Master Thesis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

WORLD AVIATION Yearbook 2013 EUROPE

WORLD AVIATION Yearbook 2013 EUROPE 1 PROFILES W ESTERN EUROPE TOP 10 AIRLINES SOURCE: CAPA - CENTRE FOR AVIATION AND INNOVATA | WEEK startinG 31-MAR-2013 R ANKING CARRIER NAME SEATS Lufthansa 1 Lufthansa 1,739,886 Ryanair 2 Ryanair 1,604,799 Air France 3 Air France 1,329,819 easyJet Britis 4 easyJet 1,200,528 Airways 5 British Airways 1,025,222 SAS 6 SAS 703,817 airberlin KLM Royal 7 airberlin 609,008 Dutch Airlines 8 KLM Royal Dutch Airlines 571,584 Iberia 9 Iberia 534,125 Other Western 10 Norwegian Air Shuttle 494,828 W ESTERN EUROPE TOP 10 AIRPORTS SOURCE: CAPA - CENTRE FOR AVIATION AND INNOVATA | WEEK startinG 31-MAR-2013 Europe R ANKING CARRIER NAME SEATS 1 London Heathrow Airport 1,774,606 2 Paris Charles De Gaulle Airport 1,421,231 Outlook 3 Frankfurt Airport 1,394,143 4 Amsterdam Airport Schiphol 1,052,624 5 Madrid Barajas Airport 1,016,791 HE EUROPEAN AIRLINE MARKET 6 Munich Airport 1,007,000 HAS A NUMBER OF DIVIDING LINES. 7 Rome Fiumicino Airport 812,178 There is little growth on routes within the 8 Barcelona El Prat Airport 768,004 continent, but steady growth on long-haul. MostT of the growth within Europe goes to low-cost 9 Paris Orly Field 683,097 carriers, while the major legacy groups restructure 10 London Gatwick Airport 622,909 their short/medium-haul activities. The big Western countries see little or negative traffic growth, while the East enjoys a growth spurt ... ... On the other hand, the big Western airline groups continue to lead consolidation, while many in the East struggle to survive. -

2021 Datalex Big Book of Airline Data Page 0

2021 Datalex Big Book of Airline Data Page 0 2021 Datalex Big Book of Airline Data by IdeaWorksCompany Table of Contents Updates to the 2021 Datalex Big Book of Airline Data .................................................................................... 3 A. Welcome Message from Datalex .................................................................................................................. 5 B. Introduction to the Data ................................................................................................................................. 6 About Special Reporting Periods ....................................................................................................................... 7 Year over Year Comparisons are Introduced this Year............................................................................... 8 2020 Was Bad – But There Were a Few Bright Spots ................................................................................. 9 C. Airline Traffic for the 2020 Period .............................................................................................................. 12 Primary Airlines in Alphabetical Order .......................................................................................................... 12 Subsidiary Airlines in Alphabetical Order ...................................................................................................... 18 Primary Airlines by Traffic ................................................................................................................................ -

The Change Is NOW ! EXECUTIVE SUMMARY

The change is NOW ! EXECUTIVE SUMMARY The inflight business has changed dramatically in recent years The aim of this presentation is to share and point out the recent evolution we, at ISG , have noticed To provide food for thought on how we can all remain competitive & efficient while answering the new expectations of our customers. AGENDA Introduction of Inflight Sales Group PART I : Evolution of passengers’ expectations PART II : Market revolution PART III : Airline perspective INTRODUCTION Inflight Sales Group ISG – The original concessionaire 2015 Opening of an ISG Office in Riga with a team dedicated to Russia and Eastern Europe Opening of Supplier of amenity kits to 2014 the European 1982 more than 60 Airlines 1994 Rapid growth from 1 ISG Office in worldwide and an airline to 34 airlines Paris exclusive distributor of major duty free brands 1996 Establishment of Awarded another Inflight Sales Group 2013 long term 1986 1st Concession at (HK) Ltd contract with Pan American Cathay Pacific and Dragonair 1999 Expansion to Asian Airlines WINNER OF MULTIPLE AWARDS “Inflight Travel Retailer of the Year” from Duty Free News International (DFNI) 2008 / 2009 / 2010 / 2011 / 2012 / 2015 “Inflight Travel Retailer of the Year” At Frontier Awards 2010 / 2011 / 2012 / 2013 / 2014 “Best new marketing initiative” in 2008 “Best Inflight Concessionaire” at the Airline Retail Conferences (ARC) in Singapore and Paris 2013 / 2014 / 2015 OUR EXPANDING CUSTOMERS FOOTPRINT ISG is proud to partner with 26 airlines worldwide Our commitment in building long-term relationships with our clients, offering innovative product sourcing and revolutionary service solutions has successfully taken inflight revenue to new heights and transformed duty free as a core component of the airline business. -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

