EY's Attractiveness Survey

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

International Organizations

INTERNATIONAL ORGANIZATIONS EUROPEAN SPACE AGENCY (E.S.A.) Headquarters: 8–10 Rue Mario Nikis, 75738 Paris Cedex 15, France phone 011–33–1–5369–7654, fax 011–33–1–5369–7560 Director General.—Johann-Dietrich Woerner. Member Countries: Austria Hungary Romania Belgium Ireland Spain Denmark Italy Sweden Estonia Luxembourg Switzerland Finland Netherlands United Kingdom France Norway Germany Poland Czech Republic Greece Portugal Associate Member Countries.—Slovenia. Cooperative Agreement.—Canada. European Space Operations Center (ESOC), Robert-Bosch-Str. 5, D–64293 Darmstadt, Germany, phone 011–49–6151–900, fax 011–49–6151–90495. European Space Research and Technology Center (ESTEC), Keplerlaan 1, NL–2201, AZ Noordwijk, ZH, The Netherlands, phone 011–31–71–565–6565, Telex: 844–39098, fax 011–31–71–565–6040. European Space Research Institute (ESRIN), Via Galileo Galilei, Casella Postale 64, 00044 Frascati, Italy, phone 011–39–6–94–18–01, fax 011–39–6–9418–0280. European Space Astronomy Centre (ESAC), P.O. Box, E–28691 Villanueva de la Can˜ada, Madrid, Spain, phone 011–34 91 813 11 00, fax: 011–34 91 813 11 39. European Astronaut Centre (EAC), Linder Hoehe, 51147 Cologne, Germany, phone 011– 49–220360–010, fax 011–49–2203–60–1103. European Centre for Space Applications and Telecommunications (ECSAT), Atlas Building, Harwell Science & Innovation Campus, Didcot, Oxfordshire, OX11 0QX, United Kingdom, phone 011–44 1235 567900. European Space Agency Washington Office (EWO), 1201 F Street, NW., Suite 470, Wash- ington, DC 20004. Head of Office.—Micheline Tabache (202) 488–4158, [email protected]. INTER-AMERICAN DEFENSE BOARD 2600 16th Street, NW., 20441, phone (202) 939–6041, fax 319–2791 Chairman.—General de Brigada DEM Luis Rodrı´guez Bucio, Me´xico. -

U.S. Optimism on Namibia Losing Credibility

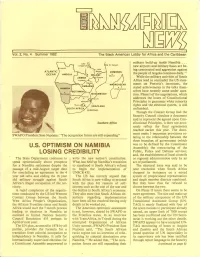

Vol. 2, No. 4 Summer 1982 The Black American Lobby for Africa and the Caribbean military build-up inside Namibia ... new airports and military bases are be~ ing constructed and aggression against COMOROS the people of Angola continues daily.'' Mo~o~ While the military activities of South Africa tend to contradict the US state ments on Pretoria's intentions, the M(JADAGASfAR stated achievements in the talks them ananvo selves have recently come under ques tion. Phase I of the negotiations, which addresses the issues of Constitutional Principles to guarantee white minority rights and the electoral system, is still unfinished. Though the Contact Group had the Security Council circulate a document said to represent the agreed upon Con Southern A/rica stitutional Principles, it does not accu rately reflect the final agreements .._....... reached earlier this year. The docu ment omits 3 important provisions re SWAPO President Sam Nujoma: ''The occupation forces are still expanding'' lating to the relationship between the three branches of government (which was to be defined by the Constituent U.S. OPTIMISM ON NAMIBIA Assembly); the restructuring of the LOSING CREDIBILITY Public, Police and Defense services; and, the establishment of local councils The State Department continues to write the new nation's constitution. or regional administration only by an speak optimistically about prospects What has held up Namibia's transition act of parliament. for a Namibia settlement despite the to statehood is South Africa's refusal The electoral issue was said to be passage of a mid-August target date to begin the implementation of near resolution when South Africa for concluding an agreement in the 4 UNSCR435. -

Living Philanthropic Values: Maintaining a “Listening Ear”

