A History of Insurance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Advantages and Disadvantages of Different Social Welfare Strategies

Throughout the world, societies are reexamining, reforming, and restructuring their social welfare systems. New ways are being sought to manage and finance these systems, and new approaches are being developed that alter the relative roles of government, private business, and individ- uals. Not surprisingly, this activity has triggered spirited debate about the relative merits of the various ways of structuring social welfare systems in general and social security programs in particular. The current changes respond to a vari- ety of forces. First, many societies are ad- justing their institutions to reflect changes in social philosophies about the relative responsibilities of government and the individual. These philosophical changes are especially dramatic in China, the former socialist countries of Eastern Europe, and the former Soviet Union; but The Advantages and Disadvantages they are also occurring in what has tradi- of Different Social Welfare Strategies tionally been thought of as the capitalist West. Second, some societies are strug- by Lawrence H. Thompson* gling to adjust to the rising costs associated with aging populations, a problem particu- The following was delivered by the author to the High Level American larly acute in the OECD countries of Asia, Meeting of Experts on The Challenges of Social Reform and New Adminis- Europe, and North America. Third, some trative and Financial Management Techniques. The meeting, which took countries are adjusting their social institu- tions to reflect new development strate- place September 5-7, 1994, in Mar de1 Plata, Argentina, was sponsored gies, a change particularly important in by the International Social Security Association at the invitation of the those countries in the Americas that seek Argentine Secretariat for Social Security in collaboration with the ISSA economic growth through greater eco- Member Organizations of that country. -

Policyholder Disclosure Notice of Terrorism Insurance Coverage

POLICYHOLDER DISCLOSURE NOTICE OF TERRORISM INSURANCE COVERAGE You are hereby notified that under the Terrorism Risk Insurance Act, as amended, that you have a right to purchase insurance coverage for losses resulting from acts of terrorism, as defined in Section 102(1) of the Act: The term “act of terrorism” means any act that is certified by the Secretary of the Treasury – in concurrence with the Secretary of State, and the Attorney General of the United States – to be an act of terrorism; to be a violent act or an act that is dangerous to human life, property, or infrastructure; to have resulted in damage within the United States, or outside the United States in the case of certain air carriers or vessels or the premises of a United States mission; and to have been committed by an individual or individuals as part of an effort to coerce the civilian population of the United States or to influence the policy or affect the conduct of the United States Government by coercion. YOU SHOULD KNOW THAT WHERE COVERAGE IS PROVIDED BY THIS POLICY FOR LOSSES RESULTING FROM CERTIFIED ACTS OF TERRORISM, SUCH LOSSES MAY BE PARTIALLY REIMBURSED BY THE UNITED STATES GOVERNMENT UNDER A FORMULA ESTABLISHED BY FEDERAL LAW. HOWEVER, YOUR POLICY MAY CONTAIN OTHER EXCLUSIONS WHICH MIGHT AFFECT YOUR COVERAGE, SUCH AS AN EXCLUSION FOR NUCLEAR EVENTS. UNDER THIS FORMULA, THE UNITED STATES GOVERNMENT GENERALLY PAYS 85% OF COVERED TERRORISM LOSSES EXCEEDING THE STATUTORILY ESTABLISHED DEDUCTIBLE PAID BY THE INSURANCE COMPANY PROVIDING THE COVERAGE. THE PREMIUM CHARGED FOR THIS COVERAGE IS PROVIDED BELOW AND DOES NOT INCLUDE ANY CHARGES FOR THE PORTION OF LOSS THAT MAY BE COVERED BY THE FEDERAL GOVERNMENT UNDER THE ACT. -

