Quarterly Commentary—Artisan Mid Cap Fund (ARTMX, APDMX, APHMX)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Investment Report West Springfield

THE DE BURLO GROUP, INC. INVESTMENT ADVISORS • CAPITAL MANAGEMENT INVESTMENT REPORT WEST SPRINGFIELD MARCH 31, 2021 THE DE BURLO GROUP, INC. 50 FEDERAL STREET • 8th FL. • BOSTON • MASSACHUSETTS 02110 • PHONE 617.482.0275 • FAX 617.338.6077 West Springfield Retirement Board Investment Report for Quarter Ended March 31, 2021 For Meeting of April 27, 2021 The Economy Makes a Comeback, but it’s Far from Complete In late March, Fed Chair Jerome Powell once again credited the extraordinary efforts and “unprecedented” support of the central bank and Congress with the success of the economic recovery but was quick to state that the recovery was ongoing and “far from complete”. He went on to say, “…at the Fed, we will continue to provide the economy the support that it needs for as long as it takes.” The ambitious task of deploying an aggressive, effective, and equitable vaccination program coupled with renewed hiring aided by the scaffolding of supportive monetary and fiscal policy, is fueling America’s economic comeback and helping consumers to gain confidence. Analysts anticipate GDP growth to be 6.5% in 2022. More than 3 million vaccine doses are currently being administered daily in the U.S. Although these results are a sign of forward momentum, it is important to vaccinate 70% to 85% of the population in order to return to “normal”, according to experts. The pace of the vaccinations is also key as new variants continue to pose a threat to public health and to the economic recovery. Three Months Benchmarks* Ended 3/31/21 Dow Industrials 7.76% S&P 500 5.77% Russell 2000 12.44% NASDAQ Composite 2.78% MSCI Emerging Markets 1.95% MSCI EAFE Index 2.83% Crude Oil 21.93% Trade-weighted Dollar 2.85% Gold -10.04% 2 Year Treasury +4 basis points 10 Year Treasury +83 basis points Fed Funds Target Rate No Change * Please note the returns listed above refer to price changes only. -

CLRG IQ Chaikin U.S. Large Cap ETF Q3 Holdings

Schedule of Investments – IQ Chaikin U.S. Large Cap ETF January 31, 2021 (unaudited) Shares Value Shares Value Common Stocks — 99.8% Common Stocks (continued) Communication Services — 12.0% Health Care (continued) Activision Blizzard, Inc. 31,519 $ 2,868,229 Cigna Corp. .................... 10,581 $ 2,296,606 ............. Alphabet, Inc., Class A* 1,615 2,951,186 CVS Health Corp.................. 31,599 2,264,068 ............. AT&T, Inc. 64,314 1,841,310 Gilead Sciences, Inc. .............. 25,076 1,644,986 ..................... Comcast Corp., Class A 54,530 2,703,052 HCA Healthcare, Inc. .............. 20,865 3,390,145 ............ Facebook, Inc., Class A* 11,239 2,903,371 Humana, Inc. ................... 5,969 2,286,783 ............ Snap, Inc., Class A* 157,672 8,347,156 Johnson & Johnson ............... 14,297 2,332,270 ............... T-Mobile US, Inc.* 22,344 2,817,132 Medtronic PLC .................. 20,788 2,314,328 ................ Twitter, Inc.* 76,334 3,857,157 Merck & Co., Inc. ................. 24,365 1,877,810 .................... Verizon Communications, Inc. 34,891 1,910,282 Thermo Fisher Scientific, Inc. ......... 6,610 3,369,117 ........ Walt Disney Co. (The)* 19,406 3,263,507 UnitedHealth Group, Inc. ............ 7,516 2,507,187 ............. Zimmer Biomet Holdings, Inc. ......... 18,546 2,849,964 Total Communication Services 33,462,382 Total Health Care 38,541,333 Consumer Discretionary — 12.8% AutoZone, Inc.* 2,218 2,480,545 Industrials — 8.3% .................. Dollar General Corp. 12,414 2,415,888 Cintas Corp. .................... 10,821 3,442,376 .............. Home Depot, Inc. (The) 10,039 2,718,762 Cummins, Inc. ................... 13,855 3,247,889 ............ -

