Social Security Bulletin, Vol. 70, No. 3, 2010 V 111 the Future Financial Status of the Social Security Program by Stephen C

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

C H a P T E R 24 the Great Depression and the New Deal

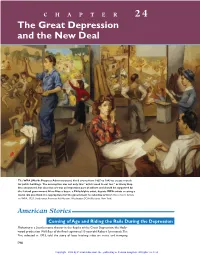

NASH.7654.CP24.p790-825.vpdf 9/23/05 3:26 PM Page 790 CHAPTER 24 The Great Depression and the New Deal The WPA (Works Progress Administration) hired artists from 1935 to 1943 to create murals for public buildings. The assumption was not only that “artists need to eat too,” as Harry Hop- kins announced, but also that art was an important part of culture and should be supported by the federal government. Here Moses Soyer, a Philadelphia artist, depicts WPA artists creating a mural. Do you think it is appropriate for the government to subsidize artists? (Moses Soyer, Artists on WPA, 1935. Smithsonian American Art Museum, Washington DC/Art Resource, New York) American Stories Coming of Age and Riding the Rails During the Depression Flickering in a Seattle movie theater in the depths of the Great Depression, the Holly- wood production Wild Boys of the Road captivated 13-year-old Robert Symmonds.The film, released in 1933, told the story of boys hitching rides on trains and tramping 790 NASH.7654.CP24.p790-825.vpdf 9/23/05 3:26 PM Page 791 CHAPTER OUTLINE around the country. It was supposed to warn teenagers of the dangers of rail riding, The Great Depression but for some it had the opposite effect. Robert, a boy from a middle-class home, al- The Depression Begins ready had a fascination with hobos. He had watched his mother give sand- Hoover and the Great Depression wiches to the transient men who sometimes knocked on the back door. He had taken to hanging around the “Hooverville” shantytown south of Economic Decline the King Street railroad station, where he would sit next to the fires and A Global Depression listen to the rail riders’ stories. -

Chapter 18: Roosevelt and the New Deal, 1933-1939

Roosevelt and the New Deal 1933–1939 Why It Matters Unlike Herbert Hoover, Franklin Delano Roosevelt was willing to employ deficit spending and greater federal regulation to revive the depressed economy. In response to his requests, Congress passed a host of new programs. Millions of people received relief to alleviate their suffering, but the New Deal did not really end the Depression. It did, however, permanently expand the federal government’s role in providing basic security for citizens. The Impact Today Certain New Deal legislation still carries great importance in American social policy. • The Social Security Act still provides retirement benefits, aid to needy groups, and unemployment and disability insurance. • The National Labor Relations Act still protects the right of workers to unionize. • Safeguards were instituted to help prevent another devastating stock market crash. • The Federal Deposit Insurance Corporation still protects bank deposits. The American Republic Since 1877 Video The Chapter 18 video, “Franklin Roosevelt and the New Deal,” describes the personal and political challenges Franklin Roosevelt faced as president. 1928 1931 • Franklin Delano • The Empire State Building 1933 Roosevelt elected opens for business • Gold standard abandoned governor of New York • Federal Emergency Relief 1929 Act and Agricultural • Great Depression begins Adjustment Act passed ▲ ▲ Hoover F. Roosevelt ▲ 1929–1933 ▲ 1933–1945 1928 1931 1934 ▼ ▼ ▼ ▼ 1930 1931 • Germany’s Nazi Party wins • German unemployment 1933 1928 107 seats in Reichstag reaches 5.6 million • Adolf Hitler appointed • Alexander Fleming German chancellor • Surrealist artist Salvador discovers penicillin Dali paints Persistence • Japan withdraws from of Memory League of Nations 550 In this Ben Shahn mural detail, New Deal planners (at right) design the town of Jersey Homesteads as a home for impoverished immigrants. -

