Western Europe Pay TV Operator Forecasts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Managing Real Options in Television Broadcasting

The Television Struggle: an Assessment of Over-the-Top Television Evolutions in a Cable Dominant Market (*) Bastiaan BACCARNE, Tom EVENS & Dimitri SCHUURMAN iMinds – MICT, Ghent University, Belgium Abstract: Traditional television screens have lost their monopoly on television content. With a helping hand of digitalization, the introduction of ever more screens in our lives and increasingly faster network technologies, a wide variety of alternative screens and sources of television content are trying to conquer a piece of the audiences' viewing time. This evolution calls for new kinds of services and has the potential to change the current television market. This paper assesses the evolution of over-the-top television services in Flanders, a cable dominant market in which several OTT TV services emerged during the past two years. By presenting an analysis of the market and the results of a large scale end-user survey (n: 1,269) we provide insights on the future of OTT TV and its impact on the current television ecosystem. In the Flemish market, both traditional broadcasters, the channels themselves and new market entrants are launching OTT TV services. These market evolutions are being related to user expectations and usage patterns in order to assess the challenges for future television. This also allows to make assumptions on future scenarios regarding so-called "cord- cutting" behaviour. Because of the high adoption of triple play bundles and fierce competition between the two dominant television distributors, a large scale video cord-cutting scenario is highly unlikely for the Flemish television market. Although OTT TV might gain importance, it will be hard for 'OTT TV- only' services to replace the traditional television distributors. -

TV Channel Distribution in Europe: Table of Contents

TV Channel Distribution in Europe: Table of Contents This report covers 238 international channels/networks across 152 major operators in 34 EMEA countries. From the total, 67 channels (28%) transmit in high definition (HD). The report shows the reader which international channels are carried by which operator – and which tier or package the channel appears on. The report allows for easy comparison between operators, revealing the gaps and showing the different tiers on different operators that a channel appears on. Published in September 2012, this 168-page electronically-delivered report comes in two parts: A 128-page PDF giving an executive summary, comparison tables and country-by-country detail. A 40-page excel workbook allowing you to manipulate the data between countries and by channel. Countries and operators covered: Country Operator Albania Digitalb DTT; Digitalb Satellite; Tring TV DTT; Tring TV Satellite Austria A1/Telekom Austria; Austriasat; Liwest; Salzburg; UPC; Sky Belgium Belgacom; Numericable; Telenet; VOO; Telesat; TV Vlaanderen Bulgaria Blizoo; Bulsatcom; Satellite BG; Vivacom Croatia Bnet Cable; Bnet Satellite Total TV; Digi TV; Max TV/T-HT Czech Rep CS Link; Digi TV; freeSAT (formerly UPC Direct); O2; Skylink; UPC Cable Denmark Boxer; Canal Digital; Stofa; TDC; Viasat; You See Estonia Elion nutitv; Starman; ZUUMtv; Viasat Finland Canal Digital; DNA Welho; Elisa; Plus TV; Sonera; Viasat Satellite France Bouygues Telecom; CanalSat; Numericable; Orange DSL & fiber; SFR; TNT Sat Germany Deutsche Telekom; HD+; Kabel -

Swisscom Sustainability Report 2018

Sustainability Report 2018 Annual Report publications Annual Report 2018 Sustainability Report 2018 2018 at a glance The Annual Report, Sustainability Report and 2018 at a glance together make up Swisscom’s reporting on 2018. The three publications are available online at: swisscom.ch/report2018 “Inspiring people” concept The networked world offers countless opportunities that we canbegin to shape today. Top quality, groundbreaking innovation, deep-rooted commitment – we feel lucky to be able to inspire people and to lead them to embrace the opportunities that a networked future offers. The images used in our reporting show how and where we inspired people in 2018: from high in the Alps to people’s homes, in business and in our Swisscom Shops. A big thank-you to all who took the time to pose for these photographs: Pius and Jeanette Jöhl with their kids at the Oberchäseren alp, a houseshare with friends in Zurich (Seraina Cadonau, Anna Spiess, Linard Baer and Johannes Schutz), Ypsomed AG in Burgdorf, Stefan Mauron, our customer Jeannette Furter, and the entire crew at House of Swisscom in Basel. Corporate Responsibility Fulfilling the expectations of our stakeholder groups in a responsible manner. Introduction Stakeholders’ letter ............................................4 Sustainable environment ......................................5 Material issues ...............................................11 Corporate Priorities and objectives up until 2020 .........................13 Responsibility strategy Priorities and objectives up until -

