Avoiding the Caffeine Crash: a Strategic Analysis and Recommendations for Starbucks

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Coca-Cola's Swoop for Costa Coffee Will Cut Its

COCA-COLA’S SWOOP FOR COSTA COFFEE WILL CUT ITS EXPOSURE TO SUGAR AND PLASTIC BOTTLES THE GROWING LOATHING FOR THE WHITE STUFF MUST KEEP SOFT DRINKS EXECS AWAKE AT NIGHT By IMD Professor John W. Walsh IMD Chemin de Bellerive 23 PO Box 915, CH-1001 Lausanne Switzerland Tel: +41 21 618 01 11 Fax: +41 21 618 07 07 [email protected] www.imd.org Copyright © 2006-2018 IMD - International Institute for Management Development. All rights, including copyright, pertaining to the content of this website/publication/document are owned or controlled for these purposes by IMD, except when expressly stated otherwise. None of the materials provided on/in this website/publication/document may be used, reproduced or transmitted, in whole or in part, in any form or by any means, electronic or mechanical, including photocopying, recording or the use of any information storage and retrieval system, without permission in writing from IMD. To request such permission and for further inquiries, please contact IMD at [email protected]. Where it is stated that copyright to any part of the IMD website/publication/document is held by a third party, requests for permission to copy, modify, translate, publish or otherwise make available such part must be addressed directly to the third party concerned. COCA-COLA’S SWOOP FOR COSTA COFFEE WILL CUT ITS EXPOSURE TO SUGAR AND PLASTIC BOTTLES Coca-Cola’s £3.9 billion acquisition of Costa Coffee has made quite a ripple. Atlanta-based Coca-Cola is obviously best known for its soft drinks portfolio, found in supermarkets, kiosks, hotels, bars and restaurants around the world. -

Coca-Cola HBC Strengthens Its Coffee Portfolio with Minority Stake in Casa Del Caffè Vergnano and Exclusive, Long-Term Distribution Agreement

Coca-Cola HBC strengthens its coffee portfolio with minority stake in Casa del Caffè Vergnano and exclusive, long-term distribution agreement Zug, Switzerland, 28 June 2021. Coca-Cola HBC AG (“Coca-Cola HBC”) is pleased to announce that on 25 June 2021, its wholly-owned subsidiary CC Beverages Holdings II B.V. (“CCH Holdings”), reached an agreement to acquire a 30% equity shareholding in Casa Del Caffè Vergnano S.p.A. (“Caffè Vergnano”), a premium Italian coffee company. Completion of the acquisition is expected in the second half of 2021 and is subject to customary closing conditions and regulatory approvals. Furthermore, Coca-Cola HBC and Caffè Vergnano will enter into an exclusive distribution agreement for Caffè Vergnano’s products in Coca-Cola HBC’s territories outside of Italy (together, the “Proposed Transaction”). CCH Holdings will be represented on the Board of Directors of Caffè Vergnano and have customary minority decision-making and governance rights. The parties have agreed not to disclose financial details of the Proposed Transaction. Caffè Vergnano is a family-owned Italian coffee company headquartered in Santena, Italy. It is one of the oldest coffee roasters in Italy with roots dating back to 1882. Its product offering consists of truly premium, high-quality coffee that represents Italian heritage and authenticity at its best. Caffè Vergnano’s portfolio includes traditional espresso in various blends, packages and formats such as beans, roast and ground coffee and single portioned pods. In 2020, the company sold approx. 7,000 tons of coffee in more than 90 countries worldwide. The Proposed Transaction represents an important milestone in Coca-Cola HBC’s vision of being the leading 24/7 beverage partner across its markets. -

