Republic of Croatia

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Press Release Changes to the List of Euro Foreign Exchange Reference

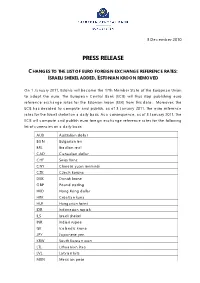

3 December 2010 PRESS RELEASE CHANGES TO THE LIST OF EURO FOREIGN EXCHANGE REFERENCE RATES: ISRAELI SHEKEL ADDED, ESTONIAN KROON REMOVED On 1 January 2011, Estonia will become the 17th Member State of the European Union to adopt the euro. The European Central Bank (ECB) will thus stop publishing euro reference exchange rates for the Estonian kroon (EEK) from this date. Moreover, the ECB has decided to compute and publish, as of 3 January 2011, the euro reference rates for the Israeli shekel on a daily basis. As a consequence, as of 3 January 2011, the ECB will compute and publish euro foreign exchange reference rates for the following list of currencies on a daily basis: AUD Australian dollar BGN Bulgarian lev BRL Brazilian real CAD Canadian dollar CHF Swiss franc CNY Chinese yuan renminbi CZK Czech koruna DKK Danish krone GBP Pound sterling HKD Hong Kong dollar HRK Croatian kuna HUF Hungarian forint IDR Indonesian rupiah ILS Israeli shekel INR Indian rupee ISK Icelandic krona JPY Japanese yen KRW South Korean won LTL Lithuanian litas LVL Latvian lats MXN Mexican peso 2 MYR Malaysian ringgit NOK Norwegian krone NZD New Zealand dollar PHP Philippine peso PLN Polish zloty RON New Romanian leu RUB Russian rouble SEK Swedish krona SGD Singapore dollar THB Thai baht TRY New Turkish lira USD US dollar ZAR South African rand The current procedure for the computation and publication of the foreign exchange reference rates will also apply to the currency that is to be added to the list: The reference rates are based on the daily concertation procedure between central banks within and outside the European System of Central Banks, which normally takes place at 2.15 p.m. -

Shipbuilding

CODEN BRODBA 59(4)307-430(2008) »ASOPIS BRODOGRADNJE I BRODOGRA–EVNE INDUSTRIJE JOURNAL OF NAVAL ARCHITECTURE AND SHIPBUILDING INDUSTRY SHIPBUILDING Prosinac Godina Broj Zagreb • December 2008 • Volume 59 • Number 4 SADRÆAJ CONTENTS Naslovna stranica (Front cover): Brodogradiliπte Viktor Lenac, Rijeka OSVRTI, POTICAJI COMMENTS, INITIATIVES 310 G. RUKAVINA Koliko brodogradnja stoji hrvatske porezne obveznike What is the Cost of the Shipbuilding Industry obveznike i kako bi bilo hrvatskim poreznim to the Croatian Taxpayers, and What Would obveznicima bez brodogradnje It BeLike for the Croatian Taxpayers Without the Shipbuilding Industry 315 *** Isporuke hrvatskih brodogradiliπta Croatian Shipyards’ Deliveries ZNANOST SCIENCE 323 P. »UDINA Projektne procedure i matematiËki Design Procedure and Mathematical modeli u projektiranju brodova za tekuÊe Models in the Concept Design of Tankers i rasute terete and Bulk Carriers Izvorni znanstveni rad Original scientific paper 340 D. OBREJA et al. Parametarsko ljuljanje pri glavnoj rezonanciji Parametric Rolling at Main Resonance Izvorni znanstveni rad Original scientific paper 348 R. GRUBI©IΔ Viπenamjenski brod za dizanje teπkih An 18 680 dwt Multipurpose/Heavy et al. tereta nosivosti 18 680 dwt, I dio Lift Cargo Vessel, Part I StruËni rad Professional paper AKTUALNOSTI CURRENT TOPICS AND NEWS 365 *** Vijesti iz Hrvatske News from Croatia 377 Z. BARI©IΔ Robert ©kifiÊ: Viktor Lenac posluje Robert ©kifiÊ: A Rising Business u znaku uzlaznog trenda Trend in Viktor Lenac 383 J. PRPIΔ-OR©IΔ Razgovor s profesorom You should never say something about O.M. Faltinsenom, Centre for Ships something that you don’t know anything about and Ocean Structures, Trondheim, Norveπka Interview with Professor O.M. -

