Demise and Fall of the Augustan Monetary System

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

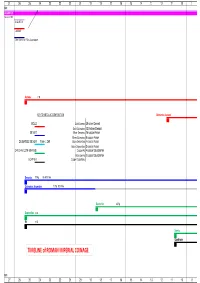

TIMELINE of ROMAN IMPERIAL COINAGE

27 26 25 24 23 22 21 20 19 18 17 16 15 14 13 12 11 10 9 B.C. AUGUSTUS 16 Jan 27 BC AUGUSTUS CAESAR Other title: e.g. Filius Augustorum Aureus 7.8g KEY TO METALLIC COMPOSITION Quinarius Aureus GOLD Gold Aureus 25 silver Denarii Gold Quinarius 12.5 silver Denarii SILVER Silver Denarius 16 copper Asses Silver Quinarius 8 copper Asses DE-BASED SILVER from c. 260 Brass Sestertius 4 copper Asses Brass Dupondius 2 copper Asses ORICHALCUM (BRASS) Copper As 4 copper Quadrantes Brass Semis 2 copper Quadrantes COPPER Copper Quadrans Denarius 3.79g 96-98% fine Quinarius Argenteus 1.73g 92% fine Sestertius 25.5g Dupondius 12.5g As 10.5g Semis Quadrans TIMELINE of ROMAN IMPERIAL COINAGE B.C. 27 26 25 24 23 22 21 20 19 18 17 16 15 14 13 12 11 10 9 8 7 6 5 4 3 2 1 1 2 3 4 5 6 7 8 9 10 11 A.D.A.D. denominational relationships relationships based on Aureus Aureus 7.8g 1 Quinarius Aureus 3.89g 2 Denarius 3.79g 25 50 Sestertius 25.4g 100 Dupondius 12.4g 200 As 10.5g 400 Semis 4.59g 800 Quadrans 3.61g 1600 8 7 6 5 4 3 2 1 1 2 3 4 5 6 7 8 91011 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 19 Aug TIBERIUS TIBERIUS Aureus 7.75g Aureus Quinarius Aureus 3.87g Quinarius Aureus Denarius 3.76g 96-98% fine Denarius Sestertius 27g Sestertius Dupondius 14.5g Dupondius As 10.9g As Semis Quadrans 3.61g Quadrans 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 TIBERIUS CALIGULA CLAUDIUS Aureus 7.75g 7.63g Quinarius Aureus 3.87g 3.85g Denarius 3.76g 96-98% fine 3.75g 98% fine Sestertius 27g 28.7g -

Agorapicbk-15.Pdf

Excavations of the Athenian Agora Picture Book No. 1s Prepared by Fred S. Kleiner Photographs by Eugene Vanderpool, Jr. Produced by The Meriden Gravure Company, Meriden, Connecticut Cover design: Coins of Gela, L. Farsuleius Mensor, and Probus Title page: Athena on a coin of Roman Athens Greek and Roman Coins in the Athenian Agora AMERICAN SCHOOL OF CLASSICAL STUDIES AT ATHENS PRINCETON, NEW JERSEY 1975 1. The Agora in the 5th century B.C. HAMMER - PUNCH ~ u= REVERSE DIE FLAN - - OBVERSE - DIE ANVIL - 2. Ancient method of minting coins. Designs were cut into two dies and hammered into a flan to produce a coin. THEATHENIAN AGORA has been more or less continuously inhabited from prehistoric times until the present day. During the American excava- tions over 75,000 coins have been found, dating from the 6th century B.c., when coins were first used in Attica, to the 20th century after Christ. These coins provide a record of the kind of money used in the Athenian market place throughout the ages. Much of this money is Athenian, but the far-flung commercial and political contacts of Athens brought all kinds of foreign currency into the area. Other Greek cities as well as the Romans, Byzantines, Franks, Venetians, and Turks have left their coins behind for the modern excavators to discover. Most of the coins found in the excavations were lost and never recovered-stamped into the earth floor of the Agora, or dropped in wells, drains, or cisterns. Consequently, almost all the Agora coins are small change bronze or copper pieces. -

