Privatization of Public Enterprises in Zambia: an Evaluation of the Policies, Procedures and Experiences

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Appendix 25 Box 31/3 Airline Codes

March 2021 APPENDIX 25 BOX 31/3 AIRLINE CODES The information in this document is provided as a guide only and is not professional advice, including legal advice. It should not be assumed that the guidance is comprehensive or that it provides a definitive answer in every case. Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 000 ANTONOV DESIGN BUREAU 001 AMERICAN AIRLINES 005 CONTINENTAL AIRLINES 006 DELTA AIR LINES 012 NORTHWEST AIRLINES 014 AIR CANADA 015 TRANS WORLD AIRLINES 016 UNITED AIRLINES 018 CANADIAN AIRLINES INT 020 LUFTHANSA 023 FEDERAL EXPRESS CORP. (CARGO) 027 ALASKA AIRLINES 029 LINEAS AER DEL CARIBE (CARGO) 034 MILLON AIR (CARGO) 037 USAIR 042 VARIG BRAZILIAN AIRLINES 043 DRAGONAIR 044 AEROLINEAS ARGENTINAS 045 LAN-CHILE 046 LAV LINEA AERO VENEZOLANA 047 TAP AIR PORTUGAL 048 CYPRUS AIRWAYS 049 CRUZEIRO DO SUL 050 OLYMPIC AIRWAYS 051 LLOYD AEREO BOLIVIANO 053 AER LINGUS 055 ALITALIA 056 CYPRUS TURKISH AIRLINES 057 AIR FRANCE 058 INDIAN AIRLINES 060 FLIGHT WEST AIRLINES 061 AIR SEYCHELLES 062 DAN-AIR SERVICES 063 AIR CALEDONIE INTERNATIONAL 064 CSA CZECHOSLOVAK AIRLINES 065 SAUDI ARABIAN 066 NORONTAIR 067 AIR MOOREA 068 LAM-LINHAS AEREAS MOCAMBIQUE Page 2 of 19 Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 069 LAPA 070 SYRIAN ARAB AIRLINES 071 ETHIOPIAN AIRLINES 072 GULF AIR 073 IRAQI AIRWAYS 074 KLM ROYAL DUTCH AIRLINES 075 IBERIA 076 MIDDLE EAST AIRLINES 077 EGYPTAIR 078 AERO CALIFORNIA 079 PHILIPPINE AIRLINES 080 LOT POLISH AIRLINES 081 QANTAS AIRWAYS -

Economic Report 2000

Republic of Zambia ECONOMIC REPORT 2000 Ministry of Finance and Economic Development Box 50062 Lusaka January 2001 Price K30,000 Table of Contents Chapter Topic Page 1 DEVELOPMENTS IN THE GLOBAL ECONOMY DEVELOPMENTS IN THE DOMESTIC ECONOMY Public Finance Monetary, banking and non-banking financial sector developments Consumer Price Developments Capital market developments Population, Labour and Employment Developments External Sector Developments External Aid External Debt and Debt Management Progress Towards Accessing the enhanced HIPC Initiative 2 SECTORAL PERFORMANCE Agriculture, forestry and fisheries sector Mining and Quarrying Sector Manufacturing sector Transport, Storage and Communications Energy and Water Developments Construction and Building Tourism Environment and Natural Resource Conservation Private Sector development Education Science, Technology and Vocational Training Health Community, Social and Personal Services Gender and Development Sport, Youth and Child Development1 3 PROSPECTS FOR 2001 Pa ge 2 Economic Report --- 2000 FOREWORD I am pleased to present the annual Economic Report for the year 2000. This report evaluates the performance of the economy during the year 2000. On 27 th January 2000, the Minister of Finance and Economic Development, Honourable Dr. Katele Kalumba, M.P., presented the 2000 National Budget to Parliament. The Budget highlighted the objectives and programmes of the Government for the year under review. Although the country experienced macroeconomic instability in the year 2000, it showed resilience by registering a positive growth rate of 3.5 percent compared to 2.0 percent in 1999. Positive developments in manufacturing, real estate and transport and communication sectors contributed to the growth. The growth was, however, against the backdrop of rising inflation and rapid depreciation of the Kwacha. -