Exchange Market Pressure on the Croatian Kuna

EXCHANGE MARKET PRESSURE ON THE CROATIAN KUNA Srđan Tatomir* Professional article** Institute of Public Finance, Zagreb and UDC 336.748(497.5) University of Amsterdam JEL F31 Abstract Currency crises exert strong pressure on currencies often causing costly economic adjustment. A measure of exchange market pressure (EMP) gauges the severity of such tensions. Measuring EMP is important for monetary authorities that manage exchange rates. It is also relevant in academic research that studies currency crises. A precise EMP measure is therefore important and this paper re-examines the measurement of EMP on the Croatian kuna. It improves it by considering intervention data and thresholds that ac- count for the EMP distribution. It also tests the robustness of weights. A discussion of the results demonstrates a modest improvement over the previous measure and concludes that the new EMP on the Croatian kuna should be used in future research. Key words: exchange market pressure, currency crisis, Croatia 1 Introduction In an era of increasing globalization and economic interdependence, fixed and pegged exchange rate regimes are ever more exposed to the danger of currency crises. Integrated financial markets have enabled speculators to execute attacks more swiftly and deliver devastating blows to individual economies. They occur when there is an abnormally large international excess supply of a currency which forces monetary authorities to take strong counter-measures (Weymark, 1998). The EMS crisis of 1992/93 and the Asian crisis of 1997/98 are prominent historical examples. Recently, though, the financial crisis has led to severe pressure on the Hungarian forint and the Icelandic kronor, demonstrating how pressure in the foreign exchange market may cause costly economic adjustment. -

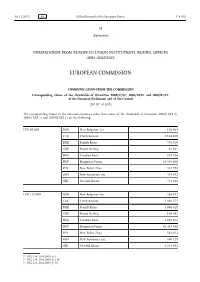

Corresponding Values of the Thresholds of Directives 2004/17/EC, 2004/18/EC and 2009/81/EC, of the European Parliament and of the Council (2015/C 418/01)

16.12.2015 EN Official Journal of the European Union C 418/1 II (Information) INFORMATION FROM EUROPEAN UNION INSTITUTIONS, BODIES, OFFICES AND AGENCIES EUROPEAN COMMISSION COMMUNICATION FROM THE COMMISSION Corresponding values of the thresholds of Directives 2004/17/EC, 2004/18/EC and 2009/81/EC, of the European Parliament and of the Council (2015/C 418/01) The corresponding values in the national currencies other than euros of the thresholds of Directives 2004/17/EC (1), 2004/18/EC (2) and 2009/81/EC (3) are the following: EUR 80 000 BGN New Bulgarian Lev 156 464 CZK Czech Koruna 2 184 400 DKK Danish Krone 596 520 GBP Pound Sterling 62 842 HRK Croatian Kuna 610 024 HUF Hungarian Forint 24 549 600 PLN New Polish Zloty 333 992 RON New Romanian Leu 355 632 SEK Swedish Krona 731 224 EUR 135 000 BGN New Bulgarian Lev 264 033 CZK Czech Koruna 3 686 175 DKK Danish Krone 1 006 628 GBP Pound Sterling 106 047 HRK Croatian Kuna 1 029 416 HUF Hungarian Forint 41 427 450 PLN New Polish Zloty 563 612 RON New Romanian Leu 600 129 SEK Swedish Krona 1 233 941 (1) OJ L 134, 30.4.2004, p. 1. (2) OJ L 134, 30.4.2004, p. 114. (3) OJ L 216, 20.8.2009, p. 76. C 418/2 EN Official Journal of the European Union 16.12.2015 EUR 209 000 BGN New Bulgarian Lev 408 762 CZK Czech Koruna 5 706 745 DKK Danish Krone 1 558 409 GBP Pound Sterling 164 176 HRK Croatian Kuna 1 593 688 HUF Hungarian Forint 64 135 830 PLN New Polish Zloty 872 554 RON New Romanian Leu 929 089 SEK Swedish Krona 1 910 323 EUR 418 000 BGN New Bulgarian Lev 817 524 CZK Czech Koruna 11 413 790 DKK -

Economic Growth in Croatia: What Have We Learned?

