Ishares TA-25 Israel UCITS ETF (TASE)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fact Sheet:Middle East and Africa ESG Screened Index Equity Sub

EMEA_INST Managed Pension Funds Limited Middle East and Africa ESG Screened Index Equity Sub-Fund Equities 30 June 2021 Fund Objective Performance ® The Sub-Fund aims to track the FTSE Developed Annualised Fund Benchmark Difference Middle East and Africa ex Controversies ex CW 1 Year (%) 23.30 23.28 0.01 Index, or its recognised replacement or equivalent. 3 Year (%) 4.75 4.84 -0.09 Investment Strategy 5 Year (%) 0.78 0.89 -0.11 The Sub-Fund primarily invests at all times in a Since Inception (%) 4.04 4.18 -0.14 sample of equities constituting the Index with such other securities as MPF shall deem it necessary Cumulative to capture the performance of the Index. Stock 3 Month (%) 11.54 11.51 0.04 index futures can be used for efficient portfolio 1 Year (%) 23.30 23.28 0.01 management. 3 Year (%) 14.95 15.24 -0.29 The following are excluded by the index provider from the index: Controversies (as defined by the ten 5 Year (%) 3.96 4.52 -0.56 principles of the UN Global Compact); Controversial Since Inception (%) 65.75 68.57 -2.81 weapons (including chemical & biological weapons, cluster munitions and anti-personnel landmines). Calendar 2021 (year to date) 9.74 9.71 0.03 Benchmark 2020 -1.28 -1.47 0.19 FTSE Developed Middle East and Africa ex 2019 10.82 11.07 -0.24 Controversies ex CW Index 2018 -0.47 -0.12 -0.35 Structure 2017 -10.77 -10.66 -0.12 Limited Company Past performance is not a guarantee of future results. -

Bluestar Israel Quarterly Update Q3 2013 Final.Pptx

BlueStar Israel Equity Update Third Quarter 2013 Q2 2013 in Review & Second Half 2013 Outlook What’s Inside Ø Global developed market equities pulled back slightly in Q2 2013 while U.S. stocks, as measured by the S&P 500 index, bucked the trend and posted a rise of 2.91%. Ø The BlueStar Israel Global Index was down by 95 bps in Q2 2013 while the MSCI Israel and TA-100 indexes were down 4.16% and 2.76%, respectively. 1. The BlueStar Ø Israeli consumer stocks, which are correlated with both domestic consumption as well as consumer spending in Israel’s export markets, lead Israeli Global Equities in Q2, while the Israel Global financial and energy stocks, which lead the Israeli Global Equity market’s rebound from the Index in Q1 2012 lows, consolidated. 2013 Ø The Israeli government decided on a 2013 and 2014 budget that will result in tax increases and spending cuts and the Shekel’s sharp appreciation versus the dollar and euro eased a bit. 2-5. About the Ø Mellanox Technologies announced it will delist its shares from the Tel Aviv Stock Exchange and the TASE’s bid to be included in MSCI’s European regional indexes was declined. Both BlueStar Israel events sparked concern about the future of the local exchange. Also, Israeli corporate Global Index pyramids come under attack by The Committee on Increasing Competitiveness in the Economy and the Business Concentration Law. (including Risk/ Ø The Energy sector is asserting itself as a major player in the Israeli economy, natural gas Return Data) reserve estimates and oil estimates are rising, and the government has decided upon an export strategy, clearing up uncertainty and removing some of the risk factors associated with investing in that sector. -

