Municipal Bonds

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mortgage-Backed Securities & Collateralized Mortgage Obligations

Mortgage-backed Securities & Collateralized Mortgage Obligations: Prudent CRA INVESTMENT Opportunities by Andrew Kelman,Director, National Business Development M Securities Sales and Trading Group, Freddie Mac Mortgage-backed securities (MBS) have Here is how MBSs work. Lenders because of their stronger guarantees, become a popular vehicle for finan- originate mortgages and provide better liquidity and more favorable cial institutions looking for investment groups of similar mortgage loans to capital treatment. Accordingly, this opportunities in their communities. organizations like Freddie Mac and article will focus on agency MBSs. CRA officers and bank investment of- Fannie Mae, which then securitize The agency MBS issuer or servicer ficers appreciate the return and safety them. Originators use the cash they collects monthly payments from that MBSs provide and they are widely receive to provide additional mort- homeowners and “passes through” the available compared to other qualified gages in their communities. The re- principal and interest to investors. investments. sulting MBSs carry a guarantee of Thus, these pools are known as mort- Mortgage securities play a crucial timely payment of principal and inter- gage pass-throughs or participation role in housing finance in the U.S., est to the investor and are further certificates (PCs). Most MBSs are making financing available to home backed by the mortgaged properties backed by 30-year fixed-rate mort- buyers at lower costs and ensuring that themselves. Ginnie Mae securities are gages, but they can also be backed by funds are available throughout the backed by the full faith and credit of shorter-term fixed-rate mortgages or country. The MBS market is enormous the U.S. -

A Pooled Municipal Bonding Program

A POOLED MUNICIPAL BONDING PROGRAM Contents Program Overview ………………………………………………... 1 History of the Bond Bank ………………………………………… 2 Tax-Exempt Financing Program ……………………….…………. 4 Other Bond Bank Programs …………………………………….… 5 Benefits to Participating Communities ……………………….…... 5 Loan Application and Financing Process…………………………. 6 Spring 2012 Financing Schedule………………………………….. 7 New Hampshire Municipal Bond Bank 25 Triangle Park Drive Concord, New Hampshire 03301 Email: [email protected] Web-site Address: www.nhmbb.org Revised 3/12 The mission of the New Hampshire Municipal Bond Bank is to provide professional services to assist qualified New Hampshire entities to obtain financing for eligible purposes. To meet its mission, the New Hampshire Municipal Bond Bank is committed to: ! Financial stability ! Strong client relations ! Low issuance costs ! Obtaining the lowest possible borrowing rates ! An efficient application process ! Maintaining strong credit ratings and financial market access ! A well trained team of professional staff & consultants ! Support best possible public finance practices ! Meeting the requirements of all applicable state and federal laws, particularly RSA:35-A “On a number of occasions, I have included the Bond Bank in my requests for proposals, which included the major private banking institutions doing business in New Hampshire at the time. After careful analysis, you have always been chosen due to the Bond Bank’s reasonable fee structure, ease of use and excellent customer service standards. The Bond Bank has seen me through the construction of a number of large projects which include a wastewater treatment facility and a new high school, as well as many others of a smaller magnitude. I look forward to working with the Bond Bank in the future.” Peter A. -

Navigating the Municipal Bond Market September 2019

Navigating the Municipal Bond Market September 2019 Craig Brandon, CFA Co-Director of Municipal Investments AN EATON VANCE COMPANY FOR INVESTMENT PROFESSIONAL USE ONLY. NOT FOR USE WITH THE PUBLIC. 2 Fixed Income Asset Class Return Analysis Higher 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 YTD EM (Local EM (Local EM (Local Investment Treasury High Yield Municipal High Yield Municipal Municipal High Yield Municipal Currency) Currency) Currency) Grade 13.74 57.51 10.70 7.42 9.05 3.30 17.49 1.28 15.68 16.76 15.21 13.94 Investment Global Agg MBS Bank Loan High Yield Treasury High Yield Bank Loan MBS Bank Loan MBS High Yield Grade Ex-U.S. 8.34 51.62 15.19 9.81 15.58 5.29 1.51 10.16 0.99 11.15 7.46 10.51 Global Agg EM (Local Investment Investment EM (Local Bank Loan MBS MBS Treasury High Yield Treasury Treasury Ex-U.S. Currency) Grade Grade Currency) 10.13 -1.41 6.08 0.84 7.48 0.86 8.63 4.40 21.98 8.15 9.82 9.94 Investment Investment Investment Investment Investment Investment Municipal MBS Bank Loan Treasury Bank Loan Municipal Grade Grade Grade Grade Grade Grade -2.47 6.23 9.66 5.05 0.44 7.61 18.68 9.00 -1.53 -0.68 6.11 6.42 Investment Global Agg EM (Local Municipal Treasury High Yield Municipal Municipal High Yield Bank Loan MBS Municipal Grade Ex-US Currency) 12.91 5.87 4.38 6.78 -2.55 2.50 -0.69 1.67 5.45 -4.94 -2.15 6.83 EM (Local Global Agg Global Agg Global Agg Global Agg MBS Treasury Bank Loan High Yield Bank Loan High Yield Bank Loan Currency) Ex-U.S. -

