Isle of Wight Council Retail Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Planning and Infrastructure Services

PLANNING AND INFRASTRUCTURE SERVICES The following planning applications and appeals have been submitted to the Isle of Wight Council and can be viewed online https://www.iow.gov.uk/Residents/Environment-Planning-and-Waste/Planning/Planning-Development/Applic ation-search-view-and-comment using the link labelled ‘planning register’. Comments on the applications must be received within 21 days from the date of this press list, and comments for agricultural prior notification applications must be received within 7 days to ensure they be taken into account within the officer report. Comments on planning appeals must be received by the Planning Inspectorate within 5 weeks of the appeal start date (or 6 weeks in the case of an Enforcement Notice appeal). Details of how to comment on an appeal can be found (under the relevant LPA reference number) at https://www.iow.gov.uk/Residents/Environment-Planning-and-Waste/Planning/Planning-Development/Applic ation-search-view-and-comment For householder, advertisement consent or minor commercial (shop) applications, in the event of an appeal against a refusal of planning permission, representations made about the application will be sent to Planning Inspectorate, and there will be no further opportunity to comment at appeal stage. Should you wish to withdraw a representation made during such an application, it will be necessary to do so in writing within 4 weeks of the start of an appeal. All written representations relating to applications will be made available to view online. PLEASE NOTE THAT APPLICATIONS -

Isle of Wight Walking Festival Walks Directory 2019

SPONSORED BY: Walks Directory 2019 For further information on each walk and to book, please visit isleofwightwalkingfestival.co.uk The Shepherd’s Trail Saturday 4 May This substantial walk follows the way-marked recreational path from Carisbrooke to Shepherd’s Chine where we’ll stop for a picnic lunch, before returning via Showell and Chillerton Down. Ventnor Geowalk Start time: 0900 Start location: Car Park opposite Carisbrooke Priory (Central A guided landscape walk by Dinosaur Isle to explore Ventnor towns geology, Wight) Distance: 16 miles Duration: 6.5 hours landscape, sea-defences, ground movement, building stone and fossils. Start time: 1000 Start location: Dudley Road Car Park, Ventnor (South Wight) Distance: 2 miles Duration: 2.5 hours Seaside Story Walk Sunday 5 May A family seaside story walk with Sue Bailey. Plenty of stops for stories and to find beach treasure. Find out why the crab has no head, or why the sea is salty. Wear suitable beach shoes! Isle of Wight Challenge (2nd half) Start time: 0930 Start location: Outside the Watersedge cafe, Gurnard seafront From Cowes to Chale: travelling clockwise along the beautiful coastline of the Isle (North Wight) Distance: 1 miles Duration: 1.5 hours of Wight. This fully supported charity challenge is a true test of determination and stamina. Isle of Wight Challenge (full) Please note: to register for this walk go to www.isleofwightchallenge.com An around the Island walk with rest stops every 8 miles or so to help you complete Start time: 0700 Start location: Chale Recreation Ground (South Wight) your challenge. The full challenge is 106km of spectacular coastlines, dramatic cliffs Distance: 33.5 miles Duration: 16 hours max. -

Temporary Train Times 7-24 August 2017 Monday To

ISLAND LINE TRAINS Isle of Wight 24 to London Waterloo TEMPORARY TRAIN TIMES 7-24 AUGUST 2017 MONDAY TO FRIDAY ONLY London Waterloo Woking (for Heathrow Airport) Guildford Haslemere Petersfield Portsmouth & Southsea Portsmouth Harbour Southsea Hoverport Ryde Pier Head Ryde Esplanade Ryde St Johns Road Smallbrook Junction (for IOW Steam Railway) Brading Sandown Lake Shanklin Ventnor Pocket 24.indd 1 26/05/2017 10:58:31 What’s happening? From 5 to 28 August inclusive, major engineering works will be taking place at London Waterloo. This is to allow work to start to extend platforms for longer trains and provide more space for more passengers. Throughout this time, fewer trains will be running across the South West Trains network. Some stations will see very significant reductions in the frequency of their train services and a small number will be closed for some or all of this time. Stations in or around London, such as London Waterloo, Clapham Junction, Vauxhall and Wimbledon are expected to be exceptionally busy during this time. We strongly advise passengers to avoid travelling during the busiest morning and evening periods if possible. Woking is expected to be extremely busy and you are advised not to change on to fast services here. Across the network, we urge passengers to leave plenty of time for their journey, plan ahead and understand the impact these temporary changes will have. Detailed travel advice, including ticket acceptance options, is available at southwesttrains.co.uk/wswupgrade August Bank Holiday Friday 25 August to Monday 28 August 2017 On Friday 25 August to Monday 28 August 2017, there will be additional works at London Waterloo. -

