Bank Loans: Looking Beyond Interest Rate Expectations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Subnational Debt of China: the Politics-Finance Nexus*

Subnational Debt of China: The Politics-Finance Nexus* HAOYU GAO, HONG RU and DRAGON YONGJUN TANG September 12, 2017 Abstract Using comprehensive proprietary loan-level data, we analyze the borrowing and defaults of local governments in China. Contrary to conventional wisdom, policy bank loans to local governments have significantly lower default rates than commercial bank loans with similar characteristics. Policy bank loans are relatively more important for local politician’s career advancement. Distressed local governments often strategically choose to default on loans from commercial banks. This selection is more pronounced after the abrupt ending of the “four trillion” stimulus when China started tightening local government borrowing. Our findings shed light on potential approach to hardening budget constraint for local government. JEL Codes: G21, G32, H74 * Haoyu Gao, Central University of Finance and Economics, 39 South College Road, Haidian Dist., Beijing 100081, China; [email protected]. Hong Ru, Nanyang Technological University, 50 Nanyang Avenue, Singapore, 639798; [email protected]. Dragon Yongjun Tang, University of Hong Kong, Pokfulam Road, Hong Kong; [email protected]. We thank Warren Bailey, Patrick Bolton, Anna Cieslak, Jinquan Duan, Di Gong, Brett Green, Zhiguo He, Harrison Hong, Sheng Huang, Liangliang Jiang, Bo Li, Hao Liang, Jose Liberti, Ruichang Lu, Wenlan Qian, Jay Ritter, Jose Scheinkman, Victor Shih, Michael Song, Mark Spiegel, Chenggang Xu, Xiaoyun Yu, Weina Zhang, Li-An Zhou, Hao Zhou, staff at China Development -

Convertible Financing Bonds As Backdoor Equity

Journal of Financial Economics 32 (1992) 3-21. North-Holland Convertible bonds as backdoor equity financing Jeremy C. Stein* Massachusetts Insrirure of Technology. Cambridge, .MA 021.59. LISA Received September 1991, final version received March 1992 This paper argues that corporations may use convertible bonds as an indirect way to get equity into their capital structures when adverse-selection problems make a conventional stock issue unattrac- tive. Unlike other theories of convertible bond issuance. the model here highlights: 1) the importance of call provisions on convertibles and 2) the significance of costs of financial distress to the information content of a convertible issue. 1. Introduction Convertible bonds are an important source of financing for many corpora- tions. According to data presented in Essig (1991), more than 10% of all COMPUSTAT companies had ratios of convertible debt to total debt exceeding 33% during the period 1963-1984. A good deal of research effort has been devoted to developing pricing models for convertibles,’ as well as to the issues surrounding corporations’ policies for calling them.2 Somewhat less work has addressed the fundamental question of why companies issue convertibles in the first place. This paper develops a rationale for the use of convertible debt. I argue that companies may use convertible bonds to get equity into their capital structures Correspondence to: Jeremy C. Stein, Sloan School of Management, Massachusetts Institute of Technology, 50 Memorial Drive, Cambridge, MA 02139. USA. *This research is supported by a Batterymarch Fellowship and by the International Financial Services Research Center at MIT. I thank Paul Asquith, Kenneth Froot, Steven Kaplan, Wayne Mikkelson (the referee). -