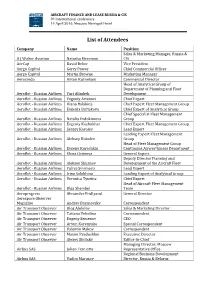

List of Attendees

AIRCRAFT FINANCE AND LEASE RUSSIA & CIS 8th international conference 14 April 2016, Moscow Metropol Hotel List of Attendees Company Name Position Sales & Marketing Manager, Russia & A J Walter Aviation Natasha Meerman CIS AerCap David Beker Vice President Aergo Capital Gerry Power Chief Commercial Officer Aergo Capital Martin Browne Marketing Manager Aerocredo Anton Kuznetsov Commercial Director Head of Analytical Group of Department of Planning and Fleet Aeroflot - Russian Airlines Yuri Alimbek Development Aeroflot - Russian Airlines Evgeniy Artemov Chief Expert Aeroflot - Russian Airlines Diana Balakina Chief Expert Fleet Management Group Aeroflot - Russian Airlines Evgenia Burlakova Chief Expert of Analytical Group Chief Specialist Fleet Management Aeroflot - Russian Airlines Natalia Evdokimova Group Aeroflot - Russian Airlines Evgeniy Kozhukhar Chief Expert Fleet Management Group Aeroflot - Russian Airlines Sergey Korolev Lead Expert Leading Expert Fleet Management Aeroflot - Russian Airlines Aleksey Kukolev Group Head of Fleet Management Group Aeroflot - Russian Airlines Evgeny Kurochkin Continuing Airworthiness Department Aeroflot - Russian Airlines Elena Ozimova General Expert Deputy Director Planning and Aeroflot - Russian Airlines Aleksey Siluanov Development of the Aircraft Fleet Aeroflot - Russian Airlines Yuliya Smirnova Lead Expert Aeroflot - Russian Airlines Irina Solokhina Leading Expert of Analytical Group Aeroflot - Russian Airlines Veronica Tyurina Chief Expert Head of Aircraft Fleet Management Aeroflot - Russian Airlines -

List of Foreign EASA Part-145 Approved Organisations

EASA-IFP - List of Valid Foreign Part 145 organisations (WEB) List of valid Foreign Part-145 organisations This list contains valid approvals, including limited and partially suspended ones. Approved organisations EASA approval number Certificate address Country - Status of Approval: Patially Suspended (3) EASA.145.0469 NW TECHNIC LLC RUSSIA EASA.145.0547 ONUR AIR TASIMACILIK A.S. D/B/A ONUR AIR TURKEY EASA.145.0660 LIMITED LIABILITY COMPANY ''UTG DOMODEDOVO'' T/A UTG AVIATION SERVICES RUSSIA - Status of Approval: Valid (334) EASA.145.0003 GOODRICH AEROSTRUCTURES SERVICE (CENTER-ASIA) PTE Ltd. SINGAPORE EASA.145.0005 CHROMALLOY (THAILAND) LTD. THAILAND EASA.145.0007 ''UZBEKISTAN AIRWAYS TECHNICS'' LIMITED LIABILITY COMPANY UZBEKISTAN EASA.145.0008 KUWAIT AIRWAYS COMPANY KUWAIT EASA.145.0010 ABU DHABI AVIATION UNITED ARAB EMIRATES EASA.145.0012 AEROFLOT RUSSIAN AIRLINES RUSSIA EASA.145.0015 AIR ASTANA JSC KAZAKHSTAN EASA.145.0016 AI ENGINEERING SERVICES LIMITED t/a AIESL INDIA EASA.145.0017 AIR MAURITIUS Ltd. MAURITIUS EASA.145.0018 AIRFOIL SERVICES SDN. BHD. MALAYSIA EASA.145.0019 GE AVIATION, ENGINE SERVICES - SING PTE. LTD. SINGAPORE EASA.145.0020 ALIA - THE ROYAL JORDANIAN AIRLINES PLC CO (ROYAL JORDANIAN) JORDAN EASA.145.0021 AIRCRAFT MAINTENANCE AND ENGINEERING CORPORATION, BEIJING (AMECO) CHINA EASA.145.0022 AMSAFE AVIATION (CHONGQING) Ltd. CHINA EASA.145.0024 ASIA PACIFIC AEROSPACE Pty. Ltd. AUSTRALIA EASA.145.0025 ASIAN COMPRESSOR TECHNOLOGY SERVICES CO. LTD. TAIWAN EASA.145.0026 ASIAN SURFACE TECHNOLOGIES PTE LTD SINGAPORE EASA.145.0027 AEROVIAS DEL CONTINENTE AMERICANO S AVIANCA S.A. COLOMBIA EASA.145.0028 BAHRAIN AIRPORT SERVICES BAHRAIN EASA.145.0029 ISRAEL AEROSPACE INDUSTRIES, Ltd. -