The Use of Propaganda on an Augustan Denarius

Pepperdine University Pepperdine Digital Commons Featured Research Undergraduate Student Research Fall 11-2013 The Use of Propaganda on an Augustan Denarius Jens Ibsen Pepperdine University, [email protected] Melissa Miller Pepperdine University Follow this and additional works at: https://digitalcommons.pepperdine.edu/sturesearch Part of the Biblical Studies Commons, History of Religion Commons, and the Other History of Art, Architecture, and Archaeology Commons Recommended Citation Ibsen, Jens and Miller, Melissa, "The Use of Propaganda on an Augustan Denarius" (2013). Pepperdine University, Featured Research. Paper 79. https://digitalcommons.pepperdine.edu/sturesearch/79 This Research Poster is brought to you for free and open access by the Undergraduate Student Research at Pepperdine Digital Commons. It has been accepted for inclusion in Featured Research by an authorized administrator of Pepperdine Digital Commons. For more information, please contact [email protected], [email protected], [email protected]. The Use of Propaganda on an Augustan Denarius Jens Ibsen & Melissa Miller ABSTRACT Our coin is a silver denarius minted in Lugdunum (now Lyon), most likely under the reign of Augustus, the first emperor of Rome. There are factors which point to a possibility of the coin being a restitution Above: A Comparable Trajan AR Denarius(c. 98 -117 CE) issue minted under either Trajan or Hadrian, such as its pristine Source; http://tjbuggey.ancients.info/ condition, which implies a lack of use, and the similarity of symbols employed on this denarius and denarii of Trajan’s era. The coin is a prime example of Augustus’ use of propaganda inserted into Roman daily life to sell the idea of empire to a Roman people who ardently defended a long-standing tradition of republican government. -

The Roman Empire – Roman Coins Lesson 1

Year 4: The Roman Empire – Roman Coins Lesson 1 Duration 2 hours. Date: Planned by Katrina Gray for Two Temple Place, 2014 Main teaching Activities - Differentiation Plenary LO: To investigate who the Romans were and why they came Activities: Mixed Ability Groups. AFL: Who were the Romans? to Britain Cross curricular links: Geography, Numeracy, History Activity 1: AFL: Why did the Romans want to come to Britain? CT to introduce the topic of the Romans and elicit children’s prior Sort timeline flashcards into chronological order CT to refer back to the idea that one of the main reasons for knowledge: invasion was connected to wealth and money. Explain that Q Who were the Romans? After completion, discuss the events as a whole class to ensure over the next few lessons we shall be focusing on Roman Q What do you know about them already? that the children understand the vocabulary and events described money / coins. Q Where do they originate from? * Option to use CT to show children a map, children to locate Rome and Britain. http://www.schoolsliaison.org.uk/kids/preload.htm or RESOURCES Explain that the Romans invaded Britain. http://resources.woodlands-junior.kent.sch.uk/homework/romans.html Q What does the word ‘invade’ mean? for further information about the key dates and events involved in Websites: the Roman invasion. http://www.schoolsliaison.org.uk/kids/preload.htm To understand why they invaded Britain we must examine what http://www.sparklebox.co.uk/topic/past/roman-empire.html was happening in Britain before the invasion. -