Mobile Data Consumption Continues to Grow – a Majority of Operators Now Rewarded with ARPU

Industry analysis #3 2019 Mobile data – first half 2019 Mobile data consumption continues to grow – a majority of operators now rewarded with ARPU Taiwan: Unlimited is so last year – Korea: 5G boosts usage Tefficient’s 24th public analysis on the development and drivers of mobile data ranks 115 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in the first half of 2019. tefficient AB www.tefficient.com 5 September 2019 1 The data usage per SIM grew for all; everybody climbed our Christmas tree. More than half of the operators could turn that data usage growth into ARPU growth – for the first time a majority is in green. Read on to see who delivered on “more for more” – and who didn’t. Speaking of which, we take a closer look at the development of one of the unlimited powerhouses – Taiwan. Are people getting tired of mobile data? We also provide insight into South Korea – the world’s leading 5G market. Just how much effect did 5G have on the data usage? tefficient AB www.tefficient.com 5 September 2019 2 Fifteen operators now above 10 GB per SIM per month Figure 1 shows the average mobile data usage for 115 reporting or reported1 mobile operators globally with values for the first half of 2019 or for the full year of 2018. DNA, FI 3, AT Zain, KW Elisa, FI LMT, LV Taiwan Mobile, TW 1) FarEasTone, TW 1) Zain, BH Zain, SA Chunghwa, TW 1) *Telia, FI Jio, IN Nova, IS **Maxis, MY Tele2, LV 3, DK Celcom, MY **Digi, MY **LG Uplus, KR 1) Telenor, SE Zain, JO 3, SE Telia, DK China Unicom, CN (handset) Bite, -

Results and Presentations

March 18, 2014 Full Year 2013 Results 1 An International Cable Operator in Attractive Markets 9 Territories Belgium Luxembourg 14m Homes Passed Western Europe Switzerland France 3m Cable Customers Portugal 6.6m Cable RGUs Israel Dominican Republic Guadeloupe & Overseas Martinique Territories French Guiana Mayotte La Réunion Note: figures above include Orange Dominicana and Tricom 2 Altice SA Full Year Results - Highlights Financials Recent Strategic Initiatives Liquidity & Capital Full-year pro forma1 revenue up 0.7% Successful IPO creates equity IPO raised c€750m primary proceeds to €3.2bn currency for future opportunities & created 26% free float • mainly driven by Israel & France, partially offset by Portugal and Increased Numericable stake to 40% Altice SA consolidated net debt of ODO €6,255bn Closed Tricom acquisition in Full-year pro forma EBITDA up 6.0% Dominican Republic; Orange to follow Altice VII net debt of €3,509bn to €1.36bn €384m consolidated cash and • Mainly driven by Israel & Portugal undrawn revolvers of €163m Full-year proforma OpFCF2 up 27% to €667m Triple-play penetration up 5% pts to 61% Notes: 1 These results reflect the pro forma results of the Altice S.A. group, including the planned acquisition of Orange Dominicana, but excluding Tricom and Mobius. 2 Defined here and throughout presentation as EBITDA - Capex 3 Altice S.A Key Operational Highlights Israel France Reorganization program finished 5% cable customer growth 3.6% ARPU growth driven by strong triple-play and high 2% ARPU growth speed -