U.S. Department of Transportation Federal

U.S. DEPARTMENT OF ORDER TRANSPORTATION JO 7340.2E FEDERAL AVIATION Effective Date: ADMINISTRATION July 24, 2014 Air Traffic Organization Policy Subject: Contractions Includes Change 1 dated 11/13/14 https://www.faa.gov/air_traffic/publications/atpubs/CNT/3-3.HTM A 3- Company Country Telephony Ltr AAA AVICON AVIATION CONSULTANTS & AGENTS PAKISTAN AAB ABELAG AVIATION BELGIUM ABG AAC ARMY AIR CORPS UNITED KINGDOM ARMYAIR AAD MANN AIR LTD (T/A AMBASSADOR) UNITED KINGDOM AMBASSADOR AAE EXPRESS AIR, INC. (PHOENIX, AZ) UNITED STATES ARIZONA AAF AIGLE AZUR FRANCE AIGLE AZUR AAG ATLANTIC FLIGHT TRAINING LTD. UNITED KINGDOM ATLANTIC AAH AEKO KULA, INC D/B/A ALOHA AIR CARGO (HONOLULU, UNITED STATES ALOHA HI) AAI AIR AURORA, INC. (SUGAR GROVE, IL) UNITED STATES BOREALIS AAJ ALFA AIRLINES CO., LTD SUDAN ALFA SUDAN AAK ALASKA ISLAND AIR, INC. (ANCHORAGE, AK) UNITED STATES ALASKA ISLAND AAL AMERICAN AIRLINES INC. UNITED STATES AMERICAN AAM AIM AIR REPUBLIC OF MOLDOVA AIM AIR AAN AMSTERDAM AIRLINES B.V. NETHERLANDS AMSTEL AAO ADMINISTRACION AERONAUTICA INTERNACIONAL, S.A. MEXICO AEROINTER DE C.V. AAP ARABASCO AIR SERVICES SAUDI ARABIA ARABASCO AAQ ASIA ATLANTIC AIRLINES CO., LTD THAILAND ASIA ATLANTIC AAR ASIANA AIRLINES REPUBLIC OF KOREA ASIANA AAS ASKARI AVIATION (PVT) LTD PAKISTAN AL-AAS AAT AIR CENTRAL ASIA KYRGYZSTAN AAU AEROPA S.R.L. ITALY AAV ASTRO AIR INTERNATIONAL, INC. PHILIPPINES ASTRO-PHIL AAW AFRICAN AIRLINES CORPORATION LIBYA AFRIQIYAH AAX ADVANCE AVIATION CO., LTD THAILAND ADVANCE AVIATION AAY ALLEGIANT AIR, INC. (FRESNO, CA) UNITED STATES ALLEGIANT AAZ AEOLUS AIR LIMITED GAMBIA AEOLUS ABA AERO-BETA GMBH & CO., STUTTGART GERMANY AEROBETA ABB AFRICAN BUSINESS AND TRANSPORTATIONS DEMOCRATIC REPUBLIC OF AFRICAN BUSINESS THE CONGO ABC ABC WORLD AIRWAYS GUIDE ABD AIR ATLANTA ICELANDIC ICELAND ATLANTA ABE ABAN AIR IRAN (ISLAMIC REPUBLIC ABAN OF) ABF SCANWINGS OY, FINLAND FINLAND SKYWINGS ABG ABAKAN-AVIA RUSSIAN FEDERATION ABAKAN-AVIA ABH HOKURIKU-KOUKUU CO., LTD JAPAN ABI ALBA-AIR AVIACION, S.L. -

Fact Finding Airports Southern Africa

2015 FACT FINDING SOUTHERN AFRICA Advancing your Aerospace and Airport Business FACT FINDING SOUTHERN AFRICA SUMMARY GENERAL Africa is home to seven of the world’s top 10 growing economies in 2015. According to UN estimates, the region’s GDP is expected to grow 30 percent in the next five years. And in the next 35 years, the continent will account for more than half of the world’s population growth. It is obvious that the potential in Africa is substantial. However, African economies are still to unlock their potential. The aviation sector in Africa faces restrictive air traffic regimes preventing the continent from using major economic benefits. Aviation is vital for the progress in Africa. It provides 6,9 million jobs and US$ 80 million in GDP with huge potential to increase. Many African governments have therefore, made infrastructure developments in general and airport related investments in particular as one of their priorities to facilitate future growth for their respective country and continent as a whole. Investment is underway across a number of African airports, as the region works to provide the necessary infrastructure to support the continent’s growth ambitions. South Africa is home to most of the airports handling 1+ million passengers in Southern Africa. According to international data 4 out of 8 of those airports are within South African Territory. TOP 10 AIRPORTS [2014] - AFRICA CITY JOHANNESBURG, SOUTH AFRICA 19 CAIRO, EGYPT 15 CAPE TOWN, SOUTH AFRICA 9 CASABLANCA, MOROCCO 8 LAGOS, NIGERIA 7,5 HURGHADA, EGYPT 7,2 ADDIS -