Currency, Bullion and Accounts. Monetary Modes in the Roman World

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Ghent University Academic Bibliography 1 Currency, bullion and accounts. Monetary modes in the Roman world Koenraad Verboven in Belgisch Tijdschrift voor Numismatiek en Zegelkunde/ Revue Belge de Numismatique et de Sigillographie 155 (2009) 91-121 Finley‟s assertion that “money was essentially coined metal and nothing else” still enjoys wide support from scholars1. The problems with this view have often been noted. Coins were only available in a limited supply and large payments could not be carried out with any convenience. Travelling with large sums in coins posed both practical and security problems. To quote just one often cited example, Cicero‟s purchase of his house on the Palatine Hill for 3.5 million sesterces would have required 3.4 tons of silver denarii2. Various solutions have been proposed : payments in kind or by means of bullion, bank money, transfer of debt notes or sale credit. Most of these combine a functional view of money („money is what money does‟) with the basic belief that coinage in the ancient world was the sole dominant monetary instrument, with others remaining „second-best‟ alternatives3. Starting from such premises, research has focused on identifying and assessing the possible alternative instruments to effectuate payments. Typical research questions are for instance the commonness (or not) of giro payments, the development (or underdevelopment) of financial instruments, the monetary nature (or not) of ancient debt notes, the commonness (or not) of payments in kind, and so forth. Despite Ghent University, Department of History 1 M. -

Presidential Address 2014 Coin Hoards and Hoarding in Britain

PRESIDENTIAL ADDRESS 2014 COIN HOARDS AND HOARDING IN BRITAIN (3): RADIATE HOARDS ROGER BLAND Introduction IN my first presidential address I gave an overview of hoarding in Britain from the Bronze Age through to recent times,1 while last year I spoke about hoards from the end of Roman Britain.2 This arises from a research project (‘Crisis or continuity? Hoards and hoarding in Iron Age and Roman Britain’) funded by the Arts and Humanities Research Council and based at the British Museum and the University of Leicester. The project now includes the whole of the Iron Age and Roman periods from around 120 BC to the early fifth century. For the Iron Age we have relied on de Jersey’s corpus of 340 Iron Age coin hoards and we are grateful to him for giving us access to his data in advance of publica- tion.3 For the Roman period, our starting point has been Anne Robertson’s Inventory of Romano-British Coin Hoards (RBCH),4 which includes details of 2,007 hoards, including dis- coveries made down to about 1990. To that Eleanor Ghey has added new discoveries and also trawled other data sources such as Guest and Wells’s corpus of Roman coin finds from Wales,5 David Shotter’s catalogues of Roman coin finds from the North West,6 Penhallurick’s corpus of Cornish coin finds,7 Historic Environment Records and the National Monuments Record. She has added a further 1,045 Roman hoards, taking the total to 3,052, but this is not the final total. -

Costs of Living in Roman Palestine Iii by Daniel

COSTS OF LIVING IN ROMAN PALESTINE III BY DANIEL SPERBER THIRD CENTURY PRICE-LEVELS Continued *) Glancing back over our price-lists, it will be seen that while I and II cent. prices are relatively simple to analyse and compare with one another, (thanks to the general economic stability of the period), the material for the III and IV cent. presents a considerably different pic- ture. For this was a phase of monetary deterioration and economic flux. Thus, even a dated III cent. price given in denarii is of little use until we determine how much silver was in a denarius of that date. And even then one cannot easily compare the resultant price (now in terms of pure silver) with those of a former century. For the value of the denarius does not seem to have declined in an exact ratio to its diminu- tion in silver content. Rather it would appear, in an attempt to stem its rapid fall in value, silver was somewhat overvalued in relationship to gold; in other words, there appears to have been a shifting silver-gold ratio throughout the period.') Only when all these factors have been taken in account, can one attempt to compare III and IV cent. prices to those of the preceding centuries. Elsewhere 2) I have examined the problems of III and early IV cent. currency developments and metrological terminology in considerable detail. Here I shall do no more than give a brief summary of some of my findings. *) See vol. IX, pp. I82-2II 1) For the problems of gold and silver "standards" during this time, and the con- temporary Rabbinic appreciation of these economic concepts, see my forthcoming article in Numismatic Chronicle 196 8, entitled "Rabbinic attitudes to Roman currency". -

Detail of a Silver Denarius from the Museum Collection, Decorated with the Head of Pax (Or Venus), 36–29 BCE

