March 17, 2017 To: Related Commercial Portfolio Ltd. RE: Value

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

READING INTERNATIONAL, INC. (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K þ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 or ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from _______ to ______ Commission File No. 1-8625 READING INTERNATIONAL, INC. (Exact name of registrant as specified in its charter) Nevada 95-3885184 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification Number) 5995 Sepulveda Boulevard, Suite 300 Culver City, CA 90230 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including Area Code: (213) 235-2240 Securities Registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol Name of each exchange on which registered Class A Nonvoting Common Stock, $0.01 par value RDI NASDAQ Class B Voting Common Stock, $0.01 par value RDIB NASDAQ Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No þ Indicate by check mark whether registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the preceding 12 months (or for shorter period than the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Harlem Transportation Study

3.0 LAND USE AND ZONING Zoning The city is divided into three basic zoning districts: residential (R), commercial (C), and manufacturing (M). The three basic categories are further subdivided into lower, medium, and higher density residential, commercial and manufacturing districts. Development within these districts is regulated by use, building size, and parking regulations. Here is a brief description of the three basic zoning districts according to the Zoning Handbook: Residential District (R) In New York City, there are ten standard residential districts, R1 through R10. The numbers refer to the permitted density (R1 having the lowest density and R10 the highest) and other controls such as required parking. A second letter or number signifies additional controls are required in certain districts. R1 and R2 districts allow only detached single-family residences and certain community facilities. The R3-2 through R10 districts accept all types of dwelling units and community facilities and are distinguished by differing bulk and density, height and setback, parking, and lot coverage or open space requirements. Commercial District (C) The commercial districts reflect the full range of commercial activity in the city from local retail and service establishmentsDRAFT to high density, shopping, entertainment and office uses. There are eight basic commercial districts where two (C1 and C2 districts) are designed to serve local needs, one district (C4) is for shopping centers outside the central business district, two (C5 and C6 districts) are for the central business districts which embrace the office, retail, and commercial functions that serve the city and region, and three (C3, C7, and C8 districts) are designed for special purposes (waterfront activity, large commercial amusement parks and heavy repair services). -

Union Square 14Th Street District Vision Plan

UNION SQUARE 14TH STREET DISTRICT VISION PLAN DESIGN PARTNER JANUARY 2021 In dedication to the Union Square-14th Street community, and all who contributed to the Visioning process. This is just the beginning. We look forward to future engagement with our neighborhood and agency partners as we move forward in our planning, programming, and design initiatives to bring this vision to reality. Lynne Brown William Abramson Jennifer Falk Ed Janoff President + Co-Chair Co-Chair Executive Director Deputy Director CONTENTS Preface 7 Introduction 8 Union Square: Past, Present and Future 15 The Vision 31 Vision Goals Major Projects Park Infrastructure Streetscape Toolkit Implementation 93 Conclusion 102 Appendix 107 Community Engagement Transit Considerations 4 UNION SQUARE PARTNERSHIP | VISIONING PLAN EXECUTIVE SUMMARY 5 6 UNION SQUARE PARTNERSHIP | VISIONING PLAN Photo: Jane Kratochvil A NEW ERA FOR UNION SQUARE DEAR FRIENDS, For 45 years, the Union Square Partnership has been improving the neighborhood for our 75,000 residents, 150,000 daily workers, and millions of annual visitors. Our efforts in sanitation, security, horticulture, and placemaking have sustained and accelerated growth for decades. But our neighborhood’s growth is not over. With more than 1 million square feet of planned development underway, it is time to re-invest for tomorrow. The projects and programs detailed in the Union Square-14th Street District Vision Plan will not just focus on the neighborhood’s competitive advantage but continue to make the area a resource for all New Yorkers for generations to come. This plan is a jumping-off point for collaboration with our constituents. At its center, the vision proposes a dramatic 33% expansion of public space. -

