Audit Report on the Accounts of Defence Services Audit Year 2017-18

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Askari Bank Limited List of Shareholders (W/Out Cnic) As of December 31, 2017

ASKARI BANK LIMITED LIST OF SHAREHOLDERS (W/OUT CNIC) AS OF DECEMBER 31, 2017 S. NO. FOLIO NO. NAME OF SHAREHOLDERS ADDRESSES OF THE SHAREHOLDERS NO. OF SHARES 1 9 MR. MOHAMMAD SAEED KHAN 65, SCHOOL ROAD, F-7/4, ISLAMABAD. 336 2 10 MR. SHAHID HAFIZ AZMI 17/1 6TH GIZRI LANE, DEFENCE HOUSING AUTHORITY, PHASE-4, KARACHI. 3280 3 15 MR. SALEEM MIAN 344/7, ROSHAN MANSION, THATHAI COMPOUND, M.A. JINNAH ROAD, KARACHI. 439 4 21 MS. HINA SHEHZAD C/O MUHAMMAD ASIF THE BUREWALA TEXTILE MILLS LTD 1ST FLOOR, DAWOOD CENTRE, M.T. KHAN ROAD, P.O. 10426, KARACHI. 470 5 42 MR. M. RAFIQUE B.R.1/27, 1ST FLOOR, JAFFRY CHOWK, KHARADHAR, KARACHI. 9382 6 49 MR. JAN MOHAMMED H.NO. M.B.6-1728/733, RASHIDABAD, BILDIA TOWN, MAHAJIR CAMP, KARACHI. 557 7 55 MR. RAFIQ UR REHMAN PSIB PRIVATE LIMITED, 17-B, PAK CHAMBERS, WEST WHARF ROAD, KARACHI. 305 8 57 MR. MUHAMMAD SHUAIB AKHUNZADA 262, SHAMI ROAD, PESHAWAR CANTT. 1919 9 64 MR. TAUHEED JAN ROOM NO.435, BLOCK-A, PAK SECRETARIAT, ISLAMABAD. 8530 10 66 MS. NAUREEN FAROOQ KHAN 90, MARGALA ROAD, F-8/2, ISLAMABAD. 5945 11 67 MR. ERSHAD AHMED JAN C/O BANK OF AMERICA, BLUE AREA, ISLAMABAD. 2878 12 68 MR. WASEEM AHMED HOUSE NO.485, STREET NO.17, CHAKLALA SCHEME-III, RAWALPINDI. 5945 13 71 MS. SHAMEEM QUAVI SIDDIQUI 112/1, 13TH STREET, PHASE-VI, DEFENCE HOUSING AUTHORITY, KARACHI-75500. 2695 14 74 MS. YAZDANI BEGUM HOUSE NO.A-75, BLOCK-13, GULSHAN-E-IQBAL, KARACHI. -

REFORM OR REPRESSION? Post-Coup Abuses in Pakistan

October 2000 Vol. 12, No. 6 (C) REFORM OR REPRESSION? Post-Coup Abuses in Pakistan I. SUMMARY............................................................................................................................................................2 II. RECOMMENDATIONS.......................................................................................................................................3 To the Government of Pakistan..............................................................................................................................3 To the International Community ............................................................................................................................5 III. BACKGROUND..................................................................................................................................................5 Musharraf‘s Stated Objectives ...............................................................................................................................6 IV. CONSOLIDATION OF MILITARY RULE .......................................................................................................8 Curbs on Judicial Independence.............................................................................................................................8 The Army‘s Role in Governance..........................................................................................................................10 Denial of Freedoms of Assembly and Association ..............................................................................................11 -