Detail of a silver denarius from the Museum collection, decorated with the head of Pax (or Venus), 36–29 BCE. PM object 29-126-864. 12 EXPEDITION Volume 60 Number 2 Like a Bad Penny Ancient Numismatics in the Modern World by jane sancinito numismatics (pronounced nu-mis-MAT-ics) is the study of coins, paper money, tokens, and medals. More broadly, numismatists (nu-MIS-ma-tists) explore how money is used: to pay for goods and services or to settle debts. Ancient coins and their contexts—including coins found in archaeological excavations—not only provide us with information about a region’s economy, but also about historical changes throughout a period, the beliefs of a society, important leaders, and artistic and fashion trends. EXPEDITION Fall 2018 13 LIKE A BAD PENNY Modern Problems, Ancient Origins Aegina and Athens were among the earliest Greek cities My change is forty-seven cents, a quarter, two dimes, to adopt coinage (ca. 7th century BCE), and both quickly and two pennies, one of them Canadian. Despite the developed imagery that represented them. Aegina, the steaming tea beside me, the product of a successful island city-state, chose a turtle, while on the mainland, exchange with the barista, I’m cranky, because, strictly Athens put the face of its patron deity, Athena, on the front speaking, I’ve been cheated. Not by much of course, (known as the obverse) and her symbols, the owl and the not enough to complain, but I recognize, albeit belat- olive branch, on the back (the reverse). They even started edly, that the Canadian penny isn’t money, not even in using the first three letters of their city’s name,ΑΘΕ , to Canada, where a few years ago they demonetized their signify: this is ours, we made this, and we stand behind it. -

Coins and Medals Including Renaissance and Later Medals from the Collection of Dr Charles Avery and Byzantine Coins from the Estate of Carroll F

Coins and Medals including Renaissance and Later Medals from the Collection of Dr Charles Avery and Byzantine Coins from the Estate of Carroll F. Wales (Part I) To be sold by auction at: Sotheby’s, in the Upper Grosvenor Gallery The Aeolian Hall, Bloomfield Place New Bond Street London W1 Days of Sale: Wednesday 11 and Thursday 12 June 2008 10.00 am and 2.00 pm Public viewing: 45 Maddox Street, London W1S 2PE Friday 6 June 10.00 am to 4.30 pm Monday 9 June 10.00 am to 4.30 pm Tuesday 10 June 10.00 am to 4.30 pm Or by previous appointment. Catalogue no. 31 Price £10 Enquiries: James Morton, Tom Eden, Paul Wood, Jeremy Cheek or Stephen Lloyd Cover illustrations: Lot 465 (front); Lot 1075 (back); Lot 515 (inside front and back covers, all at two-thirds actual size) in association with 45 Maddox Street, London W1S 2PE Tel.: +44 (0)20 7493 5344 Fax: +44 (0)20 7495 6325 Email: [email protected] Website: www.mortonandeden.com This auction is conducted by Morton & Eden Ltd. in accordance with our Conditions of Business printed at the back of this catalogue. All questions and comments relating to the operation of this sale or to its content should be addressed to Morton & Eden Ltd. and not to Sotheby’s. Important Information for Buyers All lots are offered subject to Morton & Eden Ltd.’s Conditions of Business and to reserves. Estimates are published as a guide only and are subject to review. The actual hammer price of a lot may well be higher or lower than the range of figures given and there are no fixed “starting prices”. -