Report No. 48879- HR Public Disclosure Authorized CROATIA Croatia’s EU Convergence Report: Reaching and Sustaining Higher Rates of Economic Growth Public Disclosure Authorized (In two volumes) Vol. II: Full Report June 2009 Public Disclosure Authorized Europe and Central Asia Region Document of the World Bank Public Disclosure Authorized CURRENCY AND EQUIVALENT UNITS Currency Unit=Croatian kuna US$1 =HRK 5.6102 (As of April 30, 2009) FISCAL YEAR January 1 – December 31` WEIGHTS AND MEASURES Metric System ACRONYMS AND ABBREVIATIONS AAE Agency for Adult Education IEC International Electrotechnical Commission ADR Alternative Dispute Resolution ILAC International Laboratory Accreditation Cooperation AVET Agency for Vocational Education and ILO International Labor Organization Training CA Company Act IP Intellectual Property CARDS Community Assistance for Reconstruction, ISO International Organization for Standardization Development and Stabilization CEE Central and Eastern Europe OECD Organization for Economic Cooperation and Development CENLE European Committee for Electrotechnical LLL Life Long Learning C Standardization CES ??? MoSES Ministry of Science, Education and Sports CGPM General conference on Weights and MoELE Ministry of Economy, Labor & Measures Entrepreneurship ECA Europe and Central Asia MS&T Mathematics, Science & Technology FDI Foreign Direct Investment FE Fixed Effects NIS National Innovation System FINA Financial Agency PMR Product Market Regulation GDP Gross Domestic Product PPS Purchasing Power Standards GFCF Gross Fixed -

Local Government Unit Borrowing in Croatia: Opportunities and Constraints

LOCAL GOVERNMENT UNIT BORROWING IN CROATIA: OPPORTUNITIES AND CONSTRAINTS Anto Bajo Occasional Paper No. 20 October 2004 © Institute of Public Finance 2004 2 LOCAL GOVERNMENT UNIT BORROWING IN CROATIA: OPPORTUNITIES AND CONSTRAINTS1 Abstract The paper analyses the practice and basic features of local government unit borrowing in Croatia from 1997 to 2003. Local government units still rely on classical forms of loans as a form of security for resources for financing capital projects and there is little incentive for the issue of local government bonds. The borrowing conditions laid down are not a good basis on which to develop a local debt market or for facilitating local government borrowing. One of the reasons is also the dominant role of the city of Zagreb, which should be excluded from the establishment of budgetary restrictions on the borrowing of the other local government units in Croatia. Subsidised loans to local government units via the government financial institutions have been in some periods more expensive than via the commercial banks, and it is necessary to carry out a review of their role in the financing of local government unit capital projects. In any analysis of the borrowing and the size of the debt of local government units it is necessary to include the categories of financial assets as a better indicator of solvency and ability to repay debt. The article draws attention to a potential hold-up in the implementation of fiscal decentralisation, because local government units are investing some of their funds in the financial assets (shares and equity) of local utility firms. -