Academic Search Complete

Academic Search Complete Pavadinimas Prenumerata nuo Prenumerata iki Metai nuo Metai iki 1 Technology times 2021-04-01 2021-12-31 20140601 20210327 2 Organization Development Review 2021-04-01 2021-12-31 20190101 3 PRESENCE: Virtual & Augmented Reality 2021-04-01 2021-12-31 20180101 4 Television Week 2021-04-01 2021-12-31 20030310 20090601 5 Virginia Declaration of Rights and Cardinal Bellarmine 2021-04-01 2021-12-31 6 U.S. News & World Report: The Report 2021-04-01 2021-12-31 20200124 7 Education Journal Review 2021-04-01 2021-12-31 20180101 8 BioCycle CONNECT 2021-04-01 2021-12-31 20200108 9 High Power Computing 2021-04-01 2021-12-31 20191001 10 Economic Review (Uzbekistan) 2021-04-01 2021-12-31 20130801 11 Civil Disobedience 2021-04-01 2021-12-31 12 Appeal to the Coloured Citizens of the World 2021-04-01 2021-12-31 13 IUP Journal of Environmental & Healthcare Law 2021-04-01 2021-12-31 14 View of the Revolution (Through Indian Eyes) 2021-04-01 2021-12-31 15 Narrative of Her Life: Mary Jemison 2021-04-01 2021-12-31 16 Follette's Platform of 1924 2021-04-01 2021-12-31 17 Dred Scott, Plaintiff in Error, v. John F. A. Sanford 2021-04-01 2021-12-31 18 U.S. News - The Civic Report 2021-04-01 2021-12-31 20180928 20200117 19 Supreme Court Cases: The Twenty-first Century (2000 - Present) 2021-04-01 2021-12-31 20 Geophysical Report 2021-04-01 2021-12-31 21 Adult Literacy 2021-04-01 2021-12-31 2000 22 Report on In-Class Variables: Fall 1987 & Fall 1992 2021-04-01 2021-12-31 2000 23 Report of investigation : the Aldrich Ames espionage case / Permanent Select Committee on Intelligence,2021-04-01 U.S. -

Social Security Fraud

Social Security Fraud In This Issue Prosecuting Social Security Number Misuse: Attacking Identity Theft at its Source ........................................................ 1 January By John K. Webb 2005 Volume 53 Using Electronic Evidence to Litigate Social Security Cases: Considering Number 1 the Implications of the Social Security Administration's New Signature Alternatives on Applications ..................................... 16 United States Department of Justice By Joseph Grow Executive Office for United States Attorneys Prosecuting Employers for Wage and Earnings Violations under the Office of Legal Education Washington, DC Social Security Act and the Internal Revenue Code .................. 23 20535 By John K. Webb Mary Beth Buchanan Director Overview of the Social Security Administration's Civil Monetary Penalty Contributors’ opinions and statements should not be Program: Applying Sections 1129 and 1140 of the Social Security Act .. 34 considered an endorsement by By Julia Chu and Jonathan Morse EOUSA for any policy, program, or service. The United States Attorneys’ Bulletin is published pursuant to 28 CFR § 0.22(b). The United States Attorneys’ Bulletin is published bi-monthly by the Executive Office for United States Attorneys, Office of Legal Education, 1620 Pendleton Street, Columbia, South Carolina 29201. Periodical postage paid at Washington, D.C. Postmaster: Send address changes to Editor, United States Attorneys’ Bulletin, Office of Legal Education, 1620 Pendleton Street, Columbia, South Carolina 29201. Managing Editor Jim Donovan Technical Editor Nancy Bowman Law Clerk Carolyn Perozzi Internet Address www.usdoj.gov/usao/ reading_room/foiamanuals. html Send article submissions to Managing Editor, United States Attorneys’ Bulletin, National Advocacy Center, Office of Legal Education, 1620 Pendleton Street, Columbia, SC 29201. Prosecuting Social Security Number Misuse: Attacking Identity Theft at its Source John K. -

Franklin Roosevelt's Advisory System: the Institutionalization of the Executive Office of the Esidentpr

University of Nebraska at Omaha DigitalCommons@UNO Student Work 7-1-1974 Franklin Roosevelt's advisory system: The institutionalization of the Executive office of the esidentPr James C. Rowling University of Nebraska at Omaha Follow this and additional works at: https://digitalcommons.unomaha.edu/studentwork Recommended Citation Rowling, James C., "Franklin Roosevelt's advisory system: The institutionalization of the Executive office of the President" (1974). Student Work. 488. https://digitalcommons.unomaha.edu/studentwork/488 This Thesis is brought to you for free and open access by DigitalCommons@UNO. It has been accepted for inclusion in Student Work by an authorized administrator of DigitalCommons@UNO. For more information, please contact [email protected]. FRANKLIN ROOSEVELT*S ADVISORY SYSTEM: THE INSTITUTIONALIZATION OF THE EXECUTIVE OFFICE OF THE PRESIDENT A Thesis Presented to the Department of Political Science and the Faculty of the Graduate College University of Nebraska at Omaha In Partial Fulfillment of the Requirements for the Degree Master of Arts by James C. Rowling July, 197^ 1 UMI Number: EP73126 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a complete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. UMI EP73126 Published by ProQuest LLC (2015). Copyright in the Dissertation held by the Author. Microform Edition © ProQuest LLC. All rights reserved. This work is protected against unauthorized copying under Title 17, United States Code ProQuest LLC. -