Small Change and Big Changes: Minting and Money After the Fall of Rome

This is a repository copy of Small Change and Big Changes: minting and money after the Fall of Rome. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/90089/ Version: Draft Version Other: Jarrett, JA (Completed: 2015) Small Change and Big Changes: minting and money after the Fall of Rome. UNSPECIFIED. (Unpublished) Reuse Unless indicated otherwise, fulltext items are protected by copyright with all rights reserved. The copyright exception in section 29 of the Copyright, Designs and Patents Act 1988 allows the making of a single copy solely for the purpose of non-commercial research or private study within the limits of fair dealing. The publisher or other rights-holder may allow further reproduction and re-use of this version - refer to the White Rose Research Online record for this item. Where records identify the publisher as the copyright holder, users can verify any specific terms of use on the publisher’s website. Takedown If you consider content in White Rose Research Online to be in breach of UK law, please notify us by emailing [email protected] including the URL of the record and the reason for the withdrawal request. [email protected] https://eprints.whiterose.ac.uk/ Small Change and Big Changes: It’s a real pleasure to be back at the Barber again so soon, and I want to start by thanking Nicola, Robert and Jen for letting me get away with scheduling myself like this as a guest lecturer for my own exhibition. I’m conscious that in speaking here today I’m treading in the footsteps of some very notable numismatists, but right now the historic name that rings most loudly in my consciousness is that of the former Curator of the coin collection here and then Lecturer in Numismatics in the University, Michael Hendy. -

Experimental Investigation of Silvering in Late Roman Coinage

Mat. Res. Soc. Symp. Proc. Vol. 712 © 2002 Materials Research Society Experimental investigation of silvering in late Roman coinage C. Vlachou, J.G. McDonnell, R.C. Janaway Department of Archaeological Sciences, University of Bradford, BD7 1DP, UK. ABSTRACT Roman Coinage suffered from severe debasement during the 3rd century AD. By 250 AD., the production of complex copper alloy (Cu-Sn-Pb-Ag) coins with a silvered surface, became common practice. The same method continued to be applied during the 4th century AD for the production of a new denomination introduced by Diocletian in 293/4 AD. Previous analyses of these coins did not solve key technological issues and in particular, the silvering process. The British Museum kindly allowed further research at Bradford to examine coins from Cope’s Archive in more detail, utilizing XRF, SEM-EDS metallography, LA-ICP-MS and EPMA. Metallographic and SEM examination of 128 coins, revealed that the silver layer was very difficult to trace because its thickness was a few microns and in some cases it was present under the corrosion layer. Results derived from the LA-ICP-MS and EPMA analyses have demonstrated, for the first time, the presence of Hg in the surface layers of these coins. A review of ancient sources and historic literature indicated possible methods which might have been used for the production of the plating. A programme of plating experiments was undertaken to examine a number of variables in the process, such as amalgam preparation, and heating cycles. Results from the experimental work are presented. ITRODUCTION Coinage in the Late Roman Period suffered from severe debasement. -

A Handbook of Greek and Roman Coins

CORNELL UNIVERSITY LIBRARY BOUGHT WITH THE INCOME OF THE SAGE ENDOWMENT FUND GIVEN IN 1891 BY HENRY WILLIAMS SAGE Cornell University Library CJ 237.H64 A handbook of Greek and Roman coins. 3 1924 021 438 399 Cornell University Library The original of this book is in the Cornell University Library. There are no known copyright restrictions in the United States on the use of the text. http://www.archive.org/details/cu31924021438399 f^antilioofcs of glrcfjaeologj) anU Antiquities A HANDBOOK OF GREEK AND ROMAN COINS A HANDBOOK OF GREEK AND ROMAN COINS G. F. HILL, M.A. OF THE DEPARTMENT OF COINS AND MEDALS IN' THE bRITISH MUSEUM WITH FIFTEEN COLLOTYPE PLATES Hon&on MACMILLAN AND CO., Limited NEW YORK: THE MACMILLAN COMPANY l8 99 \_All rights reserved'] ©jcforb HORACE HART, PRINTER TO THE UNIVERSITY PREFACE The attempt has often been made to condense into a small volume all that is necessary for a beginner in numismatics or a young collector of coins. But success has been less frequent, because the knowledge of coins is essentially a knowledge of details, and small treatises are apt to be un- readable when they contain too many references to particular coins, and unprofltably vague when such references are avoided. I cannot hope that I have passed safely between these two dangers ; indeed, my desire has been to avoid the second at all risk of encountering the former. At the same time it may be said that this book is not meant for the collector who desires only to identify the coins which he happens to possess, while caring little for the wider problems of history, art, mythology, and religion, to which coins sometimes furnish the only key.