Alabama Credit Unions & Banker Myths

Alabama Credit Unions & Banker Myths Bumper profits and a massive concentration of market share aren’t enough for Alabama’s bankers. They want more. And they seem willing to do anything to get it. Indeed, banking industry publications recently distributed to state policy-makers use anecdotes, half-truths, and innuendo in an all-out assault the state’s credit unions. While its true that Alabama credit unions are growing, they aren’t, as bankers suggest, taking over the world. They remain true to their original purpose. And they certainly aren’t harming the state’s banks. Growth: Banking institution deposits in Alabama grew by $10.2 billion in the 88% ISN'T ENOUGH? five years ending June 2003. Since 1998 Alabama banking deposits have grown Alabama Bankers Want More 22% more than the total growth Market Share! recorded by the state’s’ credit unions (Mid-Year 2003 Deposits) since credit unions began operating in the state in 1927! Largest 10 Banks Market Share: Banking institutions 58% control 88% of all financial institution Smaller deposits in the state of Alabama – a CUs market share that is virtually unchanged 5% over the past decade. Small banks in Alabama have a lot more Largest 10 significant competitive threats to worry CUs Smaller 7% about than the threat of credit union Banks competition. Indeed, at the mid-year 30% 2003, the largest 10 banking institutions control 58% of total deposits in the state (or 66% of total banking deposits). In contrast, credit unions control just 12% of the market and the largest 10 credit unions control just 7% of the deposit market in Alabama. -

Employment Practices Liability Insurance Program EPLI

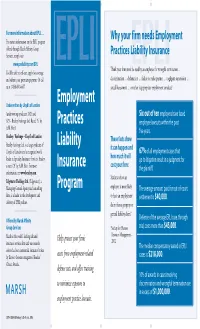

B5848_EPLI 2/14/06 2:49 PM Page 1 For more information about EPLI … Why your firm needs Employment For instant information on the EPLI program offered through Marsh Affinity Group Services, simply visit Practices Liability Insurance www.proliablity.com/EPLI Think your firm won’t be sued by an employee for wrongful termination … You’ll be able to self-rate, apply for coverage EPLI EPLI and submit your premium payment. Or call discrimination … defamation … failure to make partner … negligent supervision … us at 1-888-601-6667. sexual harassment … or other inappropriate employment conduct? Underwritten by Lloyd’s of London Employment (underwriting syndicates 2623 and Six out of ten employers have faced 623 – Beazley Furlonge Ltd. Rated “A” by Practices employee lawsuits within the past A.M. Best) five years. Beazley / Furlonge – Lloyd’s of London These facts show Beazley Furlonge Ltd. is a large syndicate of Liability it can happen and Lloyd’s of London and a recognized world 67% of all employment cases that leader in Specialty Insurance Services. Beazley how much it will go to litigation result in a judgment for is rated “A” by A.M. Best. For more Insurance cost your firm: the plaintiff. information, see www.beazley.com. Statistics show an Edgewater Holdings Ltd. (Edgewater), a Managing General Agency and consulting Program employer is more likely The average amount paid for out-of-court firm, is a leader in the development and to have an employment settlement is $40,000. delivery of EPLI policies. claim than a property or general liability claim.* Offered by Marsh Affinity Defense of the average EPLI case, through Group Services *Society for Human trial, costs more than $45,000. -

THE FREE-MARKET WELFARE STATE: Preserving Dynamism in a Volatile World

Policy Essay THE FREE-MARKET WELFARE STATE: Preserving Dynamism in a Volatile World Samuel Hammond1 Poverty and Welfare Policy Analyst Niskanen Center May 2018 INTRODUCTION welfare state” directly depresses the vote for reac- tionary political parties.3 Conversely, I argue that he perennial gale of creative destruc- the contemporary rise of anti-market populism in tion…” wrote the economist Joseph America should be taken as an indictment of our in- 4 Schumpeter, “…is the essential fact of adequate social-insurance system, and a refutation “T of the prevailing “small government” view that reg- capitalism.” For new industries to rise and flourish, old industries must fail. Yet creative destruction is ulation and social spending are equally corrosive to a process that is rarely—if ever—politically neu- economic freedom. The universal welfare state, far tral; even one-off economic shocks can have lasting from being at odds with innovation and economic political-economic consequences. From his vantage freedom, may end up being their ultimate guaran- point in 1942, Schumpeter believed that capitalism tor. would become the ultimate victim of its own suc- The fallout from China’s entry to the World Trade cess, inspiring reactionary and populist movements Organization (WTO) in 2001 is a clear case in against its destructive side that would inadvertently point. Cheaper imports benefited millions of Amer- strangle any potential for future creativity.2 icans through lower consumer prices. At the same This paper argues that the countries that have time, Chinese import competition destroyed nearly eluded Schumpeter’s dreary prediction have done two million jobs in manufacturing and associated 5 so by combining free-markets with robust systems services—a classic case of creative destruction. -