2015 Global Philanthropy Forum Conference This book includes transcripts from the plenary sessions and keynote conversations of the 2015 Global Philanthropy Forum Conference. The statements made and views expressed are solely those of the authors and do not necessarily reflect the views of GPF, its participants, the World Affairs Council of Northern California or any of its funders. Prior to publication, the authors were given the opportunity to review their remarks. Some have made minor adjustments. In general, we have sought to preserve the tone of these panels to give the reader a sense of the Conference. The Conference would not have been possible without the support of our partners and members listed below, as well as the dedication of the wonderful team at the World Affairs Council. Special thanks go to the GPF team — Suzy Antounian, Britt-Marie Alm, Pearl Darko, Brett Dobbs, Sylvia Hacaj, Ashlee Rea, Sawako Sonoyama, and Nicole Wood — for their work and dedication to the GPF, its community and its mission. FOUNDATION PARTNERS NoVo Foundation Margaret A. Cargill Foundation The David & Lucile Packard Horace W. Goldsmith Foundation Foundation Skoll Foundation SUPPORTING MEMBERS Skoll Global Threats Fund Citi Foundation International Finance Corporation Dangote Foundation The World Bank Ford Foundation The Leona M. and Harry B. Helmsley MEMBERS Charitable Trust AbbVie Conrad N. Hilton Foundation Anonymous Humanity United The Aspen Institute Inter-American Development Bank Mr. & Mrs. William H. Draper III Maja Kristin Omidyar Network John D. and Catherine T. MacArthur Salesforce.com Foundation Foundation Sall Family Foundation Charles Stewart Mott Foundation Waggener Edstrom Communications Newman’s Own Foundation The Global Philanthropy Forum is a project of the World Affairs Council of Northern California. -

World Economic Forum on Africa

World Economic Forum on Africa List of Participants As of 7 April 2014 Cape Town, South Africa, 8-10 May 2013 Jon Aarons Senior Managing Director FTI Consulting United Kingdom Muhammad Programme Manager Center for Democracy and Egypt Abdelrehem Social Peace Studies Khalid Abdulla Chief Executive Officer Sekunjalo Investments Ltd South Africa Asanga Executive Director Lakshman Kadirgamar Sri Lanka Abeyagoonasekera Institute for International Relations and Strategic Studies Mahmoud Aboud Capacity Development Coordinator, Frontline Maternal and Child Health Empowerment Project, Japan International Cooperation Agency (JICA), Sudan Fatima Haram Acyl Commissioner for Trade and Industry, African Union, Addis Ababa Jean-Paul Adam Minister of Foreign Affairs of the Seychelles Tawia Esi Director, Ghana Legal Affairs Newmont Ghana Gold Ltd Ghana Addo-Ashong Adekeye Adebajo Executive Director The Centre for Conflict South Africa Resolution Akinwumi Ayodeji Minister of Agriculture and Rural Adesina Development of Nigeria Tosin Adewuyi Managing Director and Senior Country JPMorgan Nigeria Officer, Nigeria Olufemi Adeyemo Group Chief Financial Officer Oando Plc Nigeria Olusegun Aganga Minister of Industry, Trade and Investment of Nigeria Vikram Agarwal Vice-President, Procurement Unilever Singapore Anant Agarwal President edX USA Pascal K. Agboyibor Managing Partner Orrick Herrington & Sutcliffe France Aigboje Managing Director Access Bank Plc Nigeria Aig-Imoukhuede Wadia Ait Hamza Manager, Public Affairs Rabat School of Governance Morocco & Economics -

Transformation

IFC AnnualIFC Report 2020 Transformation Transformation Annual Report 2020 CONTENTS Letter from the IFC Board 2 Letter from David Malpass, World Bank Group President 4 Letter from Philippe Le Houérou, IFC Chief Executive Officer 8 Our Management Team 13 STRATEGY IN ACTION 14 IFC Year in Review 38 FY20 Financial Highlights 40 FY20 Operational Highlights 41 World Bank Group 2020 Summary Results 44 COUNTRY STORIES 48 Creating Markets 50 Supporting Growth 60 Driving Sustainability 70 ABOUT US 78 Our Purpose 79 Measuring Up 89 Our People & Practices 97 Additional information is available on IFC’s Annual Report 2020 website: www.ifc.org/AnnualReport. Cover: The COVID-19 crisis transformed the world as we know it, exacting a massive toll on everyone, but especially the world’s poorest and most vulnerable. Over the last four years, IFC has also undergone a transformation. As a result of these changes, we are now far better equipped to help lay the seeds of a more resilient, inclusive, and sustainable recovery. For developing countries, such an outcome could be truly transformative. IFC — a member of the World Bank Group — is the largest global development institution focused on the private sector in emerging markets. We work in more than 100 countries, using our capital, expertise, and influence to create markets and opportunities in developing countries. In fiscal year 2020, we invested $22 billion in private companies and financial institutions in developing countries, leveraging the power of the private sector to end extreme poverty and boost shared prosperity. For more information, visit www.ifc.org. IFC ANNUAL REPORT 2020 1 LETTER FROM THE IFC BOARD IFC BOARD We are facing one of the most challenging times address the drivers and impacts of FCV and in for development since the creation of the World strengthening resilience, with a focus on the most Bank in 1944. -