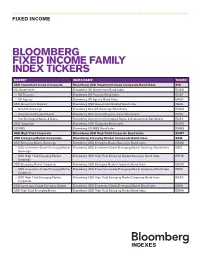

Bloomberg Fixed Income Family Index Tickers

///////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// FIXED INCOME BLOOMBERG FIXED INCOME FAMILY INDEX TICKERS MARKET INDEX NAME TICKER USD Investment Grade Composite Bloomberg USD Investment Grade Composite Bond Index BIG US Government Bloomberg US Government Bond Index BUSG » US Treasury Bloomberg US Treasury Bond Index BUSY » US Agency Bloomberg US Agency Bond Index BAGY USD Government Related Bloomberg USD Government Related Bond Index BGRL » Non-US Sovereign Bloomberg Non-US Sovereign Bond Index BNSO » Government Regional/Local Bloomberg Government Regional/Local Bond Index BRGL » Gov Developed Banks & Supra Bloomberg Government Developed Banks & Supranational Bond Index BDEV USD Corporate Bloomberg USD Corporate Bond Index BUSC US MBS Bloomberg US MBS Bond Index BMBS USD High Yield Corporate Bloomberg USD High Yield Corporate Bond Index BUHY USD Emerging Market Composite Bloomberg Emerging Market Composite Bond Index BEM USD Emerging Market Sovereign Bloomberg USD Emerging Market Sovereign Bond Index BEMS » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Sovereign Bond Index BEIS Sovereign » USD High Yield Emerging Market Bloomberg USD High Yield Emerging Market Sovereign Bond Index BEHS Sovereign USD Emerging Market Corporate Bloomberg USD Emerging Market Corporate Bond Index BEMC » USD Investment Grade Emerging Market Bloomberg USD Investment Grade Emerging Market Corporate Bond Index BIEM Corporate -

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. • Fixed-income securities. • Stocks. • Real assets (capital budgeting). Part C Determination of risk-adjusted discount rates. Part D Introduction to derivatives. Main Issues • Fixed-Income Markets • Term Structure of Interest Rates • Interest Rate Risk • Inflation Risk • Credit Risk Chapter 3 Fixed Income Securities 3-1 1 Fixed-Income Markets Definition: Fixed-income securities are financial claims with promised cash flows of fixed amount paid at fixed dates. Classification of Fixed-Income Securities: 1. Treasury Securities: • U.S. Treasury securities (bills, notes, bonds). • Bunds, JGBs, U.K. Gilts ... 2. Federal Agency Securities: • Securities issued by federal agencies (FHLB, FNMA ...). 3. Corporate Securities: • Commercial paper. • Medium-term notes (MTNs). • Corporate bonds ... 4. Municipal Securities. 5. Mortgage-Backed Securities. 6. ... Fall 2006 c J. Wang 15.401 Lecture Notes 3-2 Fixed Income Securities Chapter 3 Overview of Fixed-income Markets Composition of U.S. Debt Markets (2005) Market value % (in trillion dollars) Treasury 4.17 16.5 Corporate 4.99 19.7 Mortgage 5.92 23.4 Agency 2.60 10.3 Munies 2.23 8.8 Asset-Backed 1.96 7.7 Money Market 3.47 13.7 Total 25.33 Current Trends T. Corp. MBS Agency ABS Munies MM Total 1995 3.31 1.94 2.35 0.84 0.32 1.29 1.18 11.23 1996 3.44 2.12 2.49 0.93 0.40 1.30 1.39 12.01 1997 3.44 2.36 2.68 1.02 0.54 1.32 1.69 13.05 1998 3.34 2.71 2.96 1.30 0.73 1.40 1.98 14.42 1999 3.27 3.05 3.33 1.62 0.90 1.46 2.34 15.96 2000 2.95 3.36 3.56 1.85 1.07 1.48 2.66 16.95 2001 2.97 3.84 4.13 2.15 1.28 1.60 2.57 18.53 2002 3.20 4.09 4.70 2.29 1.54 1.73 2.55 20.15 2003 3.57 4.46 5.31 2.64 1.69 1.89 2.53 22.10 2004 3.94 3.70 5.47 2.75 1.83 2.02 2.87 23.58 2005 4.17 4.99 4.92 2.60 1.96 2.23 3.47 25.33 15.401 Lecture Notes c J. -