World Bank Document

ReportNo. 10667-ZA Zambia FinancialPerformance Public Disclosure Authorized of the Government-OwnedTransport Sector November1992 InfrastructureDivision MIC PCFICHE COPY SouthernAfrica Department F N. Type: (f Africa Region r i ti e: F INANCIAL FPF'RFOPMANCTE(F' THF CT FOR OFFICIAL USE ONLY Axt.': 3 B(: or2IJ11125 Dept.t :AFtN Ext. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Docunentof the World Bank Thisdocument has a restricteddistribution and may be used by recipients -onilyin theperformance of theirofficial duties. Its contents mnay not otherwise b!etisclosedwithout World Bank authorization. ZAMBIA CU ECEYOIVALENTS CurrencyUnit - ZambianKwacha ExchangeRates YM ~~~~~~~~~~~~~~~Kper US Do:lar 1987 8.9 1988 8.2 1989 12.9 1990 29.0 1991 50.0 1992(assumed average) 120.0 FISCAJ.YEARS Government:January 1 - December31 TransportEnterprises: April 1 - March31 ABBREVIATIONS AJAS - AfricanJoint Air Services BAU - Business-As-Usual BP - BritishPetroleum Ltd. CHL - ContractH-aulage Ltd CSO - CentralStatistical Office DC - DistrictCouncils DCA - Departmentof CivilAviation EEC - EuropeanEconomic Community ESCO - EngineeringServices Corporation Ltd IATA - InternationalAir TransportAssociation km - Kilometer MC&T - Ministryof Communicationsand Transport MH - MpulunguHarbor Corporation Ltd M-Roads - MainRoads MSD - MechanicalServices Department MT - MulungushiTraveller Ltd NACL - NationalAirports Corporation Ltd PSO - PuDlicService Obligation PTA - PreferentialTrade Area RD - RoadsDepartment SADCC - SouthAfrican -

Zambia's Ambassador to Germany, H.E. Anthony Mukwita Meets

Zambia’s ambassador to Germany, H.E. Anthony Mukwita meets German Chancellor Angela Merkel PUBLISHER Embassy of Zambia - Berlin Ambassador / Botshafter Anthony Mukwita EDITOR Kellys Kaunda First Secretary Press [email protected] CONTRIBUTORS Pictures of President obtained via State House Press Ofce headed by Special Assistant- Press and Public Relations taken by Eddie Mwanaleza, Salim Henry and Thomas Nsama. Extra write ups by Kellys Kaunda, Amos Chanda, Bernadette Deka, Chileshe Kandeta. MAKERTING/ADVERTISING Kellys Kaunda [email protected] The Diplomatic Dispatch is a quarterly magazine of the Embassy of Zambia in Berlin, Germany. The purpose of the publication is to promote the vast opportunities that exist in Zambia in various Zambia Berlin Embassy felds such as agriculture, mining and tourism to mention but a few. It is distributed to all govern- ment ministries in Zambia, all missions globally where Zambia is represented and all missions and Axel Springer Street sections of business associations and chambers of commerce in Germany. It is about the good 54a, Berlin, Germany story of Zambia known mostly for peace and stability as well as a tool for Economic Diplomacy. … the FOCAC Summit : What are the opportunities for Zambia? By Bernadette Deka - Executive director Policy Monitoring Research Center, PMRC he 3rd edition of the Forum for Africa – China Cooper- During the FOCAC summit, 8 new initiatives were an- ation (FOCAC) came to an end on 4th September nounced backed by a new US$60 billion support to Africa T 2018. We now refect on what has been deliberated for the next 3 years. These are: and more so, what Zambia has benefted. -

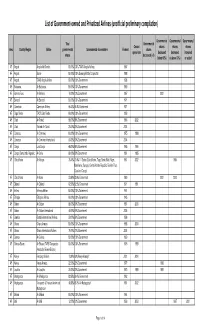

List of Government-Owned and Privatized Airlines (Unofficial Preliminary Compilation)