The Ramblers' Association

Portsmouth Group Summer - Autumn (July – October 2017) Walks Programme The Ramblers' Association Working for Walkers The RA promotes rambling, protects Rights of Way, campaigns for access to open country and defends the beauty of the countryside Web site: Head office www.ramblers.org.uk Local http://www.portsmouthramblers.org.uk/ E-mail Email: Head office [email protected] Local [email protected] PORTSMOUTH GROUP WALKING PROGRAMME Correct as at 31st May 2017. Check the website for any updates. The Portsmouth Group offers a variety of walks mainly in Hampshire, West Sussex and the Isle of Wight. On Saturdays these are moderately paced 5 to 9 mile walks whilst, on Sundays, they are faster paced 11 to 15 mile walks. The Group also has short Friday evening walks and some extra Saturday walks in more distant parts in the summer months. Most walks have a pub/cafe stop either at the end or at lunch time. INFORMATION FOR WALKERS New walkers always welcome. Just turn up at meeting place for shorter walks. For walks in excess of 10 miles, please contact leader first if you have not previously walked this distance. Grade A walks – for experienced walkers; brisk pace Grade B walks – regular pace Grade C walks – moderate pace Grade D walks – slow pace These are only general indications of the pace and will vary with the individual. All walks are circular unless otherwise stated. Wear stout footwear and carry waterproof clothing for possible wet weather. There will be stops for coffee and lunch, so please bring a flask and food. -

Minutes – Meeting 46 Brading Station Thursday 4 December 2014

Minutes – Meeting 46 Brading Station Thursday 4 December 2014 Present at the meeting: Forum Members: Mark Earp (Chairman) David Farnham Cllr Paul Fuller Cllr John Medland Cllr John Hobart Tricia Merrifield Stephen Darch Alec Lawson Penny Edwards Helen Wood Others: David Howarth Peter Fellows Tony Ridd David Marsh Belinda Walters - CLA Keith Ballard - RSPB Will Ainslie - LSTF Project Manager, Isle of Wight Council Darrel Clarke - IWC Public Rights of Way Manager (PROW) Forum Secretary: Jennine Gardiner -Rights of Way Assistant, IWC Public Rights of Way Section (PROW) 1. Apologies: Apologies were received from: Lee Matthews - IWC Recreation & Public Spaces Manager Fiona Ellis - AONB Officer Isle of Wight Council Marcus Stroud – Forestry Commission Heather Whetter – Natural England John Gurney-Champion John Heather 2. Minutes of previous meeting and matters arising: The minutes were approved as a true record of the last meeting. Matters arising from last minutes: Shanklin to Wroxall –Penny & Tricia to assess suitability for carriages – still being investigated. East Cowes / Whippingham – Tricia - permissive bridleways – no update. 3. Any Declarations of Interest: Mark Earp – IW Coastal Path & Lost Ways Project Cllr Fuller – IW Coastal Path support from his constituency 4. Brading Station Members and guests had a walk around Brading Station looking at the level crossings where the Rights of Way cross the track and the public access around the station and to the RSPB reserve / Brading marshes. Discussions took place regarding the possibility of alternative ways of crossing the track i.e the cattle creep (tunnel). Contributions to the discussion were made by Mark Earp, Darrel Clarke, Peter Fellows and Keith Ballard. -

S P a N F a R M Span Lane, Wroxall, Isle of Wight PO38 3AU RURAL CONSULTANCY | SALES | LETTINGS | DESIGN & PLANNING S P a N F a R M Wroxall, Isle of Wight

S P A N F A R M Span Lane, Wroxall, Isle of Wight PO38 3AU RURAL CONSULTANCY | SALES | LETTINGS | DESIGN & PLANNING S P A N F A R M Wroxall, Isle of Wight Farmhouse, holiday cottages, farm buildings and 9.67 acres (3.91 hectares) of land including a pond and woodland Situated within the Rew Valley, in the south of the Isle of Wight with far reaching views to the Downs. THE FARMHOUSE Kitchen/Breakfast Room with separate Utility Room and Store • Living Room• Sitting Room • Conservatory • Master bedroom with en-suite bathroom • Further two double bedrooms with en-suite • Single bedroom • Family bathroom • Further two bedrooms and bathroom on second floor • Gardens • Private driveway HOLIDAY COTTAGES Three holiday cottages: Shepherds Cottage, Well Cottage and Garden Cottage OUTBUILDINGS An extensive range of modern and traditional farm buildings LAND 9.67 acres (3.91 hectares) of land and woodland with a pond. A further approximately 170 acres (68.8 hectares) of land, woodland and farm buildings are available separately. For sale by private treaty. Southampton 1 hour by ferry | Portsmouth 45 minutes by ferry Southampton 25 minutes by foot | Portsmouth Harbour 22 minutes by foot | Southsea 10 minutes by hovercraft Trains to London Waterloo in 1 hour 36 minutes from Portsmouth Harbour and 1 hour 19 minutes from Southampton RURAL CONSULTANCY | SALES | LETTINGS | DE SIGN & PLANNING SITUATION Span Farm is located in the south of the Isle of Wight, just outside the village of Wroxall. Whilst rural in position and outlook, Span Farm is minutes away from the seaside towns of Ventnor and Shanklin, providing many shops and restaurants. -