Historia De La OFICINA DE LA INFANCIA

Historia de la OFICINA DE LA INFANCIA Cien años al servicio de los niños y las familias de nuestra nación Índice Introducción Nacimiento de una era . 3 Progreso para los niños . 5 Capítulo 1 Cooperación Antes . 9 Ahora . 11 Capítulo 2 Ayuda a estados y tribus Antes . 13 Ahora . 16 Capítulo 3 Investigación e información Antes . 20 Ahora . 24 Capítulo 4 Difusión del mensaje Antes . 28 Ahora . 31 Capítulo 5 Liderazgo Antes . 34 Ahora . 37 Historia de la OFICINA DE LA INFANCIA Introducción Nacimiento de una era La Oficina de la Infancia, como primer organismo federal dedicado al bienestar de los niños, lleva mucho tiempo ocupándose de algunos de los problemas sociales más apremiantes que enfrenta Estados Unidos. Estos problemas han cambiado con el transcurrir de los años. En sus inicios, la oficina se ocupaba de temas como mortalidad infantil, hijos dependientes y trabajo infantil, mientras que ahora las preocupaciones principales son maltrato infantil y prevención del abandono, cuidado de crianza temporal y servicios de adopción. No obstante, los valores que subyacían a nuestro trabajo en sus primeras etapas y muchos de los métodos fundamentales a los que recurríamos para materializarlos aún perduran; incluidos cooperación, ayuda a estados y tribus, investigación y recopilación de información, campañas de sensibilización social y formación de líderes. A principios del siglo pasado, las condiciones de los niños en Estados Unidos eran muy diferentes a las de hoy. Más de uno de diez bebés no sobrevivía al primer año. Muchos niños desertaban de la escuela para ayudar a conseguir el sustento de sus familias, por lo general, trabajando en condiciones peligrosas. -

Master List of Terms and Concepts : 20 Century Topics, Emphasizing the Americas

Master List of Terms and Concepts : 20th Century Topics, Emphasizing the Americas Early 20th Century- Year 1 Unit 1 - The development of modern nations 1865-1929 (8 Weeks) “Cross of Gold” Chicago School of Architecture “Melting Pot” theory Cornelius Vanderbilt AFL Coxey’s Army Andrew Carnegie Edward Bellamy Bland-Allison Act (1878) Emma Lazarus Boss Tweed Gilded Age Carry Nation Gold bugs Gospel of Wealth Railroad Strike of 1877 Haymarket Riot (1886) Robber Barons Henry George Samuel Gompers Homestead Strike (1892) Settlement Movement Horatio Alger Sherman Antitrust Act (1890) Jacob Riis Sherman Silver Purchase Act (1890) Jane Addams Silver bugs Jay Gould Social Darwinism John D. Rockefeller Social Gospel Knights of Labor Thomas A. Edison Louis Sullivan Thomas Nast Mark Hanna U. S. v. E. C. Knight (1890) Panic of 1893 William Jennings Bryan Pendleton Act (1885) William Lloyd Wright Pullman Strike (1894) Yellow-dog contract Unit 2 - Emergence of the Americas in global affairs 1880-1929 (10 Weeks) Treaty of Kanagawa Pancho Villa “Seward’s Folly” John J. Pershing Alfred Thayer Mahan “Colossus of the North Jingoism James G. Blaine Yellow journalism Pan-Americanism William Randolph Hearst U. S. S. Maine Spanish-American War (1898) Commodore Matthew Perry De Lome Letter Commodore Dewey Remember the Maine, to Hell with Spain! Treaty of Paris (1898) Rough Riders Walter Reed Queen Liliukalani Insular Cases Emilio Aguinaldo Teller Amendment “White Man’s Burden” protectorate Anti-Imperialist League John Hay, Secretary of State Platt Amendment Boxer Rebellion Open Door Policy Teddy Roosevelt’s “Big Stick” policy Roosevelt Corollary Clayton-Bulwer Treaty Panama Canal Nationalism Gentleman’s Agreement First Battle of the Somme Treaty of Portsmouth (1905) Militarism “Dollar Diplomacy” Trench warfare Henry Cabot Lodge, Sr. -