Social Insurance Law PART 1

Social Insurance Law PART 1: THE CONSOLIDATED ACT ON SOCIAL INSURANCE CHAPTER I THE REGULATION OF SOCIAL INSURANCE, SCOPE OF APPLICATION AND DEFINITIONS Article 1 This Law shall be cited as "The Social Insurance Law" and shall include the following branches of Insurance :- 1. Insurance against old age, disability and death; 2. Insurance against employment injuries; 3. Insurance against temporary disability by reason of sickness or maternity; 4. Insurance against unemployment; 5. Insurance for the self-employed and those engaged in liberal professions; 6. Insurance for employers; 7. Family Allowances; 8. Other branches of insurance which fall within the scope of social security. Each of the first two branches shall be introduced in accordance with the following provisions and the protection guaranteed by this Law shall be extended in future stages by introducing the other branches of social insurance by Order of the Council of Ministers. Article 2 The provisions of this Law shall be applied compulsorily to all workers without discrimination as to sex, nationality, or age, who work by virtue of an employment contract for the benefit of one or more employers, or for the benefit of an enterprise in the private, co-operative, or para-statal sectors and, unless otherwise provided for, those engaged in public organisations or bodies, and also those employees and workers in respect of whom Law No. 13 of 1975 does not apply, and irrespective of the duration, nature or form of the contract, or the amount or kind of wages paid or whether the service is performed in accordance with the contract within the country or for the benefit of the employer outside the country or whether the assignment to work abroad is for a limited or an unlimited period. -

Consumers Guide to Auto Insurance

CONSUMERS GUIDE TO AUTO INSURANCE PRESENTED TO YOU BY THE DEPARTMENT OF BUSINESS REGULATION INSURANCE DIVISION 1511 PONTIAC AVENUE, BLDG 69-2 CRANSTON, RI 02920 TELEPHONE 401-462-9520 www.dbr.ri.gov Elizabeth Kelleher Dwyer Superintendent of Insurance TABLE OF CONTENTS Introduction………………………………………………………………1 Underwriting and Rating………………………………………………...1 What is meant by underwriting and how is it accomplished…………..1 How are rates and premium charges determined in Rhode Island……1 What factors are considered in ratemaking……………………………. 2 What discounts are used in determining final premium cost…………..3 Rhode Island Automobile Insurance Plan…………………..…………..4 Regulation of Rates……………………………………………………….4 The Tort System…………………………………………………………..4 Liability Coverages………………………………………………………..5 Coverages Other Than Liability…………………………………………5 Physical Damage to the Automobile……………………………………..6 Other Optional Coverages………………………………………………..6 The No-Fault System……………….……………………………………..7 Smart Shopping……………………………………………………………7 Shop for True Comparison………………………………………………..8 Consumer Protection Available...…………………………………………8 What to Do if You are in an Automobile Accident………………………9 Your State Insurance Department………………………………….........9 Auto Insurance Buyer’s Worksheet…………………………………….10 Introduction Auto insurance is an expensive purchase for most Americans, and is especially expensive for Rhode Islanders. Yet consumers rarely comparison-shop for auto insurance as they might for other products and services. Auto insurance companies vary substantially both in price and service to policyholders, so it pays to shop around and compare different insurance companies. This guide to buying auto insurance was developed to help you become a more knowledgeable policyholder and to get the combination of price and service best suited to your needs. It provides information on how to shop for coverage and how insurance premiums are determined. You will also find an Auto Insurance Buyer’s Worksheet in the guide to help you compare premium prices among insurers. -