Delek Group Economic Interest 14.44%

Flow of Natural Gas from Tamar Field Restarted Tel Aviv, September 27, 2017. Delek Group (TASE: DLEKG, US ADR: DGRLY) (“the Company”) announces that attached is an Immediate Report published by Delek Drilling Limited Partnership (“the Partnership”) concerning the restart of the flow of natural gas from the Tamar field. Further to what was stated in the Partnership’s Immediate Report dated September 23, 2017 concerning locating a crack in the exhaust pipe used on the Tamar platform to release natural gas and pressure both in normal and emergency times (“the Fault”) while Noble Energy Mediterranean Ltd (“the Operator”) was carrying out upgrade and improvement works on the Tamar platform, the Partnership announces that this morning the flow of natural gas was recommenced from the Tamar field after the Operator had completed the repair of the fault yesterday. It should be noted that the Operator is continuing to carry out the planned upgrade works. It should also be noted, according to the Partnership’s estimates, that the costs of repair of the Fault and its impact on the Partnership’s revenues from sales of natural gas are not material, as detailed in the Immediate Report of September 23, 2017. Partners in the Tamar Project and their percentage holdings: Noble Energy Mediterranean Ltd 32.50% Isramco Negev 2, Limited Partnership 28.75% Delek Drilling Limited Partnership 22.00% Tamar Petroleum Ltd 9.25% Dor Gas Exploration Limited Partnership 4.00% Everest Infrastructure Limited Partnership 3.50% Delek Group economic interest 14.44% This is a convenience translation of the original HEBREW immediate report issued to the Tel Aviv Stock Exchange by the Company on September 27, 2017. -

Domestically Owned Versus Foreign-Owned Banks in Israel

Domestic bank intermediation: domestically owned versus foreign-owned banks in Israel David Marzuk1 1. The Israeli banking system – an overview A. The structure of the banking system and its scope of activity Israel has a highly developed banking system. At the end of June 2009, there were 23 banking corporations registered in Israel, including 14 commercial banks, two mortgage banks, two joint-service companies and five foreign banks. Despite the spate of financial deregulation in recent years, the Israeli banking sector still plays a key role in the country’s financial system and overall economy. It is also highly concentrated – the five main banking groups (Bank Hapoalim, Bank Leumi, First International Bank, Israel Discount Bank and Mizrahi-Tefahot Bank) together accounted for 94.3% of total assets as of June 2009. The two largest groups (Bank Leumi and Bank Hapoalim) accounted for almost 56.8% of total assets. The sector as a whole and the large banking groups in particular are organised around the concept of “universal” banking, in which commercial banks offer a full range of retail and corporate banking services. Those services include: mortgages, leasing and other forms of finance; brokerage in the local and foreign capital markets; underwriting and investment banking; and numerous specialised services. Furthermore, until the mid-1990s, the banking groups were deeply involved in non-financial activities. However, a law passed in 1996 forced the banks to divest their controlling stakes in non-financial companies and conglomerates (including insurance companies). This development was part of a privatisation process which was almost completed in 2005 (with the important exception of Bank Leumi). -

Delek Cover English 04.2006

ANNUAL REPORT 2005 Delek Group Ltd 7, Giborei Israel St., P.O.B 8464, Industrial Zone South, Netanya 42504, Israel Tel: 972 9 8638444, 972 9 8638555 Fax: 972 9 885495 www.delek-group.com Table of Contents: Chapter A Corporate Description Chapter B Director's Report on the Corporation Chapter C Financial Statements for December 31, 2004 Chapter D Additional Information on the Corporation Chapter E MATAV - CABLE SYSTEMS MEDIA LTD IMPORTANT This document is an unofficial translation from the Hebrew original of the 2005 annual report of Delek Group Ltd. that was submitted to the Tel-Aviv Stock Exchange and the Israeli Securities Authority on March 29, 2006. The Hebrew version submitted to the TASE and the Israeli Securities Authority shall be the sole binding version. Investors are urged to review the full Hebrew report. Part One – A Description of the General Development of the Company's Businesses 1. The Company's Activities and the Development of its Business ......................... 3 2. Sectors of Operation .................................................................................................. 6 3. Equity Investments in the Company and Transactions in its Shares................... 7 4. Dividend Distribution ................................................................................................. 8 5. Financial Information Regarding the Group's Sectors........................................... 9 6. The General Environment and Outside Influences................................................. 9 7. Oil Refining Sector -