The Retail Pulse Updates & Trends

May 2013 The Retail Pulse Updates & Trends Real estate investment services May 2013 New York City’s Strong Investor Demand Defi es Property Sales Volatility Tourists from around the world are not the only ones interested in New York City’s retail offerings, real estate investors have been scouring the City to BUY retail properties boosting sales volume at the end of 2012. Yet despite the numerous anecdotal stories confi rming how New York’s economy is thriving, the retail property sales sta- tistics were disappointing in the fi rst quarter of 2013. Volume fell signifi cantly, but this was expected given the rush at the end of 2012 to close deals before the capital gains tax increased as it did at the 11th hour. As per Chairman and CEO, Peter Hauspurg, “To no one’s surprise, sales volume fell in the fi rst quarter but investor inter- est has been strong. Because prices are climbing every day, more sellers are bringing properties to the market. While we will not see the same fourth quarter 2012 volume in the next quarter or two, the statistics will start to refl ect the high demand we are seeing in the market.” This issue of Eastern Consolidated’s Retail Pulse report will review every statistic pertaining to the retail industry in New York City. The fi ndings are compelling and show why New York City has retained its title of “Retail Capital of the World:” — Retail property sales volume declined in early 2013, but this was expected given the surge at the end of 2012. -

Download Report (PDF)

Dear Community Partners, “Challenging” seems both an accurate and yet inadequate word to describe the last year as we confronted - as a nation and as a community - a series of crises from public health and economic dislocation to reckonings over racial justice and equity. Through it all, the Union Square Partnership played an important role in seeking to keep residents and businesses informed and connected, guiding them to resources, and working with relevant city agencies to support the district. What started as a COVID response turned to a COVID recovery agenda and by the fall of 2020, we released the #USQNext District Recovery Plan. This plan was aimed at accelerating the resumption of business activity and introducing quality of life improvements to continue the upward trend the neighborhood was enjoying prior to the pandemic. UNION SQUARE-14TH STREET HAS DEMONSTRATED INCREDIBLE RESILIENCE OVER THE PAST YEAR, AND THE DISTRICT IS WELL-POSITIONED TO REBOUND This year’s Annual Report is organized around the five pillars of the recovery plan, including reemphasizing core services like sanitation, beautification, and public safety coordination, bolstering our marketing efforts, and pursuing exciting new projects in the bold District Vision Plan released this past January. Most important, we would like to take a moment to express gratitude for the tireless dedication of frontline workers and essential service providers who kept our city functioning and to acknowledge the loss of loved ones that has affected so many. We hold each of you in our hearts. We are committed to championing the district’s recovery With spring blooming in our area, vaccinations on the rise, and life through the vital programs outlined in our #USQNext District Recovery Plan. -

Design Forecast 2016 from the Co-Ceos

Design Forecast 2016 From the Co-CEOs We always look ahead. For 2016’s Design Forecast, we challenged ourselves to look out 10 years. Design shapes the future of human experience to create a better world. This credo is the basis of our Design Forecast. For 2016, we asked our global teams to consider how people will live, work, and play in the cities of 2025. Their insights will give our clients an insider view of the issues design will confront in the next decade. Finding opportunities requires insight and imagination. Our newly opened Shanghai Tower speaks to how we help our clients reframe the present to meet the needs of tomorrow. Design is how we do it. It makes insight actionable, creates meaningful innovation, and calls a thriving future into being. Andy Cohen, FAIA, IIDA Diane Hoskins, FAIA, IIDA, LEED AP Co-CEO Co-CEO Shanghai Tower, Shanghai on the cover: The Tower at PNC Plaza, Pittsburgh ii 1 Gensler Design Forecast 2016 Metatrends Embracing shaping the our iHumanity. 1 Digital will be such an integral part of daily life that world of 2025. we’ll leverage it much more fully. We’ll accept how it interacts with us, consciously feeding its data streams to make our lives better. Our iHumanity Looking across our markets, will be a shared, global phenomenon, but different we see six metatrends that will locales and generations will give it their own spin. transform how we live, work, and play in the next decade. Leading “smarter” lives. 2 We’ll live in a “made” environment, not just a “built” one. -