LÄNDERBERICHT Konrad-Adenauer-Stiftung E.V

LÄNDERBERICHT Konrad-Adenauer-Stiftung e.V. KROATIEN DR. MICHAEL A. LANGE 9. September 2015 Kandidaten positionieren und www.kas.de/kroatien Wahlbündnisse formieren sich PARLAMENTSWAHLEN IN KROATIEN Die Debatte um die Festsetzung des Wahl- überzeugt zeigt, auf, sich nicht weiter in termins für die anstehenden Parlaments- seinem Parteizentrale zu verkriechen son- wahlen in Kroatien kommt nicht zur Ruhe. dern sich endlich einer öffentlichen TV- Der kroatische Ministerpräsident Milano- Debatte zu stellen. vic unterstrich jüngst noch einmal, dass die aktuelle Legislaturperiode erst am 22. Aufbauend auf der Ankündigung eines be- Dezember endet und dass das kroatische vorstehenden Abschlusses einer Koalitions- Parlament in der verfassungsgemäß vor- vereinbarung seiner Partei mit den drei bis- gegebenen Frist aufgelöst werden wird, herigen Koalitionspartnern: der „Croatian sodass die Staatspräsidentin dann den People’s Party (HNS )“, der „Croatian Pensi- genauen Termin der Wahlen innerhalb der oners' Party ( HSU )“, der „Croatian Labou- 30-60 Tagefrist festlegen kann. Nach der rists ( HL )“ sowie der neuen „Autochthonous überraschenden Einberufung einer außer- Croatian Peasants’ Party ( AHSS )“, zeigte er ordentlichen Parlamentssitzung für den 8. sich optimistisch, was den Abschluss einer -11. September gehen viele politische Be- solchen Vereinbarung mit der sich diesbe- obachter nun davon aus, dass das Parla- züglich weiterhin zurückhaltenden „Istrian ment sich noch vor Ende September auf- Democratic Congress ( IDS )“ angeht. Nur lösen und damit der Staatspräsidentin den zusammen mit der IDS meint Milanovic Weg ebnen wird, einen Wahltermin zwi- Kroatien auf dem richtigen Weg halten zu schen Ende Oktober (25.) und Mitte No- können und bot deshalb allen politischen vember (1., 8. und 15.) zu bestimmen. Da Partnern bereits sichere Listenplätze an. -

2007 London Ministerial Conference

Bologna Process - Conference of Ministers Responsible for Higher Education 17 - 18 May 2007 The Queen Elizabeth II Conference Centre Name Country/Organisation Genc Pollo Albania (Head of Delegation) Edmond Cane Albania Adriana Gjonaj Albania Shezai Rrokaj Albania Valbona Sanxhaktari Albania Aleksander Xhuvani Albania Juli Minoves Andorra (Head of Delegation) Dorian Bishop Andorra Enric M. Garcia Lopez Andorra Miquel Nicolau Vila Andorra Aitor Osorio Andorra Maria Pubill Armengol Andorra Levon Mkrtchyan Armenia (Head of Delegation) Ara Avetisyan Armenia Nerses Gevorgyan Armenia Artusha Ghukasyan Armenia Hranush Hakobyan Armenia Johannes Hahn Austria (Head of Delegation) Christoph Badelt Austria Friedrich Faulhammer Austria Georg Hufgard Austria Esther Hutfless Austria Thomas Obernosterer Austria Barbara Weitgruber Austria Misir Mardanov Azerbaijan (Head of Delegation) Azad Akhundov Azerbaijan Aygun Huseynova Azerbaijan Yusif Mammadov Azerbaijan Ilham Mustafayev Azerbaijan Frank Vandenbroucke Belgium (Head of Delegation) Marie-Dominique Simonet Belgium (Head of Delegation) Bernard Devlamminck Belgium Xavier Dupont Belgium Chantal Kaufmann Belgium Amélie Louwette Belgium Marie-Anne Persoons Belgium Hans Plancke Belgium Bernard Rentier Belgium Benjamin Van Camp Belgium Noël Vercruysse Belgium Sredoje Novic Bosnia and Herzegovina (Head of Delegation) Meliha Alic Bosnia and Herzegovina Dragana Lukic-Domuz Bosnia and Herzegovina Anton Kasipovic Bosnia and Herzegovina Zenan Sabanac Bosnia and Herzegovina Stanko Stanic Bosnia and Herzegovina Vania -