Mortgage-Backed Securities & Collateralized Mortgage Obligations

Mortgage-backed Securities & Collateralized Mortgage Obligations: Prudent CRA INVESTMENT Opportunities by Andrew Kelman,Director, National Business Development M Securities Sales and Trading Group, Freddie Mac Mortgage-backed securities (MBS) have Here is how MBSs work. Lenders because of their stronger guarantees, become a popular vehicle for finan- originate mortgages and provide better liquidity and more favorable cial institutions looking for investment groups of similar mortgage loans to capital treatment. Accordingly, this opportunities in their communities. organizations like Freddie Mac and article will focus on agency MBSs. CRA officers and bank investment of- Fannie Mae, which then securitize The agency MBS issuer or servicer ficers appreciate the return and safety them. Originators use the cash they collects monthly payments from that MBSs provide and they are widely receive to provide additional mort- homeowners and “passes through” the available compared to other qualified gages in their communities. The re- principal and interest to investors. investments. sulting MBSs carry a guarantee of Thus, these pools are known as mort- Mortgage securities play a crucial timely payment of principal and inter- gage pass-throughs or participation role in housing finance in the U.S., est to the investor and are further certificates (PCs). Most MBSs are making financing available to home backed by the mortgaged properties backed by 30-year fixed-rate mort- buyers at lower costs and ensuring that themselves. Ginnie Mae securities are gages, but they can also be backed by funds are available throughout the backed by the full faith and credit of shorter-term fixed-rate mortgages or country. The MBS market is enormous the U.S. -

Capital Markets

U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities Capital Markets OCTOBER 2017 U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities Capital Markets Report to President Donald J. Trump Executive Order 13772 on Core Principles for Regulating the United States Financial System Steven T. Mnuchin Secretary Craig S. Phillips Counselor to the Secretary Staff Acknowledgments Secretary Mnuchin and Counselor Phillips would like to thank Treasury staff members for their contributions to this report. The staff’s work on the report was led by Brian Smith and Amyn Moolji, and included contributions from Chloe Cabot, John Dolan, Rebekah Goshorn, Alexander Jackson, W. Moses Kim, John McGrail, Mark Nelson, Peter Nickoloff, Bill Pelton, Fred Pietrangeli, Frank Ragusa, Jessica Renier, Lori Santamorena, Christopher Siderys, James Sonne, Nicholas Steele, Mark Uyeda, and Darren Vieira. iii A Financial System That Creates Economic Opportunities • Capital Markets Table of Contents Executive Summary 1 Introduction 3 Scope of This Report 3 Review of the Process for This Report 4 The U.S. Capital Markets 4 Summary of Issues and Recommendations 6 Capital Markets Overview 11 Introduction 13 Key Asset Classes 13 Key Regulators 18 Access to Capital 19 Overview and Regulatory Landscape 21 Issues and Recommendations 25 Equity Market Structure 47 Overview and Regulatory Landscape 49 Issues and Recommendations 59 The Treasury Market 69 Overview and Regulatory Landscape 71 Issues and Recommendations 79 -

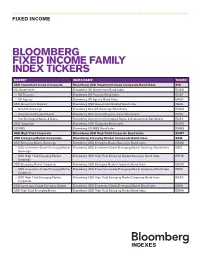

Bloomberg Fixed Income Family Index Tickers

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// FIXED INCOME BLOOMBERG FIXED INCOME FAMILY INDEX TICKERS MARKET INDEX NAME TICKER USD Investment Grade Composite Bloomberg USD Investment Grade Composite Bond Index BIG US Government Bloomberg US Government Bond Index BUSG » US Treasury Bloomberg US Treasury Bond Index BUSY » US Agency Bloomberg US Agency Bond Index BAGY USD Government Related Bloomberg USD Government Related Bond Index BGRL » Non-US Sovereign Bloomberg Non-US Sovereign Bond Index BNSO » Government Regional/Local Bloomberg Government Regional/Local Bond Index BRGL » Gov Developed Banks & Supra Bloomberg Government Developed Banks & Supranational Bond Index BDEV USD Corporate Bloomberg USD Corporate Bond Index BUSC US MBS Bloomberg US MBS Bond Index BMBS USD High Yield Corporate Bloomberg USD High Yield Corporate Bond Index BUHY USD Emerging Market Composite Bloomberg Emerging Market Composite Bond Index BEM USD Emerging Market Sovereign Bloomberg USD Emerging Market Sovereign Bond Index BEMS » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Sovereign Bond Index BEIS Sovereign » USD High Yield Emerging Market Bloomberg USD High Yield Emerging Market Sovereign Bond Index BEHS Sovereign USD Emerging Market Corporate Bloomberg USD Emerging Market Corporate Bond Index BEMC » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Corporate Bond Index BIEM Corporate -