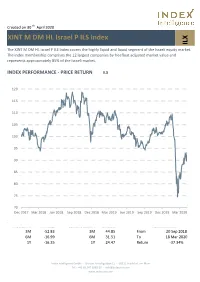

ILX XINT M DM HL Israel P ILS Index

Created on 30 th April 2020 XINT M DM HL Israel P ILS Index ILX The XINT M DM HL Israel P ILS Index covers the highly liquid and liquid segment of the Israeli equity market. The index membership comprises the 12 largest companies by freefloat adjusted market value and represents approximately 85% of the Israeli market. INDEX PERFORMANCE - PRICE RETURN ILX 120 115 110 105 100 95 90 85 80 75 70 Dec 2017 Mar 2018 Jun 2018 Sep 2018 Dec 2018 Mar 2019 Jun 2019 Sep 2019 Dec 2019 Mar 2020 Index Return % annualised Standard Deviation % annualised Maximum Drawdown 3M -52.83 3M 44.85 From 20 Sep 2018 6M -16.99 6M 31.51 To 18 Mar 2020 1Y -16.35 1Y 24.47 Return -37.34% Index Intelligence GmbH - Grosser Hirschgraben 15 - 60311 Frankfurt am Main Tel.: +49 69 247 5583 50 - [email protected] www.index-int.com TOP 10 Largest Constituents FFMV million Weight Industry Sector Check Point Software Technologies Ltd 17.07% 4,471,198 17.07% Technology Teva Pharmaceutical Industries Ltd 15.55% 4,072,206 15.55% Health Care Nice Ltd 13.77% 3,605,623 13.77% Technology Bank Leumi Le Israel BM 10.57% 2,769,635 10.57% Banks Bank Hapoalim BM 9.74% 2,551,239 9.74% Banks Wix.com Ltd 8.43% 2,206,957 8.43% Technology Israel Discount Bank Ltd 5.05% 1,323,487 5.05% Banks CyberArk Software Ltd 4.94% 1,294,068 4.94% Technology Elbit Systems Ltd 4.40% 1,152,520 4.40% Industrial Goods & Services Mizrahi Tefahot Bank Ltd 3.86% 1,010,693 3.86% Banks Total 24,457,627 93.37% This information has been prepared by Index Intelligence GmbH (“IIG”). -

State of Illinois State Universities Retirement System

State of Illinois State Universities Retirement System Compliance Examination For the Year Ended June 30, 2018 Performed as Special Assistant Auditors for the Auditor General, State of Illinois State Universities Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2018 Table of Contents Schedule Page(s) State Universities Retirement System Officials 1 Management Assertion Letter 2 Compliance Report Summary 3 Independent Accountant’s Report on State Compliance, on Internal Control Over Compliance, and on Supplementary Information for State Compliance Purposes 5 Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 9 Schedule of Findings Current Findings – State Compliance 11 Prior Findings Not Repeated 14 Financial Statement Report The System’s financial statement report for the year ended June 30, 2018, which includes the Independent Auditor’s Report, Management Discussion and Analysis, Basic Financial Statements and Notes to the Basic Financial Statements, Required Supplementary Information Other than Management Discussion and Analysis, Supplementary Information, and the Independent Auditor’s Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Basic Financial Statements performed in accordance with Government Auditing Standards has been issued separately. Supplementary Information for -

