Building a Healthy Future

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

No. 1168 BELGIUM, DENMARK, FRANCE, IRELAND, ITALY

No. 1168 BELGIUM, DENMARK, FRANCE, IRELAND, ITALY, LUXEMBOURG, NETHERLANDS, NORWAY, SWEDEN and UNITED KINGDOM OF GREAT BRITAIN AND NORTHERN IRELAND Statute of the Council of Europe. Signed at London, on 5 May 1949 Official texts: English and French. Registered by the United Kingdom of Great Britain and Northern Ireland on U April 1951. BELGIQUE, DANEMARK, FRANCE, IRLANDE, ITALIE, LUXEMBOURG, NORVÈGE, PAYS-BAS, ROYAUME-UNI DE GRANDE-BRETAGNE ET D'IRLANDE DU NORD et SUÈDE Statut du Conseil de l'Europe. Signé à Londres, le 5 mai 1949 Textes officiels anglais et fran ais. Enregistr par le Royaume-Uni de Grande-Bretagne et d* Irlande du Nord le II avril 1951. 104 United Nations Treaty Series 1951 No. 1168. STATUTE1 OF THE COUNCIL OF EUROPE. SIGNED AT LONDON, ON 5 MAY 1949 The Governments of the Kingdom of Belgium, the Kingdom of Denmark, the French Republic, the Irish Republic, the Italian Republic, the Grand Duchy of Luxembourg, the Kingdom of the Netherlands, the Kingdom of Norway, the Kingdom of Sweden and the United Kingdom of Great Britain and Northern Ireland : Convinced that the pursuit of peace based upon justice and international co-operation is vital for the preservation of human society and civilisation; Reaffirming their devotion to the spiritual and moral values which are the common heritage of their peoples and the true source of individual freedom, political liberty and the rule of law, principles which form the basis of all genuine democracy; Believing that, for the maintenance and further realisation of these ideals and in -

The Swedish Economy Showed a Relatively Robust Performance in The

2.27. SWEDEN The Swedish economy showed a relatively robust performance in the first quarter of 2020, in spite of the COVID-19 pandemic triggering a sharp deterioration in economic activity from mid-March onwards. Real GDP grew 0.1% q-o-q in the first quarter, mainly due to positive net exports. Even though only some restrictions were put in place to counter the spread of the disease, both the demand and supply side of the economy took a hit. While the rather less restrictive measures helped cushion the immediate impact on the economy, particularly on domestically oriented branches, exporting industries experienced strong declines in output as cross-borders value chains were disrupted. Durable consumer goods, travel services and capital goods-producing sectors were particularly affected. Real GDP is expected to show a sharp fall in the second quarter of 2020, with a recovery following in the second half of the year. The uncertain outlook for demand and lower capacity utilisation should lead to a sharp decline in capital formation this year. Equipment investment is also expected to suffer, as it is the investment category that reacts most strongly to the business cycle. Private consumption decreases follow on from substantial job losses and uncertainty, as well as the impact of restrictions. The sharp fall in economic activity forecast in Sweden’s main trading partners is expected to translate into a large decline in exports. Economic growth is set to turn positive in 2021 as impediments slowly dissipate and the economies of major trading partners recover. A return to work should foster a bounce back in consumption growth in 2021. -