The Winter of 1962 – 1963

THE WINTER OF 1962 – 1963 By Dave Bambrough 2009 December 1962 was heralded as the sunniest December since records began in 1914, with a total of 109.8 hours of sunshine recorded. This total exceeded the previous record of 92 hours established in December 1946. However, in the last five days of the month the sun disappeared and winter dawned on the unsuspecting local landscape. An early warning sign was the –5º-Celsius on Boxing Day and a light snow shower, a prerequisite for the warm clothes and coal fires that would soon be required. On Saturday 29 th December 1962 at about 7.30 p.m. several members of the Sandown Tap public house dart team journeyed to the Plough & Barleycorn public house, Shanklin, to support their house champion, who was representing the Tap in the first round of the News of the World National Dart competition. Despite the Tap man losing, it had been a very convivial evening at The Plough, and whilst everyone was aware that snow was falling during the evening’s entertainment, none of the participants realised just how much was falling. Not many young men between the ages of 18 and 23 had their own transport in those days, the odd luxury and a couple of nights out very quickly used up any excess money left over, once the board and keep contributions had been distributed. The cost of a motorbike was sustainable, and many youths of this age had them, the cost of a car however wasn’t, to most, therefore the bus was the most popular form of transport. -

Town Centre Health Check Study

Isle of Wight Council Town Centres Health Check Study Final Report October 2009 Isle of Wight Town Centre Health Check Study Isle of Wight Town Centre Health Check Study Contents 1 Executive Summary 1 2 INTRODUCTION 3 2.1 The Study 3 2.2 The Importance of Town Centres 3 2.3 The Retail Hierarchy 4 3 BASELINE ASSESSMENT 7 3.1 Introduction 7 3.2 Socio-Economic Profile 7 3.3 Tourism and Leisure 10 3.4 Emerging Baseline Issues 11 4 Policy Review 12 4.1 Introduction 12 4.2 PPS 6: Planning for Town Centres 12 4.3 Draft Planning Policy Statement 4 12 4.4 Regional and Local Policy 13 4.5 Local Transport Strategy 17 4.6 Supplementary Planning Guidance 18 5 Town Centre Health Check Assessment 19 5.1 Introduction 19 5.2 Methodology 19 5.3 Summary Findings 20 5.4 Cowes 23 5.5 East Cowes 32 5.6 Freshwater 39 5.7 Newport 46 5.8 Ryde 62 5.9 Sandown 73 5.10 Shanklin 80 5.11 Ventnor 87 6 SWOT ANALYSIS 94 6.1 Introduction 94 6.2 Consultation 94 6.3 Emerging Priorities 103 7 RECOMMENDATIONS & CONCLUSIONS 106 7.1 Conclusions 106 7.2 Recommendations 106 Isle of Wight Town Centre Health Check Study Isle of Wight Town Centre Health Check Study 1 Executive Summary 1.1.1 The most fundamental challenge for the Isle of Wight is sustaining its economy. In the last decade, visitor numbers to the Island have fluctuated considerably which should be of paramount concern for an economy that depends heavily on this sector. -

Historic Environment Action Plan Newchurch Environs and Sandown Bay

Directorate of Community Services Director Sarah Mitchell Historic Environment Action Plan Newchurch Environs and Sandown Bay Isle of Wight County Archaeology and Historic Environment Service October 2008 01983 823810 archaeology @iow.gov.uk Iwight.com HEAP for Newchurch Environs and Sandown Bay INTRODUCTION This HEAP Area has been defined on the basis of geology, topography, land use and settlement patterns which differentiate it from other HEAP Areas. The Area is characterised by its varied topography and mix of HEAP Types. Field patterns, valley floor types, settlement types and woodland types are all significant. However, a significant part of this Area is occupied by the towns of Sandown and Shanklin. The HEAP for this Area identifies the most important forces for change, and considers key management issues. Actions particularly relevant to this Area are identified from those listed in the Isle of Wight HEAP Aims, Objectives and Actions. ANALYSIS AND ASSESSMENT Location, Geology and Topography • Situated south of East Wight Chalk Ridge and east of Arreton Valley , extending from Newchurch to Sandown Bay. • Geology is mainly Ferruginous Sands overlain with patches of Plateau Gravel. Alluvium and Gravel Terraces in the river valleys. • Generally hillier and of higher altitude than adjacent Arreton Valley , rising to a maximum of 60m OD in various places and to 76m OD near Apsecastle Wood on southern edge of area, but also including low-lying land around the River Yar and Scotchells Brook. • Eastern Yar flows east through this area between Newchurch and Brading. Scotchells Brook flows NE from Apse Manor to join Yar east of Alverstone. -