Issuance of Tax-Exempt Municipal Debentures

Issuance of Tax-Exempt Municipal Debentures (City Council on August 1, 2, 3 and 4, 2000, adopted this Clause, without amendment.) The Policy and Finance Committee recommendations the adoption of the following report (July 4, 2000) from the Chief Financial Officer and Treasurer: Purpose: To discuss the potential advantages and disadvantages if the City is legally allowed to issue tax-free municipal bonds and to provide a strategy to proceed with this issue. Financial Implications and Impact Statement: N/A Recommendations: It is recommended that: (1) this report be received for information; and (2) a copy of this report be forwarded to Team Toronto for its consideration with other possible alternative financing strategies being explored with the provincial and federal governments. Background: At the Council meeting held on January 27, 2000, Councillor Davis moved a Notice of Motion requesting Council to establish a Working Committee on Municipal Debt composed of five members of City Council working with staff to establish a proposal for presentation to federal and provincial finance Ministers and officials concerning tax-free municipal bonds. The motion was referred to the Chief Administrative Officer for a report to the Policy and Finance Committee who requested a report from the Chief Financial Officer and Treasurer. Comments: In the United States, the federal government exempts interest payments on municipal debt from federal income taxes, thus lowering the cost of borrowing for state and local governments. Bonds purchased in one’s own jurisdiction are usually also exempt from local and state income taxes, e.g., New York residents who purchase New York City bonds. -

Managing Fixed Income Late in the Credit Cycle: Navigating the Path Forward

INCOME INVESTING Managing fixed income late in the credit cycle: navigating the path forward nuveen knows Highlights • While we are clearly in the late stage of the credit cycle, we don’t think a recession is imminent and believe investors should feel comfortable investing in credit 2Q19 markets throughout the rest of 2019. • We believe investors should focus on higher-quality issues with improving credit fundamentals, while seeking to diversify across industries and geographies. • Nuveen’s sector specialist teams are finding attractive opportunities in U.S. credit sectors, including high yield, but they are increasingly diversifying into other higher-income areas, such as emerging market debt and leveraged loans. • Active management can add value in any environment, but we believe it is especially beneficial at the current stage of the credit cycle. The multi-trillion-dollar question for investors: How late are we in the credit cycle, and what are the portfolio implications? That’s the question we most often hear from our clients. And while there are few certainties in life or markets, we feel confident in our answer: We are clearly in the late stage of the credit cycle. But “late” doesn’t mean “done,” and credit cycles don’t die of old age. Rather, a combination of fundamentals and sentiment bring about their demise, and even in their later stages, savvy investors can find opportunities not only to protect their investments, but to position their portfolios for an emphasis on income as the cycle turns. Nuveen believes most investors should be comfortable investing in the credit markets throughout the rest of 2019. -

Glossary of Bond Terms

Glossary of Bond Terms Accreted value- The current value of your zero-coupon municipal bond, taking into account interest that has been accumulating and automatically reinvested in the bond. Accrual bond- Often the last tranche in a CMO, the accrual bond or Z-tranche receives no cash payments for an extended period of time until the previous tranches are retired. While the other tranches are outstanding, the Z-tranche receives credit for periodic interest payments that increase its face value but are not paid out. When the other tranches are retired, the Z-tranche begins to receive cash payments that include both principal and continuing interest. Accrued interest- (1) The dollar amount of interest accrued on an issue, based on the stated interest rate on that issue, from its date to the date of delivery to the original purchaser. This is usually paid by the original purchaser to the issuer as part of the purchase price of the issue; (2) Interest deemed to be earned on a security but not yet paid to the investor. Active tranche- A CMO tranche that is currently paying principal payments to investors. Adjustable-rate mortgage (ARM)- A mortgage loan on which interest rates are adjusted at regular intervals according to predetermined criteria. An ARM's interest rate is tied to an objective, published interest rate index. Amortization- Liquidation of a debt through installment payments. Arbitrage- In the municipal market, the difference in interest earned on funds borrowed at a lower tax-exempt rate and interest on funds that are invested at a higher-yielding taxable rate. -

Product Pitchbook

2Q 2021 Separately Managed Accounts WESTERN ASSET MUNICIPAL BOND LADDERS Separately Managed Accounts (SMAs) are investment services provided by Legg Mason Private Portfolio Group, LLC (LMPPG), a federally registered investment advisor. Client portfolios are managed based on investment instructions or advice provided by one or more of the following Franklin Templeton affiliated subadvisors: ClearBridge Investments, LLC. Management is implemented by LMPPG, the designated subadvisor or, in the case of certain programs, the program sponsor or its designee. These materials are being provided for illustrative and informational purposes only. The information contained herein is obtained from multiple sources that are believed to be reliable. However, such information has not been verified, and may be different from the information included in documents and materials created by the sponsor firm in whose investment program a client participates. Some sponsor firms may require that these materials be preceded or accompanied by investment profiles or other documents or materials prepared by such sponsor firms, which will be provided upon a client's request. For additional information, documents and/or materials, please speak to your financial professional or contact your sponsor firm. INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE Introduction | Franklin Templeton Franklin Templeton We aim to offer the best of both worlds: global strength and boutique specialization. Providing real customization backed by the scale and -