Proposed Acquisition of Costa Limited

PROPOSED ACQUISITION OF COSTA LIMITED AUGUST 31, 2018 FORWARD-LOOKING STATEMENTS This presentation may contain statements, estimates or projections that constitute “forward-looking statements” as defined under U.S. federal securities laws. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will,” “plan,” “seek” and similar expressions identify forward-looking statements, which generally are not historical in nature. However, the absence of these words or similar expressions does not mean that a statement is not forward-looking. Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from The Coca-Cola Company’s historical experience and our present expectations or projections. These risks include, but are not limited to, obesity and other health-related concerns; water scarcity and poor quality; evolving consumer preferences; increased competition; product safety and quality concerns; perceived negative health consequences of certain ingredients, such as non- nutritive sweeteners and biotechnology-derived substances, and of other substances present in our beverage products or packaging materials; an inability to be successful in our innovation activities; increased demand for food products and decreased agricultural productivity; an inability to protect our information systems against service interruption, misappropriation of data or breaches of security; changes in the retail landscape or the loss of key retail or foodservice -

Restaurants in West Des Moines, Iowa

RESTAURANTS IN WEST DES MOINES, IOWA NAME ADDRESS AREA PHONE NAME ADDRESS AREA PHONE NAME ADDRESS AREA PHONE Restaurants - American Restaurants - Other Ethnic La Barista Coffee Bar 1963 Grand Avenue G3 515-267-1814 Applebee's Neighborhood Grill 6190 Mills Civic Pkwy B5 515-225-8646 Jethro's Jambalaya 9350 University Avenue inset 1 opens soon Let Them Eat Cake 405 Maple Street H4 515-277-1709 Bambino's Restaurant 1220 R 45 Hwy inset 2 515-981-9127 Mi Patria (Ecuadorian) 1410 22nd Street F1 515-222-2755 My Favorite Muffin 4949 Westown Pkwy # 170 D1 515-457-7117 Champps Americana 101 Jordan Creek Pkwy # 12520 B4 515-440-6565 Saraj (Bosnian) 1300 50th St # 206 D2 515-255-1133 Starbucks 101 Jordan Creek Pkwy # 12118 B4 515-222-2254 Cheesecake Factory 101 Jordan Creek Pkwy # 12550 B4 515-457-9888 Restaurants - Seafood Starbucks 1990 Grand Ave (in HyVee) G3 515-223-8151 Dahl's Grocery 1208 Prospect G3 515-224-2144 Bonefish Grill 650 S Prairie View Dr # 100 C4 515-267-0064 Starbucks 2800 University Ave # H3 F1 515-223-4200 Dahl's Grocery - Jordan Creek Cafe 5003 EP True Parkway D3 515-225-4445 Joe's Crab Shack 130 S Jordan Creek Pkwy B4 515-226-9966 Starbucks 5405 Mills Civic Pkwy (in Target) C4 515-223-0262 Famous Dave's 1720 22nd St F1 515-267-0800 Red Lobster 3838 Westown Pkwy E1 515-226-2150 Starbucks 555 S 51st St (in HyVee) D4 515-221-2610 Fire Creek Grill 800 S 50th St # 110 D5 515-224-0500 Waterfront Seafood Market 2900 University Ave # A4 F1 515-223-5106 Starbucks 6305 Mills Civic Pkwy B4 515-223-9263 Fresh Cafe & Market 1721 25th St -

Arby's Restaurant Group (ARG) Operates the Arby's Fast Food Chain Popular for Its Hot Roast Beef Sandwiches