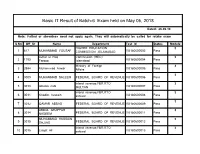

Basic IT Result of Batch-6 Exam Held on May 05, 2018

Basic IT Result of Batch-6 Exam held on May 05, 2018 Dated: 26-06-18 Note: Failled or absentees need not apply again. They will automatically be called for retake exam S.No Off_Sr Name Department Test Id Status Module HIGHER EDUCATION 3 1 617 MUHAMMAD YOUSAF COMMISSION ,ISLAMABAD VU180600002 Pass Azhar ul Haq Commission (HEC) 3 2 1795 Farooq Islamabad VU180600004 Pass Ministry of Foreign 3 3 2994 Muhammad Anwar Affairs VU180600005 Pass 3 4 3009 MUHAMMAD SALEEM FEDERAL BOARD OF REVENUE VU180600006 Pass inland revenue,FBR,RTO 3 5 3010 Ghulan nabi MULTAN VU180600007 Pass inland revenue,FBR,RTO 3 6 3011 Khadim hussain sahiwal VU180600008 Pass 3 7 3012 QAMAR ABBAS FEDERAL BOARD OF REVENUE VU180600009 Pass ABDUL GHAFFAR 3 8 3014 NADEEM FEDERAL BOARD OF REVENUE VU180600011 Pass MUHAMMAD HUSSAIN 3 9 3015 SAJJAD FEDERAL BOARD OF REVENUE VU180600012 Pass inland revenue,FBR,RTO 3 10 3016 Liaqat Ali sahiwal VU180600013 Pass inland revenue,FBR,RTO 3 11 3017 Tariq javed sahiwal VU180600014 Pass 3 12 3018 AFTAB AHMAD FEDERAL BOARD OF REVENUE VU180600015 Pass Basic IT Result of Batch-6 Exam held on May 05, 2018 Dated: 26-06-18 Muhammad inam-ul- inland revenue,FBR,RTO 3 13 3019 haq MULTAN VU180600016 Pass Ministry of Defense (Defense Division) 3 Rawalpindi. 14 4411 Asif Mehmood VU180600018 Pass 3 15 4631 Rooh ul Amin Pakistan Air Force VU180600022 Pass Finance/Income Tax 3 16 4634 Hammad Qureshi Department VU180600025 Pass Federal Board Of Revenue 3 17 4635 Arshad Ali Regional Tax-II VU180600026 Pass 3 18 4637 Muhammad Usman Federal Board Of Revenue VU180600027 -

Cards by Country PAKISTAN

Index cards by country PAKISTAN EXPORT PROCESSING ZONES, SPECIAL ECONOMIC ZONES Index cards realized by the University of Reims, France Conception: F. Bost Data collected by F. Bost and D. Messaoudi Map and layout: S. Piantoni WFZO Index cards - Pakistan Oicial Terms for Free Zones Year of promulgation of the irst text of law concerning the Free Zones Export Processing Zones, Special Economic Zones 1980 Possibility to be established as Exact number of Free Zones Free Points 12 No TABLE OF CONTENTS General information ........................................................................................................................................................................4 List of operating Export Processing Zones .............................................................................................................................6 List of Special Economic Zones (SEZ) ........................................................................................................................................9 Contacts ............................................................................................................................................................................................ 10 Free Zones Web sites selection ................................................................................................................................................ 11 2 WFZO Index cards - Pakistan Mary UZBEKISTAN TAJIKISTAN Termez TURKMENISTAN Konduz Mashhad Mazar-E Sharif Baghlan CHINA Kabul Jalabad 07 AFGHANISTAN -

Deh Safooran, Tappo Malir, Karachi

FEDERAL EMPLOYEES AIRPORT RESENDCIA KARACHI Project Is Located On Jinnah Avenue, Opposite Malir Cantonment And Adjacent To Karachi Airport. A Project of FGEHA With Smart Living Concept Smart Planning Concept 3, 4 & 5 Rooms Apartments JINNAH A VE PROPOSED ACACIA GOLF CLUB SITE FOR FGEHA TANK CHOWK VE VE TERMINAL A TIONAL JINNAH 14.20 ACRES JINNAH AVENUE ADJOINING KARACHI JINNAH INTERNA AIRPORT NEAR ACACIA GOLF CLUB 3, 4 & 5 Rooms Apartments State of the art facilities & amenities AIRPORT RD Introduction of FGEHA The Federal Government Employees Housing Authority was established through an act of parliament in January 2020. Main objective of FGEHA is to initiate, launch, sponsor and implement housing schemes for serving/retired Federal Government Employees on ownership basis in all major cities of Pakistan to eradicate shelterlessness. Before introduction of FGEHA Act 2020, it was known as Federal Government Employees Housing Foundation (FGEHF) under Ministry of Housing & Works, since 1989, as a guarantee limited company with Securities & Exchange Commission of Pakistan under section 42 of Companies Ordinance 1984. ACHIEVEMENTS FGE Housing Authority allotted number of units to its members in Islamabad,Peshawar & Karachi – 22483 number of units from 1989 to 2013 • 19421 Plots • 1595 Houses • 1467 Apartments – 32007 number of units from 2014 to 2019 planned/allotted to its members registered in Membership Drive Phase-I & Phase-II • 28923 Plots • 3084 Apartments Karachi City of Lights remains Pakistan's largest urban economy despite the economic stagnation caused by sociopolitical unrest during the late 1980s and 1990s. The city forms the centre of an economic corridor stretching from Karachi to nearby Hyderabad and Thatta. -

