Corporate Strategy at Caribou Coffee [On Screen] Corporate Strategy At

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Restaurants in West Des Moines, Iowa

RESTAURANTS IN WEST DES MOINES, IOWA NAME ADDRESS AREA PHONE NAME ADDRESS AREA PHONE NAME ADDRESS AREA PHONE Restaurants - American Restaurants - Other Ethnic La Barista Coffee Bar 1963 Grand Avenue G3 515-267-1814 Applebee's Neighborhood Grill 6190 Mills Civic Pkwy B5 515-225-8646 Jethro's Jambalaya 9350 University Avenue inset 1 opens soon Let Them Eat Cake 405 Maple Street H4 515-277-1709 Bambino's Restaurant 1220 R 45 Hwy inset 2 515-981-9127 Mi Patria (Ecuadorian) 1410 22nd Street F1 515-222-2755 My Favorite Muffin 4949 Westown Pkwy # 170 D1 515-457-7117 Champps Americana 101 Jordan Creek Pkwy # 12520 B4 515-440-6565 Saraj (Bosnian) 1300 50th St # 206 D2 515-255-1133 Starbucks 101 Jordan Creek Pkwy # 12118 B4 515-222-2254 Cheesecake Factory 101 Jordan Creek Pkwy # 12550 B4 515-457-9888 Restaurants - Seafood Starbucks 1990 Grand Ave (in HyVee) G3 515-223-8151 Dahl's Grocery 1208 Prospect G3 515-224-2144 Bonefish Grill 650 S Prairie View Dr # 100 C4 515-267-0064 Starbucks 2800 University Ave # H3 F1 515-223-4200 Dahl's Grocery - Jordan Creek Cafe 5003 EP True Parkway D3 515-225-4445 Joe's Crab Shack 130 S Jordan Creek Pkwy B4 515-226-9966 Starbucks 5405 Mills Civic Pkwy (in Target) C4 515-223-0262 Famous Dave's 1720 22nd St F1 515-267-0800 Red Lobster 3838 Westown Pkwy E1 515-226-2150 Starbucks 555 S 51st St (in HyVee) D4 515-221-2610 Fire Creek Grill 800 S 50th St # 110 D5 515-224-0500 Waterfront Seafood Market 2900 University Ave # A4 F1 515-223-5106 Starbucks 6305 Mills Civic Pkwy B4 515-223-9263 Fresh Cafe & Market 1721 25th St -

Arby's Restaurant Group (ARG) Operates the Arby's Fast Food Chain Popular for Its Hot Roast Beef Sandwiches

Arby’s Restaurant 2312 Trustar Lane NW | Bemidji, MN | 56601 Keith A. Sturm, CCIM | 612.376.4488 | [email protected] 50 South 6th Street | Suite 1418 Amanda C. Leathers | 612.436.0045 | [email protected] Minneapolis, MN | 55402 Deborah K. Vannelli, CCIM | 612.376.4475 | [email protected] www.nnnsales.com Look Upland. Where Properties & People Unite! Arby’s Restaurant CONFIDENTIALITY & DISCLAIMER Bemidji, MN NET LEASED DISCLAIMER Upland Real Estate Group, Inc. hereby advises all prospective purchasers of Net Leased property as follows: The information contained in this Marketing Package has been obtained from sources we believe to be reliable. However, Upland Real Estate Group, Inc. has not and will not verify any of this information, nor has Upland Real Estate Group, Inc. conducted any investigation regarding these matters. Upland Real Estate Group, Inc. makes no guarantee, warranty or representation whatsoever about the accuracy or completeness of any information provided. As the Buyer of a net leased property, it is the Buyer’s responsibility to independently confirm the accuracy and completeness of all material information before completing any purchase. This Marketing Package is not a substitute for your thorough due diligence investigation of this investment opportunity. Upland Real Estate Group, Inc. expressly denies any obligation to conduct a due diligence examination of this Property for Buyer. Any projections, opinions, assumptions or estimates used in this Marketing Package are for example only and do not represent the current or future performance of this property. The value of a net leased property to you depends on factors that should be evaluated by you and your tax, financial, legal and other advisors. -