“The National Voice” Across the Bayard and Ringo Stories

UNIVERSITY OF OKLAHOMA GRADUATE COLLEGE POPULAR FAULKNER: THE DEVELOPMENT OF “THE NATIONAL VOICE” ACROSS THE BAYARD AND RINGO STORIES A THESIS SUBMITTED TO THE GRADUATE FACULTY in partial fulfillment of the requirements for the Degree of MASTER OF ARTS By WILLIAM WILDE JANUARY VI Norman, Oklahoma 2018 POPULAR FAULKNER: THE DEVELOPMENT OF “THE NATIONAL VOICE” ACROSS THE BAYARD AND RINGO STORIES A THESIS APPROVED FOR THE DEPARTMENT OF ENGLISH BY ______________________________ Dr. James Zeigler, Chair ______________________________ Dr. Daniela Garofalo ______________________________ Dr. William Henry McDonald © Copyright by WILLIAM WILDE JANUARY VI 2018 All Rights Reserved. To Claire, as a monument to our adventure in Oklahoma. Acknowledgements This project is in many ways the culmination of everything I have done before, and thus it is necessary to acknowledge everyone I have had the pleasure to have known the past three years in the University of Oklahoma English Department: faculty, staff, and my fellow graduate students. In particular, I would like to thank both Dr. McDonald and Dr. Garofalo for not only serving on my committee, but for teaching seminars so influential that they changed the way that I viewed the world and, subsequently, my future plans. In a similar vein, I would like to thank Dr. John Burke and Dr. William Ulmer at the University of Alabama, as I would have never even been here without their part in shaping my formless undergraduate curiosity into the more disciplined inquisitiveness of a scholar. Most of all, I am indebted to my Chair, Dr. James Zeigler, who has over the past three years listened carefully to every road not taken by this work, and always provided clear, helpful feedback as well as a sense of positivity that has made all the difference in its completion. -

One Hundred Twelfth Congress of the United States of America

H. R. 3630 One Hundred Twelfth Congress of the United States of America AT THE SECOND SESSION Begun and held at the City of Washington on Tuesday, the third day of January, two thousand and twelve An Act To provide incentives for the creation of jobs, and for other purposes. Be it enacted by the Senate and House of Representatives of the United States of America in Congress assembled, SECTION 1. SHORT TITLE; TABLE OF CONTENTS. (a) SHORT TITLE.—This Act may be cited as the ‘‘Middle Class Tax Relief and Job Creation Act of 2012’’. (b) TABLE OF CONTENTS.—The table of contents for this Act is as follows: Sec. 1. Short title; table of contents. TITLE I—EXTENSION OF PAYROLL TAX REDUCTION Sec. 1001. Extension of payroll tax reduction. TITLE II—UNEMPLOYMENT BENEFIT CONTINUATION AND PROGRAM IMPROVEMENT Sec. 2001. Short title. Subtitle A—Reforms of Unemployment Compensation to Promote Work and Job Creation Sec. 2101. Consistent job search requirements. Sec. 2102. State flexibility to promote the reemployment of unemployed workers. Sec. 2103. Improving program integrity by better recovery of overpayments. Sec. 2104. Data exchange standardization for improved interoperability. Sec. 2105. Drug testing of applicants. Subtitle B—Provisions Relating To Extended Benefits Sec. 2121. Short title. Sec. 2122. Extension and modification of emergency unemployment compensation program. Sec. 2123. Temporary extension of extended benefit provisions. Sec. 2124. Additional extended unemployment benefits under the Railroad Unem- ployment Insurance Act. Subtitle C—Improving Reemployment Strategies Under the Emergency Unemployment Compensation Program Sec. 2141. Improved work search for the long-term unemployed. Sec. -

In the Beginning...An Introductory Essay by Don Wolfensberger for the Congress Project Seminar O

Congress and Social Security: In the Beginning.... An Introductory Essay By Don Wolfensberger For the Congress Project Seminar On “Congress and the Politics of Aging” Woodrow Wilson International Center for Scholars Tuesday, September 13, 2005 We put those payroll contributions there so as to give the contributors a legal, moral, and political right to collect their pensions and their unemployment benefits. With those taxes in there, no damn politician can ever scrap my social security program. --President Franklin D. Roosevelt Social Security is the third rail of American politics. Touch it and you die. –Attributed to House Speaker Thomas P. Tip O’Neill, Jr. President Franklin Delano Roosevelt is widely recognized as the father of the New Deal, including the landmark Social Security Act of 1935. Arthur M. Schlesinger, Jr., calls Roosevelt “the single national political leader to identify himself with the social insurance cause.”1 Martha Derthick says the 1935 Act “marks the founding of the welfare state in the United States.”2 The impression one gets from most histories of the depression era is that Roosevelt and his “Brain Trust” conceived the New Deal programs, sent them to Hill, and Congress dutifully and expeditiously enacted them into law with little change. However, a closer examination reveals a different picture. As Patrick Maney of the University of South Carolina tells us, “Far from being the brainchild of one person, the enduring accomplishments of the Depression decade were the products of a richly collaborative process in which FDR, presidential advisers, government bureaucrats, well- organized interest groups, grass-roots activists, and legislators all played parts.” And, Maney continues, “. -