Stephen Ison and Jon Shaw

PARKING ISSUES AND POLICIES TRANSPORT AND SUSTAINABILITY Series Editors: Stephen Ison and Jon Shaw Recent Volumes: Volume 1: Cycling and Sustainability Volume 2: Transport and Climate Change Volume 3: Sustainable Transport for Chinese Cities Volume 4: Sustainable Aviation Futures TRANSPORT AND SUSTAINABILITY VOLUME 5 PARKING ISSUES AND POLICIES EDITED BY STEPHEN ISON Transport Studies Group, Loughborough University, UK CORINNE MULLEY Institute of Transport and Logistics Studies, The University of Sydney Business School, Sydney, Australia United Kingdom À North America À Japan India À Malaysia À China Emerald Group Publishing Limited Howard House, Wagon Lane, Bingley BD16 1WA, UK First edition 2014 Copyright r 2014 Emerald Group Publishing Limited Reprints and permission service Contact: [email protected] No part of this book may be reproduced, stored in a retrieval system, transmitted in any form or by any means electronic, mechanical, photocopying, recording or otherwise without either the prior written permission of the publisher or a licence permitting restricted copying issued in the UK by The Copyright Licensing Agency and in the USA by The Copyright Clearance Center. Any opinions expressed in the chapters are those of the authors. Whilst Emerald makes every effort to ensure the quality and accuracy of its content, Emerald makes no representation implied or otherwise, as to the chapters’ suitability and application and disclaims any warranties, express or implied, to their use. British Library Cataloguing in Publication Data A catalogue record for this book is available from the British Library ISBN: 978-1-78350-919-5 ISSN: 2044-9941 (Series) ISOQAR certified Management System, awarded to Emerald for adherence to Environmental standard ISO 14001:2004. -

CITYLAND NEW FILINGS & DECISIONS | August 2015

CITYLAND NEW FILINGS & DECISIONS | August 2015 CITY PLANNING PIPELINE New Applications Filed with DCP — August 1 to August 31, 2015 APPLICANT PROJECT/ADDRESS DESCRIPTION ULURP NO. REPResentatiVE ZONING TEXT AND MAP AMENDMENTS 385 Gold Property Investors 141 Willoughby Street, BK Private application for a zoning map amendment, 160029 ZRK; Greenberg Traurig street demapping, and a zoning text change to 160030 ZMK facilitate a new 310,065 SF mixed-use development, including 62,013 SF of retail and office, and 248,052 SF of residential (270 dwelling units) including 74,416 SF of affordable residential (81 DUs). Gleitman Realty Associates Seagirt Blvd at Fernside Place, Zoning change to facilitate construction of an 160033ZMQ Holland & Knight QN approximately 5,629 SF, one-story commercial building with 14 parking spaces and to facilitate construction of a five-story, approximately 31,850 SF residential building with 29 spaces and zoning change to establish a C1-3 commercial overlay. SPECIAL PERMITS/OTHER ACTIONS Hamilton Plaza Associates 1-37 12th Street, BK Applicants would like to amend the conditions of the 780389BZSK Sheldon Lobel Goya special permit to allow non-warehouse and non-office uses on the third floor of the building to allow them to build a physical culture establishment. Buffalo Ave. Realty Associates 170 Buffalo Avenue, BK St. Mary’s Hospital Nursing Home special permit to 160028ZSK Eric Palatnik allow for the repurposing of the former St. Mary’s Hospital as a Use Group 3 nursing home. Hamilton Plaza Associates 1-37 12th Street, BK Certification by the Chairperson, pursuant to ZR 62- 160026ZCK Sheldon Lobel 811 waterfront public access and visual corridors. -

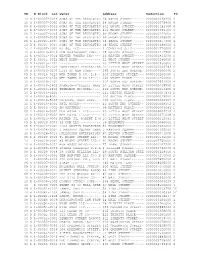

Store # Phone Number Store Shopping Center/Mall Address City ST Zip District Number 318 (907) 522-1254 Gamestop Dimond Center 80

