report

COMMITTEE’S REPORT (filed by committees that support or oppose one or more candidates and/or propositions and that are not candidate committees) 1. Full Name and Address of Political Committee OFFICE USE ONLY LA CONSERVATIVE MAJORITY PAC Report Number: 77343 2900 CLEARVIEW PKWY, SUITE 206 Date Filed: 7/10/2019 METAIRIE, LA 70006 Report Includes Schedules: Schedule A-1 2. Date of Primary Monthly Schedule E-1 This report covers from 6/1/2019 through 6/30/2019 3. Type of Report: 180th day prior to primary 40th day after general 90th day prior to primary Annual (future election) X 30th day prior to primary Monthly 10th day prior to primary 10th day prior to general Amendment to prior report 4. All Committee Officers (including Chairperson, Treasurer, if any, and any other committee officers) a. Name b. Position c. Address DONALD (BOYSIE) BOLLINGER Chairperson PO BOX 4097 HOUMA, LA 70360 WILLIAM J VANDERBROOK Treasurer 2900 CLEARVIEW PKWY SUITE 206 METAIRIE, LA 70006 5. Candidates or Propositions the Committee is Supporting or Opposing (use additional sheets if necessary) a. Name & Address of Candidate/Description of Proposition b. Office Sought c. Political Party d. Support/Oppose On attached sheet 6. Is the Committee supporting the entire ticket of a political party? Yes X No If “yes”, which party? 7. a. Name of Person Preparing Report WILLIAM J VANDERBROOK b. Daytime Telephone 504-455-0762 8. WE HEREBY CERTIFY that the information contained in this report and the attached schedules is true and correct to the best of our knowledge , information and belief, and that no expenditures have been made nor contributions received that have not been reported herein, and that no information required to be reported by the Louisiana Campaign Finance Disclosure Act has been deliberately omitted .