TRIA's Failure to Encourage a Private Market for Terrorism Insurance And

Terror CATs: TRIA’s Failure to Encourage a Private Market for Terrorism Insurance and How Federal Securitization of Terrorism Risk May Be a Viable Alternative Andrew Gerrish∗ Table of Contents I. Introduction ............................................................................ 1826 II. The Structure of TRIA ............................................................ 1831 III. Private Market’s Failure to Create a Long-Term Solution to Terrorism Risk ..................................................... 1833 A. Mandatory/Discretionary Recovery ................................. 1833 B. Large Insurers Can Game TRIA ...................................... 1840 C. Lack of Information Sharing ............................................ 1843 D. TRIA Creates Regulatory Certainty ................................. 1846 E. Insurers Believe They Can Rely on Traditional Coverage Exclusions........................................................ 1848 F. TRIA Displaces Traditional Private Reinsurance ............. 1850 IV. Why Continuing Under TRIA in Its Current Form Is Not Attractive ......................................................................... 1850 V. Proposed Alternatives to TRIA ............................................... 1852 A. Alteration of the Tax Code to Allow Insurers to Build Additional Reserves ........................................... 1852 B. Creation of Terrorism Insurance Pools ............................ 1854 VI. Federal Terror CATs .............................................................. 1856 A. Risk -

786-1 Credit for Reinsurance Model Regulation

NAIC Model Laws, Regulations, Guidelines and Other Resources—Summer 2019 CREDIT FOR REINSURANCE MODEL REGULATION Table of Contents Section 1. Authority Section 2. Purpose Section 3. Severability Section 4. Credit for Reinsurance—Reinsurer Licensed in this State Section 5. Credit for Reinsurance—Accredited Reinsurers Section 6. Credit for Reinsurance—Reinsurer Domiciled in Another State Section 7. Credit for Reinsurance—Reinsurers Maintaining Trust Funds Section 8. Credit for Reinsurance––Certified Reinsurers Section 9. Credit for Reinsurance—Reciprocal Jurisdictions Section 10. Credit for Reinsurance Required by Law Section 11. Asset or Reduction from Liability for Reinsurance Ceded to Unauthorized Assuming Insurer Not Meeting the Requirements of Sections 4 Through 10 Section 12. Trust Agreements Qualified Under Section 11 Section 13. Letters of Credit Qualified Under Section 11 Section 14. Other Security Section 15. Reinsurance Contract Section 16. Contracts Affected Form AR-1 Certificate of Assuming Insurer Form CR-1 Certificate of Certified Reinsurer Form RJ-1 Certificate of Reinsurer Domiciled in Reciprocal Jurisdiction Form CR-F Form CR-S Section 1. Authority This regulation is promulgated pursuant to the authority granted by Sections [insert applicable section number] and [insert applicable section number] of the Insurance Code. Section 2. Purpose The purpose of this regulation is to set forth rules and procedural requirements that the commissioner deems necessary to carry out the provisions of the [cite state law equivalent to the Credit for Reinsurance Model Law (#785)] (the Act). The actions and information required by this regulation are declared to be necessary and appropriate in the public interest and for the protection of the ceding insurers in this state. -

Admiralty, Maritime & Naval

30 ANTIQUARIAN TITLES ON ADMIRALTY, MARITIME & NAVAL LAW May 10, 2016 The Lawbook Exchange, Ltd. (800) 422-6686 or (732) 382-1800 | Fax: (732) 382-1887 [email protected] | www.lawbookexchange.com 30 Antiquarian Titles on Admiralty, Maritime and Naval Law Scarce Eighteenth-Century Treatise on Prize Law and Privateering 1. Abreu y Bertodano, Felix Joseph de [c.1700-1775]. Traite Juridico-Politique sur les Prises Maritimes, et Sur les Moyens qui Doivent Concourir pour Rendre ces Prises Legitimes. Paris: Chez la Veuve Delaguette, 1758. Two volumes in one, each with title page and individual pagination. Octavo (6-1/2" x 4"). Contemporary speckled sheep, raised bands, lettering piece and gilt ornaments to spine, speckled edges, patterned endpapers. Some wear to corners, joints starting, some worming to lettering piece, joints and hinges. Attractive woodcut head-pieces. Toning to sections of text, light foxing to a few leaves, internally clean. An appealing copy of a scarce title. $1,500. * Second French edition. First published in Madrid in 1746, this treatise on prize law and privateering went through three other editions, all in France in a translation by the author, in 1753, 1758 and 1802. Little is known about Abreu, a minor Spanish noble and diplomat. According to the title page, he was a "membre de l'Academie Espagnole, & actuellement Envoye Extraordinaire de S.M. Catholique aupres du Roi de la Grande-Bretagne." All editions are scarce. OCLC locates 5 copies of all editions in the Americas, 1 of this edition (at Columbia University Law Library). Not in the British Museum Catalogue. -