Bank and MIGA New Boards.Xlsx

Page 1 of 2 MULTILATERAL INVESTMENT GUARANTEE AGENCY MIGA DIRECTORS AND ALTERNATES Director Alternate Elected by the votes of the 6 largest shareholders: Erik BETHEL (Vacant) United States Hervé DE VILLEROCHÉ Pierre-Olivier CHOTARD France Richard MONTGOMERY David KINDER United Kingdom Yingming YANG Minwen ZHANG China Masanori YOSHIDA Kenichi NISHIKATA Japan Juergen ZATTLER Claus Michael HAPPE Germany Director Alternate Elected by the votes of: Hesham Fahad ALOGEEL Abdulmuhsen Saad ALKHALAF Saudi Arabia (Saudi Arabia) (Saudi Arabia) Rodrigo CARRIEDO HARO Fernando JIMENEZ Costa Rica Mexico (Mexico) (Spain) El Salvador Nicaragua Guatemala Spain Honduras Venezuela, Republica Bolivariana de Koen DAVIDSE Roman KACHUR Armenia Macedonia, former Yugoslav Republic of (Netherlands) (Ukraine) Bosnia and Herzegovina Moldova Bulgaria Montenegro Croatia Netherlands Cyprus Romania Georgia Ukraine Israel Adrian FERNANDEZ Daniel PIERINI Argentina Paraguay (Uruguay) (Argentina) Bolivia Peru Chile Uruguay Nathalie FRANCKEN Guenther SCHOENLEITNER Austria Kosovo (Belgium) (Austria) Belarus Luxembourg Belgium Slovak Republic Czech Republic Slovenia Hungary Turkey Werner GRUBER Katarzyna ZAJDEL-KUROWSKA Azerbaijan Switzerland (Switzerland) (Poland) Kazakhstan Tajikistan Kyrgyz Republic Turkmenistan Poland Uzbekistán Serbia Merza HASAN Ragui EL-ETREBY Bahrain Libya (Kuwait) (Egypt) Egypt, Arab Republic of Maldives Iraq Oman Jordan Qatar Kuwait United Arab Emirates Lebanon Yemen, Republic of Christine HOGAN Donna Oretha HARRIS Antigua and Barbuda Guyana (Canada) -

Page 1 of 3 Corporate Secretariat 05/04/2020 MULTILATERAL

Page 1 of 3 MULTILATERAL INVESTMENT GUARANTEE AGENCY DIRECTORS AND ALTERNATES Executive Director Alternate Elected by the votes of the 6 largest shareholders: Arnaud BUISSÉ Pierre-Olivier CHOTARD France Richard MONTGOMERY David Stephen KINDER United Kingdom DJ NORDQUIST VACANT United States Yingming YANG Minwen ZHANG China Masanori YOSHIDA Ryosuke FUJII Japan Juergen Karl ZATTLER Nikolai PUTSCHER Germany Executive Director Alternate Elected by the votes of: VACANT Elsa Patriarca AGUSTIN Brazil Panama (Philippines) Colombia Philippines Dominican Suriname Republic Trinidad and Ecuador Tobago Haiti Hesham ALOGEEL Abdulmuhsen Saad ALKHALAF Saudi Arabia (Saudi Arabia) (Saudi Arabia) Jorge Alejandro CHÁVEZ-PRESA Fernando JIMENEZ Mexico (Mexico) (Spain) Costa Rica Nicaragua El Salvador Spain Guatemala Venezuela, Honduras Republica Bolivariana de Koen DAVIDSE Florin VODITA Armenia Israel (Netherlands) (Romania) Bosnia and Moldova Herzegovina Montenegro Bulgaria Netherlands Croatia Romania Cyprus Ukraine Georgia Adrian FERNANDEZ VACANT Argentina Paraguay (Uruguay) Bolivia Peru Chile Uruguay Nathalie FRANCKEN Guenther SCHOENLEITNER Austria Kosovo (Belgium) (Austria) Belarus Luxembourg Belgium Slovak Republic Czech Republic Slovenia Hungary Turkey Corporate Secretariat 05/04/2020 Page 2 of 3 Werner GRUBER Katarzyna ZAJDEL-KUROWSKA Azerbaijan Switzerland (Switzerland) (Poland) Kazakhstan Tajikistan Kyrgyz Republic Turkmenistan Poland Uzbekistan Serbia Geir H. HAARDE Antero KLEMOLA Denmark Latvia (Iceland) (Finland) Estonia Lithuania Finland Norway -