Different Countries – Different Cultures Germany Vs Sweden

Avdelningen för ekonomi Different Countries – Different Cultures Germany vs Sweden Cecilia Jensen och Changiz Saadat Beheshti December 2012 Examensarbete 15 hp C-nivå Examensarbete Akmal Hyder/Lars Ekstrand 1 ABSTRACT Title: Different countries – different cultures Level: Thesis for Bachelor Degree in Business Administration Authors: Cecilia Jensen and Changiz Saadat Behesthi Supervisor: Lars Ekstrand Date: 2011 – 12 Our study is based on two countries, Sweden and Germany, and is aiming to find out if the cultural differences between the two countries have a major impact when doing business together or not. Cross-cultural management is a modern topic and can help transnational companies deal with problems that occur due to different cultures in the organization, but is it really necessary to spend huge amount on intercultural training? We used a qualitative method and did a survey through a convenience sampling among six managers in the two countries. We analyzed the answers sorted by country and then compared them to each other. The result of the survey was that Swedish managers inform and include their staff in decisions to a bigger extend than German managers. Other than the preferences of a more democratic leadership the differences were, according to us, insignificant to perform any cultural training between the two countries. For further studies we suggest a deeper research method with a field study at every workplace, to conclude that the manager‟s answers concurred to the actual outcome. We also think that interviewing more managers, and within the same branch, would increase the creditability of the study. The result indicates that the money spent on intercultural training between Sweden and Germany is quite unnecessary and that the differences are smoothing out. -

Transparency International Sweden

TRANSPARENCY INTERNATIONAL SWEDEN Business Integrity across the Baltic Sea: A needs assessment for effective business integrity in Lithuania and Sweden This assessment is part of the project ”Together towards integrity: Building partnerships for sustainable future in the Baltic Sea region” and has been conducted by financial support from the Swedish Institute. © 2020 Transparency International Sweden Author/Editor: Lotta Rydström Editor: Alf Persson Design: Transparency International Sweden/AB Grafisk Stil Transparency International Sweden (TI Sweden) conducts broad awareness raising efforts to inform decision-makers and the public about the harmful effects of corruption. TI Sweden works for greater transparency, integrity and accountability in both public and private sectors. ”The abuse of entrusted power for private gain”. Transparency International Sweden (TI Sweden) is an independent non-for-profit organisation that, together with a hundred national chapters worldwide, is part of the global coalition Transparency International. Transparency International (TI), founded in 1993 and based in Berlin, has come to be acknowledged in the international arena as the leading organisation combating corruption in all its forms. TABLE OF CONTENT INTRODUCTION ........................................................................................................................................................ 6 Background ................................................................................................................................................ -

GOING GLOBAL EXPORTING to SWEDEN a Guide for Clients

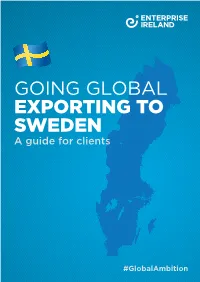

GOING GLOBAL EXPORTING TO SWEDEN A guide for clients #GlobalAmbition Capital Stockholm Population 10.1m1 GDP Per Capita: $52,7662 Unemployment 6.7%3 UMEA SUNDSVALL Swedish exports increased by 23.5% in 20184 Predicted economic growth for 2019 5 UPPSALA 1.9% OREBRO STOCKHOLM KARLSTAD Enterprise Ireland client exports (2018) LINKOPING ¤338m6 JONKOPING GOTHENBURG KALMAR HELSINGBORG MALMO 2 WHY EXPORT TO SWEDEN? Sensitive to change and quick offers a variety of opportunities to Irish businesses. Construction and infrastructure, renewable energy to adapt, Sweden is a global and life sciences are all sectors that have received knowledge and innovation hub. investment in the last few years. With a strong economy and a Bordering Norway and Finland, and connected to highly educated labour force, this Denmark by the Öresund Bridge, Sweden allows good access to the Nordic region. Flight connections is a country where high standards from Ireland to Sweden are good, with direct flights go hand in hand with tomorrow’s to and from Dublin to Stockholm with SAS and brightest ideas. Norwegian. Sweden is a politically stable country whose combination of a largely free-market economy and far-reaching welfare investments has facilitated some of the highest living standards in the world. OTHER ENTERPRISE IRELAND As the EU’s largest producer of renewable energy, CLIENT COMPANIES ARE SELLING 7 timber and iron ore , exports of goods and services INTO SWEDEN, SO WHY AREN’T comprise more than 45% of Sweden’s GDP8. The Swedish economy has performed strongly over YOU? the last few years, and even though GDP growth • Sweden is the 10th best place to do business in is expected to slow down somewhat in 2019, the the world15 economy is still predicted to continue to grow. -