Mediaconcentratie in Vlaanderen

MMediaconcentratieediaconcentratie iinn VVlaanderenlaanderen rapport 2009 VLAAMSE REGULATOR VOOR DE MEDIA Koning Albert II-laan 20,bus 21 1000 Brussel COLOFON Samenstelling, redactie en eindredactie: Stijn Bruyneel, Ingrid Kools en Francis Soulliaert Verantwoordelijke uitgever: Joris Sels, gedelegeerd bestuurder Koning Albert II-laan 20, bus 21 1000 Brussel Tel.: 02/553 45 04 Fax: 02/553 45 06 e-mail:[email protected] website: www.vlaamseregulatormedia.be Lay-out en druk: Digitale drukkerij Facilitair Management Vlaamse Overheid Depotnummer: D/2009/3241/429 Mediaconcentratie in Vlaanderen INHOUDSTAFEL Samenvatting ......................................................................................................................... 10 1 DE VLAAMSE MEDIASECTOR ............................................................................................... 13 1.1 RADIO ......................................................................................................................... 17 1.1.1 Contentleveranciers ........................................................................................................................ 17 1.1.2 Radio-omroeporganisaties ............................................................................................................. 18 1.1.2.1 Landelijke publieke radio-omroeporganisaties ........................................................ 18 1.1.2.2 Regionale publieke radio-omroeporganisaties ......................................................... 19 1.1.2.3 Wereldomroep .............................................................................................................. -

Results from the Third Quarterly

Euskaltel – Third Quarter 2015 Results 28 October 2015 Executive summary (i/iv) 241 247 118 173 Main figures for the business for the periods ended September 30th, 2015 and 2014 28 119 Key financials for the 9-month period ended September 30th, 2015 and 2014 177 132 177 143 177 159 3Q15 adjusted vs 0 41 3Q15 3Q15 Adjusted (**) 3Q14 3Q14 % 3Q14 102 184 Total Revenue 244.4 244.4 239.0 5.4 2.3% 153 255 Residential 151.5 151.5 146.1 5.4 3.7% 123 178 151 199 Business 69.0 69.0 70.4 (1.4) -2.0% 73 139 Wholesale & Other 17.3 17.3 17.3 0.0 0.1% 194 218 Others (*) 6.6 6.6 5.2 1.4 27.3% 172 205 141 187 Ebitda 103.9 116.7 112.3 4.4 3.9% 206 Ebitda Margin 42.5% 47.7% 47.0% 0.8 pp 52 OpFCF 75.3 88.1 86.3 1.8 2.0% 3 conversion rate 72.5% 75.5% 76.9% -1.4 pp Net Income (3.3) 36.0 25.6 10.4 40.7% Net Financial Debt 449.8 266.6 183.2 68.7% Net Debt / Ebitda 2.8x 1.7x 1.1x (*) Profit neutral operations (**) Excluded costs related to the IPO process, debt cancellation and the acquisition of R Cable. 1 Executive summary (ii/iv) Business: Inflexion point in revenue 241 247 118 173 28 119 • Total revenue for the period ended September 30th, 2015, have been €244.4mn vs €239.0mn, +€5.4mn (+2.3% YoY). -

THE E-HEALTH OPPORTUNITY for the TELECOMMUNICATION INDUSTRY and PORTUGAL TELECOM – a CASE STUDY Cover

THE E-HEALTH OPPORTUNITY FOR THE TELECOMMUNICATION INDUSTRY AND PORTUGAL TELECOM – A CASE STUDY Cover Francisco Borges d’Almeida Nascimento Master of Science in Business Administration Orientador: Prof. Jorge Lengler, ISCTE Business School, Departamento de Marketing, Operações e Gestão Geral April 2015 THE E-HEALTH OPPORTUNITY FOR THE TELECOMMUNICATION INDUSTRY AND PORTUGAL TELECOM – A CASE STUDY Francisco Borges d’Almeida Nascimento Case Study – E-Health in the telecommunication industry and at PT Abstract Electronic-Health (e-health) is a recent answer to some pressing challenges on health. Aging of western societies and treatments’ rising costs raised doubts about health systems’ sustainability. Individuals, companies and public administration alike are looking for technology to find aid in addressing these challenges. Several industries are tacking those issues offering innovative solutions among which Telecommunication’s. Nonetheless, this industry is facing challenges from over- the-top players menacing its business model. Portugal Telecom shares these challenges and is looking to diversify to guarantee future growth, namely, by developing in e-health solutions. This case study follows two important threads in strategy literature: diversification and the resource-based view, applied Portugal Telecom and the e-health opportunity. As a case study, it aims providing readers a tool to better understand and employ strategic management concepts and frameworks in an applied business context. E-health as an opportunity for growth to Telecommunication companies and Portugal Telecom is described from three points of view: i) an actual market need ii) that may be addressed by Telecommunication companies and iii) should be addressed by those companies as they need to grow. -