The Importance of the Capital Structure in Credit Investments: Why Being at the Top (In Loans) Is a Better Risk Position

Understanding the importance of the capital structure in credit investments: Why being at the top (in loans) is a better risk position Before making any investment decision, whether it’s in equity, fixed income or property it’s important to consider whether you are adequately compensated for the risks you are taking. Understanding where your investment sits in the capital structure will help you recognise the potential downside that could result in permanent loss of capital. Within a typical business there are various financing securities used to fund existing operations and growth. Most companies will use a combination of both debt and equity. The debt may come in different forms including senior secured loans and unsecured bonds, while equity typically comes as preference or ordinary shares. The exact combination of these instruments forms the company’s “capital structure”, and is usually designed to suit the underlying cash flows and assets of the business as well as investor and management risk appetites. The most fundamental aspect for debt investors in any capital structure is seniority and security in the capital structure which is reflected in the level of leverage and impacts the amount an investor should recover if a company fails to meet its financial obligations. Seniority refers to where an instrument ranks in priority of payment. Creditors (debt holders) normally have a legal right to be paid both interest and principal in priority to shareholders. Amongst creditors, “senior” creditors will be paid in priority to “junior” creditors. Security refers to a creditor’s right to take a “mortgage” or “lien” over property and other assets of a company in a default scenario. -

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. • Fixed-income securities. • Stocks. • Real assets (capital budgeting). Part C Determination of risk-adjusted discount rates. Part D Introduction to derivatives. Main Issues • Fixed-Income Markets • Term Structure of Interest Rates • Interest Rate Risk • Inflation Risk • Credit Risk Chapter 3 Fixed Income Securities 3-1 1 Fixed-Income Markets Definition: Fixed-income securities are financial claims with promised cash flows of fixed amount paid at fixed dates. Classification of Fixed-Income Securities: 1. Treasury Securities: • U.S. Treasury securities (bills, notes, bonds). • Bunds, JGBs, U.K. Gilts ... 2. Federal Agency Securities: • Securities issued by federal agencies (FHLB, FNMA ...). 3. Corporate Securities: • Commercial paper. • Medium-term notes (MTNs). • Corporate bonds ... 4. Municipal Securities. 5. Mortgage-Backed Securities. 6. ... Fall 2006 c J. Wang 15.401 Lecture Notes 3-2 Fixed Income Securities Chapter 3 Overview of Fixed-income Markets Composition of U.S. Debt Markets (2005) Market value % (in trillion dollars) Treasury 4.17 16.5 Corporate 4.99 19.7 Mortgage 5.92 23.4 Agency 2.60 10.3 Munies 2.23 8.8 Asset-Backed 1.96 7.7 Money Market 3.47 13.7 Total 25.33 Current Trends T. Corp. MBS Agency ABS Munies MM Total 1995 3.31 1.94 2.35 0.84 0.32 1.29 1.18 11.23 1996 3.44 2.12 2.49 0.93 0.40 1.30 1.39 12.01 1997 3.44 2.36 2.68 1.02 0.54 1.32 1.69 13.05 1998 3.34 2.71 2.96 1.30 0.73 1.40 1.98 14.42 1999 3.27 3.05 3.33 1.62 0.90 1.46 2.34 15.96 2000 2.95 3.36 3.56 1.85 1.07 1.48 2.66 16.95 2001 2.97 3.84 4.13 2.15 1.28 1.60 2.57 18.53 2002 3.20 4.09 4.70 2.29 1.54 1.73 2.55 20.15 2003 3.57 4.46 5.31 2.64 1.69 1.89 2.53 22.10 2004 3.94 3.70 5.47 2.75 1.83 2.02 2.87 23.58 2005 4.17 4.99 4.92 2.60 1.96 2.23 3.47 25.33 15.401 Lecture Notes c J. -