Partner Communications Reports the Appointment of a Director

PARTNER COMMUNICATIONS REPORTS THE APPOINTMENT OF A DIRECTOR Rosh Ha’ayin, Israel, May 5, 2015 - Partner Communications Company Ltd. ("Partner" or "the Company") (NASDAQ and TASE: PTNR), a leading Israeli mobile communications operator, reports that the Company's Board of Directors approved on April 29, 2015 the appointment of Mr. Yehuda Saban as a member to the Company's Board of Directors. Mr. Yehuda Saban was nominated by the court appointed receiver with respect to most of Scailex Corporation Ltd.'s shares in the Company. In accordance with the Company's Articles of Association and applicable law, Mr. Yehuda Saban shall serve in office until the Coming Annual General Meeting of shareholders. Mr. Saban served as Vice President Economics & Regulation and FLNG (Floating Liquefied Natural Gas) manager at Delek Drilling & Avner oil exploration. Mr. Saban holds a B.A. in Economics & Business Management "Gradual with Honors" and an M.B.A specializing in Financing, both from the Hebrew University in Jerusalem. Mr.Yehuda Saban has a deep understanding of the telecommunications field from his term as Manager of the Telecommunications and Tourism Unit in the Budgets Department of the Ministry of Finance, from where he retired in September 2011 and as an active partner in the Hayek Committee that dealt with formulating a policy in the fixed line field. 1 Forward-Looking Statements This press release includes forward-looking statements, as this term is defined in Section 27A of the US Securities Act of 1933, as amended, Section 21E of the US Securities Exchange Act of 1934, as amended, and the safe-harbor provisions of the US Private Securities Litigation Reform Act of 1995. -

Israeli Catalyst Census Report Was Written and Edited in Accordance with the Research Methods and Professional Advice of Catalyst Inc

The Strauss Group and the Israel Women's Network are proud to present: THE ISRAELI CATALYST REPORT WOMEN LEADING BUSINESS The Third Israeli Census Report 2012 Women's Representation in the TA-100 Companies March 2013 Diversity is an Opportunity Table of Contents Foreword 3 Executive summary 4 Part A: The 2012 Catalyst Census 1. Main findings – the 2012 Catalyst Census on women's representation in TA-100 companies 5 2. Introduction 8 3. Background, goals and methodology 9 4. Detailed findings – women on boards of directors 10 4.1 Women on boards of directors 10 4.2 Chairperson of the board positions held by women 11 4.3 Companies according to the number of women on the board of directors 11 4.4 Membership of more than one board of directors – gender comparison 12 4.5 Women on the board of directors by industry 13 4.6 International comparison – women on boards of directors 14 4.7 International comparison – companies with at least one woman on the board of directors 15 4.8 Summary – women on boards of directors 15 5. Detailed findings – women in top executive positions 16 5.1 Women in top executiVe positions 16 5.2 Chief ExecutiVe Officer positions held by women 16 5.3 Companies according to the number of women in top executiVe positions 17 5.4 Women in top executiVe positions by industry 18 5.5 International comparison – women in top executiVe positions 19 6. Annexes 19 6.1 Census size 19 6.2 2011 Census data for comparison: ranking of companies with 25% and more of women on the board of directors and in management 20 Part B: Accompanying research – the Talent Index 1. -

Holy Land Investment Fund

HOLY LAND INVESTMENT FUND Bond Street Mercantile Spring 2020 1 A balanced fund which invests in Israel-related equities and bonds Equity investments are focused on large cap, publicly traded, Israeli or Israel-related companies primarily in the areas of: Oil and gas Financial Services Technology Real Estate Infrastructure Bonds RRSP, RRIF and TFSA eligible HOLY LAND INVESTMENT FUND 2 OIL AND GAS 9,5%% BONDS 0% FINANCIALS 35.51% CASH 9.126% TECHNOLOGY 24.14% OTHER 9.252% OIL AND GAS FINANCIALS TECHNOLOGY REAL ESTATE 11.69% REAL ESTATE BONDS CASH ► PORTFOLIO OTHER COMPOSITION OTHER OIL AND SPRING 2020 10% CASH GAS 5% 15% BONDS 5% REAL ESTATE FINANCIALS 12% 28% TECHNOLOGY 25% 3 HOLY LAND INVESTMENT FUND OUR TOP 15 HOLDINGS INCLUDE: • Azrieli Group • Delek Drilling • HaPoalim • Nice • Bank Discount • Delek Group • Housing Corp. • Solaredge Technologies • Bank Leumi • Elbit • International F&F • United Mizrahi Bank • Checkpoint Software • Elektra Israel Ltd • Matrix 4 TASE has consistently outperformed the TSX over the HLIF has retained some of Israel’s best fund managers past 1, 3, 5 and 10 years HLIF has just concluded 88 months of excellent returns, Investing in Israel is an excellent diversification strategy averaging 13.5% annual return (after fees) during this time Israel’s economy is booming in almost every sector There is an excellent opportunity to “Buy Israel” as the Israeli market is still considerably underpriced relative to all major Western markets HLIF is a balanced fund and is RRSP and TFSA eligible HOLY LAND INVESTMENT FUND SUMMARY 5 Bond Street Mercantile offers an excellent way to diversify your investments. -