Usg Humanitarian Assistance to Pakistan in Areas

USG HUMANITARIAN ASSISTANCE TO CONFLICT-AFFECTED POPULATIONS IN PAKISTAN IN FY 2009 AND TO DATE IN FY 2010 Faizabad KEY TAJIKISTAN USAID/OFDA USAID/Pakistan USDA USAID/FFP State/PRM DoD Amu darya AAgriculture and Food Security S Livelihood Recovery PAKISTAN Assistance to Conflict-Affected y Local Food Purchase Populations ELogistics Economic Recovery ChitralChitral Kunar Nutrition Cand Market Systems F Protection r Education G ve Gilgit V ri l Risk Reduction a r Emergency Relief Supplies it a h Shelter and Settlements C e Food For Progress I Title II Food Assistance Shunji gol DHealth Gilgit Humanitarian Coordination JWater, Sanitation, and Hygiene B and Information Management 12/04/09 Indus FAFA N A NWFPNWFP Chilas NWFP AND FATA SEE INSET UpperUpper DirDir SwatSwat U.N. Agencies, E KohistanKohistan Mahmud-e B y Da Raqi NGOs AGCJI F Asadabad Charikar WFP Saidu KUNARKUNAR LowerLower ShanglaShangla BatagramBatagram GoP, NGOs, BajaurBajaur AgencyAgency DirDir Mingora l y VIJaKunar tro Con ImplementingMehtarlam Partners of ne CS A MalakandMalakand PaPa Li Î! MohmandMohmand Kabul Daggar MansehraMansehra UNHCR, ICRC Jalalabad AgencyAgency BunerBuner Ghalanai MardanMardan INDIA GoP e Cha Muzaffarabad Tithwal rsa Mardan dd GoP a a PeshawarPeshawar SwabiSwabi AbbottabadAbbottabad y enc Peshawar Ag Jamrud NowsheraNowshera HaripurHaripur AJKAJK Parachinar ber Khy Attock Punch Sadda OrakzaiOrakzai TribalTribal AreaArea Î! Adj.Adj. PeshawarPeshawar KurrumKurrum AgencyAgency Islamabad Gardez TribalTribal AreaArea AgencyAgency Kohat Adj.Adj. KohatKohat Rawalpindi HanguHangu Kotli AFGHANISTAN KohatKohat ISLAMABADISLAMABAD Thal Mangla reservoir TribalTribal AreaArea AdjacentAdjacent KarakKarak FATAFATA BannuBannu us Bannu Ind " WFP Humanitarian Hub NorthNorth WWaziristanaziristan BannuBannu SOURCE: WFP, 11/30/09 Bhimbar AgencyAgency SwatSwat" TribalTribal AreaArea " Adj.Adj. -

Paf Celebrates Golden Jubilee of Defence Day

PAF CELEBRATES GOLDEN JUBILEE OF DEFENCE DAY Islamabad 06 September, 2015:- Defence Day of Pakistan was celebrated at all PAF Bases in a befitting manner. The year has been marked as the Golden Jubilee of 1965 war, when PAF vanquished a three times large Indian Air Force and wrote an epic of unmatched valor and sacrifice. The auspicious day was observed with a renewed pledge and determination to make “Fizaia” even more stronger and potent force to face any challenge. The day started with special Du’a and Quran Khawani for the Shahuda at all PAF Bases. A special feature of the day was the change of guards ceremony at the Mazar of Quaid-e-Azam in Karachi. Aviation Cadets from Pakistan Air Force Academy, Risalpur assumed guard duties at the Mazar to honour the Father of the Nation. On the occasion of Defence Day Air Chief Marshal Sohail Aman, Chief of the Air Staff, Pakistan Air Force said in his message, “We are a resilient nation, which has always proved its worth in difficult times, whether those were natural calamities or an imposed armed conflict, as in 1965. Though, we are a peace loving nation, but we know how to thwart the heinous attempts that disrupt our peaceful way of life and certainly, our strength is in this resolve. Today, let us re- pledge to make Pakistan a truly dynamic and prosperous country by firmly following the great Quaid’s golden principles of Unity, Faith and Discipline as our national ideals. On this occasion, I would like to assure you that Pakistan Air Force, with state-of-the-art equipment on its inventory and a highly capable workforce, is fully prepared to defend the aerial frontiers of its motherland”. -