Aurora Airlines to Launch New Charter Service Between Narita and Yuzhno-Sakhalinsk!

[Joint Press Release] Aurora Airlines (UTS Air Service Inc.) Narita International Airport Corporation Aurora Airlines to Launch New Charter Service between Narita and Yuzhno-Sakhalinsk! Tokyo, 15 April 2014: We are delighted to announce the launch of a new charter service between Narita and Yuzhno-Sakhalinsk to be operated by Aurora Airlines (IATA Code: HZ) from Thursday, 1 May 2014. Aurora Airlines was established in September 2013 by amalgamating SAT Airlines and Vladivostok Air. It operates domestic services within Russia between Yuzhno-Sakhalinsk and major cities in the Russian Far East, while operating international services from Yuzhno-Sakhalinsk to 3 countries including the Narita route. Yuzhno-Sakhalinsk, the capital of the state of Sakhalin in Russia is located two and a half hours away from Narita by air, and is a key economic and cultural center and as the base for large-scale underground resource development projects by joint ventures comprising firms from Japan, Russia, Europe and the US. The launch of this new Aurora Airlines service will stimulate greater exchanges between Japan and the Russian Far East region. Flight Schedule: 2 flights/week (Tue, Thu) from 1 May 2014 Flight Departure STD Arrival STA Outbound HZ9234 Narita 16:30 Y-Sakhalinsk 21:00 Inbound HZ9233 Y-Sakhalinsk 13:05 Narita 13:50 * All times local Terminal: Terminal 1, North Wing Aircraft: Boeing B737-500 Seating Capacity: 108 in total (8 Business Class, 100 Economy Class) * Conditional upon approval by the relevant governments. Schedule and other details are subject to change without notice. *Courtesy of Aurora Airlines . -

Air Transport in Russia and Its Impact on the Economy

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Tomsk State University Repository Вестник Томского государственного университета. Экономика. 2019. № 48 МИРОВАЯ ЭКОНОМИКА UDC 330.5, 338.4 DOI: 10.17223/19988648/48/20 V.S. Chsherbakov, O.A. Gerasimov AIR TRANSPORT IN RUSSIA AND ITS IMPACT ON THE ECONOMY The study aims to collect and analyse statistics of Russian air transport, show the in- fluence of air transport on the national economy over the period from 2007 to 2016, compare the sector’s role in Russia with the one in other countries. The study reveals the significance of air transport for Russian economy by comparing airlines’ and air- ports’ monetary output to the gross domestic product. On the basis of the research, the policies in the aviation sector can be adjusted by government authorities. Ключевые слова: Russia, aviation, GDP, economic impact, air transport, statistics. Introduction According to Air Transport Action Group, the air transport industry supports 62.7 million jobs globally and aviation’s total global economic impact is $2.7 trillion (approximately 3.5% of the Gross World Product) [1]. Aviation transported 4 billion passengers in 2017, which is more than a half of world population, according to the International Civil Aviation Organization [2]. It makes the industry one of the most important ones in the world. It has a consid- erable effect on national economies by providing a huge number of employment opportunities both directly and indirectly in such spheres as tourism, retail, manufacturing, agriculture, and so on. Air transport is a driving force behind economic connection between different regions because it may entail economic, political, and social effects. -