Arby’s Restaurant 2312 Trustar Lane NW | Bemidji, MN | 56601 Keith A. Sturm, CCIM | 612.376.4488 | [email protected] 50 South 6th Street | Suite 1418 Amanda C. Leathers | 612.436.0045 | [email protected] Minneapolis, MN | 55402 Deborah K. Vannelli, CCIM | 612.376.4475 | [email protected] www.nnnsales.com Look Upland. Where Properties & People Unite! Arby’s Restaurant CONFIDENTIALITY & DISCLAIMER Bemidji, MN NET LEASED DISCLAIMER Upland Real Estate Group, Inc. hereby advises all prospective purchasers of Net Leased property as follows: The information contained in this Marketing Package has been obtained from sources we believe to be reliable. However, Upland Real Estate Group, Inc. has not and will not verify any of this information, nor has Upland Real Estate Group, Inc. conducted any investigation regarding these matters. Upland Real Estate Group, Inc. makes no guarantee, warranty or representation whatsoever about the accuracy or completeness of any information provided. As the Buyer of a net leased property, it is the Buyer’s responsibility to independently confirm the accuracy and completeness of all material information before completing any purchase. This Marketing Package is not a substitute for your thorough due diligence investigation of this investment opportunity. Upland Real Estate Group, Inc. expressly denies any obligation to conduct a due diligence examination of this Property for Buyer. Any projections, opinions, assumptions or estimates used in this Marketing Package are for example only and do not represent the current or future performance of this property. The value of a net leased property to you depends on factors that should be evaluated by you and your tax, financial, legal and other advisors. -

Cultural Innovation: Triumph of a Better Ideology’ Look to Anthropology for Inspiration

QUARTER 1 JANUARY 2012 NEW THINKING, DIFFERENT PERSPECTIVES Cultural innovation: triumph of a better ideology Douglas Holt and Douglas Cameron NEVER WASTE A GOOD CRISIS Sir Terry Leahy QUARTER 1 QUARTER 2012 JANUARY ACCOUNTABILITY IS NOT ENOUGH Rory Sutherland THROUGH THE GLASS CEILING Janet Hull 1 cover.indd 1 28/11/2011 19:34:31 Market Leader_Experienica.HR.pdf 1 11/11/2011 13:05 Editorial Keeping brands healthy i rEcEntly attended a lecture on the applications of neuroscience to marketing. All the data marketers will ever need, it was claimed, can now be obtained from ‘neurometrics’ – via MRI scanning, EEG measurement and eye-tracking devices. I listened to the lengthening list of uses with mounting disquiet and an article formed in my mind entitled ‘Caution: neuroscience may be dangerous to the health of your brand’. The lead article in this issue provides the explanation of why the skills required for brand building live in a parallel universe. Douglas Holt and Douglas Cameron in ‘Cultural innovation: triumph of a better ideology’ look to anthropology for inspiration. It is commonplace to say that brands live in the mind (as opposed to the factory). But where they really live is in culture, in society’s norms, values, codes and practices. And while yes, neuroscience and anthropology can exist together, the danger is in what we qualitative researchers call ‘physics envy’ (the need to elevate market research to the level of the pure sciences). Put access to the brain – the human version of the Rosetta Stone – together with lots of gadgetry that measures things and before you know it, the new and intriguing drives out the old but essential. -