The Second New Deal

THE SECOND NEW DEAL Chapter 12 Section 2 US History THE SECOND NEW DEAL • LAUNCHING THE SECOND NEW DEAL • MAIN IDEA – By 1935, the New Deal faced political and legal challenges, as well as growing concern that it was not ending the Depression LAUNCHING THE SECOND NEW DEAL • Roosevelt and Hopkins (head of FERA) openly supported the New Deal policies – Needed support and effective speakers to defend against opposition to policies • Economy only showed slight improvement after 2 years of Roosevelt’s policies – Even though created 2 million new jobs, nations income only half of income from 1929 LAUNCHING THE SECOND NEW DEAL • Criticism from left and right – Roosevelt got criticism from both political parties • Right wing believed expanded Fed. Gov’t at expense of states’ rights • Right had always opposed new deal, but increased by 1934 – To pay for programs used “deficit spending” and many alarmed by growing deficit in gov’t – August 1934 Business and anti-New Deal politicians created “American Liberty League” • Organize opposition to New Deal • ‘teach necessity of respect for the rights of person and property LAUNCHING THE SECOND NEW DEAL – Left also criticized New Deal for not doing enough – Wanted more gov’t intervention to shift wealth from rich to middle/poor Americans • Huey Long – He was most serious threat to New Deal – Governor of Louisiana • Improved schools, hospitals and built roads/bridges – Created a large corrupt political machine, 1930 elected to senate – Attacked rich and was a great public speaker (lots of support) – 1934 created Share Our Wealth Society and announced run for President in 1936 LAUNCHING THE SECOND NEW DEAL • Father Coughlin – Catholic Priest from Detroit with radio show • 30-45 million listeners – At first supported New Deal but wasn’t fast or radical enough – Wanted national banking system and inflated currency – 1935 organized National Union for Social Justice • Worried might become new political party LAUNCHING THE SECOND NEW DEAL • The Townsend Plan – Third challenge to Roosevelt… Francis Townsend – Wanted Fed. -

Congressional Record United States Th of America PROCEEDINGS and DEBATES of the 105 CONGRESS, SECOND SESSION

E PL UR UM IB N U U S Congressional Record United States th of America PROCEEDINGS AND DEBATES OF THE 105 CONGRESS, SECOND SESSION Vol. 144 WASHINGTON, THURSDAY, FEBRUARY 12, 1998 No. 11 House of Representatives The House met at 10 a.m. Mr. GIBBONS. Mr. Speaker, I object Herger Markey Redmond The Reverend Ronald F. Christian, Hill Martinez Regula to the vote on the ground that a Hinojosa Mascara Reyes Director, Lutheran Social Services of quorum is not present and make the Hobson Matsui Riley Fairfax, VA, offered the following pray- point of order that a quorum is not Hoekstra McCarthy (MO) Rivers er: present. Holden McCarthy (NY) Rodriguez Almighty God, Your glory is made Hooley McCollum Roemer The SPEAKER. Evidently a quorum Horn McCrery Rogan known in the heavens, and the fir- is not present. Hostettler McGovern Rogers mament declares Your handiwork. The Sergeant at Arms will notify ab- Houghton McHale Rohrabacher Hoyer McHugh Ros-Lehtinen With the signs of Your creative good- sent Members. ness all about us, we must acknowledge Hulshof McInnis Rothman The vote was taken by electronic de- Hutchinson McIntosh Roukema Your presence in our world, through vice, and there wereÐyeas 353, nays 43, Inglis McIntyre Roybal-Allard Your people, and within us all. answered ``present'' 1, not voting 33, as Istook McKeon Royce So, therefore, we pray for Your Jackson (IL) McKinney Ryun follows: mercy when our ways are stubborn or Jackson-Lee Meehan Sabo [Roll No. 14] (TX) Meek (FL) Salmon uncompromising and not at all akin to Jefferson Meeks (NY) Sanchez Your desires.