List of Government-owned and Privatized Airlines (unofficial preliminary compilation) Governmental Governmental Governmental Total Governmental Ceased shares shares shares Area Country/Region Airline governmental Governmental shareholders Formed shares operations decreased decreased increased shares decreased (=0) (below 50%) (=/above 50%) or added AF Angola Angola Air Charter 100.00% 100% TAAG Angola Airlines 1987 AF Angola Sonair 100.00% 100% Sonangol State Corporation 1998 AF Angola TAAG Angola Airlines 100.00% 100% Government 1938 AF Botswana Air Botswana 100.00% 100% Government 1969 AF Burkina Faso Air Burkina 10.00% 10% Government 1967 2001 AF Burundi Air Burundi 100.00% 100% Government 1971 AF Cameroon Cameroon Airlines 96.43% 96.4% Government 1971 AF Cape Verde TACV Cabo Verde 100.00% 100% Government 1958 AF Chad Air Tchad 98.00% 98% Government 1966 2002 AF Chad Toumai Air Tchad 25.00% 25% Government 2004 AF Comoros Air Comores 100.00% 100% Government 1975 1998 AF Comoros Air Comores International 60.00% 60% Government 2004 AF Congo Lina Congo 66.00% 66% Government 1965 1999 AF Congo, Democratic Republic Air Zaire 80.00% 80% Government 1961 1995 AF Cofôte d'Ivoire Air Afrique 70.40% 70.4% 11 States (Cote d'Ivoire, Togo, Benin, Mali, Niger, 1961 2002 1994 Mauritania, Senegal, Central African Republic, Burkino Faso, Chad and Congo) AF Côte d'Ivoire Air Ivoire 23.60% 23.6% Government 1960 2001 2000 AF Djibouti Air Djibouti 62.50% 62.5% Government 1971 1991 AF Eritrea Eritrean Airlines 100.00% 100% Government 1991 AF Ethiopia Ethiopian -

Ben Guttery Collection History of Aviation Collection African Airlines Box 1 ADC – Nigeria Aero Contractors Aeromaritime Aerom

Ben Guttery Collection History of Aviation Collection African Airlines Box 1 ADC – Nigeria Aero Contractors Aeromaritime Aeromas African Intl Air Afrique #1 Air Afrique #2 Air Algerie Air Atlas Air Austral Air Botswana Air Brousse Air Cameroon Air Cape Air Carriers Air Djibouti Air Centrafique Air Comores Air Congo Air Gabon Air Gambia Air Ivoire Air Kenya Aviation Airlink Air Lowveld Air Madagascar Air Mahe Air Malawi Air Mali Air Mauritanie Air Mauritius Air Namibia Box 2 Air Rhodesia Air Senegal Air Seychelles Air Tanzania Air Zaire Air Zimbabwe Aircraft Operating Co. Alliances Avex Avia Bechuanaland Natl. Bellview Bop Air Cameroon Airlines Campling Bros. Capital Air Caspair / Caspar Cata Catalina Safari Central African Airways Christowitz Clairways Command Airways Commercial Air Service Copperbelt Court Heli DAS – Dairo Desert Airways Deta DTA Angola East African Airways Corp Eastern Air Zambia Egypt Air Elders Colonial Box 3 Ethiopian Federal Airlines Sudan Flite Star Gambia Airways German Ghana Airways Guinea Hold – Trade Hunting Clan Imperial Inter Air International Air Kitale Zaire Katanga Kenya Airways Lam Lara Leopard Air Lana Lesotho Airways Liverian National Libyan Arab Magnum MISR Namib Air National Nigeria Airways North African Airlines (Tunisia) Phoenix Protea Pyramid RAC – Rhodesia Regie Malgache R.A.N.A Rhodesian Air Service Box 4 Rossair Royal Air Maroc Royal Swazi Ruac Sa Express Safair Safari Air Svcs Saide Sata Algeria SATT Scibe Shorouk Sierra Leone Airlines Skyways Sobelair South African Aerial Transport Somali Airlines -