GOLDMINE? a Critical Look at the Commercialization of Afghan Demining

Bolton, Matthew GOLDMINE? A Critical Look at the Commercialization of Afghan Demining Centre for the Study of Global Governance (LSE) Research Paper 01/2008 Centre for the Study of Global Governance London School of Economics and Political Science Houghton Street, London WC2A 2AE http://www.lse.ac.uk/Depts/global 1 GOLDMINE ? A Critical Look at the Commercialization of Afghan Demining Matthew Bolton Centre for the Study of Global Governance London School of Economics and Political Science This research is funded in part by the Economic and Social Research Council All text, graphics and photos © Matthew Bolton, 2008. 2 Contents Acronyms........................................................................................................................ 4 Executive Summary........................................................................................................ 5 1. Introduction................................................................................................................. 8 2. A Brief History of Afghan Demining ....................................................................... 10 2.1 The Three Roots of Afghan Demining, 1987-1994............................................ 10 2.2. UN Hegemony, 1994-2001................................................................................ 19 2.3. The 9/11 Sea Change ......................................................................................... 23 2.4. Summary........................................................................................................... -

Annexures for Annual Report 2020

List of Annexures Annex A Minutes of the Annual General Meeting held on March 08, 2019 Annex B Detailed Expenditures on Purchase and Establishment of PCATP Head Office Islamabad Annex C Policy guidelines for Online Teaching-Learning and Assessment Implementation Annex D Thesis guidelines for graduating batch during COVID-19 pandemic Annex E Inclusion of PCATP in NAPDHA Annex F Inclusion of role of Architects and Town Planners in the CIDB Bill 2020 Annex G Circulation List for Compliance of PCATP Ordinance IX of 1983 Annex H Status of Institutions Offering Architecture and Town Planning Undergraduate Degree Programs in Pakistan Annex I List of Registered Members and Firms who have contributed towards COVID- 19 fund in PCATP Account Annex J List of Registered Members and Firms who have contributed towards COVID- 19 fund in IAP Account Audited Accounts and Balance Sheet of PCATP General Fund and RHS Annex K Account for the Year 2018-2019 Page | 1 ANNEX A MINUTES OF THE ANNUAL GENERAL MEETING OF THE PAKISTAN COUNCIL OF ARCHITECTS AND TOWN PLANNERS ON FRIDAY, 8th MARCH, 2019, AT RAMADA CREEK HOTEL, KARACHI. In accordance with the notice, the Annual General Meeting of the Pakistan Council of Architects and Town Planners was held at 1700 hrs on Friday, 8th March, 2019 at Crystal Hall, Ramada Creek Hotel, Karachi, under the Chairmanship of Ar. Asad I. A. Khan. 1.0 AGENDA ITEM NO.1 RECITATION FROM THE HOLY QURAN 1.1 The meeting started with the recitation of Holy Quran, followed by playing of National Anthem. 1.2 Ar. FarhatUllahQureshi proposed that the house should offer Fateha for PCATP members who have left us for their heavenly abode. -

South Central Asia

Volume I Section IV-V - South Central Asia Afghanistan ALP - Fiscal Year 2013 Department of Defense Training Course Title Qty Training Location Student's Unit US Unit - US Qty Total Cost Start Date End Date ALC ALP Scholarship 1 DLIELC, LACKLAND AFB TX Ministry of Defense DLIELC, LACKLAND AFB TX $17,120 9/10/2012 1/18/2013 Oral PROF AV ALP Scholarship 1 DLIELC, LACKLAND AFB TX Ministry of Defense DLIELC, LACKLAND AFB TX $12,548 12/31/2012 6/21/2013 Fiscal Year 2013 Program Totals 2 $29,668 CTFP - Fiscal Year 2013 Department of Defense Training Course Title Qty Training Location Student's Unit US Unit - US Qty Total Cost Start Date End Date ALC Specialized English Training Only 1 DLIELC, LACKLAND AFB TX National Directorate of Security DLIELC, LACKLAND AFB TX $10,464 1/14/2013 3/8/2013 American Language Course General English Training Only 1 DLIELC, LACKLAND AFB TX National Directorate of Security DLIELC, LACKLAND AFB TX $10,980 12/17/2012 1/11/2013 American Language Course General English Training Only 1 DLIELC, LACKLAND AFB TX National Directorate of Security DLIELC, LACKLAND AFB TX $20,705 1/14/2013 4/5/2013 American Language Course General English Training Only 2 DLIELC, LACKLAND AFB TX Ministry of Defense DLIELC, LACKLAND AFB TX $28,702 7/22/2013 9/6/2013 American Language Course General English Training Only 1 DLIELC, LACKLAND AFB TX National Directorate of Security DLIELC, LACKLAND AFB TX $15,036 7/22/2013 9/6/2013 American Language Course GET and SET 2 DLIELC, LACKLAND AFB TX National Directorate of Security DLIELC, LACKLAND AFB -