B. 1. Prva Bodovna Skupina

B. 1. PRVA BODOVNA SKUPINA B. 1. 1. Metodološki predmeti Zdravko Lacković: M1. STRUKTURA, METODIKA I FUNKCIONIRANJE ZNANSTVENOG RADA Broj sati: Ukupno 26 (predavanja 5, seminari + rasprave “oko okruglog stola”/ 10, vježbe 6, “on-line” vježbe 5); BODOVI: 4,5 Sadržaj predmeta: Znanost o znanosti i osebujnosti medicinskih znanosti. Sociologija i ekonomika znanosti. Znanost i drugi oblici čovjekove kulture. Povijesna uvjetovanost medicinskih znanosti. Logičke zakonitosti znanstvenog rada i najčešće pogreške Etička pitanja i dileme znanstvenih istraživanja u medicini. Organizacija znanstvenog rada u Republici Hrvatskoj. Organizacija znanstvenog rada u farmaceutskoj industriji. Znanstvena karijera u medicini: od diplome do HAZU; magisteriji, doktorati, znanstvena zvanja, vanjska usavršavanja. Složenost bibliotečno informacijskog sustava znanosti i kako naći znanstvene podatke. Kako pohraniti i obraditi znanstvene podatke. Od izuma do patenta i primjene; osebujnosti zaštite intelektualnog vlasništva u medicini. Znanstveni članak: od pisanja do objave u časopisu. Znanost i javnost. Prosudba vrsnoće znanstvenog djela. Suradnici u nastavi. Prof. dr. sc. Biserka Belicza, prof. dr. sc. Jadranka Božikov, mr. sc. Zoran Buneta, ing. Božidar Ferek-Petrić, prof. dr. sc. Slaven Letica, prof. dr. sc. Zdenko Kovač, prof. Darko Marinović, prof. dr. sc. Ana Marušić, doc. dr. sc. Jelka Petrak, prof. dr. sc. Mladen Petrovečki, akademik prof. dr. sc. Vlatko Silobrčić, prof.. dr. sc. Melita Šalković-Petrišić, Sudionici “okruglih stolova” do sada (promjenljivo): prof. dr. sc. Nada Čikeš, dr. Czaba Dohoczky, dr. Veljko Đorđević, prof. dr. sc. Radovan Fuchs, prof. dr. sc. Stjepan Gamulin, Stanko Govedić, Blanka Jergović mr. sc. Gabrijela Kobrehal, prof. dr. sc. Ivica Kostović, dr. sc. Krunoslav Kovačević, prof. dr. sc. Slobodan Lang, mr. sc. Gorjana Lazarevski, prof. -

On Underrepresented and Vulnerable Groups of Students: Contributions to the Enhancement of the Social Dimension of Higher Education in Croatia

On Underrepresented and Vulnerable Groups of Students: Contributions to the Enhancement of the Social Dimension of Higher Education in Croatia Authors: Saša Puzić Nikola Baketa Branislava Baranović Margareta Gregurović Teo Matković Mirta Mornar Iva Odak Josip Šabić IMPRESSUM Title: On Underrepresented and Vulnerable Groups of Students: Contributions to the Enhancement of the Social Dimension of Higher Education in Croatia Publisher: Ministry of Science and Education, Institute for Social Research in Zagreb For the publisher: prof Radovan Fuchs, PhD, Minister Boris Jokić, PhD, Director Reviewers: Martina Gaisch, PhD, Higher Education Researcher at FH Upper Austria and National Expert for the Social Dimension in Austria Martin Unger, Head of Higher Education Research Group at IHS Vienna Editor: Saša Puzić Translator: Lida Lamza Graphic design: ILI NET d.o.o. ISBN: 978-953-8374-06-7, ISBN: 978-953-6218-87-5 Europan Commission's support for the development of this publication does not represent support for the content, which solely reflects the opinions of the authors. The Commission cannot be held responsible for the usage of information contained within. On Underrepresented and Vulnerable Groups of Students: Contributions to the Enhancement of the Social Dimension of Higher Education in Croatia Authors: Saša Puzić, Nikola Baketa, Branislava Baranović, Margareta Gregurović, Teo Matković, Mirta Mornar, Iva Odak and Josip Šabić Institute for Social Research in Zagreb Zagreb, 2021 Contents 1. INTRODUCTION .................. .................................................................................................................................................7 -