Vantage Towers AG

Prospectus dated March 8, 2021 Prospectus for the public offering in the Federal Republic of Germany of 88,888,889 existing ordinary registered shares with no par value (Namensaktien ohne Nennbetrag) from the holdings of the Existing Shareholder, of 22,222,222 existing ordinary registered shares with no par value (Namensaktien ohne Nennbetrag) from the holdings of the Existing Shareholder, with the number of shares to be actually placed with investors subject to the exercise of an Upsize Option upon the decision of the Existing Shareholder, in agreement with the Joint Global Coordinators, on the date of pricing, and of 13,333,333 existing ordinary registered shares with no par value (Namensaktien ohne Nennbetrag) from the holdings of the Existing Shareholder in connection with a possible over-allotment, and at the same time for the admission to trading on the regulated market (regulierter Markt) of the Frankfurt Stock Exchange (Frankfurter Wertpapierbörse) with simultaneous admission to the sub- segment of the regulated market with additional post-admission obligations (Prime Standard) of the Frankfurt Stock Exchange (Frankfurter Wertpapierbörse) of 505,782,265 existing ordinary registered shares with no par value (Namensaktien ohne Nennbetrag) (existing share capital), each such share with a notional value of EUR 1.00 in the Company’s share capital and full dividend rights as of April 1, 2020 of Vantage Towers AG Düsseldorf, Germany Price Range: EUR 22.50 – EUR 29.00 International Securities Identification Number (ISIN): DE000A3H3LL2 German Securities Code (Wertpapierkennnummer, WKN): A3H 3LL Common Code: 230832161 Ticker Symbol: VTWR Joint Global Coordinators BofA Securities Morgan Stanley UBS Joint Bookrunners Barclays Berenberg BNP PARIBAS Deutsche Bank Goldman Sachs Jefferies TABLE OF CONTENTS Page I. -

Determinants of Convertible Bond Structure;

University of New Orleans ScholarWorks@UNO Department of Economics and Finance Working Papers, 1991-2006 Department of Economics and Finance 2005 Determinants of Convertible Bond Structure; Sudha Krishnaswami University of New Orleans Devrim Yaman Western Michigan University Follow this and additional works at: https://scholarworks.uno.edu/econ_wp Recommended Citation Krishnaswami, Sudha and Yaman, Devrim, "Determinants of Convertible Bond Structure;" (2005). Department of Economics and Finance Working Papers, 1991-2006. Paper 37. https://scholarworks.uno.edu/econ_wp/37 This Working Paper is brought to you for free and open access by the Department of Economics and Finance at ScholarWorks@UNO. It has been accepted for inclusion in Department of Economics and Finance Working Papers, 1991-2006 by an authorized administrator of ScholarWorks@UNO. For more information, please contact [email protected]. Determinants of Convertible Bond Structure Sudha Krishnaswami* Department of Economics & Finance College of Business Administration University of New Orleans New Orleans, LA 70148 (504) 280-6488 [email protected] Devrim Yaman Department of Finance & Commercial Law Haworth College of Business Western Michigan University Kalamazoo, MI 49008 (269) 387-5749 [email protected] _______________________________ * Corresponding author. We thank Ranjan D’Mello, Tarun Mukherjee, Oranee Tawatnuntachai, Oscar Varela, Gerald Whitney, and seminar participants at the University of New Orleans, the 2002 Financial Management Association Meetings, and the 2004 European Financial Management Association Meetings for their comments and suggestions. Devrim Yaman acknowledges funding support from the Faculty Research and Creative Activities Support Fund at Western Michigan University. All errors remain our responsibility. Determinants of Convertible Bond Structure Abstract Theoretical research argues that convertible bonds mitigate the contracting costs of moral hazard, adverse selection, and financial distress. -