Frequently Asked Questions About Oneworld, Codeshare and Other Partner Airlines

FREQUENTLY ASKED QUESTIONS ABOUT ONEWORLD, CODESHARE AND OTHER PARTNER AIRLINES 1. What will happen to AA’s participation in the oneworld Alliance and its relationships with its codeshare partners or other partner airlines? We expect our participation in oneworld and our relationships with our other partners to remain unchanged. 2. Can I still accrue miles and redeem mileage awards through oneworld and American's frequent flyer air partners? Yes, we expect our partnerships with airlines such as British Airways, Cathay Pacific, Finnair, Iberia, Japan Airlines (JAL), LAN, Malév, Qantas, Royal Jordanian and S7 Airlines and others remain unchanged as a result of the Chapter 11 filing. 3. Will my elite status with AAdvantage still be recognized by oneworld Alliance partners? Yes, we expect that your elite status with AAdvantage will continue to be recognized by our oneworld partners, and that the benefits you receive when flying with them will not change as a result of the Chapter 11 filing. 4. Will there be a reduction of routes that AA currently offers through oneworld and its codeshare partners? We remain deeply committed to meeting your travel needs with the same standards of safe, secure and reliable service, and intend to maintain a strong presence in domestic and international markets. As we and all airlines routinely do, we will continue to evaluate our operations and service, assuring that our network is as efficient and productive as possible. 5. Will AA’s airline partners continue to honor their ticket reservation and baggage transfer commitments? Yes. We expect that all benefits with partner airlines will remain intact. -

Monthly OTP July 2019

Monthly OTP July 2019 ON-TIME PERFORMANCE AIRLINES Contents On-Time is percentage of flights that depart or arrive within 15 minutes of schedule. Global OTP rankings are only assigned to all Airlines/Airports where OAG has status coverage for at least 80% of the scheduled flights. Regional Airlines Status coverage will only be based on actual gate times rather than estimated times. This July result in some airlines / airports being excluded from this report. If you would like to review your flight status feed with OAG pleas [email protected] MAKE SMARTER MOVES Airline Monthly OTP – July 2019 Page 1 of 1 Home GLOBAL AIRLINES – TOP 50 AND BOTTOM 50 TOP AIRLINE ON-TIME FLIGHTS On-time performance BOTTOM AIRLINE ON-TIME FLIGHTS On-time performance Airline Arrivals Rank No. flights Size Airline Arrivals Rank No. flights Size SATA International-Azores GA Garuda Indonesia 93.9% 1 13,798 52 S4 30.8% 160 833 253 Airlines S.A. XL LATAM Airlines Ecuador 92.0% 2 954 246 ZI Aigle Azur 47.8% 159 1,431 215 HD AirDo 90.2% 3 1,806 200 OA Olympic Air 50.6% 158 7,338 92 3K Jetstar Asia 90.0% 4 2,514 168 JU Air Serbia 51.6% 157 3,302 152 CM Copa Airlines 90.0% 5 10,869 66 SP SATA Air Acores 51.8% 156 1,876 196 7G Star Flyer 89.8% 6 1,987 193 A3 Aegean Airlines 52.1% 155 5,446 114 BC Skymark Airlines 88.9% 7 4,917 122 WG Sunwing Airlines Inc. -