BUDG/CONT Delegation Visit to Croatia 22 - 25 June 2010

BUDG/CONT Delegation visit to Croatia 22 - 25 June 2010 CONTENTS 1. Programme 2. Policy Department for Budgetary Affairs: The Economic and Political Situation in Croatia 3. Country Report, Economist Intelligence Unit 4. EC Conclusions on Croatia 5. European Parliament Resolution on the Progress report on Croatia 6. IPA 2009 Commission Decision with annex 7. Overview of EC Assistance to Croatia over the period 2001-2008 DRAFT PROGRAMME Joint Delegation of the Budgetary Control Committee and Budgets Committee to CROATIA 22-25 June 2010 Participants MEPs Luigi de Magistris - Head of delegation (CONT / ALDE) Jean Pierre Audy (CONT / EPP) Tamas Deutsch (CONT / (EPP) Goran Farm (BUDG / (S&D) Monica Luisa Macovei (CONT / EPP) Theodor Stolojan (BUDG / EPP) Derek Vaughn (CONT / S&D) Secretariat of the Committee on Budgetary Control: Mr Rudolfs Verdins (Administrator) Ms Sylvana Zammit (Assistant) (Special GSM number for the days 22-25 June 2010: +32 475-75 46 68) Secretariat of the Committee on Budgets: Lucia Cojocaru (Administrator) Political group advisors Jonas Kraft (EPP) Maggie Coulthard (S&D) Dominykas Mordas (ALDE) Interpreters (Active: EN, IT, HR - Passive: FR) Fusco Maria Antonietta (IT) (Team Leader) Varesco Enrico (FR, EN) Mance Natasa (EN) Levak Potrebica Tamara (EN, HR) Maras Marija (EN, HR) Hobbs James (IT) Collins Mani Anna (FR, IT) Members' Assistants Emilie Apell (assistant to Mr Farm S&D) Ana Brinza (assistant to Mr Stolojan EPP) EC Delegation in Zagreb: Mr Paul Vandoren Head of Delegation [email protected] Mr Sandro Ciganovic [email protected] Accommodation and transport in Croatia/Zagreb: Hotel Regent Esplanade Mihanoviceva 1, 10000 Zagreb Croatia Telephone: +385-(0)1-45 66 666 Fax: +385 1 45 66050 The delegation will have a bus at its disposal in Zagreb during meeting days. -

Macedonian Historical Review 3 (2012) Македонска Историска Ревија 3 (2012) EDITORIAL BOARD

Macedonian Historical Review 3 (2012) Македонска историска ревија 3 (2012) EDITORIAL BOARD: Boban PETROVSKI, University of Ss. Cyril and Methodius, Macedonia (editor-in-chief) Nikola ŽEŽOV, University of Ss. Cyril and Methodius, Macedonia Dalibor JOVANOVSKI, University of Ss. Cyril and Methodius, Macedonia Toni FILIPOSKI, University of Ss. Cyril and Methodius, Macedonia Charles INGRAO, Purdue University, USA Bojan BALKOVEC, University of Ljubljana,Slovenia Aleksander NIKOLOV, University of Sofia, Bulgaria Đorđe BUBALO, University of Belgrade, Serbia Ivan BALTA, University of Osijek, Croatia Adrian PAPAIANI, University of Elbasan, Albania Oliver SCHMITT, University of Vienna, Austria Nikola MINOV, University of Ss. Cyril and Methodius, Macedonia (editorial board secretary) ISSN: 1857-7032 © 2012 Faculty of Philosophy, University of Ss. Cyril and Methodius, Skopje, Macedonia University of Ss. Cyril and Methodius - Skopje Faculty of Philosophy Macedonian Historical Review vol. 3 2012 Please send all articles, notes, documents and enquiries to: Macedonian Historical Review Department of History Faculty of Philosophy Bul. Krste Misirkov bb 1000 Skopje Republic of Macedonia http://mhr.fzf.ukim.edu.mk/ [email protected] TABLE OF CONTENTS 7 Nathalie DEL SOCORRO Archaic Funerary Rites in Ancient Macedonia: contribution of old excavations to present-day researches 15 Wouter VANACKER Indigenous Insurgence in the Central Balkan during the Principate 41 Valerie C. COOPER Archeological Evidence of Religious Syncretism in Thasos, Greece during the Early Christian Period 65 Diego PEIRANO Some Observations about the Form and Settings of the Basilica of Bargala 85 Denitsa PETROVA La conquête ottomane dans les Balkans, reflétée dans quelques chroniques courtes 95 Elica MANEVA Archaeology, Ethnology, or History? Vodoča Necropolis, Graves 427a and 427, the First Half of the 19th c.