Alliant Techsystems, Inc

Appendix A General Industry Compensation Benchmark Group A&P Cincinnati Bell GTECH McDermott A.O. Smith Cintas H.B. Fuller McGraw-Hill Abercrombie & Fitch Clear Channel Communications H.J. Heinz MeadWestvaco AbitibiBowater Cliffs Natural Resources Hanesbrands Mecklenburg County ACH Food Clorox Harland Clarke Medtronic Activision Blizzard Coach Harley-Davidson Memorial Sloan-Kettering Cancer Center Acuity Brands Coinstar Hasbro Meredith Advanced Micro Devices Cole Haan HD Supply Metro-Goldwyn-Mayer Aeropostale Colgate-Palmolive Health Net Micron Technology Agilent Technologies Columbia Sportswear HealthSouth Millennium Inorganic Chemicals Agrium ConAgra Foods Hearst Millennium Pharmaceuticals Air Liquide Conde Nast Publications Henkel of America Millipore Air Products and Chemicals ConvaTec Henry Ford Health Systems Mizuno USA Alcoa Convergys Herman Miller Molson Coors Brewing Alcon Laboratories Cooper Industries Hershey Momentive Specialty Chemicals Alexander & Baldwin Corning Hertz Monsanto Allergan Covance Hexcel Mosaic Alpha Natural Resources Covidien HNI MTV Networks American Crystal Sugar Cox Enterprises Home Shopping Network Murphy Oil AMERIGROUP Cracker Barrel Old Country Stores Hormel Foods MWH Global AMETEK Crown Castle Hospira Nash-Finch Amgen Crown Holdings Host Hotels & Resorts National Starch Polymers Group Anadarko Petroleum CSC Houghton Mifflin Harcourt Publishing Navistar International Ann Taylor Stores CSM HR Access NCR AOL CSX Hunt Consolidated Neoris USA APL Curtiss-Wright Huntsman New York Times Applied Materials Cytec -

Hiring Our Heroes Employer List Houston, TX 2-Mar-16

Hiring Our Heroes Employer List Houston, TX 2-Mar-16 Company Name Website Aerospec Technologies LLC Aerospec.us AFPM https://www.afpm.org/ AIG Airstreams Renewables, Inc. www.air-streams.com AlliedBarton Security Services Aon http://jobs.aon.com/ Avis Budget Group https://abg.greatjob.net BASF Corporation BP http://www.bp.com CB&I http://www.cbi.com Cintas Corporation www.cintas.com/careers City of Houston - Environmental Services Cluster http://agency.governmentjobs.com/houston/default.cfm City of Houston, Department of Public Works and Engineering http://www.houstontx.gov/jobs Comcast Comerica Bank http://www.comerica.com Corner Store/CST Brands www.cornerstore.com Doubletree DT Houston http://jobs.hiltonworldwide.com/ E.A. Renfroe & Company http://www.earenfroe.com Emerson Exxon Mobil Corporation Fastport LLC http://fastport.com FDM Group http://www.fdmgroup.com/us/ First Command Financial Services www.wehireleaders.com Fluor Goodyear Tire & Rubber Co. http://www.goodyear.com Harris County Human Resources & Risk Management Harris County Sheriff's Office http://www.hcsojobs.com Harris County Toll Road Authority Hertz Equipment Rental hertzequip.com Hilton Americas-Houston www.Hiltonworldwide.com/militarycareers Hilton Houston Post Oak http://www3.hilton.com/en/hotels/texas/hilton-houston-post-oak-IAHWSHH/index.html Home Depot Houston Fire Department www.hfdcareers.org Houston Housing Authority http://www.housingforhouston.com/careers.aspx Houston ISD Apollo 20 Fellowship Program http://www.houstonisd.org/Page/116407 Houston Police Department http://www.hpdcareer.com/ Hunter Buildings http://www.hunterbuildings.com Igloo Products Corp Intel Corporation http://www.intel.com/content/www/us/en/homepage.html Jeppesen www.jeppesen.com KPMG http://www.kpmg.com/us/en/careers/pages/default.aspx McKesson www.mckesson.com Mercuria Energy Trading, Inc. -

Impact Shares NAACP Minority Empowerment ETF Schedule of Investments September 30, 2020 (Unaudited)