Trailblazers PORTRAITS of FEMALE BUSINESS LEADERSHIP in EMERGING and FRONTIER MARKETS

Trailblazers PORTRAITS OF FEMALE BUSINESS LEADERSHIP IN EMERGING AND FRONTIER MARKETS Groundbreakers, Market Makers, Value Creators IN PARTNERSHIP WITH © 2019 International Finance Corporation. All rights reserved 2121 Pennsylvania Avenue, NW Washington DC, 20433 USA Internet: ifc.org The material in this work is copyrighted. Copying and/or transmitting portions or all of this work without permission may be a violation of applicable law. IFC encourages dissemination of its work and will normally grant permission to reproduce portions of the work promptly, and when the reproduction is for educational and non-commercial purposes, without a fee, subject to such attributions and notices as we may reasonably require. IFC does not guarantee the accuracy, reliability or completeness of the content included in this work, or for the conclusions or judgments described herein, and accepts no responsibility or liability for any omissions or errors (including, without limitation, typographical errors and technical errors) in the content whatsoever or for reliance thereon. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries. The findings, interpretations, and conclusions expressed in this volume do not necessarily reflect the views of the Executive Directors of The World Bank or the governments they represent. The contents of this work are intended for general informational purposes only and are not intended to constitute legal, securities, or investment advice, an opinion regarding the appropriateness of any investment, or a solicitation of any type. -

Multilateral Investment Guarantee Agency

Page 1 of 2 MULTILATERAL INVESTMENT GUARANTEE AGENCY DIRECTORS AND ALTERNATES Executive Director Alternate Elected by the votes of the 6 largest sharholders: Hervé de VILLEROCHÉ Benoit CATZARAS France Kazuhiko KOGUCHI Hideyuki URATA Japan Melanie ROBINSON David Stephen KINDER United Kingdom (VACANT) Erik BETHEL United States Yingming YANG Minwen ZHANG China Juergen ZATTLER Claus HAPPE Germany Executive Director Alternate Elected by the votes of: Khalid ALKHUDAIRY Turki ALMUTAIRI Saudi Arabia (Saudi Arabia) (Saudi Arabia) Jason ALLFORD Hoe Jeong KIM Australia Palau (Australia) (Korea, Republic of) Cambodia Papua New Guinea Korea, Republic of Samoa Micronesia, Federated States of Solomon Islands Mongolia Vanuatu New Zealand Seydou BOUDA Jean-Claude TCHATCHOUANG Benin Gabon (Burkina Faso) (Cameroon) Burkina Faso Guinea Cabo Verde Guinea-Bissau Cameroon Madagascar Central African Republic Mali Chad Mauritania Comoros Mauritius Congo, Democratic Republic of Niger Congo, Republic of Sao Tome and Principe Cote d'Ivoire Senegal Djibouti Togo Equatorial Guinea Omar BOUGARA Shahid Ashraf TARAR Afghanistan Morocco (Algeria) (Pakistan) Algeria Pakistan Ghana Tunisia Iran, Islamic Republic of Andrew N. BVUMBE Anne KABAGAMBE Botswana Rwanda (Zimbabwe) (Uganda) Burundi Seychelles+ Eritrea Sierra Leone Ethiopia South Sudan Gambia, The Sudan Kenya Swaziland Lesotho Tanzania Liberia Uganda Malawi Zambia Mozambique Zimbabwe Namibia + Otaviano CANUTO Diana QUINTERO Brazil Panama (Brazil) (Colombia) Colombia Philippines Dominican Republic Suriname + Ecuador -