Managing Fixed Income Late in the Credit Cycle: Navigating the Path Forward

INCOME INVESTING Managing fixed income late in the credit cycle: navigating the path forward nuveen knows Highlights • While we are clearly in the late stage of the credit cycle, we don’t think a recession is imminent and believe investors should feel comfortable investing in credit 2Q19 markets throughout the rest of 2019. • We believe investors should focus on higher-quality issues with improving credit fundamentals, while seeking to diversify across industries and geographies. • Nuveen’s sector specialist teams are finding attractive opportunities in U.S. credit sectors, including high yield, but they are increasingly diversifying into other higher-income areas, such as emerging market debt and leveraged loans. • Active management can add value in any environment, but we believe it is especially beneficial at the current stage of the credit cycle. The multi-trillion-dollar question for investors: How late are we in the credit cycle, and what are the portfolio implications? That’s the question we most often hear from our clients. And while there are few certainties in life or markets, we feel confident in our answer: We are clearly in the late stage of the credit cycle. But “late” doesn’t mean “done,” and credit cycles don’t die of old age. Rather, a combination of fundamentals and sentiment bring about their demise, and even in their later stages, savvy investors can find opportunities not only to protect their investments, but to position their portfolios for an emphasis on income as the cycle turns. Nuveen believes most investors should be comfortable investing in the credit markets throughout the rest of 2019. -

Product Pitchbook

2Q 2021 Separately Managed Accounts WESTERN ASSET MUNICIPAL BOND LADDERS Separately Managed Accounts (SMAs) are investment services provided by Legg Mason Private Portfolio Group, LLC (LMPPG), a federally registered investment advisor. Client portfolios are managed based on investment instructions or advice provided by one or more of the following Franklin Templeton affiliated subadvisors: ClearBridge Investments, LLC. Management is implemented by LMPPG, the designated subadvisor or, in the case of certain programs, the program sponsor or its designee. These materials are being provided for illustrative and informational purposes only. The information contained herein is obtained from multiple sources that are believed to be reliable. However, such information has not been verified, and may be different from the information included in documents and materials created by the sponsor firm in whose investment program a client participates. Some sponsor firms may require that these materials be preceded or accompanied by investment profiles or other documents or materials prepared by such sponsor firms, which will be provided upon a client's request. For additional information, documents and/or materials, please speak to your financial professional or contact your sponsor firm. INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE Introduction | Franklin Templeton Franklin Templeton We aim to offer the best of both worlds: global strength and boutique specialization. Providing real customization backed by the scale and -

Morningstar Global Fixed Income Classification Methodology

? Morningstar Global Fixed Income Classification Morningstar Research Introduction Effective Oct. 31, 2016 Fixed-Income Sectors Contents The fixed-income securities and fixed-income derivative exposures within a portfolio are mapped into 1 Introduction Secondary Sectors that represent the most granular level of classification. Each item can also be 2 Super Sectors 10 Sectors grouped into one of several higher-level Primary Sectors, which ultimately roll up to five fixed-income Super Sectors. Important Disclosure The conduct of Morningstar’s analysts is governed Cash Sectors by Code of Ethics/Code of Conduct Policy, Personal Cash securities and cash-derivative exposures within a portfolio are mapped into Secondary Sectors that Security Trading Policy (or an equivalent of), and Investment Research Policy. For information represent the most granular level of classification. Each item can also be grouped into cash & regarding conflicts of interest, please visit: http://global.morningstar.com/equitydisclosures equivalents Primary Sector and into cash & equivalents Super Sector (cash & equivalents Primary Sector = cash & equivalents Super Sector ). Morningstar includes cash within fixed-income sectors. Cash is not a bond, but it is a type of fixed- income. When bond-fund managers are feeling nervous about interest rates rising, they might increase their cash stake to shorten the portfolio’s duration. Moving assets into cash is a defensive strategy for interest-rate risk. In addition, Morningstar includes securities that mature in less than 92 days in the definition of cash. The cash & equivalents Secondary Sectors allow for more-detailed identification of cash, allowing clients to see, for example, if the cash holdings are in currency or short-term government bonds.