Municipal Securities Transparency Subcommittee

Preliminary Recommendation Regarding Certain Principal Transactions with Advisory Clients Seeking to Liquidate Bond Positions The Municipal Securities Transparency Subcommittee (“Subcommittee”) of the Fixed Income Market Structure Advisory Committee (“FIMSAC”) was formed to consider the impact of transparency, both pre-trade and post-trade, on the municipal securities markets. As a result of such consideration, this Subcommittee determines whether to make policy recommendations to enhance the liquidity, transparency and efficiency of the municipal bond markets. Further, a mandate of FIMSAC is to consider policy recommendations to improve execution, access, and transparency of fixed-income markets with a specific emphasis on the retail investor. One area of focus of the Subcommittee has been on direct interactions where retail customers buy and sell individual bonds through their investment advisers or broker-dealers. In a traditional brokerage account, broker-dealers are required to provide a fair and reasonable price to their customer and meet best execution requirements. Mostly, broker-dealers with a customer looking to sell a bond will solicit bids from other market participants (dealers) and quite often may be willing to commit their own capital by providing a bid for the broker- dealers own account. In contrast, for advisory accounts held by broker-dealers that are also registered with the Securities and Exchange Commission (“SEC”) as investment advisers, broker-dealers are not permitted to enter a bid for the broker-dealer’s own account for their client wishing to sell a bond, without complying with the disclosure and consent requirements of the Investment Advisers Act of 1940 (“Advisers Act”). This could cause a client in an advisory account to receive a less favorable price, especially during volatile markets. -

Glossary of Municipal Finance Terms

Glossary of Municipal Finance Terms Accreted Value The Price of the Zero Coupon Bond on the Call Date as calculated using the original interest rate to maturity as the Yield, the Call Date as the Settlement Date, and the Maturity of the Bond. Accrued Interest Interest earned on a bond between the dated date (date interest starts accruing) and the date bonds are sold to the bond buyer. Accrued interest is normally paid by the bond buyer upon the purchase of a bond (interest accrued is added to the purchase price) and rebated back to the buyer by the issuer with the first payment. The buyer keeps the full coupon payment when it becomes due. Advance Refunding Financing transactions under which new bonds are issued to repay an outstanding bond issue prior to its first call date. Money raised from the new issue is usually placed in an escrow account and invested in government securities. The interest and principal repayments of these escrowed securities are used to pay the old bonds until they can be called. Ad Volrem Tax A tax based on assessed property value. Amortization A reduction of debt by means of periodic payments, which usually include current interest payments and principal payments sufficient to retire the debt (bond) at maturity. AMT Bonds The interest from certain tax-free municipal bonds is required to be included in the calculation of alternative minimum tax. These bonds are generally called AMT bonds. Qualified Small Issue bonds (IDBs) are AMT bonds along with other types of Private Activity bonds, excluding 501 (c)(3) bonds. -

Morningstar Global Fixed Income Classification Methodology

? Morningstar Global Fixed Income Classification Morningstar Research Introduction Effective Oct. 31, 2016 Fixed-Income Sectors Contents The fixed-income securities and fixed-income derivative exposures within a portfolio are mapped into 1 Introduction Secondary Sectors that represent the most granular level of classification. Each item can also be 2 Super Sectors 10 Sectors grouped into one of several higher-level Primary Sectors, which ultimately roll up to five fixed-income Super Sectors. Important Disclosure The conduct of Morningstar’s analysts is governed Cash Sectors by Code of Ethics/Code of Conduct Policy, Personal Cash securities and cash-derivative exposures within a portfolio are mapped into Secondary Sectors that Security Trading Policy (or an equivalent of), and Investment Research Policy. For information represent the most granular level of classification. Each item can also be grouped into cash & regarding conflicts of interest, please visit: http://global.morningstar.com/equitydisclosures equivalents Primary Sector and into cash & equivalents Super Sector (cash & equivalents Primary Sector = cash & equivalents Super Sector ). Morningstar includes cash within fixed-income sectors. Cash is not a bond, but it is a type of fixed- income. When bond-fund managers are feeling nervous about interest rates rising, they might increase their cash stake to shorten the portfolio’s duration. Moving assets into cash is a defensive strategy for interest-rate risk. In addition, Morningstar includes securities that mature in less than 92 days in the definition of cash. The cash & equivalents Secondary Sectors allow for more-detailed identification of cash, allowing clients to see, for example, if the cash holdings are in currency or short-term government bonds.