Impact Shares NAACP Minority Empowerment ETF Schedule of Investments September 30, 2020 (Unaudited) Description Shares Fair Value Description Shares Fair Value Hannon Armstrong Sustainable COMMON STOCK†† — 97.4% Infrastructure Capital‡ .... 1,418 $ 59,939 Hartford Financial Services Communication Services— 11.3% Group .............. 239 8,810 Alphabet, Cl A* .......... 157 $ 230,099 Huntington Bancshares ..... 728 6,676 Alphabet, Cl C* .......... 151 221,910 JPMorgan Chase ......... 2,051 197,450 AT&T ................ 4,561 130,034 KeyCorp .............. 696 8,303 Comcast, Cl A ........... 2,932 135,634 Moody's .............. 99 28,695 Verizon Communications .... 2,671 158,898 Morgan Stanley .......... 764 36,939 Walt Disney ............ 1,151 142,816 Prudential Financial ....... 256 16,261 S&P Global ............ 137 49,402 1,019,391 State Street ............ 220 13,053 Consumer Discretionary— 13.1% US Bancorp ............ 943 33,806 Wells Fargo ............ 2,625 61,714 Amazon.com* ........... 167 525,838 Aptiv ................. 113 10,360 818,366 Autoliv ................ 53 3,863 Best Buy .............. 143 15,914 Health Care— 14.4% Carnival ............... 218 3,309 Abbott Laboratories ....... 1,107 120,475 eBay ................. 364 18,964 AbbVie ............... 1,121 98,189 Ford Motor ............. 2,529 16,843 Agilent Technologies ...... 200 20,188 Gap ................. 123 2,095 Baxter International ....... 329 26,458 General Motors .......... 844 24,974 Becton Dickinson ........ 180 41,882 Hanesbrands ........... 218 3,434 Biogen* ............... 102 28,935 Hasbro ............... 75 6,204 Bristol-Myers Squibb ...... 1,455 87,722 Hilton Worldwide Holdings ... 179 15,272 Cardinal Health .......... 201 9,437 Home Depot ............ 703 195,230 CVS Caremark .......... 865 50,516 Marriott International, Cl A ... 168 15,553 Eli Lilly .............. -

EQUITY RESEARCH MORNING RESEARCH SUMMARY July 16, 2014

EQUITY RESEARCH MORNING RESEARCH SUMMARY July 16, 2014 What's Inside Focus Items Initiation Country Allocation Samuel Burns, CFA UNFI O United Natural Foods Inc. Portfolio Strategy Country Allocation July 2014 Estimates & PT Revisions INDUSTRIAL/CAPITAL GOODS Christopher Glynn CTAS P ¯ Cintas Corporation 2Q14 Industrial Preview GS P Goldman Sachs Group INTC P Intel Corp. TECHNOLOGY Andrew Uerkwitz 2 Up, 1 Down SYNA P Synaptics, Incorporated TSCO P ¯ Tractor Supply Company Yahoo! Inc. (YHOO) Jason Helfstein YHOO O Yahoo! Inc. Core Results Below Expectations, But Will Maintain Larger Post- IPO Stake Estimates/Ratings/Price Target Updates Annual Estimates Tractor Supply Company (TSCO) Brian Nagel, CFA Current FY Next FY Ratings Price Targets Still Not the Time to Jump into TSCO Company Ticker Prev Curr Prev Curr Prev Curr Prev Curr Other Headlines Intel Corp. (INTC) Rick Schafer Cintas CTAS 3.04 3.00 3.36 3.36 P P NA NA Corporation Solid Print and Guidance, Driven by PC & Data Center Goldman Sachs GS 16.50 17.12 17.61 18.50 P P NA NA Group TECHNOLOGY Rick Schafer Intel Corp. INTC 1.94 2.13 1.84 2.15 P P NA NA Daily Chip Clips Synaptics, SYNA 4.15 4.15 -- -- P P NA NA Incorporated United Natural Foods Inc. (UNFI) Rupesh Parikh, CFA Tractor Supply TSCO 2.64 2.55 3.05 2.90 P P $70.00 $60.00 Pullback Creates an Attractive Entry Point; Initiating with an Company Outperform Rating Yahoo! Inc. YHOO 1.52 1.28 1.82 0.94 O O $40.00 $43.00 Cintas Corporation (CTAS) Scott Schneeberger, CFA Solid F4Q14; FY15 Adjusted EPS Guidance Consistent with Consensus Goldman Sachs Group (GS) Chris Kotowski Solid 2Q14 Beat On Investing & Lending, Assist By FICC Oppenheimer & Co. -