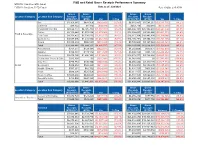

F&B and Retail Performance Summary

F&B and Retail Gross Receipts Performance Summary MTD PFY: Feb 20 vs. MTD: Feb 21 FYTD PY: Feb 20 vs. FYTD: Feb 21 Data as of: 2/28/2021 Run: 4/3/2021 2:45:35 PM 12:00:00 AM Gross Gross Gross Gross Location Category Location Sub Category Receipts Receipts Receipts Receipts (MTD PFY) (MTD) Var % Chg (FYTD PFY) (FYTD) Var % Chg Bar $1,304,445 $683,506 ($620,940) (47.6%) $6,915,987 $3,584,251 ($3,331,736) (48.2%) Cafeteria $94,422 $4,412 ($90,010) (95.3%) $563,776 $20,988 ($542,788) (96.3%) Casual Dining / Bar $8,622,777 $4,725,760 ($3,897,017) (45.2%) $46,204,191 $25,962,497 ($20,241,694) (43.8%) Coffee $2,113,840 $1,033,894 ($1,079,946) (51.1%) $12,008,453 $5,566,940 ($6,441,513) (53.6%) Food & Beverage Fast Food $4,732,427 $2,720,270 ($2,012,157) (42.5%) $26,617,764 $16,492,804 ($10,124,960) (38.0%) Quick Serve $3,087,096 $1,424,890 ($1,662,206) (53.8%) $16,105,292 $7,854,187 ($8,251,105) (51.2%) Snack $1,039,834 $506,591 ($533,243) (51.3%) $5,780,045 $3,187,024 ($2,593,021) (44.9%) Total $20,994,841 $11,099,323 ($9,895,517) (47.1%) $114,195,509 $62,668,691 ($51,526,818) (45.1%) Accessories $751,271 $129,194 ($622,077) (82.8%) $4,282,609 $879,671 ($3,402,938) (79.5%) Apparel $460,801 $149,112 ($311,689) (67.6%) $3,092,455 $864,193 ($2,228,262) (72.1%) Convenience $2,475,796 $1,456,149 ($1,019,648) (41.2%) $13,378,877 $8,728,854 ($4,650,022) (34.8%) Destination Themed Gifts $325,092 $0 ($325,092) (100.0%) $1,742,871 $0 ($1,742,871) (100.0%) Duty Free $778,784 $230,746 ($548,038) (70.4%) $6,056,484 $1,429,170 ($4,627,314) (76.4%) Retail -

CARIBOU COFFEE 520 JEFFERSON BOULEVARD • BIG LAKE, MN 55309 Affiliated Business Disclosure Property

BRAND NEW CONSTRUCTION COMPLETED DECEMBER 2019 FOR SALE CARIBOU COFFEE 520 JEFFERSON BOULEVARD • BIG LAKE, MN 55309 Affiliated Business Disclosure Property. All references to acreages, square footages, and other measurements are approximations. This Memorandum describes certain documents, including CBRE, Inc. operates within a global family of companies with many subsidiaries leases and other materials, in summary form. These summaries may not be and related entities (each an “Affiliate”) engaging in a broad range of commercial complete nor accurate descriptions of the full agreements referenced. Additional real estate businesses including, but not limited to, brokerage services, property information and an opportunity to inspect the Property may be made available and facilities management, valuation, investment fund management and to qualified prospective purchasers. You are advised to independently verify the development. At times different Affiliates, including CBRE Global Investors, Inc. accuracy and completeness of all summaries and information contained herein, or Trammell Crow Company, may have or represent clients who have competing to consult with independent legal and financial advisors, and carefully investigate interests in the same transaction. For example, Affiliates or their clients may the economics of this transaction and Property’s suitability for your needs. ANY have or express an interest in the property described in this Memorandum (the RELIANCE ON THE CONTENT OF THIS MEMORANDUM IS SOLELY AT “Property”), and may be the successful bidder for the Property. Your receipt YOUR OWN RISK. of this Memorandum constitutes your acknowledgment of that possibility and your agreement that neither CBRE, Inc. nor any Affiliate has an obligation to The Owner expressly reserves the right, at its sole discretion, to reject any or all disclose to you such Affiliates’ interest or involvement in the sale or purchase of expressions of interest or offers to purchase the Property, and/or to terminate the Property. -