Insurance Companies Axa, Zurich, and Swiss Re: Divestment in Canadian Oil and Gas Compared with Their Investments in “Not Free” Countries

Insurance Companies Axa, Zurich, and Swiss Re: Divestment in Canadian Oil and Gas Compared with Their Investments in “Not Free” Countries CEC Research Brief Ten Lennie Kaplan and Mark Milke Table of contents Page Executive Summary 1 Introduction 4 Overview of the Worldwide Insurance Industry 5 Key Findings 6 Axa, Zurich, and Swiss Re investments in “Not Free” countries 6 Axa, Zurich, and Swiss Re Property and Casualty (P&C) insurance 6 premiums in “Not Free countries Breakdowns by company 8 Axa 8 Zurich Insurance 9 Swiss Re 10 Summary 12 References 12 About CEC Research Briefs 13 About the authors 13 Acknowledgements 13 Insurance Companies Axa, Zurich, and Swiss Re: Divestment in Canadian Oil & Gas Compared with Their Investments in “Not Free” Countries Executive summary Insurance companies Axa, Swiss Re, and While these companies have apparently bowed to pressure Zurich versus Canadian oil and gas from some anti-oil and gas activists to curtail their investments in Canadian oil and gas, they continue to invest Property and casualty (P&C) insurance allows oil and gas in other countries, including those considered “Not Free.” companies to protect themselves against such events as This report profiles the investments and insurance coverage damage to property, accidents and other incurred liabilities. of these three insurers in Not Free countries2, where civil and other rights, labour standards and environmental According to HTF Market Intelligence, the size of the oil and performances are often far below those of Free countries. gas property and casualty (P&C) insurance premiums market was about $17.3 billion in 2018. -

Credit for Reinsurance Model Regulation

Model Regulation Service—January 1997 CREDIT FOR REINSURANCE MODEL REGULATION Table of Contents Section 1. Authority Section 2. Purpose Section 3. Severability Section 4. Credit for Reinsurance—Reinsurer Licensed in this State Section 5. Credit for Reinsurance—Accredited Reinsurers Section 6. Credit for Reinsurance—Reinsurer Domiciled and Licensed in Another State Section 7. Credit for Reinsurance—Reinsurers Maintaining Trust Funds Section 8. Credit for Reinsurance Required by Law Section 9. Asset or Reduction from Liability for Reinsurance Ceded to Unauthorized Assuming Insurer Not Meeting the Requirements of Sections 4 Through 8 Section 10. Trust Agreements Qualified Under Section 9 Section 11. Letters of Credit Qualified Under Section 9 Section 12. Other Security Section 13. Reinsurance Contract Section 14. Contracts Affected Form AR-1 Certificate of Assuming Insurer Section 1. Authority This regulation is promulgated pursuant to the authority granted by Sections [insert applicable section number] and [insert applicable section number] of the Insurance Code. Section 2. Purpose The purpose of this regulation is to set forth rules and procedural requirements that the commissioner deems necessary to carry out the provisions of the [cite state law equivalent to the Credit for Reinsurance Model Law] (the Act). The actions and information required by this regulation are declared to be necessary and appropriate in the public interest and for the protection of the ceding insurers in this state. Section 3. Severability If any provision of this regulation, or the application of the provision to any person or circumstance, is held invalid, the remainder of the regulation, and the application of the provision to persons or circumstances other than those to which it is held invalid, shall not be affected.