Hot Jobs! Week of May 1St to May 5Th 2017

Hot Jobs! Week of May 1st to May 5th 2017 City of Renton Job Fair Wednesday May 3rd 3pm to 6pm Location: Renton Technical College 3000 NE 4th St – Roberts Campus Center, Building I 50 Employers that are motivated to hire! (For a list of employers and shuttle times), http://chamber.gorenton.com/events/details/2017-renton-career-fair-4008 0r https://bit.ly/RCF2017 Airport Terminal Services Hiring Event! Thursday May 4th, 2017 10am-1pm Location: Airport Jobs Office at SeaTac Airport Mezzanine Level, Room 6626 Looking for Ramp Agents!! $15.34/hr Part-time 20-30 hours per week with Paid training and flight benefits! Bring resume and/or apply online www.atsstl.com prior to the event. Special requirements: Must be 18 years or older with a Diploma or GED or work experience Proficient in speaking, reading and writing English Currently have a valid driver’s license Be able to lift up to 70 lbs. Have a flexible work schedule Pass a background screening and drug test Must be 16+ Who is Hiring? Pedalheads Bike Camps What is the Position? Site Instructor for Summer Youth Program What is the Pay Rate? $13.00 – 15.60/hour depending on location Where is the Location? Seattle, Bellevue, Redmond, Shoreline When to Apply? ASAP How to Apply? Apply online at: https://www.jotform.com/AtlantisandPedalheads/2017- Washington-PH-Application Special Requirements: Must be at least 15yrs of age by June 1st, 2017 Posted by WorkSource Business Services Who is Hiring? City of Burien What is the Position? Recreation Leader 1 Where is the Location? Burien When to Apply? ASAP How to Apply? Apply on line at: http://www.burienwa.gov/DocumentCenter/View/3860 Special Requirements: Must be at least 15yrs of age. -

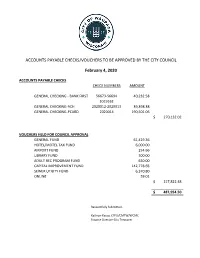

Council Payment Authorization Report 2-4-20

ACCOUNTS PAYABLE CHECKS/VOUCHERS TO BE APPROVED BY THE CITY COUNCIL February 4, 2020 ACCOUNTS PAYABLE CHECKS CHECK NUMBERS AMOUNT GENERAL CHECKING - BANK FIRST 56673-56694 40,232.58 2019162 GENERAL CHECKING-ACH 2020012-2020013 39,398.38 GENERAL CHECKING-PCARD 2020014 190,501.06 $ 270,132.02 VOUCHERS HELD FOR COUNCIL APPROVAL GENERAL FUND 61,429.36 HOTEL/MOTEL TAX FUND 6,000.00 AIRPORT FUND 254.66 LIBRARY FUND 300.00 ADULT REC PROGRAM FUND 630.00 CAPITAL IMPROVEMENT FUND 142,778.65 SEWER UTILITY FUND 6,370.80 ONLINE 59.01 $ 217,822.48 $ 487,954.50 Respectfully Submitted, Kathryn Kasza, CPFO/CMTW/WCMC Finance Director-City Treasurer CITY OF WAUPACA CITY OF WAUPACA COUNCIL CHECK REGISTER Page: 1 Check Issue Dates: 1/22/2020 - 1/31/2020 Jan 31, 2020 11:27AM Check Check Invoice Date Invoice Description Check Invoice Invoice GL Account Title Issue Date Number Payee Number Amount GL Account 55617 01/24/2020 55617 BUNGE, LOGAN 05/24/2019 MAY 2019 MEN'S SOFTBALL 25.00- 252-55219-232-000 ADULT SOFTBALL: UMPS, ETC V Total 55617: 25.00- 55677 01/24/2020 55677 WITTMAN, BRENT 05/17/2019 19170 TRAINING REIMBURSEMENT 14.15- 100-52112-111-000 POL PATROL: MEALS V Total 55677: 14.15- 55707 01/24/2020 55707 ZIEBELL, SAM 06/04/2019 WWTP90663 DNR WASTEWATER EXAM FEE 25.00- 620-83210-202-000 OTHER GEN EXP: TRAINING V Total 55707: 25.00- 56673 01/24/2020 56673 BUNGE, LOGAN 05/24/2019 MAY 2019 MEN'S SOFTBALL 25.00 252-55219-232-000 ADULT SOFTBALL: UMPS, ETC Total 56673: 25.00 56674 01/24/2020 56674 WITTMAN, BRENT 05/17/2019 19170 TRAINING REIMBURSEMENT 14.15 -