Cadenza Document

VGM Club Report Date: Jul 2019 Contracted Manufacturer Report Mfr Name Has Rebate Has Pricing 3M Y Y Abbott Nutrition Y N ACH Food Companies Y N Advance Food Products LLC AFP Y Y AdvancePierre Y Y Agro Farma Inc Y Y Ajinomoto Windsor Inc (formerly Windsor Frozen Foods) Y N Allied Buying Corporation (ABC) Y N All Round Foods Bakery Products Y N Alpha Baking/National Baking Y N American Licorice Co Y N American Metalcraft Y N American Roland Food Corp Y N Amplify Snack Brands Y N Amy's Kitchen Inc Y N Anchor Packaging Y Y Antonio Mozzarella Factory Y N Appetizers And Inc Y Y Apple & Eve Y Y Argo Tea Y Y Arizona Tea - Hornell Brewing Company Y Y Armanino Foods Y Y Armour-Eckrich Meats LLC DBA Carando Y N Armour Eckrich - Smithfield Y Y Ateeco/Mrs T's Pierogies Y Y Atlantic Mills Co Y Y Awake Chocolate Y N Azar Nut Company Y N Bagcraft Packaging LLC Y N Bake N Joy Inc Y N Bakery De France Y Y Ballard Brands Y Y BarFresh Corporation Inc Y Y Barilla America Inc Y Y Basic American Food Co Y Y Bay Valley Foods LLC Y N Belgioioso Cheese Inc Y N Bel Kaukauna Cheese Co Y Y Berks Packing Co Inc Y N Berry Plastics Diet Kits Y N Berry Plastics Liners Y Y Beverage Air Y N Page 1 Of 9 VGM Club Report Date: Jul 2019 Contracted Manufacturer Report Mfr Name Has Rebate Has Pricing Beyond Meat Y Y B&G Foods Inc Y Y Big City Reds /American Foods Y N Big Red Inc Y Y BioSelect N Y Biscomerica Corp. -

Brandmaster Jack Food Court Pioneer Juggles Multiple Brands Masterfully

MULTI-BRAND 50 BY DEBBIE SELINSKY Brandmaster Jack Food court pioneer juggles multiple brands masterfully n 1996, Jack Hough was trying to had never been done before, but after including Arby’s, Sbarro, Subway, Steak figure out which restaurants to place I explained that it would not interfere ’n Shake, and signature concepts such where in a somewhat limited space with their menus and concepts, we were as JJ’s Sports Bar & Grill and the Buck- I at the North Georgia Premium able to get it done.” head Grill. Outlets mall. Over the years, Hough has extended When Hough explains how all his “It was our first outlet, and space for that consolidated food court model into brands work together, he makes it sound everything was an issue,” says the Ala- 14 airports, outlet malls, universities, simple. He says the cooking and presenta- bama native. “So I said, ‘Why can’t we and other “non-traditional” settings tion of most of his brands are done ahead run nine separate concepts out of the across 12 states. Today his company, of time. “The only thing we have in the same kitchen with one GM?’ A few of MSE Branded Foods, represents more kitchen is prep. That really streamlines my franchise friends had a fit because it than a dozen national franchise brands, things,” he says. “If I brought in a con- 26 MULTI-UNIT FRANCHISEE ISSUE II, 2014 MULTI-BRAND 50 cept with a kitchen in the back room, NAME: Jack Hough ery location we look at, we’re compet- that could be problematic, but we have ing with somebody. -

U.S. Sweets Sector: Ice Cream - Bakery and Pastry - Coffee

U.S. SWEETS SECTOR: ICE CREAM - BAKERY AND PASTRY - COFFEE MARKET REPORT 1 SWEETS 2 Index SWEETS ● Consumer Trends………………………………………... 4 ICE CREAM ● Overview…………………………………………………... 6 ● Top chains and producers…………………....………... 12 ● Trends……………………………………………………. 15 BAKERY AND PASTRY ● Overview………………………………………………….. 21 ● Top chains and producers…………………....……….... 25 ● Trends……………………………………………………...31 COFFEE ● Overview………………………………………………….. 35 ● Top chains and producers…………………....……….... 42 ● Trends…………………………………………………….. 46 PURCHASING POWER OF MILLENNIALS ● Ice Cream………………………………………………… 52 ● Bakery and Pastry……………………………………….. 53 ● Coffee……………………………………………………... 54 3 SWEETS Consumer trends According to a recent Tecnomic survey on consumers and desserts ● 49% of post-restaurant meal dessert occasions are eaten at a different location than where the main meal was eaten ● 41% eat dessert after a meal at least once a week ● 27% say they eat indulgent desserts more now than two years ago ● 46 % eat fruit for dessert at least once a week ● 31% say they’re more willing to try dairy free desserts than two years ago ● 34% say they’d be likely to order desserts that contain CBD from foodservice venues Key points from the survey ● 32% of consumers eat dessert after a meal at least twice a week ● 46% of consumers’ dessert occasions are planned (rather than impulse) ● 48% of consumers say they are willing to pay more for desserts made from scratch Source: Tecnomic 4 ICE CREAM OVERVIEW 5 ICE CREAM Overview ● The average American consumes more than 23 pounds of ice cream per year which equates 48 pints per person per year ● 98% of all U.S. households purchase ice cream, with more sold on Sunday than any other day of the week, while 87% have ice cream in their freezer at any given time. -