Global Pay TV Operator Forecasts

Global Pay TV Operator Forecasts Table of Contents Published in October 2016, this 190-page electronically-delivered report comes in two parts: A 190-page PDF giving a global executive summary and forecasts. An excel workbook giving comparison tables and country-by-country forecasts in detail for 400 operators with 585 platforms [125 digital cable, 112 analog cable, 208 satellite, 109 IPTV and 31 DTT] across 100 territories for every year from 2010 to 2021. Forecasts (2010-2021) contain the following detail for each country: By country: TV households Digital cable subs Analog cable subs Pay IPTV subscribers Pay digital satellite TV subs Pay DTT homes Total pay TV subscribers Pay TV revenues By operator (and by platform by operator): Pay TV subscribers Share of pay TV subscribers by operator Subscription & VOD revenues Share of pay TV revenues by operator ARPU Countries and operators covered: Country No of ops Operators Algeria 4 beIN, OSN, ART, Algerie Telecom Angola 5 ZAP TV, DStv, Canal Plus, Angola Telecom, TV Cabo Argentina 3 Cablevision; Supercanal; DirecTV Australia 1 Foxtel Austria 3 Telekom Austria; UPC; Sky Bahrain 4 beIN, OSN, ART, Batelco Belarus 2 MTIS, Zala Belgium 5 Belgacom; Numericable; Telenet; VOO; Telesat/TV Vlaanderen Bolivia 3 DirecTV, Tigo, Entel Bosnia 3 Telemach, M:Tel; Total TV Brazil 5 Claro; GVT; Vivo; Sky; Oi Bulgaria 5 Blizoo, Bulsatcom, Vivacom, M:Tel, Mobitel Canada 9 Rogers Cable; Videotron; Cogeco; Shaw Communications; Shaw Direct; Bell TV; Telus TV; MTS; Max TV Chile 6 VTR; Telefonica; Claro; DirecTV; -

Providence Equity Partners to Acquire a Majority Stake in the Dutch and Flemish Satellite TV Providers Canaldigitaal and TV Vlaanderen

PRESS RELEASE Providence Equity Partners to Acquire a Majority Stake in the Dutch and Flemish Satellite TV Providers CanalDigitaal and TV Vlaanderen Hilversum, February 22, 2007 -- CanalDigitaal and TV Vlaanderen, the Dutch and Flemish DTH satellite TV operators, announced today that Providence Equity Partners will acquire a majority stake in the companies. Airbridge Investments, currently the 100% owner of the companies, will co- invest alongside Providence and will hold the remaining shares together with management. The executive management team will remain unchanged. CanalDigitaal will continue its expansion in the Dutch market for TV distribution, and the start up TV Vlaanderen will continue its very successful rollout in the Flemish market. The transaction is subject to the approval of the Netherlands Competition Authority (NMa). “CanalDigitaal and TV Vlaanderen are exceptionally well positioned to drive and benefit from the expansion of satellite television in the Netherlands and Belgium,” said Jörg Mohaupt, a Managing Director of Providence Equity Partners. “The management team has a tremendous understanding of the rapidly evolving digital television marketplace in the Netherlands and Belgium and are focusing these companies on meeting the increasing demand for digital media services there. We look forward to partnering with them to support the growth of these companies.” Hans Wolfert, Partner of Airbridge Investments and Chairman of CanalDigitaal, said “This agreement marks a new phase in Dutch and Flemish DTH satellite TV distribution. Particularly in the Netherlands watching TV via satellite has rapidly matured, with a market share of over 9% already. With Providence, the largest investor in this field, we will have various benefits and are well prepared for the next phase, which includes challenges such as the successful introduction of HDTV and expansion where possible. -