Establishing Business and Managing Workforce in the Nordics

Establishing your business & managing your workforce in the Nordics Contents Establishment of companies in the Nordics Page 4 Employment in the Nordics Page 7 • Did you know (quick facts)? Page 7 • Employment relationships and Governing Law – the basics Page 8 • Employee entitlements and employer obligations at a glance Page 9 • Mandatory employer requirements Page 10 • Terminations Page 14 • Protecting business secrets; non-competition restrictions Page 16 • Transfer of a Business Page 17 Immigration in the Nordics Page 19 Tax and social security obligations Page 23 Data Protection Page 26 2 © 2018 Bird & Bird All Rights Reserved Introduction The Nordic countries offer a very attractive business environment with a well-educated and skilled workforce. The Nordic region is known for its ingenuity and know-how, but also for its relatively unique welfare systems. This, together with a low degree of corruption and a high degree of trust amongst the citizens for the state and business environment that work in tandem with it, provides a unique sphere that many non- Nordic corporations have already discovered. Despite the many similarities between Finland, Sweden and Denmark, both in terms of history and cultural values, there are notable differences when it comes to the approach taken to establish a business friendly environment. HR professionals and other individuals with a pan-Nordic responsibility need to be aware of these differences, as methods and practices that have proved to work perfectly in one country, might not work in another. The purpose of this brochure is to provide a quick overview of basic elements relevant for establishing and building your business in the Nordic region, including assisting in the process of deciding in which country to start. -

Strategic Cooperation Between Sweden and Poland – Update of the Background Paper

Warsaw, 14th October 2013 Strategic cooperation between Sweden and Poland – update of the Background Paper European Union The financial crisis Continuing close bilateral cooperation on issues associated with the Economic and Financial Affairs Council (ECOFIN). Europe 2020 The EU growth agenda Europe 2020 involves a large number of policy areas. The focus is on structural reforms at national level, following an annual process known as the European semester. Cooperation on the enhancement of the European semester. Sweden and Poland have similar views on growth issues, as manifested, for example, being among the countries signing a joint letter to President Van Rompuy and President Barroso – ‘A plan for growth in Europe’. Like-minded cooperation in the internal market context has clear links to Europe 2020. Internal market Continued cooperation based on current like-minded endeavours in the internal market area, with a focus on growth-promoting measures, particularly in the three principal areas of the digital single market, better regulation and trade in services. 2 Cooperation on the completion of negotiations concerning the two single market acts, eCommerce and the Baltic Sea Strategy (including agency-level cooperation), as well as promotion of women’s participation in the labour market. Cooperation on two flagship initiatives aimed at eliminating trade barriers in the region (National Board of Trade) and sharing expertise at regional level (Swedish Board for Accreditation and Conformity Assessment). One result of the cooperation in the internal market area is a joint Swedish-Polish initiative for a Nordic-Baltic-Visegrad meeting in Stockholm in June 2013. EU Strategy for the Baltic Sea Region (EUSBSR) Cooperation on the future strategic direction of the EU Strategy for the Baltic Sea Region, including the external dimension and collaboration with relevant multilateral organisations. -