![Download Complete [PDF]](https://docslib.b-cdn.net/cover/6761/download-complete-pdf-896761.webp)

Download Complete [PDF]

Institute for Defence Studies and Analyses No.1, Development Enclave, Rao Tula Ram Marg Delhi Cantonment, New Delhi-110010 Journal of Defence Studies Publication details, including instructions for authors and subscription information: http://www.idsa.in/journalofdefencestudies Critical Analysis of Pakistani Air Operations in 1965: Weaknesses and Strengths Arjun Subramaniam To cite this article: Arjun Subramaniam (201 5): Critical Analysis of Pakistani Air Op erations in 1965: Weaknesses and Strengths, Journal of Defence Studies, Vol. 9, No. 3 July-September 2015, pp. 95-113 URL http://idsa.in/jds/9_3_2015_CriticalAnalysisofPakistaniAirOperationsin1965.html Please Scroll down for Article Full terms and conditions of use: http://www.idsa.in/termsofuse This article may be used for research, teaching and private study purposes. Any substantial or systematic reproduction, re- distribution, re-selling, loan or sub-licensing, systematic supply or distribution in any form to anyone is expressly forbidden. Views expressed are those of the author(s) and do not necessarily reflect the views of the IDSA or of the Government of India. Critical Analysis of Pakistani Air Operations in 1965 Weaknesses and Strengths Arjun Subramaniam* This article tracks the evolution of the Pakistan Air Force (PAF) into a potent fighting force by analysing the broad contours of joint operations and the air war between the Indian Air Force (IAF) and PAF in 1965. Led by aggressive commanders like Asghar Khan and Nur Khan, the PAF seized the initiative in the air on the evening of 6 September 1965 with a coordinated strike from Sargodha, Mauripur and Peshawar against four major Indian airfields, Adampur, Halwara, Pathankot and Jamnagar. -

Company Profile

Shaheen Medical Services, Opposite Benazir Bhutto Airport Chaklala, Rawalpindi Phone: +92-51-5405270,5780328, PAF: 3993 http://shaheenmedicalservices.com / Email: [email protected] Page 1 MISSION Gain trust of our valuable clients, with most efficient and ethical services, by providing quality pharmaceutical products with maximum shelf life procured from authentic sources. VISION SMS is continuously striving to be recognized as a leading distributor of pharmaceutical products by focusing on efficient and ethical delivery of services. GOAL To work in collaboration with our worthy partners, to provide high value and premium quality pharmaceutical products to our clients, in order to sustain long-term business relationship. Shaheen Medical Services, Opposite Benazir Bhutto Airport Chaklala, Rawalpindi Phone: +92-51-5405270,5780328, PAF: 3993 http://shaheenmedicalservices.com / Email: [email protected] Page 2 INTRODUCTION Shaheen Foundation, Pakistan Air Force (PAF), was established in 1977 under the Charitable Endowment Act, 1890, essentially to promote welfare for the benefit of serving and retired PAF personnel including its civilian’s employees and their dependents, and to this end generates funds through industrial and commercial enterprises. Since then, it has launched a number of profitable ventures to generate funds necessary for financing the Foundation’s welfare activities. Shaheen Medical Services (SMS) was established to fulfill the pharmaceutical and surgical requirement of Armed forces and public/private sector. Since it’s founding in Rawalpindi in 1996, Shaheen Medical Services, Shaheen Foundation, PAF has become the leading distributor of Pharmaceuticals & Surgical products in Pakistan Air Force Hospitals, with offices in 22 cities nationwide. SMS is a registered member of Rawalpindi Chamber of Commerce and Industries (RCC&I), Export Promotion Bureau (EPB) of Pakistan and Director General Defense Purchase (DGDP).