Store # Phone Number Store Shopping Center/Mall Address City ST Zip District Number 318 (907) 522-1254 GameStop Dimond Center 800 East Dimond Boulevard #3-118 Anchorage AK 99515 665 1703 (907) 272-7341 GameStop Anchorage 5th Ave. Mall 320 W. 5th Ave, Suite 172 Anchorage AK 99501 665 6139 (907) 332-0000 GameStop Tikahtnu Commons 11118 N. Muldoon Rd. ste. 165 Anchorage AK 99504 665 6803 (907) 868-1688 GameStop Elmendorf AFB 5800 Westover Dr. Elmendorf AK 99506 75 1833 (907) 474-4550 GameStop Bentley Mall 32 College Rd. Fairbanks AK 99701 665 3219 (907) 456-5700 GameStop & Movies, Too Fairbanks Center 419 Merhar Avenue Suite A Fairbanks AK 99701 665 6140 (907) 357-5775 GameStop Cottonwood Creek Place 1867 E. George Parks Hwy Wasilla AK 99654 665 5601 (205) 621-3131 GameStop Colonial Promenade Alabaster 300 Colonial Prom Pkwy, #3100 Alabaster AL 35007 701 3915 (256) 233-3167 GameStop French Farm Pavillions 229 French Farm Blvd. Unit M Athens AL 35611 705 2989 (256) 538-2397 GameStop Attalia Plaza 977 Gilbert Ferry Rd. SE Attalla AL 35954 705 4115 (334) 887-0333 GameStop Colonial University Village 1627-28a Opelika Rd Auburn AL 36830 707 3917 (205) 425-4985 GameStop Colonial Promenade Tannehill 4933 Promenade Parkway, Suite 147 Bessemer AL 35022 701 1595 (205) 661-6010 GameStop Trussville S/C 5964 Chalkville Mountain Rd Birmingham AL 35235 700 3431 (205) 836-4717 GameStop Roebuck Center 9256 Parkway East, Suite C Birmingham AL 35206 700 3534 (205) 788-4035 GameStop & Movies, Too Five Pointes West S/C 2239 Bessemer Rd., Suite 14 Birmingham AL 35208 700 3693 (205) 957-2600 GameStop The Shops at Eastwood 1632 Montclair Blvd. -

East Harlem, Manhattan (September 2016)

PLACE-BASED COMMUNITY BROWNFIELD PLANNING FOUNDATION REPORT ON EXISTING CONDITIONS EAST HARLEM, MANHATTAN FINAL SEPTEMBER 2016 BILL deBLASIO MAYOR DANIEL C. WALSH, Ph.D. DIRECTOR Mayor’s Office of Environmental Remediation This document was prepared by the New York City Department of City Planning for the New York City Mayor’s Office of Environmental Remediation and the New York State Department of State with state funds provided through the Brownfield Opportunity Areas Program. CONTENTS PURPOSE 4 EXECUTIVE SUMMARY 5 PART ONE Geography and Land Use 10 Demographic and Economic Profile 28 Recent Public Initiatives and Private Investments 35 PART TWO Environmental Conditions 41 Potential Strategic Sites 43 KEY FINDINGS AND NEXT STEPS 57 APPENDIX 58 PURPOSE This existing conditions foundation report was commissioned by the New York City Mayor’s Office of Environmental Remediation (OER) to help community members and community-based organizations (CBO’s) conduct place-based planning for revitalization of vacant and underutilized brownfield properties. Place- based planning by community groups is supported by OER under the NYC Place-Based Community Brownfield Planning Program and by the New York State Department of State in the Brownfield Opportunity Area Program. To advance implementation of plans, OER provides financial and technical assistance to CBO’s for cleanup and redevelopment of brownfield properties and seeks to help people foster greater health and well-being in their neighborhoods. Brownfields are vacant or underutilized properties where environmental pollution has deterred investment and redevelopment. Pollution introduces many risks to land development and often causes community and private developers to pass over these properties, especially in low-income neighborhoods where land values may be depressed and insufficient to cover added cleanup costs. -