Vodafone Revolutionises Roaming Rules

VODAFONE REVOLUTIONISES ROAMING RULES VODAFONE ALLOWS CUSTOMERS TO MAKE OVERSEAS CALLS AT DOMESTIC RATES Milan, May 17, 2005 – The Vodafone Group is about to revolutionise roaming prices, responding to customers’ demands for greater transparency and clarity when making or receiving calls whilst abroad. June 1 is to see the launch of Vodafone Passport, the first price plan forming part of the Group’s new Vodafone Travel Promise package. Vodafone Passport enables Vodafone customers who access the Group’s networks to make calls at domestic rates, paying just € 1.00 at the start of each call. The new offering provides Vodafone customers with greater transparency, giving better value for money and eliminating any doubts about cost effectiveness. When overseas Vodafone customers will thus be able to: • Call Italy: at the same prices charged for domestic calls, paying an additional €1.00 per call. • Receive calls: talking free of charge having paid a connection fee of just €1.00. “The nature of the Vodafone Group enables us to offer a veritable revolution in roaming services,” claimed Pietro Guindani, CEO of Vodafone Italia. “Vodafone Passport will make the customer feel at home in any country with a Vodafone network.” The new service will be available in Germany, Greece, Italy, the Netherlands, Spain, Sweden, Fiji and Japan from June 1. Hungary, Malta, Portugal, Ireland, the UK, Albania, Australia and New Zealand will introduce the price plan during the summer. Customers who use the SFR (France), Swisscom (Switzerland) and Proximus (Belgium) networks will also subsequently gain access. Vodafone Passport is the latest innovation created by the Vodafone Group with the aim of making it easier to make mobile calls when abroad and thus increase the use of roaming services. -

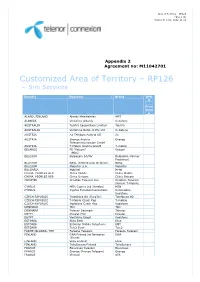

Customized Area of Territory – RP126 – Sim Services

Area of Territory – RP126 Page 1 (3) Version D rel01, 2012-11-21 Appendix 2 Agreement no: M11042701 Customized Area of Territory – RP126 – Sim Services Country Operator Brand GPR S Price Grou p ALAND, FINLAND Alands Mobiltelefon AMT ALBANIA Vodafone Albania Vodafone AUSTRALIA Telstra Corporation Limited Telstra AUSTRALIA Vodafone Network Pty Ltd Vodafone AUSTRIA A1 Telekom Austria AG A1 AUSTRIA Orange Austria Orange Telecommunication GmbH AUSTRIA T-Mobile Austria GmbH T-mobile BELARUS FE “Velcom” Velcom (MDC) BELGIUM Belgacom SA/NV Belgacom (former Proximus) BELGIUM BASE (KPN Orange Belgium) BASE BELGIUM Mobistar S.A. Mobistar BULGARIA Mobiltel M-tel CHINA, PEOPLES REP. China Mobile China Mobile CHINA, PEOPLES REP. China Unicom China Unicom CROATIA Croatian Telecom Inc. Croatian Telecom (former T-Mobile) CYPRUS MTN Cyprus Ltd (Areeba) MTN CYPRUS Cyprus Telecommunications Cytamobile- Vodafone CZECH REPUBLIC Telefónica O2 (EuroTel) Telefónica O2 CZECH REPUBLIC T-Mobile Czech Rep T-mobile CZECH REPUBLIC Vodafone Czech Rep Vodafone DENMARK TDC TDC DENMARK Telenor Denmark Telenor EGYPT Etisalat Misr Etisalat EGYPT Vodafone Egypt Vodafone ESTONIA Elisa Eesti Elisa ESTONIA Estonian Mobile Telephone EMT ESTONIA Tele2 Eesti Tele2 FAROE ISLANDS, THE Faroese Telecom Faroese Telecom FINLAND DNA Finland (fd Networks DNA (Finnet) FINLAND Elisa Finland Elisa FINLAND TeliaSonera Finland TeliaSonera FRANCE Bouygues Telecom Bouygues FRANCE Orange (France Telecom) Orange FRANCE Vivendi SFR Area of Territory – RP126 Page 2 (3) Version D rel01, 2012-11-21 GERMANY E-Plus Mobilfunk E-plus GERMANY Telefonica O2 Germany O2 GERMANY Telekom Deutschland GmbH Telekom (former T-mobile) Deutschland GERMANY Vodafone D2 Vodafone GREECE Vodafone Greece (Panafon) Vodafone GREECE Wind Hellas Wind Telecommunications HUNGARY Pannon GSM Távközlési Pannon HUNGARY Vodafone Hungary Ltd.