The History of Nordic Labour Law

The Roots – the History of Nordic Labour Law Ole Hasselbalch 1 Scandinavian Societies and Law-Tradition …………………………….. 12 2 Relics of Feudalism and Rise of the Individual Contract ……………… 14 3 The Collective Dimension ………………………………………………... 15 3.1 Denmark ……………………………………………………………. 16 3.2 Norway ……………………………………………………………… 18 3.3 Sweden ……………………………………………………………… 19 3.4 Finland ……………………………………………………………… 21 4 State Intervention in Labour Relations………………………………….. 22 4.1 Welfare Legislation and Social Security ……………………………. 22 4.2 Rise of Responsibility for Social Security on The Job ……………… 24 4.2.1 Health and Safety at Work and Industrial Injuries …………. 24 4.2.2 Loss of Wages During Employment ………………………. 26 4.2.3 Unemployment and Protection Against Dismissals ……….. 28 4.2.3.1 Protection Against Dismissals ……………………. 28 4.2.3.2. Unemployment Insurance ………………………... 29 4.2.3.3 Labour Exchange ………………………………… 29 5 Integration: Co-Influence and Co-Determination ……………………… 30 6 Turbulence: Growing State-Intervention, Internationalisation, Market-orientation and Reorganisation ………… 33 References in Non-Scandinavian Languages …………………………..………. 35 © Stockholm Institute for Scandianvian Law 1957-2009 12 Ole Hasselbalch: The Roots: The History of Nordic Labour Law The term “the Nordic model” has been widely used by international labour lawyers to indicate special features which characterise Scandinavian labour law. This article outlines the history of the Nordic model, thereby demonstrating the reasons for using the term Nordic Model to indicate common Scandinavian trends in this particular field of law. 1 Scandinavian Societies and Law-Tradition Traditionally, the Scandinavian countries have close mutual ties, which is owing to their common cultural and linguistic background. To a large degree their social development have followed identical paths too. Thus Scandinavia today forms a common area of language and culture and the various functions of societies are based on a common tradition. -

The Øresund Fixed Link (Denmark – Sweden)

Draft for Consultation The Øresund Fixed Link (Denmark – Sweden) Source: Ramboll Location Copenhagen (Denmark) – Malmö (Sweden) Northern Europe, Øresund region, Sector Transportation Procuring Authorities Øresundsbro Konsortiet Project Company Øresundsbro Konsortiet Project Company Obligations Design, Build, Finance, Maintain, Own and Operate (DBFMOO) Financial Closure Year - Capital Value USD 3.7 billion (DKK 30.1 billion) 2000 prices Start of Operations 2000 Contract Period (years) - Key Facts Government financed, 100% user funded 1/11 Draft for Consultation Project highlights The Øresund Fixed Link (the Link) is a fixed combined bridge and tunnel link across the Øresund Sound (the Sound) between Denmark and Sweden. It comprises: ● The Øresund tunnel between Amager – at Kastrup, south of Copenhagen, and the artificial island Peberholm. 1 ● The Øresund Bridge, a combined girder and cable-stayed bridge between Peberholm and Lernacken – south of Malmö, in Skåne. The Link is composed of a motorway and a dual 1. The Øresund Fixed Link rail track. The total length is 15.9 km. (Source: Øresundsbro Konsortiet) The Øresund Fixed Link is owned and operated by Øresundsbro Konsortiet, which is jointly owned by state-owned enterprises A/S Øresund and Svensk-danska Broförbindelsen (SVEDAB) AB. The latter is owned by the Swedish Government, while A/S Øresund is 100 per cent owned by Sund & Bælt, which is owned by the Danish state (see also Figure Error! Reference source not found.). The total cost of the Link, including the motorway and rail connection on land, was calculated at DKK 30.1 billion in 2000 (circa USD 3.7 billion, 2000 prices). The realisation of the project received financial support of DKK 780 million (USD 96.6 million) from the Trans-European Transport Network (TEN-T) funding. -