Actions on Applications in 2010

YR B Block Lot Owner Address Reduction TC 10 R 1-00007-0029 SONS OF THE REVOLUTIO 26 WATER STREET~~~~~~ 0000000048200 4 10 R 1-00007-0030 SONS OF THE REVOLUTIO 24 WATER STREET~~~~~~ 0000000075400 4 09 R 1-00007-0033 SONS OF THE REVOLUTIO 101 BROAD STREET~~~~~ 0000000183700 4 10 R 1-00007-0033 SONS OF THE REVOLUTIO 101 BROAD STREET~~~~~ 0000000386500 4 09 R 1-00007-0035 SONS OF THE REVOLUTIO 99 BROAD STREET~~~~~~ 0000000244000 4 10 R 1-00007-0035 SONS OF THE REVOLUTIO 99 BROAD STREET~~~~~~ 0000000305500 4 09 R 1-00007-0037 SONS OF THE REVOLUTIO 58 PEARL STREET~~~~~~ 0000000277800 4 10 R 1-00007-0037 SONS OF THE REVOLUTIO 58 PEARL STREET~~~~~~ 0000000389000 4 10 R 1-00007-1001 BZ 66, LLC~~~~~~~~~~~ 1 COENTIES SLIP~~~~~~ 0000001770000 4 10 R 1-00010-0019 JMW RESTAURANT CORP~~ 25 BRIDGE STREET~~~~~ 0000000217500 4 10 R 1-00011-0014 BEAVER TOWERS INC~~~~ 26 BEAVER STREET~~~~~ 0000000813000 2 10 R 1-00015-0022 WEST EDEN~~~~~~~~~~~~ 21 WEST STREET~~~~~~~ 0000000280000 2 09 R 1-00015-1101 ~~~~~~~~~~~~~~~~~~~~~ 20 LITTLE WEST STREET 0000000950000 4 10 R 1-00015-1102 TWENTYWEST PROPERTIES 20 LITTLE WEST STREET 0000000003783 2 09 R 1-00016-0100 CITY OF NEW YORK~~~~~ 345 SOUTH END AVENUE~ 0000005600000 2 09 R 1-00016-0120 WFP TOWER A CO. L.P.~ 200 LIBERTY STREET~~~ 0000010200000 4 09 R 1-00016-0150 WFP TOWER D CO LP~~~~ 250 VESEY PLACE~~~~~~ 0000010250000 4 10 R 1-00016-1301 ~~~~~~~~~~~~~~~~~~~~~ 102 NORTH END AVENUE~ 0000007661000 4 10 R 1-00016-1402 SCANLON-O'KELLY, MARY 30 LITTLE WEST STREET 0000000018585 2 09 R 1-00016-2200 ZEMELMAN MICHAEL~~~~~ -

Exploring Union Square's Landmarked Buildings

Town & Village — Thursday, October 8, 2015 — 5 Exploring Union Square’s landmarked buildings By Wally Dobelis egant original carriage house been the Daryl Roth Theatre is a gracious horse carriage In this year of many an- (1854), which has served as for several years. Note the house (1904) built by Van niversaries of political, civil residence, office, cafe and magnificent four columns. A Tassel and Kearney, a Beaux rights and social significance, now houses a restaurant, The few doors east at 109-111 East Arts survivor from the Gilded we should also celebrate House. Farther east, across 15th Street, the former Cen- Era. Originally a Horse Auc- those of direct impact on Irving Place at 129 East 17th tury Association Clubhouse tion Mart and subsequently helping New York maintain Street, is a red six-story seem- (1869) was another Gilded artist Frank Stella’s studio, its historic past, letting us ingly oversize town house, Age phenomenon. Union it now serves as work space preserve our architectural known to be the first apart- for various dance compa- and social accomplishments. ment house in New York City. nies. Farther south at 34 1/2 The Landmarks Law of 1965 It was designed by Napoleon East 12th Street, west of was prompted by widespread Le Brun of Metropolitan Life (Guardian Life), Broadway in a dark group popular anger over the loss tower frame and still serves originally named of houses (1855), was one of of Pennsylvania Station, the original purpose. Farther the first NYC all-girls’ public and the Union Square Com- east at 141 East 17th near the Germania Life, Photos courtesy of the Union Square Community Coalition schools.