City of La Porte Fiscal Affairs Committee Meeting Agenda

CHUCK ENGELKEN, CHAIR THOMAS GARZA Councilmember, District 2 Councilmember, District 4 Alternate JAY MARTIN VACANT Councilmember, District 5 CITY OF LA PORTE FISCAL AFFAIRS COMMITTEE MEETING AGENDA Notice is hereby given of a meeting of the City of La Porte Fiscal Affairs Committee to be held on July 26, 2021, in the City Hall Council Chamber, 604 West Fairmont Parkway, La Porte, Texas, beginning at 5:00 pm regarding the items of business according to the agenda listed below: Remote participation is available. Attend via a screen using this link: https://us02web.zoom.us/j/86779605862?pwd=V1pjTXVHNnp4ZjI0NG9tYnJtVWdmUT09. Join by phone at 877-853-5257 or 888-475-4499. The meeting ID is 867 7960 5862 and the passcode is 276435. 1. CALL TO ORDER 2. CITIZEN COMMENT (Generally limited to five minutes per person; in accordance with state law, the time may be reduced if there is a high number of speakers or other considerations.) 3. STATUTORY AGENDA (a) Presentation, discussion, and possible action to approve the minutes of the March 22, 2021, meeting. [Chair Engelken] (b) Presentation, discussion, and possible action to receive and review Purchasing Card expenditures for March, April, and May 2021. [Cherell Daeumer, Purchasing Manager] (c) Presentation, discussion, and possible action to receive and review the Third Quarter (FY2021) Investment Report. [Shelley Wolny, Asst. Finance Director] 4. SET NEXT MEETING 5. COMMITTEE COMMENT Hear announcements concerning matters appearing on the agenda; items of community interest; and/or inquiries of staff regarding specific factual information or existing policy from the Committee members and City staff, for which no formal action will be discussed or taken. -

Cintas (CTAS) Is the Largest US Uniform Rental and Facility Services Business with >1M Customers and >11,000 Delivery Routes

Tanya Kostrinsky Value Investing with Legends Cintas (NASDAQ: CTAS) – Buy May 5, 2020 % Ups ide / Margin of Current Stock Price: $211.81 Valuation Approach Dow ns ide Safety Target Price $295.78 25x Base Case FY23 EBIT 39.6% 28.4% Bear Case Price $180.40 18x Bear Case FY23 EBIT -14.8% Historicals Forecast $m FY ends 5/31 2015 2016 2017 2018 2019 2020E 2021E 2022E 2023E Price $211.81 Uniform Rental and Facility Services 3,519 3,760 4,202 5,247 5,552 5,441 4,897 5,142 5,656 FSDO (m) 104.1 Yoy % -- 6.8% 11.8% 24.9% 5.8% -2.0% -10.0% 5.0% 10.0% Market Cap $22,039 All Other 850 1,036 1,121 1,230 1,340 1,405 1,425 1,530 1,629 Plus: Debt 2,739 Yoy % -- 21.8% 8.2% 9.7% 9.0% 4.8% 1.4% 7.4% 6.5% Less: Cash 234 Revenue 4,370 4,796 5,323 6,477 6,892 6,846 6,322 6,672 7,285 Enterprise Value $24,543 Yoy % -- 9.8% 11.0% 21.7% 6.4% -0.7% -7.7% 5.5% 9.2% EV /EBIT LTM 19.3x Uniform Rental and Facility Services 604 672 756 860 991 958 767 865 1,020 Dividend Yield 1.1% EBIT margin % 17.2% 17.9% 18.0% 16.4% 17.9% 17.6% 15.7% 16.8% 18.0% All Other 80 97 97 132 157 168 165 178 203 Debt/Capital 45.2% EBIT margin % 9.4% 9.3% 8.6% 10.8% 11.7% 11.9% 11.6% 11.6% 12.5% Net Debt/LTM EBITDA 1.5x EBIT 684 769 853 992 1,148 1,126 933 1,043 1,223 Short Interest 1.8% EBIT margin % 15.6% 16.0% 16.0% 15.3% 16.7% 16.4% 14.8% 15.6% 16.8% EBIT yoy % -- 12% 11% 16% 16% -2% -17% 12% 17% Net Income 431 694 481 843 885 820 666 754 898 Yoy % -- 61% -31% 75% 5% -7% -19% 13% 19% Net Margin % 9.9% 14.5% 9.0% 13.0% 12.8% 12.0% 10.5% 11.3% 12.3% EPS$ 3.63 $ 6.21 $ 4.38 $ 7.56 $ 7.99 $ 7.88 $ 6.40 $ 7.24 $ 8.63 Yoy % -- 71% -29% 73% 6% -1% -19% 13% 19% Capex 218 275 273 272 277 250 200 185 225 % Sales 5.0% 5.7% 5.1% 4.2% 4.0% 3.7% 3.2% 2.8% 3.1% FCF/Share$ 3.06 $ 1.71 $ 4.47 $ 6.21 $ 7.14 $ 10.38 $ 10.68 $ 9.04 $ 9.13 FCF Yield % 1.4% 0.8% 2.1% 2.9% 3.4% 4.9% 5.0% 4.3% 4.3% ROIC 24.3% 25.7% 16.2% 18.3% 19.9% 20.0% 17.5% 19.7% 22.7% Note: Market data as of 5/1/20. -