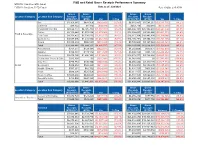

F&B and Retail Performance Summary

F&B and Retail Gross Receipts Performance Summary MTD PFY: Feb 20 vs. MTD: Feb 21 FYTD PY: Feb 20 vs. FYTD: Feb 21 Data as of: 2/28/2021 Run: 4/3/2021 2:45:35 PM 12:00:00 AM Gross Gross Gross Gross Location Category Location Sub Category Receipts Receipts Receipts Receipts (MTD PFY) (MTD) Var % Chg (FYTD PFY) (FYTD) Var % Chg Bar $1,304,445 $683,506 ($620,940) (47.6%) $6,915,987 $3,584,251 ($3,331,736) (48.2%) Cafeteria $94,422 $4,412 ($90,010) (95.3%) $563,776 $20,988 ($542,788) (96.3%) Casual Dining / Bar $8,622,777 $4,725,760 ($3,897,017) (45.2%) $46,204,191 $25,962,497 ($20,241,694) (43.8%) Coffee $2,113,840 $1,033,894 ($1,079,946) (51.1%) $12,008,453 $5,566,940 ($6,441,513) (53.6%) Food & Beverage Fast Food $4,732,427 $2,720,270 ($2,012,157) (42.5%) $26,617,764 $16,492,804 ($10,124,960) (38.0%) Quick Serve $3,087,096 $1,424,890 ($1,662,206) (53.8%) $16,105,292 $7,854,187 ($8,251,105) (51.2%) Snack $1,039,834 $506,591 ($533,243) (51.3%) $5,780,045 $3,187,024 ($2,593,021) (44.9%) Total $20,994,841 $11,099,323 ($9,895,517) (47.1%) $114,195,509 $62,668,691 ($51,526,818) (45.1%) Accessories $751,271 $129,194 ($622,077) (82.8%) $4,282,609 $879,671 ($3,402,938) (79.5%) Apparel $460,801 $149,112 ($311,689) (67.6%) $3,092,455 $864,193 ($2,228,262) (72.1%) Convenience $2,475,796 $1,456,149 ($1,019,648) (41.2%) $13,378,877 $8,728,854 ($4,650,022) (34.8%) Destination Themed Gifts $325,092 $0 ($325,092) (100.0%) $1,742,871 $0 ($1,742,871) (100.0%) Duty Free $778,784 $230,746 ($548,038) (70.4%) $6,056,484 $1,429,170 ($4,627,314) (76.4%) Retail -

CARIBOU COFFEE 520 JEFFERSON BOULEVARD • BIG LAKE, MN 55309 Affiliated Business Disclosure Property

BRAND NEW CONSTRUCTION COMPLETED DECEMBER 2019 FOR SALE CARIBOU COFFEE 520 JEFFERSON BOULEVARD • BIG LAKE, MN 55309 Affiliated Business Disclosure Property. All references to acreages, square footages, and other measurements are approximations. This Memorandum describes certain documents, including CBRE, Inc. operates within a global family of companies with many subsidiaries leases and other materials, in summary form. These summaries may not be and related entities (each an “Affiliate”) engaging in a broad range of commercial complete nor accurate descriptions of the full agreements referenced. Additional real estate businesses including, but not limited to, brokerage services, property information and an opportunity to inspect the Property may be made available and facilities management, valuation, investment fund management and to qualified prospective purchasers. You are advised to independently verify the development. At times different Affiliates, including CBRE Global Investors, Inc. accuracy and completeness of all summaries and information contained herein, or Trammell Crow Company, may have or represent clients who have competing to consult with independent legal and financial advisors, and carefully investigate interests in the same transaction. For example, Affiliates or their clients may the economics of this transaction and Property’s suitability for your needs. ANY have or express an interest in the property described in this Memorandum (the RELIANCE ON THE CONTENT OF THIS MEMORANDUM IS SOLELY AT “Property”), and may be the successful bidder for the Property. Your receipt YOUR OWN RISK. of this Memorandum constitutes your acknowledgment of that possibility and your agreement that neither CBRE, Inc. nor any Affiliate has an obligation to The Owner expressly reserves the right, at its sole discretion, to reject any or all disclose to you such Affiliates’ interest or involvement in the sale or purchase of expressions of interest or offers to purchase the Property, and/or to terminate the Property. -