Letter to the World Bank President

Letter to World Bank President and Executive Directors calling for more action on climate change 18 October 2019 Mr. David Malpass, President, World Bank Group, 1818 H St., NW Washington, DC 20433 Dear President Malpass: The signs of the unfolding climate emergency are evident: record-breaking forest fires in the Brazilian Amazon and Cerrado biomes; ice-melt in the Arctic; devastating flooding in Mozambique and South Asia; and unprecedented and deadly heatwaves across Europe in just the past year. World leaders and institutions have a responsibility to act now to stop the climate catastrophe. Instead of helping countries make the transition out of fossil fuels, the World Bank Group (WBG), from 2014 to 2018 alone, has facilitated fossil fuel development in 45 countries, either through project finance or development policy finance and technical assistance according to data gathered by environmental group, urgewald, from the World Bank website. During this period, the WBG provided over $12 billion in project finance for 88 fossil fuel projects in 38 countries. In addition, the WBG assisted the development of fossil fuels through policy programs in at least 28 countries, including the development of coal in six countries. Given this reality, plus the fundamental threat that climate change poses to the Bank’s mission, we call on the World Bank to play a leading role among MDBs by committing to end all support for fossil fuels by the end of 2020, and signal the immediate shift to a carbon neutral world that is necessary to stabilize the global climate. This shift should be accompanied by increased investments in renewable energy access, particularly in SubSaharan Africa and South Asia, where access rates to electricity and clean cooking remain low. -

Page 1 of 3 * Not a Member of IFC. + Not a Member of IDA. Corporate

Page 1 of 3 INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL FINANCE CORPORATION INTERNATIONAL DEVELOPMENT ASSOCIATION EXECUTIVE DIRECTORS AND ALTERNATES Executive Director Alternate Appointed by: Arnaud BUISSÉ Pierre-Olivier CHOTARD France Richard MONTGOMERY David Stephen KINDER United Kingdom DJ NORDQUIST VACANT United States Yingming YANG Minwen ZHANG China Masanori YOSHIDA Kenichi NISHIKATA Japan Juergen Karl ZATTLER Nikolai PUTSCHER Germany Executive Director Alternate Elected by the votes of: VACANT Elsa Patriarca AGUSTIN Brazil Panama (Philippines) Colombia Philippines Dominican Suriname+ Republic Trinidad and Ecuador Tobago Haiti Hesham ALOGEEL Abdulmuhsen Saad ALKHALAF Saudi Arabia (Saudi Arabia) (Saudi Arabia) Jorge Alejandro CHÁVEZ-PRESA Fernando JIMENEZ Mexico (Mexico) (Spain) Costa Rica Nicaragua El Salvador Spain Guatemala Venezuela, Honduras Republica Bolivariana de+ Koen DAVIDSE Florin VODITA Armenia Moldova (Netherlands) (Romania) Bosnia and Montenegro Herzegovina Netherlands Bulgaria+ North Croatia Macedonia*+ Cyprus Romania Georgia Ukraine Israel Adrian FERNANDEZ Cecilia NAHÓN Argentina Paraguay (Uruguay) (Argentina) Bolivia Peru Chile Uruguay+ Werner GRUBER Katarzyna ZAJDEL-KUROWSKA Azerbaijan Switzerland (Switzerland) (Poland) Kazakhstan Tajikistan Kyrgyz Republic Turkmenistan+ Poland Uzbekistan Serbia * Not a member of IFC. Corporate Secretariat + Not a member of IDA. 05/04/2020 Page 2 of 3 Geir H. HAARDE Antero KLEMOLA Denmark Latvia (Iceland) (Finland) Estonia Lithuania Finland Norway Iceland -

Interim Report 2020 Africa Group 1 Constituency

INTERIM REPORT 2020 AFRICA GROUP 1 CONSTITUENCY ANNE N. KABAGAMBE EXECUTIVE DIRECTOR April 2020 | 73428 Table of Contents Acronyms and abbreviations ....................................................................................................... 3 Message from the Executive Director .......................................................................................... 5 Map of Africa Group 1 Constituency Countries ............................................................................ 9 Executive Summary .....................................................................................................................11 PART 1. Think-Piece | Driving Structural Change and Economic Transformation In Africa ......... 17 Introduction ..................................................................................................................18 What is economic transformation? ...............................................................................19 Promoting structural change and economic transformation ....................................... 22 Getting the basics right for transformation | The first-order conditions ...................... 23 Getting the basics right for transformation | The second-order conditions ................. 26 Getting the basics right for transformation | The third-order conditions ..................... 28 Conclusion .................................................................................................................. 33 PART 2. Selected Policy Issues and Updates ............................................................................37