U.S. Department of Transportation Federal

U.S. DEPARTMENT OF ORDER TRANSPORTATION JO 7340.2E FEDERAL AVIATION Effective Date: ADMINISTRATION July 24, 2014 Air Traffic Organization Policy Subject: Contractions Includes Change 1 dated 11/13/14 https://www.faa.gov/air_traffic/publications/atpubs/CNT/3-3.HTM A 3- Company Country Telephony Ltr AAA AVICON AVIATION CONSULTANTS & AGENTS PAKISTAN AAB ABELAG AVIATION BELGIUM ABG AAC ARMY AIR CORPS UNITED KINGDOM ARMYAIR AAD MANN AIR LTD (T/A AMBASSADOR) UNITED KINGDOM AMBASSADOR AAE EXPRESS AIR, INC. (PHOENIX, AZ) UNITED STATES ARIZONA AAF AIGLE AZUR FRANCE AIGLE AZUR AAG ATLANTIC FLIGHT TRAINING LTD. UNITED KINGDOM ATLANTIC AAH AEKO KULA, INC D/B/A ALOHA AIR CARGO (HONOLULU, UNITED STATES ALOHA HI) AAI AIR AURORA, INC. (SUGAR GROVE, IL) UNITED STATES BOREALIS AAJ ALFA AIRLINES CO., LTD SUDAN ALFA SUDAN AAK ALASKA ISLAND AIR, INC. (ANCHORAGE, AK) UNITED STATES ALASKA ISLAND AAL AMERICAN AIRLINES INC. UNITED STATES AMERICAN AAM AIM AIR REPUBLIC OF MOLDOVA AIM AIR AAN AMSTERDAM AIRLINES B.V. NETHERLANDS AMSTEL AAO ADMINISTRACION AERONAUTICA INTERNACIONAL, S.A. MEXICO AEROINTER DE C.V. AAP ARABASCO AIR SERVICES SAUDI ARABIA ARABASCO AAQ ASIA ATLANTIC AIRLINES CO., LTD THAILAND ASIA ATLANTIC AAR ASIANA AIRLINES REPUBLIC OF KOREA ASIANA AAS ASKARI AVIATION (PVT) LTD PAKISTAN AL-AAS AAT AIR CENTRAL ASIA KYRGYZSTAN AAU AEROPA S.R.L. ITALY AAV ASTRO AIR INTERNATIONAL, INC. PHILIPPINES ASTRO-PHIL AAW AFRICAN AIRLINES CORPORATION LIBYA AFRIQIYAH AAX ADVANCE AVIATION CO., LTD THAILAND ADVANCE AVIATION AAY ALLEGIANT AIR, INC. (FRESNO, CA) UNITED STATES ALLEGIANT AAZ AEOLUS AIR LIMITED GAMBIA AEOLUS ABA AERO-BETA GMBH & CO., STUTTGART GERMANY AEROBETA ABB AFRICAN BUSINESS AND TRANSPORTATIONS DEMOCRATIC REPUBLIC OF AFRICAN BUSINESS THE CONGO ABC ABC WORLD AIRWAYS GUIDE ABD AIR ATLANTA ICELANDIC ICELAND ATLANTA ABE ABAN AIR IRAN (ISLAMIC REPUBLIC ABAN OF) ABF SCANWINGS OY, FINLAND FINLAND SKYWINGS ABG ABAKAN-AVIA RUSSIAN FEDERATION ABAKAN-AVIA ABH HOKURIKU-KOUKUU CO., LTD JAPAN ABI ALBA-AIR AVIACION, S.L. -

Recognised Leadership

ANNUAL REPORT 2013 RECOGNISED LEADERSHIP 1 Contents 1. 2. 4. 5. ABOUT THE COMPANY LETTERS TO CORPORATE RISK SHAREHOLDERS GOVERNANCE MANAGEMENT AND SECURITIES 5 22 81 109 1.1. Aeroflot Today ...............................................................................6 2.1. Letter from the Chairman of the Board of Directors................ 22 4.1. Corporate Governance ............................................................. 82 1.2. A Year of Confident Growth......................................................... 8 2.2. Letter from the Chief Executive Officer.................................... 24 Corporate Governance Principles ............................................ 82 1.3. Main Events in 2013................................................................... 10 Structure of Corporate Governance ......................................... 83 1.4. Aircraft Fleet and Route Network.............................................. 14 General Meeting of Shareholders ............................................ 83 1.5. Acclaim for the Company from Passengers and Professionals .20 Board of Directors ..................................................................... 83 Committees of the Board of Directors .....................................91 Executive Board ........................................................................ 93 3. Committees ............................................................................ 100 Internal Control and Audit ........................................................101 DESCRIPTION OF THE