Norway Sweden Finland Russia Iceland Canada Alaska (United

TERRITORIAL DISPUTES Aleutian Islands 1 Delimitation of the boundary between Russia and Norway in the Barents Sea PACIFIC 5 OCEAN 2 The sovereignty of Hans Island, claimed by Greenland (Denmark) and Canada 3 Management and control of the North-West Passage ºbetween the United States BERING SEA EXXON VALDEZ and Canada) Delimitation of the boundary between TRANS-ALASKA Anchorage BERING 4 PIPELINE SYSTEM (TAPS) STRAIT Alaska (United States) and Canada North-East in the Beaufort Sea Alaska Passage (United States) Chukotka 5 Delimitation of the boundary between Alaska (United States) and Russia Fairbanks in the Barents Sea BEAUFORT SEA New 4 Siberian Islands 3 Banks LAPTEV Island SEA Victoria Island Queen ARCTIC North-West Elizabeth OCEAN Canada Islands Passage Russia Alpha Ridge Lomonosov Ridge North Resolute NORTH Land Norilsk Bay POLE HUDSON Ellesmere Nansen BAY Nanisivik Island Gakkel KARA Ridge SEA Franz Novy Urengoï Thulé 2 Hans Josef Land Island (Russia) BAFFIN Baffin Novaya Island BAY Salekhard Zemlya Vorkuta Nadym Svalbard 1 Shtokman Canada Greenland (Norway) gas field (Denmark) USINSK DAVIS BARENTS Peshora STRAIT Bear Island SEA GREENLAND SEA (Norway) Nuuk Murmansk Jan Monchegorsk Mayen Island (Norway) Tromsø Archangelsk NORWEGIAN Apatity SEA Bodø Rovaniemi Severodvinsk Towards the major Major urban populations American ports Iceland 400,000 Finland Towards 200,000 Reykjavik 100,000 Western Europe 50,000 Sea routes which will come into Sweden St Petersburg permanent use within 10 or 15 ATLANTIC Norway Maritime areas claimed by years, -

FATCA Agreement Sweden

Agreement between the Government of the United States of America and the Government of Sweden to Improve International Tax Compliance and to Implement FATCA Whereas, the Government of the United States of America and the Government of Sweden (each, a “Party,” and together, the “Parties”) have a longstanding and close relationship with respect to mutual assistance in tax matters and desire to conclude an agreement to improve international tax compliance by further building on that relationship; Whereas, Article 26 of the Convention Between the Government of the United States of America and the Government of Sweden for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with Respect to Taxes on Income done at Stockholm on September 1, 1994, together with a related exchange of notes, and as amended by the Protocol done at Washington on September 30, 2005, (together the “Convention”), authorizes the exchange of information for tax purposes, including on an automatic basis; Whereas, the United States of America enacted provisions commonly known as the Foreign Account Tax Compliance Act (“FATCA”), which introduce a reporting regime for financial institutions with respect to certain accounts; Whereas, the Government of Sweden is supportive of the underlying policy goal of FATCA to improve tax compliance; Whereas, FATCA has raised a number of issues, including that Swedish financial institutions may not be able to comply with certain aspects of FATCA due to domestic legal impediments; Whereas, the Government of the United States -

Sweden, Norway & Denmark Information

Sweden, Norway & Denmark Information Sweden, Norway and Denmark are highlighted by charming, pristine cities, spectacular fjords, and a smorgasbord of cultural traditions. From Viking lore to pop culture icons and unmatched hospitality, these Nordic lands are sure to enthrall and delight. And with surroundings as serene as this, you’ll come to understand how they became host to the world’s most revered peace prize. History As merchant seamen, well known for their far-reaching trade, the Nordic Vikings dominated Europe in the eighth and ninth centuries. Many historians credit the Vikings with the first European discovery of the Americas, with the exploits of Leif Ericsson around 1000. In 1397, Queen Margaret of Denmark united Sweden (which included Finland), Norway, Denmark, Iceland, Greenland and other territories into the Kalmar Union. Tension within the countries gradually led to open conflict and the union split in the early sixteenth century. A long-lived rivalry ensued with Norway and Denmark on one side and Sweden and Finland on the other. During the seventeenth century, Sweden-Finland emerged as a great power. Its contributions during the Thirty Years’ War under Gustavus Adolphus determined the political, as well as religious, balance of power in Europe. At its zenith in 1658, Sweden ruled several provinces of Denmark, as well as parts of present-day Germany, Russia, Estonia and Latvia. In 1813, Sweden joined the allies against Napoleon, which resulted in the acquisiton of Norway from Denmark (an ally of Napoleon). The merger lasted until 1905, when Norway peaceably gained its independence. Sweden has not participated in any war in almost two centuries.