Cadenza Document

VGM Club Report Date: Jul 2019 Contracted Manufacturer Report Mfr Name Has Rebate Has Pricing 3M Y Y Abbott Nutrition Y N ACH Food Companies Y N Advance Food Products LLC AFP Y Y AdvancePierre Y Y Agro Farma Inc Y Y Ajinomoto Windsor Inc (formerly Windsor Frozen Foods) Y N Allied Buying Corporation (ABC) Y N All Round Foods Bakery Products Y N Alpha Baking/National Baking Y N American Licorice Co Y N American Metalcraft Y N American Roland Food Corp Y N Amplify Snack Brands Y N Amy's Kitchen Inc Y N Anchor Packaging Y Y Antonio Mozzarella Factory Y N Appetizers And Inc Y Y Apple & Eve Y Y Argo Tea Y Y Arizona Tea - Hornell Brewing Company Y Y Armanino Foods Y Y Armour-Eckrich Meats LLC DBA Carando Y N Armour Eckrich - Smithfield Y Y Ateeco/Mrs T's Pierogies Y Y Atlantic Mills Co Y Y Awake Chocolate Y N Azar Nut Company Y N Bagcraft Packaging LLC Y N Bake N Joy Inc Y N Bakery De France Y Y Ballard Brands Y Y BarFresh Corporation Inc Y Y Barilla America Inc Y Y Basic American Food Co Y Y Bay Valley Foods LLC Y N Belgioioso Cheese Inc Y N Bel Kaukauna Cheese Co Y Y Berks Packing Co Inc Y N Berry Plastics Diet Kits Y N Berry Plastics Liners Y Y Beverage Air Y N Page 1 Of 9 VGM Club Report Date: Jul 2019 Contracted Manufacturer Report Mfr Name Has Rebate Has Pricing Beyond Meat Y Y B&G Foods Inc Y Y Big City Reds /American Foods Y N Big Red Inc Y Y BioSelect N Y Biscomerica Corp. -

Coca-Cola HBC 2020 Integrated Annual Report

Integrated Annual Report 2020 Coca‑Cola HBC Integrated Annual Report 2020 ADAPT TO WIN OUR PEOPLE p.38 OUR SUPPLIERS p.34 THANK YOU In a year of being apart, we have been more together. OUR PEOPLE p.38 OUR CUSTOMERS p.30 OUR SUPPLIERS p.34 OUR COMMUNITIES p.42 THANK YOU OUR CONSUMERS p.26 In a year of being apart, we have been more together. 2020 highlights Volume (m unit cases) Net sales revenue (€m) 2,135.6 6,131.8 2019: 2,264.5 2019: 7,026.0 Comparable EBIT1 (€m) Comparable EBIT1 margin (%) 672.3 11.0% 2019:758.7 2019: 10.8% Profit before tax (€m) Net profit2 (€m) 593.9 414.9 2019: 661.2 2019: 487.5 Comparable EPS1 (€) Basic EPS (€) 1.185 1.140 2019: 1.436 2019: 1.340 Primary packaging collected In 2020, we started reporting against for recycling (equivalent) the SASB framework. 44% 2019: 48% 1. For details on APMs, refer to ‘Alternative performance measures’ section. 2. Net profit and comparable net profit refer to net You can read more on page 132. profit and comparable net profit respectively after tax attributable to owners of the parent. Contents Strategic Report Corporate Governance Supplementary Information 10 Chairman’s letter 76 Chairman’s introduction 230 Alternative performance measures 12 Chief Executive Officer’s letter to corporate governance 233 Other supplementary information 14 Our business at a glance 80 Board of Directors 234 Assurance statement 16 Our business model 84 Corporate Governance Report 238 Glossary 18 Our socio-economic impact 110 Directors’ Remuneration Report 20 Stakeholder engagement 131 Statement -