Product Guide

PRODUCT GUIDE Table of Contents Convenient and easy ordering 2 Coffee Phone: Toll Free 800.465.2088 Gold Star • Segafredo Zanetti • True Coffee Roasters • Fax: Toll Free at 800.465.2108 Steep & Brew • Starbucks Online: www.gold-star.biz 3 Coffee cont. Email: [email protected] Ancora • Stone Creek Coffee • Peet’s Coffee & Tea Just Coffee Cooperative • Kauai Coffee • Berres Brothers 4 K-Cups K-Cup Regular Coffees and Decaf Coffees K-Cup Flavored Coffees K-Cup Tea, Apple Cider and Hot Chocolate K-Cup Café Escapes K-Cup Value K-Cups 5 OC Capsules / Espresso Capsules / Pods Avalon Single Cup / Liquid Coffee OC Capsules - Segafredo Zanetti Espresso Capsules - Segafredo Zanetti Pod Regular and Decaf Coffees Pod Flavored Coffees Pod Teas Avalon Single Cup Liquid Coffee 6 Tea Bigelow Twinings Four Elements Tea Lipton 7 Hot Drink Mixes • Hot Drink Mixes BULK • Soda / Juice / Water • Popcorn 8 Ready-to-Bake Cookies Homestyle / Value Dough Cookies Additional Baking Needs 9 Cream & Sugar / Coffee Extras / Segafredo Zanetti Cups and Mugs Biodegradable Products 10 Paper Products Coffee Gold Star Premium 4879 ................................................................42 1.5 oz bags 8420PRE .........................................................48 2.0 oz bags Premium Decaf 4895 .....................................................42 1.5 oz bags 8420PREDF .........................................48 2.0 oz bags Signature Blend 091444 ................................................40 1.5 oz bags Dawnbreaker special blend for Gold Star JUSTDAWN .........18 -

Free2work Presents

FREE2WORK PRESENTS: COFFEE INDUSTRY TRENDS COFFEE COMPANY RATINGS | 2014 FREE2WORK PRESENTS: AUTHORS: Elin Eriksson, Hannah Darnton & Haley Wrinkle CO-AUTHOR: COFFEE INDUSTRY Tim Park ORGANIZATION: Not For Sale PRODUCED WITH SUPPORT FROM: TRENDS International Labor Rights Forum FREE2WORK COFFEE RATINGS | 2014 This Coffee Industry Trends report was funded in part by a grant from the United States Department of State. The opinions, findings, and conclusions stated herein are those of the author and do not necessarily reflect those of the United States Department of State. 1 Introduction | Coffee Industry Trends See how companies perform: (See Index pg 20 for brands these companies represent) Coffee is the world’s second-most traded commodity,1 supporting the livelihoods of an esti- mated 25 million smallholder farmers and workers around the globe.2 Its producers have faced CERTIFICATION LABEL KEY: difficult times over the last decade and a half; many farmers continuously fail to break even on A Green Mountain Coffee Roasters (FLO) FLO: Fairtrade Products their production costs.3 What is even worse, though, is that child and forced laborers work in Starbucks (FLO) RAC: Rainforest Alliance Products coffee production in fourteen countries around the world.4 The manner in which coffee compa- UTZ: UTZ Products nies purchase from and manage their supply chains has a direct impact on the welfare of these free and forced workers. Allegro Coffee (FLO) Peet’s (FLO) Coffee Industry Trends is the second of a series of Free2Work reports that examine what Allegro Coffee (RAC) Peet’s (RAC) leading brands are doing to assess and address modern day slavery within their supply chains. -