Shanklin Historic Pub Walk

Shanklin Historic Pub Walk IW Branch CAMRA An historic walk around Shanklin, the route reveals the changing history of the settlement from a small fishing village to a major sea resort town and its continued development and popularity in the face of globalism; Shanklin still maintains its charm and character. Contents An Introduction to Shanklin Welcome to Shanklin, a seaside resort town, made famous by its chine, charm and water of both spring and sea. Establishment of the Current Village It was not until the early 1800s that the small coastal fishing village that was Shanklin started to draw attraction and develop as a seaside holiday destination from such luminaries as Keats. The transformation occurred relatively quickly, with the Chine becoming the first paying tourist attraction on the Island in 1817 and the Crab, Holliers and Daishes being in establishment by 1833, then increased at an even faster pace with the arrival of Queen Victoria at Obsorne in 1845. So, the revenue from smuggling activities changed to tourism and the cliff to Customs patrol paths became scenic caminaries for the visitors, now arriving by train after the opening of the line in 1864. Noted for its pure spring water, sea air and pleasant scenery, Shanklin’s heyday was in the early 1900s, and, maybe the now disappeared, after a WWII bombing raid, Royal Spa Hotel, on the Esplanade, may have marked the height of its climb, being resort of European Royals. Shanklin Pier The Shanklin Esplanade & Pier Co. was formed in the 1870s and work began in August 1888 to the plans of F.C.Dixon and M.N.Ridley. -

25 to 28 October 2013

The UK’s biggest walking festival! 25 TO 28 OCTOBER 2013 www.isleofwightwalkingfestival.co.uk Exodus Travels are the proud sponsors of this year’s festival. They specialise in small group and family walking holidays with over 150 treks across the globe. Key to symbols Dogs on leads Walk pace welcome Leisurely Gentle Suitable for pushchairs Moderate Brisk Packed lunch Walk difficulty advised Easy: Mainly flat walking, on paths with good Refreshments surfaces. No stiles, no (or few) steps. available Fairly easy: Gentle rolling landscape, walking Bring binoculars on paths with average to good surfaces. Some walking on gentle inclines, some stiles or steps to be expected en route. Wear sturdy Moderate: Varying landscape with more shoes challenging slopes. Stiles and steps to be expected Family en route. Suitable for keen walkers and anyone who is reasonably active. friendly Fairly strenuous: A challenging walk for fit Coastal scenery walkers with some experience. Steep gradients, stiles and steps and uneven surfaces to be expected. Local woodlands Strenuous: Long walk with terrain suitable for fit, experienced walkers. Beach/rockpool For walkers with disabilities Mobility 1 Suitable for a person with Toilets available sufficient mobility to climb a flight of steps but would benefit from fixtures and fittings to aid balance. Mobility 2 Suitable for a person with Stiles (number 3 restricted walking ability and for those that may on walk) need to use a wheelchair some of the time. Circular walk Mobility 3 Suitable for a person who depends on the use of a wheelchair. Mobility 4 Suitable for a person who depends Linear walk on the use of a medium-sized scooter. -

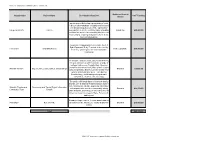

SWR CCIF 2020-2022 Schemes Full List - Island Line

SWR CCIF 2020-2022 schemes full list - Island Line Station or Nearest Organisation Project Name Description of project CCIF Funding Station an arts project delivering a programme of artist led outreach workshops engaging local isolated and disadvantaged people in the eight station Independent Arts 8 miles communities to create a lasting legacy of publicly Island Line £20,000.00 exhibited art works, demonstrating trainlines can be a unifying, inspiring and positive force at the heart of communities. To provide changing places accessible toilet at Ryde Esplanade Ferry Terminal, to be used by Hovertravel Changing Places Ryde Esplanade £30,000.00 both ferry passengers, rail users and wider community An inclusive and accessible project will involving integenerational research to provide a range of heritage trails across Shanklin Bay, Beaches (war-time and recreational); Bars (a trail of pubs Shanklin SVYCC Bay, Beaches, Bars, Battles and Buildings Shanklin £4,500.00 past and present); Battles (Commonwealth War Graves and World War sites – VC’s born in Shanklin Bay); and Buildings of significance (Churches, Theatres, Lift, Cinemas) The project will install digital information display boards, one at Shanklin Railway Station and the other at Shanklin Theatre displaying information Shanklin Theatre and Community and Tourist Digital Information on transport links and other community activity Shanklin £22,539.00 Community Trust Boards within Shanklin, and transport information and rail times for onward journeys to Ryde, Portsmouth and beyond. Providing