Top 25 Employers from Online Ads Washington State and Counties

Top 25 employers from online ads Washington state and counties, October 2020 through January 2021 Source: Employment Security Department/LMEA; The Conference Board® Burning Glass® Help Wanted OnLine™ Geographic areas Washington state Adams Asotin Benton Chelan Clallam Clark Columbia Cowlitz Douglas Ferry Franklin Garfield Grant Grays Harbor Island Jefferson King Kitsap Kittitas Klickitat Lewis Lincoln Mason Okanogan Pacific Pend Oreille Pierce San Juan Skagit Skamania Snohomish Spokane Stevens Thurston Wahkiakum Walla Walla Whatcom Whitman Yakima Employment Security Department is an equal opportunity employer/programs. Auxiliary aids and services are available upon request to individuals with disabilities. Language assistance services for limited English proficient individuals are available free of charge. Washington Relay Service: 711 Top 25 employers from online ads Return to content Washington state, October 2020 through January 2021 Source: Employment Security Department/LMEA; The Conference Board® Burning Glass® Help Wanted OnLine™ Rank Employer Number 1 Amazon 12,204 2 University of Washington 2,806 3 Microsoft Corporation 2,330 4 Providence Health & Services 1,634 5 Allied Universal 1,186 6 Providence 1,172 7 Lowe's Companies, Inc 1,087 8 The Home Depot Incorporated 978 9 Swedish Health Service 940 10 Washington Department Of Health 906 11 Facebook 845 12 PeaceHealth 829 13 Salesforce 808 14 Soliant 785 15 T Mobile Usa Incorporated 781 16 Nordstrom 762 17 Kaiser Permanente 727 18 Fred Meyer 676 19 Anthem Blue Cross 636 20 King County -

View Annual Report

2003 ANNUAL REPORT The is the Difference THE UNIFORM PEOPLE Cintas Corporation provides highly specialized services to businesses of all types throughout North America. We design, manufacture, and implement corporate identity uniform programs, provide entrance mats, restroom supplies, promotional products, and first aid and safety products for over 500,000 businesses. One Source, One Company, One Answer TABLE OF CONTENTS Accomplishments 2 Financial Highlights 3 Letter to Shareholders 4 Uniform Rental Business 10 Uniform Sales Business 12 Facility Services 14 First Aid and Safety Supplies 16 Cleanroom 18 Flame Resistant Clothing 20 Partner Success Stories 23 Eleven Year Financial Summary 31 Financial Statements and Notes 32 Management’s Discussion and Analysis 57 Directors and Officers 66 Shareholder Information 67 THE UNIFORM PEOPLE Celebrating THE SPIRIT THAT IS CINTAS Fiscal 2003 Accomplishments Financial, operating and recognition highlights for fiscal year 2003 for Cintas Corporation. • Achieved 34th consecutive year of uninterrupted growth in sales and profits. Only two other companies have achieved longer standing records—ADP and Wal-Mart • Revenue was a record $2.69 billion, up 18 percent • Achieved record profits of $249 million, up 6 percent • Increased dividends by 8 percent. Mergent calls Cintas a “Dividend Achiever”, a distinction given to the top 2.5 percent of all dividend-paying companies • Expanded uniform rental presence into 13 new cities • Opened six new state-of-the-art uniform rental plants • Expanded First Aid and