F&B and Retail Performance Summary

F&B and Retail Gross Receipts Performance Summary MTD PFY: Mar 20 vs. MTD: Mar 21 FYTD PY: Mar 20 vs. FYTD: Mar 21 Data as of: 3/31/2021 Run: 4/27/2021 2:16:34 PM 12:00:00 AM Gross Gross Gross Gross Location Category Location Sub Category Receipts Receipts Receipts Receipts (MTD PFY) (MTD) Var % Chg (FYTD PFY) (FYTD) Var % Chg Bar $722,594 $1,161,967 $439,373 60.8% $7,638,581 $4,746,218 ($2,892,363) (37.9%) Cafeteria $91,622 $6,166 ($85,456) (93.3%) $655,398 $27,155 ($628,244) (95.9%) Casual Dining / Bar $4,546,381 $7,407,690 $2,861,309 62.9% $50,750,572 $33,370,187 ($17,380,385) (34.2%) Coffee $1,428,441 $1,544,922 $116,482 8.2% $13,436,894 $7,111,862 ($6,325,032) (47.1%) Food & Beverage Fast Food $3,468,624 $4,316,885 $848,261 24.5% $30,086,387 $20,809,689 ($9,276,699) (30.8%) Quick Serve $1,766,286 $2,350,758 $584,472 33.1% $17,871,578 $10,204,945 ($7,666,633) (42.9%) Snack $644,084 $995,468 $351,383 54.6% $6,424,129 $4,182,492 ($2,241,638) (34.9%) Total $12,668,031 $17,783,856 $5,115,825 40.4% $126,863,541 $80,452,547 ($46,410,993) (36.6%) Accessories $314,282 $334,449 $20,167 6.4% $4,596,891 $1,214,120 ($3,382,771) (73.6%) Apparel $246,957 $252,860 $5,902 2.4% $3,339,413 $1,117,053 ($2,222,360) (66.5%) Convenience $1,683,733 $2,451,123 $767,390 45.6% $15,062,610 $11,179,977 ($3,882,633) (25.8%) Destination Themed Gifts $185,611 $0 ($185,611) (100.0%) $1,928,482 $0 ($1,928,482) (100.0%) Duty Free $497,311 $421,179 ($76,132) (15.3%) $6,553,795 $1,850,349 ($4,703,446) (71.8%) Retail Electronics $502,169 $627,045 $124,877 24.9% $6,089,028 -

Avoiding the Caffeine Crash: a Strategic Analysis and Recommendations for Starbucks

Avoiding the Caffeine Crash: A Strategic Analysis and Recommendations for Starbucks Remle Crowe Advisor: Prof. Parthiban David Spring 2010 University Honors in Business, Language & Culture Studies: Spanish Executive Summary On a mission to caffeinate the world, Starbucks set out to establish itself as the “most recognized and respected brand” (Starbucks, “About Us”). Starbucks appears to be well on its way to achieving this goal having seen astonishing success in recent years and becoming an international symbol for not only coffee, but for growth. Starbucks had what it believed to be a recession-proof product as during the post-9/11 recession, while other retailers were being hit hard, Starbucks was experiencing its 11 th consecutive year of 5% or higher comparable store sales growth (Moon and Quelch). However, with collapse of the housing bubble in the United States, the economy is once again on the downswing and consumers are pinching pennies. The coffee giant will not be able to walk away from this battle unscathed as Starbucks began to show signs of weakness for the first time, in January 2009 when the company announced that it would close 900 stores worldwide (Flynn). The following report is an evaluation of the key issues facing Starbucks and the specialty coffee shop industry as a whole. Recommendations are then provided for the strategic direction Starbucks should follow in order to face these challenges head-on and stay on top. Key Issues The year 2010 will pose a variety of obstacles for this caffeine giant: • How should Starbucks -

Starbucks BLM&P Research BLMP Research

BLM&P Research Starbucks BLM&P Research BLMP Research • Lourdes Becerra • Brian Litke • Kari McLean • Rebecca Prindable BLM&P Research Decline in Sales BLM&P Research Second Quarter 2009 Fiscal Highlights Apr. 29, 2009-- Starbucks Corporation (NASDAQ: SBUX) today reported financial results for its second quarter ended March 29, 2009. Net revenues of $2.3 billion, a decrease of 7.6 percent • Comparable store sales of negative eight percent; compared to negative nine percent in Q1 2009 • Cost reduction of approximately $120 million versus target of $100 million • EPS of $0.03; Non-GAAP EPS (excluding restructuring) of $0.16 BLM&P Research Starbucks Problem • Decrease in: • profit margin • drop in sales BLM&P Research Historical Financials & Employees Income Statement Year Revenue Net Income Net Profit Employees ($ mil.) ($ mil.) Margin Sep 2008 10,383.0 315.5 3.0% 176,000 Sep 2007 9,411.5 672.6 7.1% 172,000 Sep 2006 7,786.9 581.5 7.5% 145,800 Sep 2005 6,369.3 494.5 7.8% 115,000 Sep 2004 5,294.2 391.8 7.4% 96,700 Sep 2003 4,075.5 268.3 6.6% 74,000 Sep 2002 3,288.9 215.1 6.5% 62,000 Sep 2001 2,649.0 181.2 6.8% 54,000 BLM&P Research Decline in Sales BLM&P Research Decline in Sales BLM&P Research Coffee Market Overview • 54% of US adult population are coffee consumers1 • Americans drink more than 488 million cups of coffee a year2 • US coffee drinkers spend on average $164.71 per year on coffee3 • Average coffee consumption in the United States is 3.1 cups of coffee per day (NCA).