20Th ANNIVERSARY of CENTRAL AFRICAN AIRWAYS (CAA) Issued 1St June 1966

20th ANNIVERSARY OF CENTRAL AFRICAN AIRWAYS (CAA) Issued 1st June 1966 The following is extracted from R. C. Smith’s book “Rhodesia - A Postal History” (pages 432 to 434) “To commemorate the twentieth anniversary of the formation of Central African Airways, the Ministry of Posts issued a set of four postage stamps on 1st June, 1966. The issue was printed by Mardon Printers (Pvt.) Ltd., by the offset litho process. The four values depicted three aircraft used by the Corporation during its service in Central Africa and one was a pure jet aircraft which was to be introduced in the future. In fact this aircraft should have been in service at the time the stamps were issued, but the British Government, in pursuance of its policy of retribution against Rhodesia, refused to allow the aircraft to be supplied. At the time the stamps were being printed negotiations with the British Government had reached a critical stage, and in order to avoid any embarrassment it was decided that the jet to be depicted on the 5s value be called 'Jet of the future' and not specifically named BAC1-11, which was the aircraft ordered. The other stamps were as follows: De Havilland Dragon Rapide (value 6d.). The first De Havilland Rapide was acquired by Rhodesia and Nyasaland Airways (the forerunner of Central African Airways) in 1935 and two years later three more were brought into service. The Rapide was an improved version of the earlier Dragon, and was a biplane powered by two 200 h.p. Gipsy VI engines. It had a cruising speed of 120 miles per hour, with a still range of 475 miles and could accommodate five passengers. -

Investigation Into Passenger Volumes and Financial Performance of the Low-Cost Carriers in the Southern African Development Community Region

Investigation into passenger volumes and financial performance of the low-cost carriers in the Southern African Development Community region Michael E. Mononga University of Westminster January 2020 A dissertation submitted to the University of Westminster in partial fulfilment of the requirements of the degree of Masters of Science, Air Transport Planning and Management Left blank i Abstract Since the emergence of the first low cost carrier (LCC) back in 2002 on the African continent in the South African Development Community (SADC) region, LCC activity has been moderate. Compared to LCC activity, from other parts of the world, such as Europe, North America and South East Asia, LCC activity has increased to the extent it the market has neared maturity and has made a huge impact to the passenger market. As for Africa, industry experts still consider that the air transport market is yet to experience further growth, as, as of 2017, Africa only represented 2.2% of the global market share according to a report on passenger demand and load factors by the International Air Transport Association (IATA). The main objective of this research is to investigate passenger volumes and financial performance of the LCCs in the Southern African Development Community region. The existing literature for the LCC market has resulted in limited knowledge about the impact to the passenger market for this specific business model at regional economic bloc level. Analysis of secondary data; passenger traffic volumes, seat capacity and load factors and airline case studies were conducted to identify growth in passenger volumes from 2000 to 2017, and financial performance of two airlines against industry global levels. -

The Journey of Ethiopian Airlines Arkebe Oqubay and Taffere Tesfachew HDI 2019 L VOLUME 2 L ISSUE 1

HDI 2019 l VOLUME 2 l ISSUE 1 The Journey of Ethiopian Airlines Arkebe Oqubay and Taffere Tesfachew HDI 2019 l VOLUME 2 l ISSUE 1 The Journey of Ethiopian Airlines Arkebe Oqubay 2 and Taffere Tesfachew 3 Abstract Despite sceptics who believed Ethiopia lacked the comparative advantage to adopt the latest aviation technologies, Ethiopian Airlines (EAL) has in the past seven decades narrowed the gap between itself and leading global players in the aviation industry by upgrading its technological, organizational, and management capabilities. This paper reviews EAL’s journey to build an internationally competitive airline, explores the challenges and complexities of learning for African firms, and examines implications for capability building and catch-up in late-latecomer countries. One key to EAL’s success was the partnership with a leading global player, TWA. Another was a strong commitment to “Ethiopianization” from an early stage, which increased learning intensity and highlighted the industry’s narrow latitude for poor performance. In the early 21st century, EAL embarked on Vision 2025, at the heart of which are technological capability development, skills formation, aggressive new market development, and commitment to Pan-Africanism. The story shows that African firms can successfully move closer to the productivity frontier in a particularly challenging industry. Keywords: Learning, capability building, catch-up, Ethiopia, aviation industry, intensity of learning This paper is a contribution to the How They Did It (HDI) series, a new line of publications from the Vice-Presidency for Economic Governance and Knowledge Management. As part of the African Development Bank’s strategy to help its regional member countries achieve the High-5 priorities, it aims to present interesting economic transformation experiences and discuss how some countries have addressed various development issues.