REGULAMIN KONKURSU PROWADZONEGO POD NAZWĄ: „Święta W Livio Z Coca-Cola” §1 POSTANOWIENIA OGÓLNE

REGULAMIN KONKURSU PROWADZONEGO POD NAZWĄ: „Święta w Livio z Coca-Cola” §1 POSTANOWIENIA OGÓLNE 1. Konkurs będzie prowadzony pod nazwą „Święta w Livio z Coca-Cola” (zwany dalej „Konkursem”). 2. Podmiotem urządzającym Konkurs jest „Agencja Reklamowa Fortis” Sp. Jawna, z siedzibą w Warszawie przy ul. Gawińskiego 7, wpisana do Rejestru Przedsiębiorców w Krajowym Rejestrze Sądowym prowadzonym przez Sąd Rejonowy dla m.st. Warszawy, nr KRS 0000080471, NIP: 5240304216 („Organizator”). 3. Organizator przeprowadza Konkurs na zlecenie Coca-Cola HBC Polska sp. z o.o. z siedzibą w Warszawie (03-236), przy ul. Annopol 20, wpisaną do Krajowego Rejestru Sądowego prowadzonego przez Sąd Rejonowy w Warszawie, XIII Wydział Gospodarczy Krajowego Rejestru Sądowego pod nr KRS: 0000015664, o kapitale zakładowym 400.292.600,00 PLN, REGON: 012833736, NIP: 524-21-06-963, BDO: 000035278, reprezentowaną przez należycie umocowanego przedstawiciela, zwaną dalej („CCHBC”). 4. Uczestnikiem Konkursu może być każda pełnoletnia osoba fizyczna zamieszkała na terenie Polski, dokonująca zakupu w sklepach prowadzących sprzedaż produktów objętych Konkursem na terenie Polski, będąca konsumentem w rozumieniu art. 22¹ kodeksu cywilnego (zwany dalej „Uczestnikiem”). 5. Konkurs prowadzony będzie w sieci sklepów Polska Sieć Handlowa Livio S.A., ul. Pszczyńska 186, 44-335 Jastrzębie-Zdrój występujących pod nazwą Livio – lista sklepów dostępna jest na stronie https://liviosklepy.pl/znajdz-sklep 6. Konkurs zaczyna się 23.11.2020 roku, a kończy dnia 20.12.2020 roku. 7. Konkursem objęte są wszystkie produkty Coca-Cola w wszystkich dostępnych pojemnościach od 2l do 0,2l w tym puszki oraz produkty Costa Coffee we wszystkich dostępnych opakowaniach. Listę stanowi załącznik nr 1 (dalej: „Produkty Promocyjne”) 8. -

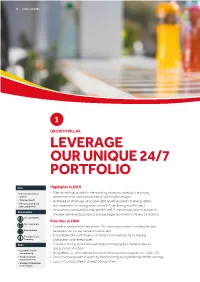

Leverage Our Unique 24/7 Portfolio

26 COCA-COLA HBC 1 GROWTH PILLAR LEVERAGE OUR UNIQUE 24/7 PORTFOLIO KPIs Highlights in 2019 • FX-neutral revenue • Maintained high growth in the sparkling category, aided by the strong growth performance of sophisticated adult sparkling beverages • Volume growth • Achieved another year of double-digit revenue growth in energy drinks • FX-neutral revenue per case growth and expanded the energy portfolio with Coke Energy and Predator • Innovations supported overall growth, with 4.2pp of total volume growth in Stakeholders the year delivered by products and packages launched in the last 12 months Our consumers Priorities in 2020 Our customers • Continue expanding to become a 24/7 beverage partner, creating shared Shareholders value with our consumers and customers The Coca-Cola • Consolidate the performance of product innovations by increasing Company distribution and repeat sales Risks • Continue driving growth in sparkling by leveraging light variants, flavour and pack architecture • Consumer health and wellbeing • Bring ready-to-drink tea back to growth through a strong plan for FUZETEA • Geopolitical and • Drive revenue growth in water by implementing our hydration portfolio strategy macroeconomic • Launch Costa Coffee in at least 10 countries • Strategic stakeholder relationships INTEGRATED ANNUAL REPORT 2019 27 SR CG FS SSR SI Introduction As lifestyles and consumer habits change, Percentage the motivations and occasions driving of Coca-Cola beverage consumption are also evolving. HBC revenue Our category strategy We are unlocking growth potential in segments beyond our core sparkling portfolio, offering a wider choice of drinks to meet consumer needs at any time of the day. In line with growing societal concerns around environmental issues, consumers are looking for sustainably-sourced ingredients and responsible packaging.