Class Actions Against Banks Under the New Israeli Law on Class Actions

CLASS ACTIONS AGAINST BANKS UNDER THE NEW ISRAELI LAW ON CLASS ACTIONS * DR. RUTH PLATO SHINAR I. Introduction....................................................................256 II. Causes of Action for Class Actions Against Banks ....... 259 III. The Representative Filing The Action ........................... 264 IV. The Conditions for Certification of a Class Action....... 265 V. Conclusion .................................................................... 281 * Dr. Ruth Plato Shinar is the Senior Lecturer and Director of the Center for Banking Law, Netanya Academic College, Israel. The author wishes to thank the Van Calker Foundation and the Swiss Institute of Comparative law for their generous support of the research for this article, which was principally conducted at the Swiss Institute of Comparative Law in Lausanne, Switzerland during the summer of 2006. 2007 CLASS ACTIONS AGAINST BANKS IN ISRAEL 256 I. INTRODUCTION In March 2006, Israel enacted a modern and far-reaching Class Action Law1 (the “Class Action Law”) to regulate class action suits in a centralized and exhaustive manner. Prior to the law’s enactment, class actions in Israel were common in various fields,2 including banking. The basis for class actions against banks was the Banking (Service to Customer) Law (“the Banking Law”), which contained a chapter on class actions. However, the new Class Action Law abolished this chapter, as well as all other laws concerning Class Actions in different fields, and today the arrangement of class actions is concentrated in -

Tamar Petroleum Ltd

Tamar Petroleum Ltd. Annual Report 2018 Table of Contents Chapter A Description of the Company's Business Chapter B Board of Directors Report for the year ended December 31, 2018 Chapter C Financial Statements as of December 31, 2018 Chapter D Additional Details regarding the Company Chapter E Annual Report on Effectiveness of Internal Control over Financial Reporting and Disclosure Tamar Petroleum Ltd. Chapter A Description of the Company's Business A-1 This report is a translation of Tamar Petroleum Ltd.'s Hebrew-language Description of the Company's Business, and is prepared solely for convenience purposes. Please note that the Hebrew version constitutes the binding version, and in the event of any discrepancy, the Hebrew version shall prevail. Chapter A – Description of the Company's Business 1. Description of the General Development of the Company’s Business1 1.1 Tamar Petroleum Ltd. (the "Company") was incorporated on November 4, 2015 as a private company limited by shares under the Companies Law, 5759-1999 (the "Companies Law"). The Company’s name was changed to its current name on May 21, 2017. 1.2 Pursuant to Israeli Government Resolution No. 476 from August 16, 2015 (which was readopted by the Government with certain changes on May 22, 2016) regarding "a framework for the increase of the natural gas quantity produced from the ‘Tamar’ natural gas field and the rapid development of the natural gas fields ‘Leviathan’, ‘Karish’ and ‘Tanin’ and other natural gas fields" (the "Framework" or the "Gas Framework"), the Company entered